Aircraft Sensors Market Size, Share & Industry Analysis By Platform (Fixed-Wing Aircraft, Rotary Blade Aircraft, and UAV), By Sensor Type (Temperature, Pressure, Force, Speed, Torque, and Others), By Application (Engine Turbine & APU, Flight Control & Actuation, Landing Gear & Brakes and others), By Connectivity (Wired Sensors and Wireless Sensors), By End Use (OEMs and Aftermarket) and Regional Forecast, 2026-2034

Aircraft Sensors Market Size and Industry Overview

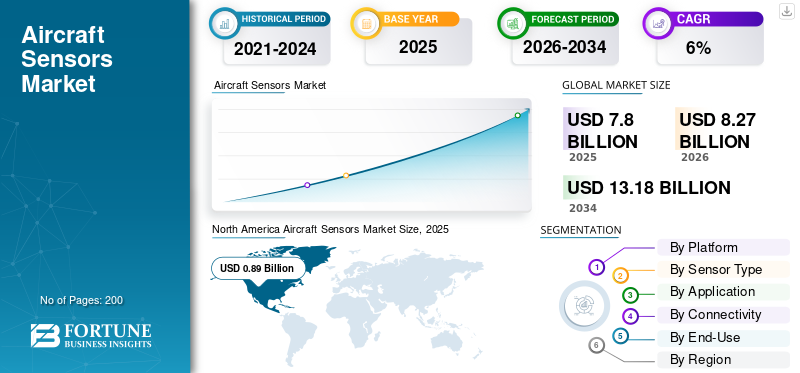

The global aircraft sensors market size was valued at USD 7.80 billion in 2025. The market is projected to grow from USD 8.27 billion in 2026 to USD 13.18 billion by 2034, exhibiting a CAGR of 6.00% during the forecast period. North America dominated the aircraft sensors market with a market share of 39.91% in 2025.

An aircraft sensor is a device that detects events or changes in its environment and transforms it into a signal which can be interpreted easily. Minor discrepancies in the aircraft can lead to severe catastrophes. The sensors integrated into the aircraft detect such irregular discrepancies and notifies the pilot. Such occurrences have initiated the demand for aircraft sensors in the aviation sector. Due to automation, the number of sensors in an aircraft is increasing, which increases the accuracy of the intended aircraft functions. The advances in microelectromechanical system (MEMS) technology have extensively impacted the global market. Moreover, the rising adoption of sensors in the unmanned aerial vehicles (UAVs) industry is foreseen to create several market opportunities in the coming years. Factors that are predicted to propel the growth of the market are the development of advanced sensors and the rise in the demand for wireless sensors for commercial and military purposes.

Download Free sample to learn more about this report.

GLOBAL AIRCRAFT SENSORS MARKET Snapshot & Highlights

Market Size & Forecast:

- 2026 Market Size: USD 8.27 billion

- 2034 Forecast Market Size: USD 13.18 billion

- CAGR: 6 % from 2026–2034

Market Share:

- North America dominated the aircraft sensors market with a 39.91% share in 2025, driven by the presence of major OEMs and sensor manufacturers, rising demand for technologically advanced aircraft, and increasing investments in next-gen defense aviation systems.

- By sensor type, temperature, pressure, and position sensors held the largest market share in 2019 and are expected to remain dominant through 2032 due to their critical roles in engine monitoring, flight control, and airframe operations.

Key Country Highlights:

- United States: Market growth is propelled by high defense budgets, rapid UAV development, and stringent FAA safety standards that encourage frequent sensor upgrades.

- China: Expanding aircraft fleet and increasing investments in civil aviation infrastructure fuel demand for new-generation aircraft sensors.

- India: Indigenous defense aircraft programs like Tejas and growing MRO activity are driving localized sensor integration.

- France: Home to global aerospace leaders like Safran and Thales, France benefits from robust aircraft sensor manufacturing and innovation capabilities.

- United Kingdom: Increasing focus on UAV development and collaborations in European defense programs support stable market growth.

Aircraft Sensors Market TRENDS

Download Free sample to learn more about this report.

High-tech Advancements In Micro-Electro-Mechanical-Systems (MEMS)

Micro-Electro-Mechanical-Systems (MEMS) are miniature devices, which incorporate actuators, sensors, and a processor or controller to form intelligent systems. The use of MEMS in aerospace applications enhances the performance and extends the lifetime with a low-cost, high-end functionality. MEMS has the potential to eradicate conventional flight control surfaces, enhance the performance of compressors and turbines, reduce drag, and enhance overall aerodynamic performance. It offers a major advantage in terms of size, weight, and cost as compared to conventional systems. The complete inertial and navigation units can be integrated into a single chip. The advancements in MEMS technology allows it to sustain in harsh environments such as high temperature, vibration, etc. The rise in demand for MEMS technology in the aviation industry will boost this market. North America witnessed aircraft sensors market growth from USD 0.85 Billion in 2018 to USD 0.89 Billion in 2019.

Wireless Sensing To Be The Future Of Digital Avionics

The conventional aircraft uses sensors that are connected through wired networks, which pose challenges such as cable routing, noise, added weight to the structure, and others. The usage of wireless sensors in aircraft has remarkable advantages in terms of flexibility in sensor configuration, design optimization, and weight optimization. The new aircraft are designed with the incorporation of wireless sensors. The main factor to use wireless sensors over the wired sensor is its low weight. The weight of aircraft electrical components, such as wires and cables, adds significantly to the overall weight of the aircraft. The OEMs are focused on reducing the weight of the aircraft to increase fuel efficiency, thus reducing the fuel cost, thus reducing the carbon emissions. Thus, the wireless sensors play a vital role in the advancement of the aviation industry.

Aircraft Sensors Market growth FACTORS

Rising Demand For UAV Will Aid Market Growth

UAVs utilize a wide range of sensors to improve the operation of the vehicle or to gather the data. Apart from conventional sensors such as flight control sensors, flow & level, temperature & pressure, and other UAVs use various advanced sensor technologies such as LIDAR sensors (Light Detection and Ranging), which are used for navigation and imaging purpose.

Rising adoption of UAVs in the military for Intelligence, Surveillance, and Reconnaissance (ISR) operations across the globe is expected to support aircraft sensors market growth. Moreover, the rise in the use of UAVs in life-threatening missions and growing demand for modern warfare techniques are also expected to fuel the growth of the market.

Furthermore, increasing the adoption of UAVs for civil and commercial operations such as agricultural activities, real estate, engineering, security, and others is anticipated to augment market growth.

Rise In Demand For Expansion Of Aircraft Fleet Across The Globe Will Boost The Market Growth

The increase in the financial condition of the middle classes in developing countries is the reason for the rise in air passenger traffic. As stated by Oliver Wyman, there were 27,492 aircraft across the globe, and it is anticipated to rise by 11,600 aircraft in the next ten years. This demand for new aircraft will, in turn, drive the aircraft sensors market. Moreover, increased investment in the aviation industry by emerging economies such as China and India is expected to fuel the market.

RESTRAINING FACTORS

Regulations By Aviation Safety Agencies Expected To Hinder The Market Growth

The aviation industry follows strict rules and regulations regarding the use of electronic components in use for the aviation industry. Manufacturers need to follow certain guidelines related to safety and design concerns regulated by the Federal Aviation Administration (FAA). Such regulations imposed by the FAA will hamper the growth of the market. For instance, in March 2020, the FAA proposed to fine the Boeing Company with USD 19.7 million for allegedly installing types of equipment containing sensors in 737 aircraft and 791 jetliners that had not been approved as compatible with the guidance systems.

Aircraft Sensors Market SEGMENTATION analysis

By Platform Analysis

Fixed-Wing Aircraft Segment Expected To Dominate the Global Market

Based on the platform, the aircraft sensors market is divided into fixed-wing aircraft, rotary-blade aircraft, and UAV segment. The fixed-wing aircraft segment is expected to be the largest segment owing to the rise in the global aircraft fleet. In contrast, the UAV segment is anticipated to be the fastest-growing segment due to the rising adoption of UAVs in the military for intelligence, surveillance, and reconnaissance (ISR) and combat application. The fixed-wing segment in this market is further divided into commercial aircraft and military aircraft. Owing to an increase in the number of aircraft deliveries and air passenger traffic, the demand for commercial aircraft is rising. Thus, the rise in demand for fixed-wing aircraft is anticipated to propel the growth of the market for aircraft sensors.

The rotary-blade segment is further classified into commercial helicopters and military helicopters. The military helicopter is anticipated to grow at a higher CAGR owing to rising modernization programs across the globe.

By Sensor Type Analysis

To know how our report can help streamline your business, Speak to Analyst

Temperature Sensor To Acquire Dominance In The Market

Based on sensor type, the aircraft sensors market is classified into temperature sensor, pressure sensor, force sensor, speed sensor, torque sensor, accelerometer sensor, flow sensor, position sensor, proximity sensor, GPS sensor, gyroscope, radar sensor, smoke detection sensor, angle of attack (AOA) sensor, level sensor, vibration sensor, airspeed & altitude sensor, and others. Position sensors, pressure sensors, and temperature sensors are predicted to dominate the market through the forecast period, owing to the rise in its use in flight control and cockpit control systems. These sensors are integrated into various parts of the aircraft, such as cabin, air ducts, brakes, turbines, hydraulic lines, and others. The rapid growth in the manufacturing of new aircraft is predicted to increase the use of temperature, pressure, and position sensors in the aircraft, thus propelling the market during the forecast period.

- The Temperature Sensor segment is expected to hold a 12.86% share in 2019.

By Application Analysis

Cockpit Control & Flight Control Segment Anticipated To Drive The Market Growth

Based on application, the market is segmented into engine turbine & auxiliary power unit (APU), flight controls & actuation, landing gear & brakes, environmental control system, doors & slides, cabin galley & cargo, and cockpit controls. The cockpit control and flight control & actuation system is predicted to continue to be the dominant application in the market during the forecast period, driven by rising aircraft deliveries, and increased integration of avionics in the next-generation aircraft. Engine, turbine & APU and landing gear & brakes segment is expected to grow during the forecast period, owing to increased maintenance due to increased flight hours of aircraft; thus, a rise in requirement for MRO. The cabin, galley & cargo segment is expected to play a vital role in market growth due to the rise in demand for passenger safety and environmental control.

By Connectivity Analysis

Wireless Sensors To Gain Supremacy In The Market

Based on connectivity, the aircraft sensors market is segmented into the wired sensor and wireless sensor. The wired sensor is expected to be the largest segment owing to its high reliability. The wireless sensor is anticipated to be the fastest-growing segment during the forecast period, owing to the rising demand for lightweight aircraft. Moreover, the wireless sensors have low installation and maintenance costs, which is expected to drive the market through the forecast period.

By End Use Analysis

OEM Will Endure Its Dominance Through The Forecast Period

Based on end-use, the market is divided into OEM and aftermarket. The OEM is anticipated to be the largest and fastest-growing segment through the forecast period, owing to the rise in demand for commercial airlines. Moreover, with the growing number of flight passengers, the manufacturing of commercial aircraft is increasing swiftly across the globe. The aftermarket segment is expected to witness a healthy growth owing to the increase in flight hours of aircraft. It is estimated that an electronic device must be replaced after 1000 flight hours. Hence, it creates a huge demand for the aftermarket as the sensors need to be replaced after specific flight hours. Moreover, the growing age of commercial aircraft will fuel the growth of the aftermarket segment.

REGIONAL INSIGHTS

North America Aircraft Sensors Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

The outcomes based on our research methodology indicate North America is anticipated to be the largest segment during the forecast period, as it is the manufacturing capital of the aerospace industry due to the presence of many aircraft OEMs and sensor manufacturers.

Asia Pacific

Asia Pacific is anticipated to grow at the highest CAGR during the forecast period owing to the rise of the aviation industry due to increasing air travel. Moreover, the growing demand for new aircraft deliveries boosts the demand for aircraft sensors. The developments in regional and commercial aircraft programs will result in the growth of the aircraft sensor market.

Europe

Europe is predicted to have healthy growth during the forecast period owing to a rise in investments for UAV developments. Moreover, increasing commercial applications of drones are fueling the market.

KEY INDUSTRY PLAYERS

Deep-Rooted Contracts With Government To Make The Raytheon Company A Leader In The Market

The competitive factors among the major players are technical and management capability, affordability, the ability to develop and execute complex integrated system architectures, and the ability to deliver solutions to the clients. Various contracts, partnerships, agreements, acquisitions, joint ventures, and new product launches are key strategies embraced by the key players in the aircraft sensors market.

List of Top Aircraft Sensors Companies:

- Honeywell International, Inc. (The U.S.)

- Ametek, Inc. (The U.S.)

- General Electric Company (The U.S.)

- Meggitt PLC (The U.K.)

- Safran S.A. (France)

- Woodward Inc. (The U.S.)

- Thales Group (France)

- Zodiac Aerospace (France)

- Curtiss-Wright Corporation (The U.S.)

- Schneider Electric SE (France)

- General Atomics Corporation (The U.S.)

- The Raytheon Company (The U.S.)

- TE Connectivity (Switzerland)

- Lockheed Martin Corporation (The U.S.)

KEY INDUSTRY DEVELOPMENTS:

- In May 2021, L3Harris Technologies was awarded a contract worth USD 96.4 million by the U.S. Special Operations Command (SOCOM) to modernize the forward-looking infrared systems on military-rotary wing aircraft. The SOCOM is expecting to invest USD 7.6 million in initial defense-wide funds to procure sensors and program management services.

- In March 2021, Teledyne Controls, LLC obtained FAA Supplemental Type Certification (STC) approval for installation of its new advanced Aircraft Cabin Environment Sensor (ACES) on Boeing 737 aircraft.

- In November 2020, General Atomics Aeronautical Systems, Inc. was awarded a contract worth USD 93.3 million by the Joint Artificial Intelligence Center (JAIC) to improve the autonomous sensing capabilities of unmanned aircraft.

REPORT COVERAGE

The aircraft sensors market research report provides a detailed analysis of the aviation sensors. It focuses on key aspects such as leading companies, sensors types, and applications of the aircraft sensors.

Besides this, the aircraft sensors report offers insights into the market trends, market dynamics, and highlights key aircraft sensors industry developments. In addition to the factors mentioned earlier, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021–2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021–2024 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Platform

|

|

By Sensor Type

|

|

|

By Application

|

|

|

By Connectivity

|

|

|

By End-Use

|

|

|

By Geography

|

Frequently Asked Questions

According to Fortune Business Insights, the global aircraft sensors market was valued at USD 8.27 billion in 2026 and is projected to reach USD 13.18 billion by 2034.

Growing at a CAGR of 6%, the market will exhibit steady growth in the forecast period (2026-2034).

The market growth is driven by the rising adoption of unmanned aerial vehicles (UAVs), increasing demand for wireless and MEMS-based sensors, expansion in aircraft fleets, and growing investments in next-generation avionics by OEMs and defense agencies.

North America dominates the aircraft sensors market due to the presence of major aircraft OEMs and sensor technology leaders. The region accounted for nearly 40% of the global market share in 2025.

Key sensor types include temperature sensors, pressure sensors, position sensors, gyroscopes, accelerometers, radar sensors, and angle of attack (AOA) sensors, with temperature and pressure sensors witnessing the highest adoption.

MEMS (Micro-Electro-Mechanical Systems) technology is revolutionizing aircraft sensors by offering miniaturized, lightweight, and low-cost components that can withstand harsh environments and enhance flight control, navigation, and engine monitoring.

Wireless sensors are emerging as a game changer in aviation due to their lightweight, low maintenance, and ability to reduce wiring complexity, thereby improving fuel efficiency and design flexibility in both commercial and military aircraft.

The fixed-wing aircraft segment, particularly commercial aircraft, is expected to lead in demand for sensors due to increasing global passenger traffic and aircraft deliveries. However, UAVs are projected to show the fastest growth rate.

Key challenges include strict regulatory compliance from aviation safety authorities like the FAA, high development costs, and delays in aircraft manufacturing, especially during global disruptions like the COVID-19 pandemic.

Major players include Honeywell International Inc., Raytheon Technologies, General Electric, Safran S.A., Thales Group, Meggitt PLC, and TE Connectivity, all of whom focus on innovation, government contracts, and M&A to strengthen market presence.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us