Connected Car Market Size, Share & Industry Analysis, By Application Type (Mobility Management, Telematics, Infotainment, and Driver Assistance), By Network Type (3G, 4G, 5G, and Satellite), By Technology Type (Embedded, Tethered, and Integrated), By Sales Channel Type (OEM and Aftermarket), By Communication Type (Vehicle to Vehicle and Vehicle to Infrastructure) and Regional Forecasts, 2026-2034

KEY MARKET INSIGHTS

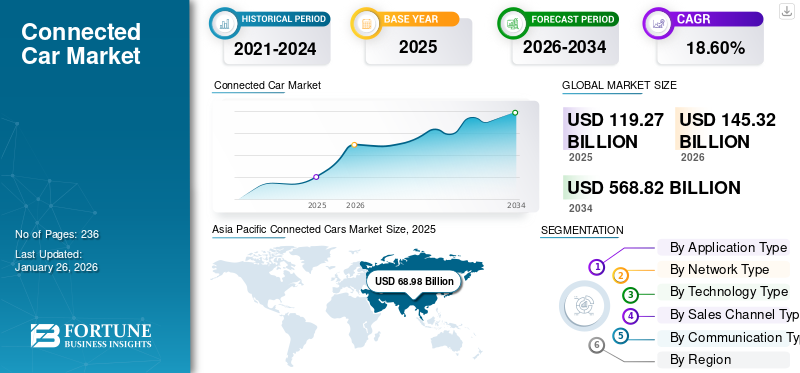

The connected car market size was valued at USD 119.27 billion in 2025. The market is expected to grow from USD 145.32 billion in 2026 to USD 568.82 billion by 2034, exhibiting a CAGR of 18.60% during the forecast period. Asia Pacific dominated the global connected car market with a share of 57.83% in 2025.

A connected car has hardware and software to communicate bidirectionally with external systems, such as the Internet, other vehicles, infrastructure, or mobile devices. This connectivity allows services such as real‑time navigation, remote diagnostics, over‑the‑air software updates, in‑car entertainment, emergency response, vehicle‑to‑vehicle (V2V) or vehicle‑to‑infrastructure (V2I) coordination, and data‑driven analytics. Built‑in GSM/4G/5G modules or aftermarket dongles are used to facilitate this communication. These vehicles support safety, convenience, and smart mobility features, and increasingly form the foundation of autonomous driving platforms and IoT ecosystems within modern transportation.

The global market spans a complex ecosystem of automotive OEMs, technology firms, telecommunication providers, and suppliers, collaborating on infotainment, telematics, ADAS, V2X communications, and vehicle management systems.

Leading automakers such as General Motors (OnStar), Ford (SYNC / FordPass), BMW (ConnectedDrive), Mercedes‑Benz, Toyota, Volkswagen, Audi, and Tesla integrate embedded connectivity in their models. Technology giants including Apple (CarPlay, Project Titan), Google (Android Auto/Android Automotive), Microsoft, and semiconductor firms such as NXP, Qualcomm, NVIDIA, Bosch, Continental, and Aptiv provide the hardware, software, and platforms that enable robust connectivity solutions. Telecommunications operators such as Vodafone, Verizon, and AT&T also play a key role by supporting real‑time data transfer and emerging 5G‑based services.

The COVID‑19 pandemic significantly disrupted the global industry due to lockdown-induced shutdowns in automotive manufacturing and supply chain delays, especially in sourcing electronic modules and telematics hardware. Consumers also deferred new vehicle purchases amid economic uncertainty, dampening the adoption of advanced connected technologies. Joint projects between OEMs, tech providers, and service firms were delayed or paused, slowing deployment of new connectivity services. However, as production restarted and demand recovered, the need for remote vehicle diagnostics, contactless services, and smart mobility tools accelerated renewed interest in connected offerings. Government stimuli measures and infrastructure investments further supported momentum in digital automotive ecosystems post‑2020.

Download Free sample to learn more about this report.

Connected Car Market Trends

Integration of Artificial Intelligence (AI) and Machine Learning (ML) to Enhance Car Capabilities Boosts Market Growth

The automotive industry is experiencing a shift toward intelligent vehicles, with the utilization of AI and ML enhancing the capabilities of connected cars by enabling them to learn, adapt, and make real-time decisions based on dynamic driving conditions. This trend is improving safety and convenience features while driving the development of autonomous vehicles that can operate without human intervention.

AI and ML play a crucial role in the evolution of ADAS, including systems such as adaptive cruise control, lane-keeping assist, automatic emergency braking, and collision avoidance. These technologies rely on real-time data from a combination of sensors, cameras, and radars, which AI algorithms process to identify potential hazards and determine vehicle actions. Tesla's Autopilot system is a prime example of AI integration in ADAS, using deep learning algorithms to process road data and enhance driving automation. As of 2024, Tesla's Full Self-Driving (FSD) system incorporates ML models to continuously improve driving decision-making and route planning, building on years of AI-driven data training.

The trend toward autonomous driving is closely tied to the growing importance of AI-powered connected cars. Waymo, the self-driving car subsidiary of Alphabet, has pioneered the autonomous driving space, utilizing AI and ML to process vast amounts of data collected from Lidar, cameras, and other sensors. Waymo's fleet of autonomous cars is already operating in parts of Phoenix, with expansion plans underway, showcasing the potential of AI in achieving Level 4 and Level 5 autonomy, where human intervention is no longer necessary.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Increasing Demand for Autonomous Vehicles and Advanced Driver-Assistance Systems is Propelling Market Growth

With the automotive industry witnessing a transformative shift toward autonomous mobility, connected cars are increasingly equipped with intelligent technologies that enhance safety, efficiency, and convenience for drivers and passengers. ADAS technologies such as lane-keeping assistance, adaptive cruise control, automatic emergency braking, and traffic sign recognition are now standard features in many new vehicle models. These systems rely heavily on real-time data exchange, which is facilitated by connected car technology, making vehicles smarter and more capable of responding to dynamic driving conditions.

Growth in this sector is directly linked to the increasing adoption of connected car technologies that provide the necessary infrastructure for these systems to operate efficiently. For instance, automakers such as Tesla, Waymo (Google's self-driving unit), and General Motors already incorporate advanced ADAS features into their vehicles, relying on real-time connectivity to enable autonomous capabilities such as self-parking, automated highway driving, and collision avoidance.

The U.S. National Highway Traffic Safety Administration (NHTSA) has also contributed to the advancement of vehicle safety through regulatory frameworks mandating certain ADAS technologies. In 2022, NHTSA proposed rules for vehicle-to-everything (V2X) communication, enabling vehicles to communicate with infrastructure and other vehicles to enhance safety and traffic flow. The regulatory push for safer vehicles and the rising consumer preference for cars with driver assistance features propel automakers to incorporate more connected and autonomous capabilities in their offerings.

OEMs such as Mercedes-Benz, Audi, and BMW have committed significant investments to autonomous driving technologies, integrating connectivity solutions that support ADAS features such as hands-free driving and remote software updates. These efforts have developed Level 3 autonomous vehicles, already been tested on certain regions' public roads. As regulatory standards evolve and consumer confidence in autonomous systems grows, the market is set to expand exponentially, with connected cars becoming integral to the advancement of autonomous driving technologies.

Market Restraints

Increasing Concerns Around Data Security and Privacy to Restrain Market Development

As vehicles become more connected, they generate vast amounts of data vulnerable to cyberattacks, breaches, and unauthorized access. This issue is particularly critical as connected cars rely on exchanging real-time information, such as vehicle diagnostics, driver behavior, location data, and personal preferences. With growing concerns over data misuse and privacy violations, consumers and regulatory bodies scrutinize how OEMs (Original Equipment Manufacturers) and service providers handle this sensitive information.

According to a 2023 European Union Agency for Cybersecurity (ENISA) survey, the automotive industry is increasingly becoming a target for cyberattacks, with connected vehicles vulnerable to remote hacking attempts. The 2022 Cybersecurity Report by NHTSA (National Highway Traffic Safety Administration) highlighted that around 70% of connected car systems contained vulnerabilities that could potentially be exploited by hackers, posing risk of remote vehicle control, data theft, and vehicle disruption. These vulnerabilities have raised alarms among consumers, leading to hesitancy in adopting connected car technologies, especially in regions such as Europe and North America, where data protection laws such as the GDPR (General Data Protection Regulation) impose stringent requirements on data handling and storage requirements.

OEMs face significant challenges in ensuring that data shared between vehicles and external networks (such as cloud services) is encrypted and safeguarded from unauthorized access. Automakers including BMW, Audi, and Ford have been actively investing in improving the cybersecurity of their connected vehicles through initiatives such as security testing, end-to-end data encryption, and the implementation of firewalls.

Market Opportunities

Expansion of Over-the-Air (OTA) Software Updates and Vehicle Personalization to Present Significant Growth Opportunities

A significant opportunity driving the growth of the global market is the expansion of over-the-air (OTA) software updates and the increasing demand for vehicle personalization. As automakers integrate more connected technologies, the ability to deliver continuous improvements through remote software updates is becoming a key competitive differentiator. OTA updates allow automakers to push new software to vehicles without requiring drivers to visit service centers, providing consumers with convenience, cost savings, and faster access to the latest features.

The rise of OTA updates in the automotive sector transforms how consumers interact with their vehicles. Instead of waiting for an in-person service visit, car owners can now receive real-time updates for vehicle diagnostics, infotainment systems, driver-assistance features, and even autonomous driving software. This technology also opens new revenue streams for OEMs, allowing them to offer subscriptions for premium features, access to advanced functionalities, and software-based upgrades traditionally tied to hardware upgrades.

In 2023, Tesla led the charge in leveraging OTA updates, continuously enhancing its autopilot system, battery management features, and infotainment options. Tesla's ability to push software updates to over 1 million vehicles globally within hours demonstrates the immense potential of OTA technology in providing both consumer convenience and OEM cost savings.

SEGMENTATION Analysis

By Application Type

Driver Assistance Segment to Dominate the Market due to Proven Safety Benefits

As per application type, the market is divided into mobility management, telematics, infotainment, and driver assistance. The driver assistance segment is projected to dominate the market with a share of 36.13% in 2026. An advanced driver assistance system consists of technologically advanced features such as adaptive cruise control, lane keep assist, 360 view camera, and park assist that enhance the vehicle's safety. Various governments across the globe have imposed stringent safety norms on automotive manufacturers. In May 2023, the National Highway Traffic Safety Administration (NHTSA) announced that the inclusion of both AEB and pedestrian AEB (PAEB) in its two main programs for increasing vehicle safety: the New Car Assessment Program (NCAP) and a Federal Motor Vehicle Safety Standard (FMVSS) regulation. The decision was driven by AEB's potential to prevent fatalities and mitigate a large number of non-fatal injuries.

The mobility management segment holds the second-largest position in the market. This system enables driver reach their destination safely, in the shortest time, and with optimal fuel efficiency. It also offers vital information such as extreme weather alerts, road conditions, and real-time alternative routes to avoid external hazards, ensuring a superior driving experience.

The telematics segment is anticipated to achieve considerable growth during the steady period. The increasing IT infrastructure along highways that can seamlessly connect to mobile networks is expected to drive the demand for connected telematics solutions.

The infotainment segment is also expected to grow well over the forecast period. In recent years, infotainment systems have become one of the most vital components of vehicles. As a result, automakers are increasingly installing infotainment features such as Wi-Fi hotspots, social media access, smartphone interfaces, and advanced mobile office platforms in their products to enhance user experience.

To know how our report can help streamline your business, Speak to Analyst

By Technology Type

Integrated Segment to Lead due to its Cost-effectiveness

The market is segmented into embedded, tethered, and integrated systems based on technology type. The integrated segment is expected to dominate the market over the forecast period. These systems provide unlimited data-sharing capabilities and are more cost-effective compared to embedded and tethered systems. Key OEMs across the globe have partnered with various key players to develop advanced integrated systems for connected vehicles that provide seamless connectivity to consumers. For example, Ford partnered with Geotab to develop a telematics solution for Ford vehicles.

The embedded segment is expected to lead the market, contributing 64.02% globally in 2026. The embedded segment is expected to occupy the second-largest market. Factors such as cost optimization of service plans, cloud services, and governmental regulations are expected to strengthen its position. In addition, key features such as remote diagnostics and eCall systems rely on embedded system, making it indispensable. Hence, the rising adoption of embedded systems is expected to fuel the adoption of connected vehicles over the forecast period.

By Network Type Analysis

5G Segment to Lead the Market due to Enhanced Safety Potential

Based on network type, the market is segmented into 3G, 4G, 5G, and satellite. The 5G segment is anticipated to dominate the market during the forecast period. Several telecommunication companies are developing advanced 5G networks for better communication between connected vehicles and external devices. According to the 5G Automotive Association, more than 60% of road accidents can be avoided with the help of seamless 5G network. In February 2024, Cisco and TELUS introduced 5G capabilities in North America, focusing on IoT applications for connected cars. TELUS planned to onboard 1.5 million 5G standalone cars onto Cisco's IoT Control Center, starting in 2024, enhancing driver experience and enabling new revenue streams for car manufacturers. The 4G segment will account for 78.73% market share in 2026.

The satellite segment is expected to be the fastest-growing over the forecast period. Cellular and Wi-Fi networks support connected vehicles only in areas where mobile towers are present, primarily urban areas. Once the vehicle moves beyond tower coverage, the network gets completely cut off, which may cause serious problems for the occupants in the connected vehicles. Various automotive OEMs, satellite operators, and mobile operators focus on developing hybrid satellite-terrestrial networks to overcome this problem, which would offer uninterrupted connectivity. Hence, the increasing demand for satellite and 5G networks is expected to drive the industry.

By Sales Channel Type

OEM Segment Captures the Largest Market Share due to Technological Advancements

Based on sales channel, the market is segmented into OEM and aftermarket. The OEM segment is expected to account for 36.47% of the market in 2026. Increasing technological developments such as uninterrupted connectivity, enhanced cybersecurity, and the development of driverless vehicles integrated with highly secure software are anticipated to aid the dominance of OEMs during the forecast period. In addition, increasing partnerships with key players to develop high-quality and cost-effective components are another reason fueling the OEM segment's growth.

The aftermarket segment is expected to grow faster throughout the period due to increasing penetration of connected cars and the demand for technological services. As the demand for affordable connectivity rises, aftermarket solutions provide better access, allowing a wider consumers base to experience the benefits of connected car technologies.

By Communication Type

Vehicle 2 Vehicle Segment to Lead due to its Ability to Improve Passenger Comfort

The market is categorized into Vehicle to Vehicle (V2V) and Vehicle to Infrastructure (V2I) based on communication type. The V2V segment is expected to dominate the market over the forecast period. Vehicle-to-vehicle communication helps reduce traffic congestion in large cities, enhances road safety, and improve the comfort of the occupants. Developments in wireless technologies and the increasing usage of advanced equipment such as sensors and GPS in V2V systems are anticipated to maintain the segment's dominance over the forecast period.

The Vehicle to Infrastructure segment is expected to experience higher growth during the forecast period. Increasing government initiatives to develop V2I frameworks are ensuring the stable growth of the segment in the market. As more cities adopt connected infrastructure, V2I technology will become integral to improving urban mobility by enabling smoother traffic flow, reducing emissions, and enhancing overall transportation efficiency, thereby fueling connected car market growth.

CONNECTED CAR MARKET REGIONAL OUTLOOK

The market is segmented based on region: North America, Europe, Asia Pacific, and the Rest of the World.

Asia Pacific Connected Cars Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

In 2025, the Asia Pacific market stood at USD 68.98 billion, representing 57.83% of global demand, and is projected to grow to USD 83.84 billion in 2026. In addition, spurring consumer demand for in-vehicle embedded connectivity systems and the increasing shift toward connected vehicles have propelled the growth of the market in this region. The Japan market is projected to reach USD 16.11 billion by 2026, the China market is projected to reach USD 52.21 billion by 2026, and the India market is projected to reach USD 6.41 billion by 2026.

Europe

Europe contributed approximately USD 35.46 billion to the global market in 2025, accounting for 29.73% share, and is expected to reach USD 43.52 billion in 2026. Europe is expected to be the second-largest market. Consumers in Europe increasingly demand vehicles equipped with advanced connectivity features for enhanced safety, convenience, and entertainment. Features such as in-car Wi-Fi, real-time traffic updates, remote diagnostics, and smartphone integration are becoming more popular among European drivers. In October 2023, Yahoo partners with Xperi to deliver in-car video to BMW drivers, featuring Yahoo Finance, Yahoo Sports, and In the Know, through Xperi's TiVo-powered DTS AutoStage service. This followed BMW's earlier collaboration with Meta on integrating AR and VR solutions into vehicles, further highlighting region’s focus on product innovation. The UK market is projected to reach USD 4.41 billion by 2026, while the Germany market is projected to reach USD 14.51 billion by 2026.

North America

The market in North America reached USD 9.58 billion in 2025, representing 8.03% of total market revenue, and is projected to reach USD 11.63 billion in 2026. North America is expected to grow steadily in the market over the forecast period, supported by the growing adoption of advanced technologies such as 5G connectivity. The U.S. market is projected to reach USD 9.47 billion by 2026.

Rest of the World

Rest of the World recorded a market size of USD 5.26 billion in 2025, capturing 4.41% of the global market share, and is projected to reach USD 6.34 billion in 2026. In the Rest of the World (RoW), the market is growing steadily, driven by increasing urbanization and the demand for modern mobility solutions in emerging markets such as Brazil and South Africa.

Competitive Landscape

KEY INDUSTRY PLAYERS

Key Players Focus on Product Development to Enhance their Product Portfiolio

Harman International pioneered automotive connectivity through its comprehensive portfolio of infotainment, ADAS, and audio solutions for connected vehicles. Its Harman's Harman Ignite platform serves as a cloud-based ecosystem that enables seamless integration with mobile devices, voice recognition, and over-the-air updates, offering real-time connectivity to vehicles. Its in-car audio systems, such as JBL and Harman Kardon, deliver immersive sound experiences, further enhancing the driving experience.

Continental AG is another major player in the connected car market, offering various technologies in infotainment, ADAS, and vehicle-to-everything (V2X) communication. Continental's Continental Connected platform integrates cloud-based services such as OTA updates and real-time traffic data, making vehicles smarter and more efficient. The company's infotainment systems enable seamless connectivity with mobile devices, supporting navigation, voice control, and hands-free communications. Additionally, its electric mobility and autonomous driving investment positions it as a front-runner in developing future-ready connected vehicles.

LIST OF KEY CONNECTED CAR COMPANIES PROFILED

- Harman International (U.S.)

- Continental AG (Germany)

- AT&T (U.S.)

- Robert Bosch GmbH (Germany)

- Daimler AG (Germany)

- Audi (Germany)

- TomTom Inc. (Netherlands)

- General Motors (U.S.)

- Ford Motor Company (U.S.)

- HYUNDAI MOTOR GROUP (South Korea)

- Volvo (Sweden)

KEY INDUSTRY DEVELOPMENTS

- In July 2025, Tata Elxsi proposed a strategic partnership with Telecom Operators to integrate its indigenous connected vehicle platform, TETHER AUTO, with telco networks by leveraging the CAMARA network APIs. This collaboration aims to enhance services for automotive customers and create new revenue streams for Telecom Operators and Automakers.

- In June 2025, Oppo signed a global patent licensing deal with Volkswagen for connected car technologies. By incorporating OPPO's cellular solutions, Volkswagen seeks to improve connectivity features, aligning with the growing demand for advanced in-car communication systems.

- In May 2025, LG showcased its Satellite-Based Next-Gen Connected Car Solution at the 2025 5GAA Conference. Company Demonstrated Satellite-Based Voice Communication from a Moving Vehicle, pioneering the future of safe and connected mobility.

- In March 2024, Vero and Privacy4Cars joined forces to offer privacy tools and identity protection services tailored for connected car owners. Their collaborative solution, Identi-FI, ensure secure data deletion from connected cars and offers recovery assistance in identity theft cases.

- In January 2024 - Hyundai and Kia partnered with Samsung Electronics for Car-to-Home and Home-to-Car services, enabling seamless connectivity between residential and mobility spaces. Customers can remotely control appliances from cars and vice versa via in-car infotainment systems and AI speakers, TVs, and smartphone apps. This integration utilizes Hyundai and Kia's connected car services with Samsung's SmartThings IoT platform, promising uninterrupted connectivity experiences in daily life.

REPORT COVERAGE

The global market analysis provides detailed market report analysis and focuses on key aspects such as leading companies, product types, and leading product applications. Besides this, the report offers insights into the current market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that have contributed to the market's growth over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 18.60% from 2026 to 2034 |

|

Unit |

Value (USD billion) & Volume (Million units) |

|

Segmentation |

By Application Type

|

|

By Network Type

|

|

|

By Technology Type

|

|

|

By Sales Channel Type

|

|

|

By Communication Type

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 145.32 billion in 2026 and is projected to reach USD 568.82 billion by 2034.

In 2025, the Asia Pacific market size stood at USD 68.98 billion.

The market is projected to grow at a CAGR of 18.60% and exhibit excellent growth during the forecast period (2026-2034).

By technology type, integrated segment is expected to lead the market during the forecast period.

The increasing adoption of advanced driver assistance systems is a key factor driving the global market.

Harman International is the leading player in the global market.

Asia Pacific dominated the global connected car market with a share of 57.83% in 2025.

The rising adoption of 5G connectivity is expected to drive the adoption of connected vehicles.

- 2021-2034

- 2025

- 2021-2024

- 236

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us