Subsea Power Cable Market Size, Share & Industry Analysis, By Cable Type (Single-core and Multi-core), By Voltage Type (Medium Voltage and High Voltage), By Conductor Type (Copper and Aluminum), By Application (Wind Power Generation, Oil & Gas, and Remote Areas), and Regional Forecast, 2024-2032

KEY MARKET INSIGHTS

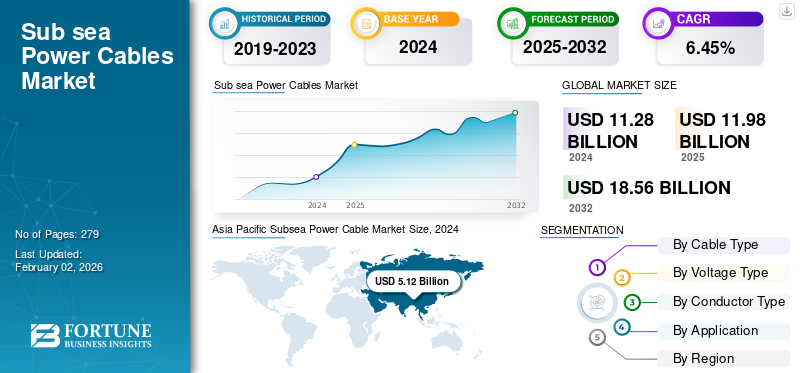

The global subsea power cable market size was valued at USD 11.28 billion in 2024. The global market is projected to grow from USD 11.98 billion in 2025 to USD 18.56 billion by 2032, exhibiting a CAGR of 6.45% during the forecast period.

Subsea power cable, or submarine cable, is a durable fiber optic cable that traverses the ocean floor between land-based stations to carry telecommunications signals. Factors such as enhancing grid stability, climate resilience, and offshore oil and gas facility electrification are driving demand.

Prysmian Group is a global market leader. It specializes in designing, manufacturing, and installing cables and systems, including high-voltage submarine power cables. With a global presence and a long history in the cabling industry, the company has successfully undertaken several submarine power cable projects.

Download Free sample to learn more about this report.

Subsea Power Cable Market KEY TAKEAWAYS

- 2024 Market Size: USD 11.28 billion

- 2025 Market Size: USD 11.98 billion

- 2032 Forecast Market Size: USD 18.56 billion

- CAGR: 6.45% from 2025–2032

- Asia Pacific dominated the subsea power cable market with a 45.42% share in 2024.

- The single-core segment accounted for the largest market share of 68.78%.

- The high-voltage segment held the largest market share of 71.81%.

Asia Pacific

Asia Pacific reached USD 5.12 billion in 2024, driven by offshore wind projects and expanding cross-border power connectivity.

North America

North America is projected to reach USD 0.91 billion in 2025, supported by offshore renewable energy and grid modernization.

Europe

Europe is projected to reach USD 5.08 billion in 2025, driven by offshore wind expansion and renewable energy integration.

U.S.

The U.S. market is projected to reach USD 0.84 billion in 2025, supported by offshore wind targets and investments in subsea transmission infrastructure.

Japan

Japan is witnessing steady market growth, supported by rising offshore wind development and investments in high-capacity power transmission.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Enhancing Grid Stability and Climate Resilience Driving Market Growth

The subsea cable project ensures a more stable power supply and is part of a broader strategy to strengthen many countries’ energy infrastructure against climate-related disruptions. As many regions are increasingly affected by severe weather events, strengthening grid interconnections will improve grid stability and mitigate the risks associated with isolated power generation systems. The offshore projects are aligned with many nations' long-term energy strategy by reducing dependence on local, fossil energy sources. The initiative intends to provide cost savings for residential and commercial consumers while promoting economic development in the many regions.

As renewable energy, especially offshore wind power generation, continues to scale globally, robust subsea transmission infrastructure is critical. This makes subsea power cables a foundational enabler in the global energy transition. These cables connect different regions and form the foundation of the global energy system. They also enable offshore energy generation by transmitting electricity between power grids and offshore energy sources, such as offshore wind farms. For instance, in June 2025, Danish power cable maker and services provider NKT ordered OSBIT, a U.K.-based original equipment supplier, to design and build the NKT T3600 to become the world’s most powerful subsea trencher. To meet the growing demand for high-voltage power cables required for renewable energy, NKT is investing in manufacturing and installation capabilities, comprising the NKT Eleonora, a new cable lay vessel that can lay weighty and longer-length power cables.

Electrification of Offshore Oil and Gas Facilities to Boost Market Growth

Traditionally, offshore platforms rely on gas or diesel turbines, emitting CO2 and NOx. Subsea cables from shore power can slash CO2 emissions by 90%, eliminating hundreds of thousands of tons annually per platform. The Utsira High Power Hub Project in Norway has constantly increased the power from shore capabilities during the last decade to lower the carbon emissions from the offshore operations.

The Utsira High area, located 160 km off the coast of Stavanger, collects six offshore energy production fields on the Norwegian continental shelf. With the development and addition of platforms, the objective has been to electrify operations. By substituting fossil-fueled generators with power from shore electrical power cable systems, operating the connected platforms utilizing renewable energy transmitted from the onshore grid is now possible. This has permitted a remarkable reduction in greenhouse gas emissions and paved the way for achieving climate ambitions, including the goal for net zero emissions by 2050. Powering offshore platforms with shore cables is also considered safer and more energy-efficient.

MARKET RESTRAINTS

High Installation, Maintenance Costs, and Lack of Maritime Security Might Limit Market Growth

The market faces a significant restraint in the form of high installation and maintenance costs. These cables require specialized equipment, vessels, and skilled personnel for deployment in challenging underwater environments. Installing cables at great depths or across long distances often involves advanced cable-laying ships, subsea trenching and burial systems, and cable protection structures. Such operations are capital-intensive and can cost several million dollars per kilometer, especially in deep water or high-voltage projects.

In addition, the lack of maritime security is an important factor in the market growth. For instance, according to the Observer Research Foundation, in February 2024, Houthi missiles sank a British bulk carrier, the Rubymar, that was carrying around 41,000 tons of inflammable fertilizer. The sinking of the ship caused a 38 km wide oil spill. Several media reports noted that the ship's anchor dragged along the seabed, damaging four submarine cables. Of the 28 countries affected by the damage to the four submarine cables, 17 are African countries, which have struggled with digital connectivity issues. Around 100 million people in over a dozen West and North African countries were affected, including Ghana, Liberia, and Côte d'Ivoire, which experienced internet outages lasting seven to ten days.

MARKET OPPORTUNITIES

Rising Traction for Interconnection Projects/HVDC links in Developing Regions is Expected to Offer Lucrative Opportunities

Major Asian Pacific countries are expected to develop interconnection projects, High-Voltage Direct Current (HVDC) links, to enhance their energy systems by improving dependability, enhancing efficiency, and easing the merger of renewable energy sources such as offshore wind. HVDC technology is specifically advantageous for long-distance power transmission and can assist in creating a more robust and interconnected energy grid. The subsea power cables market might grow as the Asian continent is a group of emerging economies, and the HVDC link/ interconnection projects might foster a more integrated Asian Energy Market. The HVDC link eases the interconnection of different nations' grids, sharing electricity and resources between nations.

For instance, some initiatives, such as the India-Middle East-Europe Economic Corridor (IMEC), might act as growth factors for the stakeholders active in the market. As per the Press Information Bureau (PIB) of the Government of India, the IMEC corridor would comprise railways, roadways, energy pipelines, and clean energy infrastructure, including undersea cables. India is already in discussions with Singapore on clean energy transmission.

MARKET CHALLENGES

Environmental & Regulatory Standards Expected to Challenge Market Expansion

Managing complicated and frequently drawn-out environmental rules and approval procedures for subsea cable projects is a major and increasing challenge. Underwater infrastructure, fisheries, and marine ecosystems can all be impacted by installing cables over large seabed areas. Numerous permits from different national and international organizations, public consultations, and thorough environmental impact assessments are necessary due to concerns about electromagnetic fields, sediment disturbance, noise pollution during installation, and the possible disruption of sensitive habitats.

Project delays and higher planning expenses are common outcomes of these regulatory restrictions, which can even call for route modifications or technical advancements to lessen environmental effects. The requirement to strike a balance between the expansion of energy infrastructure and marine conservation adds a layer of complexity and risk. This factor makes project deadlines uncertain and necessitates a large upfront investment in environmental assessments and stakeholder management.

SUBSEA POWER CABLE MARKET TRENDS

Increase in Offshore Wind Farm Connectivity is one of the Latest Trends

The demand for subsea cables is mostly driven by the global push for renewable energy, especially offshore wind. High-capacity subsea cables are required to transfer the generated power back to mainland grids due to the development of enormous offshore wind farms farther from the coast as nations seek to lower carbon emissions and improve energy security. A steady and expanding pipeline of significant subsea cable projects is being created by this trend, which uses alternating current (AC) and high-voltage direct current (HVDC) cables depending on the distance and power capacity.

For instance, in November 2024, TechnipFMC and Prysmian declared that the two companies had signed a partnership agreement further to increase the growth of offshore wind to help meet increasing demand for renewable electricity. The partnership agreement brings together the technologies and capabilities of these two offshore industry leaders, offering the distinctive capabilities to develop a complete water column solution, from seabed to ocean surface. The collaboration will strengthen the exceptional skill of TechnipFMC’s system design and integration abilities in dynamic offshore applications with Prysmian’s worldwide leadership in producing and installing submarine power cable systems.

Download Free sample to learn more about this report.

IMPACT OF TARIFFS

Tariffs' impact on the subsea cable industry can be restrictive and catalytic depending on the region and market conditions. USA tariffs on Chinese cable imports led to the expansion of local cable manufacturing and support for domestic HVDC projects. Europe is imposing duties on non-EU suppliers to protect Nexans, NKT, and Prysmian, leading to stronger EU cable industry dominance. Due to budget overruns, developers delay or scale back offshore wind and interconnection projects. Tariffs on key components, e.g., from China, lead to material shortages and longer lead times. Tariffs affect global cable flow, complicating procurement from key manufacturing hubs such as China, South Korea. “Make in India” and high import duties encourage domestic cable production for offshore wind and interconnectors in India.

SEGMENTATION ANALYSIS

By Cable Type

Single-core Cable Dominates Market Due to Feasibility for Long-Distance Transmission

Based on cable type, the market is segmented into single-core and multi-core.

The single-core accounts for the largest market share of 68.78%. The single-core segment is preferred for high voltage and extra high voltage transmission, essential in offshore wind farms and long-distance subsea transmission. They allow for better heat dissipation, critical in high-capacity power transmission. Each turbine typically connects via single-core cables in a bundled configuration for export lines such as HVAC or HVDC.

Multi-core subsea power cable is anticipated to grow at a highest CAGR of 7.43% in the coming year due to the increasing demand for compact, cost-effective power transmission solutions in offshore and underwater infrastructure projects. These cables are particularly suited for medium voltage applications, inter-array connections, and space-constrained environments.

By Voltage Type

High Voltage Cable Dominates Market Due to Application in High-Capacity Transmission Projects

Based on the voltage type, the market is segmented into medium-voltage and high-voltage.

The high voltage segment accounted for the largest market share of 71.81%. The high voltage subsea cable market is growing due to the global shift toward offshore renewable energy, international power connections, and the electrification of offshore infrastructure. These cables are important for efficient long-distance, high-capacity transmission under the sea. High-voltage subsea cables are critical for exporting power from offshore wind farms, especially beyond 50 Km from shore to onshore grids. Commonly utilized in both HVAC and HVDC configurations.

The medium voltage subsea cable market is growing at a CAGR of 6.31% primarily due to the expansion of offshore renewable energy, nearshore electrification projects, and rising demand for efficient power transmission between offshore units and substations. These cables, typically between 6 KV and 66 KV, effectively connect distributed systems in marine environments.

By Conductor Type

Copper Conductor Dominates Market Due to High Electrical Conductivity

Based on conductor type, the market is segmented into copper and aluminum.

The copper segment holds the largest share of 71.33%. The copper subsea power cable is growing due to its excellent electrical conductivity, durability in harsh marine environments, and continued use in short to medium distance subsea power transmission. Copper cables remain a preferred choice in several applications as offshore infrastructure expands.

Aluminum subsea power cable is growing at a CAGR of 6.30% as aluminum is significantly cheaper than copper, making it an attractive option for utility-scale projects such as offshore wind farms and subsea interconnectors. Ideal for projects where budget and large volume installations are key considerations.

By Application

To know how our report can help streamline your business, Speak to Analyst

Wind Power Generation Dominates Market Due to Expanding Wind Power Projects

Based on application, the market is segmented into wind power generation, oil and gas, and remote areas.

The wind power generation segment holds the largest subsea power cable market share of 58.88%. The market for wind power generation is growing rapidly due to the global expansion of offshore wind farms, which require reliable underwater cables to transmit electricity from turbines to shore. These cables are critical infrastructure for inter-array connections and export transmission systems in offshore wind projects.

The oil and gas segment is growing at a CAGR of 4.43% due to the industry’s push for electrification of offshore operations, improved efficiency, and carbon emission reduction. Subsea power cables are increasingly used to supply electricity from onshore grids to offshore platforms and subsea production systems, replacing traditional onboard diesel or gas turbines.

Cables from nearby urban areas or renewable energy zones (Remote Areas) bring a consistent power supply. For example, Subsea cables in Alaska and Northern Canada connect remote communities to larger grids.

SUBSEA POWER CABLE MARKET REGIONAL OUTLOOK

The market has been studied regionally across five main regions: North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Asia Pacific dominates the market due to increasing energy security projects in island countries and energy demands.

Asia Pacific

Asia Pacific Subsea Power Cable Market Size, 2024 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific held the dominant share in 2024, valued at USD 5.12 billion, and also took the leading share in 2024 with 45.42%. In the Asia Pacific, projects such as the ASEAN power grid aim to interconnect Southeast Asia for energy security and trading surpluses across nations. Inter-country and island nations rely on subsea cables to link to mainland grids. Subsea cables support offshore platforms, providing stable power for drilling and processing, thus meeting the growth in oil and gas activity in nations such as Malaysia and Indonesia. Advances in HVDC, insulation materials, and cable laying technologies have enabled subsea installations. These innovations help reduce costs, increase lifespan, and bolster confidence in large-scale deployment.

In March 2025, China revealed an influential deep-sea cable cutter that could reset the world order. After scientists revealed a device that can disconnect undersea cables, Beijing now has the power to disrupt global communications. China unveiled a close-packed, deep-sea, cable-cutting device capable of severing the world’s most fortified underwater communication or power lines. It could shake up global maritime power dynamics.

China is the dominating region of the Asia Pacific Subsea Power Cables market. China is part of the Greater Tokyo Area, Japan’s biggest population and industrial zone. To ensure a reliable, high-capacity power supply, utilities invest in subsea HV power links, especially as the city electrifies further.

China is the world leader in offshore wind installations, especially in coastal provinces such as Guangdong, Jiangsu, Fujian, and Shandong. These offshore wind farms require subsea interarray and export cables to transmit power to shore. Chinese companies such as CNNOC are electrifying platforms in the Bohai Sea and South China Sea. This requires subsea cables to deliver power from shore or offshore substations to rigs and production facilities. These companies supply cables domestically and for export, helping reduce costs and speed up deployments.

North America

The North America market is growing at a CAGR of 4.64% during the forecast period. The market in North America is estimated to reach USD 0.91 billion in 2025 and secure the position of the third-largest region in the market. In the region, the U.S. is estimated to reach USD 0.84 billion each in 2025. The North America subsea power cable is increasing due to energy demands, offshore renewable development, and infrastructure modernization.

The U.S is the dominating country in the power cable market. The U.S. subsea power cable market is growing due to several key drivers across renewable energy. Increasing digitalization and remote monitoring demand more robust electrical and fiber optic subsea cabling. U.S. federal and state-level clean energy goals, 30 GW of offshore wind by 2030, push subsea transmission and infrastructure investment. Some legacy submarine cables are nearing the end of life and being replaced with newer, more efficient systems, boosting the market.

Europe

Europe is projected to record a growth rate of 5.62%, which is the second highest amongst all the regions, and touch the valuation of USD 5.08 billion in 2025. The European subsea power cable market growth is due to policy, energy transition, goals, interconnectivity needs, and offshore renewable energy development. EU green deal and country-specific net zero goals, such as the UK by 2050, Germany by 2045, require massive renewable energy integration. However, the U.S. administration's insisting that European nations balance the trade might increase the supply of U.S. energy in the European market, affecting Europe's sustainability goals and delaying renewable energy investments. The U.K. are expected to record a valuation of USD 1.07 billion, Germany to record USD 1.60 billion, and France to record USD 0.36 billion in 2025.

Latin America

Latin America has more remote islands and coastal areas with limited or unreliable grid access. Countries such as Chile, Brazil, and the Caribbean are investing in subsea power cables to replace expensive diesel generation, improve grid reliability, and integrate clean energy. The Latin America market in 2025 is set to record USD 0.18 billion as its valuation.

Middle East & Africa

Middle East countries with major offshore oil and gas fields, such as Saudi Arabia, UAE, Angola, Nigeria, and Egypt, are adopting power from shore solutions to cut emissions, reduce diesel or gas generators' dependence on platforms, and support subsea processing and control systems. Africa, especially South Africa, Morocco, and Egypt, is exploring offshore wind farms to diversify its energy supply. Morocco’s floating wind projects and South Africa’s proposed offshore wind near Port Elizabeth will require high-voltage export subsea cables and MV array cables between turbines. In the Middle East & Africa, GCC is set to attain the value of USD 0.18 billion in 2025.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Product Development and Collaboration with Industry Players Drive Competitive Landscape

In the market, a few players hold a major market share due to the complexity and nature of the business related to subsea power cables. Owing to their enriched experience, financial capability, and technical know-how, market players such as Prysmian Group, Sumitomo Electric, and Nexans are attributed to significant market share. Companies also focus on product development and collaborate with industry players, network providers, system integrators, and end-users. This allows companies to access new markets and enhance their market share. Strategic partnerships and alliances provide companies with a broader customer base and improved market reach.

List of the Key Subsea Power Cable Companies Profiled

- ABB (Switzerland)

- Prysmian (Italy)

- Tratos (Italy)

- LS Cable & System Ltd. (South Korea)

- ZTT Group (China)

- Universal Cables Ltd (India)

- Furukawa Electric Co., Ltd. (Japan)

- NKT A/S (Denmark)

- KEI Industries (India)

- Nexans (France)

- Hengtong (China)

- Sumitomo Electric Industries, Ltd. (Japan)

KEY INDUSTRY DEVELOPMENTS

- April 2025- LS Cable & System declared that its U.S. subsidiary, LS GreenLink, had held a groundbreaking ceremony for what the company says will be the largest factory in the U.S. As per the company, this investment, worth a total of USD 776.77 million, is significant as it is the first case of large-scale local investment by a Korean firm since the second term of the Trump administration.

- March 2025- LS Cable & System of South Korea, along with its subsidiary LS Eco Energy Limited, secured the order for the initial delivery of MV-grade aluminum power cables. The two firms will provide 35 kV aluminum power cables valued at USD 25 million to a solar EPC company in the US. The cables will be used to construct power grids for California, New Jersey, and Indiana solar energy facilities. These cables improve the reliability of solar energy systems due to their excellent durability and consistent high-voltage transmission capabilities.

- March 2025- As the world's largest cable manufacturer capitalizes on its over USD 5 billion of U.S. purchases and makes use of the AI-driven expansion for data centers, Italy's Prysmian (PRY.MI) predicts an increase of about two-thirds in core profit by 2028 in its new Prysmian (PRY.MI) forecast. The day after President Donald Trump's inauguration, a vocal opponent of wind energy, Prysmian abandoned its intentions to build a U.S. plant for offshore wind farms in January.

- December 2024- ABB said that it has purchased Solutions Industry & Building (SIB), a top producer of high-end cable glands and building products for the construction industry that safeguard vital electrical equipment in railway, industrial, and hazardous environments. With the acquisition of SIB, ABB's footprint in the railway, mining, OEM, and specialized markets throughout Europe, the Middle East, and North America has increased.

- July 2024- All shares of AFL Telecommunications Europe Limited, a subsidiary of AFL Telecommunications LLC (AFL), have been acquired by Tratos Cavi Spa, a company headquartered in Pieve Santo Stefano, Tuscany, Italy, which Tratos Srl entirely owns. The acquisition covers the power utility, rail, and oil and gas industries' whole fiber optic cable product line, which includes the SkyWrap fiber optic cable for overhead power lines, robust trackside fiber optic cables, and submarine umbilical fiber optic cable components.

Investment Analysis and Opportunities

- Increasing demand for renewable power projects, especially offshore projects, is expected to attract high investments in this sector. This increasing investment in technological advancements, product enhancement is anticipated to create growth opportunities for market expansion over the forecast period.

- The U.S. federal and state-level clean energy goals, such as 30 GW of offshore wind by 2030, push subsea transmission and infrastructure investment. Some legacy submarine cables are nearing the end of their lives and being replaced with newer, more efficient systems, boosting the market.

- Along with government initiatives, major players are investing in expanding the subsea cable development sector. For instance, in July 2024, LS Cable & System announced to establish a facility in Virginia for high-voltage direct current (HVDC) subsea cables, which the company claims will be the largest factory of its type in the U.S. Via LS GreenLink, its American subsidiary, LS Cable & System plans to invest USD 681 million to construct the new plant.

REPORT COVERAGE

The global subsea power cable market report delivers a detailed insight into the market and focuses on key aspects such as the leading companies in the market. Besides, the report offers insights into the market trends & technology and highlights key industry developments. In addition to the factors above, the report encompasses several factors and challenges that contributed to the growth and downfall of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2019-2032 |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2025-2032 |

|

Historical Period |

2019-2023 |

|

Growth Rate |

CAGR of 6.45% from 2025 to 2032 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Cable Type

|

|

By Voltage Type

|

|

|

By Conductor Type

|

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was USD 11.28 billion in 2024.

The market is expected to grow at a CAGR of 6.45% over the forecast period.

The market size of the Asia Pacific stood at USD 5.12 billion in 2024.

Enhancing grid stability, climate resilience, and offshore oil and gas facility electrification are the key factors driving the market growth.

Some of the top players in the market are Nexans, NKT A/S, Prysmian Group, and others.

The global market size is expected to reach USD 18.56 billion by 2032.

- 2019-2032

- 2024

- 2019-2023

- 279

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us