Natural Gas Storage Market Size, Share & Industry Analysis, By Type (Underground {Depleted Gas Reservoirs, Salt Caverns, and Aquifer Reservoirs} and Above Ground {Liquefied Natural Gas (LNG) Storage, Compressed Natural Gas (CNG) Storage, and Others}), By End-User (Natural Gas Producers, Utility Companies, Industrial Customers, Power Generation Companies, and Others), Regional Forecast, 2026-2034

Natural Gas Storage Market Size and Future Outlook

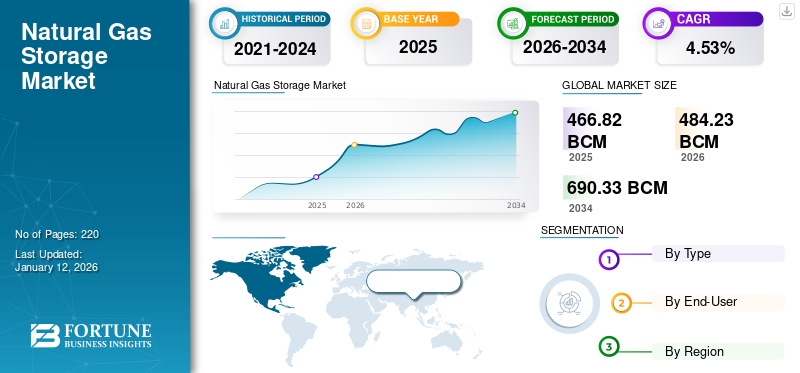

The global natural gas storage market size was valued at 466.82 billion cubic metres (bcm) in 2025 and is projected to grow from 484.23 billion cubic metres (bcm) in 2026 to USD 690.33 billion cubic metres (bcm) by 2034, exhibiting a CAGR of 4.53% during the forecast period. North America dominated the natural gas storage market, with a 38.53% market share in 2025.

The natural gas storage market demand is increasing rapidly, owing to the growing demand from the industrial and power generation sectors. As sectors such as chemicals, fertilizers, metals, and manufacturing progressively shift toward natural gas for a cleaner and more efficient energy solution, the demand for a steady and dependable supply of gas has grown. In 2024, the global consumption of industrial gas increased by close to 3%, as reported by the International Energy Agency (IEA), with the Asia Pacific and Middle East regions contributing significantly to this market growth. Moreover, natural gas is increasingly being employed as a balancing and peaking fuel to support system stability.

McDermott International, Inc., Enbridge, Inc., NAFTA A.S., Gazprom, and others are the key companies operating in the natural gas storage industry. Enbridge’s natural-gas storage business includes integrated flexible storage assets across Canada and the U.S., offering working capacity through both its transmission operations and utility operations. For instance, the company reports about 622 billion cubic feet (Bcf) of net working storage across North America.

The natural gas storage market represents a foundational component of global energy infrastructure, enabling supply reliability, seasonal demand balancing, and price stabilization across interconnected gas networks. Storage capacity increasingly functions as a strategic asset rather than a purely operational buffer, particularly amid supply volatility and geopolitical uncertainty affecting global gas flows.

Natural gas storage market growth is expected to remain closely linked to energy security policies, LNG trade expansion, and renewable energy integration within power systems. As intermittent renewable generation expands, gas-fired plants increasingly require dependable fuel availability supported by responsive storage infrastructure. This dynamic reinforces long-term utilization even as broader decarbonization policies evolve.

Underground storage continues to dominate global installed capacity due to cost efficiency and large-volume containment capability. Depleted gas reservoirs account for the majority of operational facilities, supported by existing pipeline connectivity and proven geological performance. However, salt cavern storage is gaining strategic importance due to its rapid injection and withdrawal capability, supporting trading markets and peak electricity demand balancing. Above-ground liquefied natural gas storage infrastructure is expanding rapidly across import-dependent economies. LNG terminal development across Asia-Pacific and Europe is directly increasing investment in cryogenic storage systems designed to manage supply diversification strategies.

Download Free sample to learn more about this report.

NATURAL GAS STORAGE MARKET KEY TAKEAWAYS

- 2025 Market Size: 466.82 bcm

- 2026 Market Size: 484.23 bcm

- 2034 Forecast Market Size: 690.33 bcm

- CAGR: 4.53% from 2026–2034

- North America dominated the natural gas storage market with a 38.53% share in 2025.

- The underground storage segment is expected to lead the market with a 77.97% share in 2026.

- The utility companies segment accounted for the largest share, contributing 39.74% in 2025.

North America

North America generated 179.86 bcm in 2025 and remains the leading market due to extensive pipeline infrastructure, strong seasonal demand, and growing LNG export activities.

Europe

Europe accounted for 128.38 bcm in 2025 (27.50% share), supported by energy security initiatives and mandatory gas storage requirements before winter.

Asia Pacific

Asia Pacific reached 105.90 bcm in 2025 (22.69% share), driven by rising gas consumption, industrialization, and strategic LNG reserve investments.

U.S.

The U.S. natural gas storage market was valued at 137.56 bcm in 2026.

Japan

Japan’s natural gas storage market is projected to reach 14.74 bcm in 2026

Read More

MARKET DYNAMICS

Market Drivers

Growing Demand for Natural Gas from the Utility Sector to Propel Market Growth

Utilities are increasingly opting for natural gas since it provides a versatile, lower-carbon substitute for coal and oil, aiding them in achieving both reliability and emissions targets. Natural gas power plants can adjust output swiftly, making them well-suited to balance the fluctuating energy production from renewables such as solar and wind, a key factor driving market growth.

Globally, the demand for natural gas reached a record high in 2024, increasing by around 2.7% (approximately 115 billion cubic meters) compared to the previous year, largely fueled by electricity generation. In Latin America, demand saw a rise of about 1.6% in 2024, particularly in Brazil and Colombia, where drought conditions impacted hydropower availability and prompted utilities to rely more on gas-fired generation.

Energy security concerns remain the primary structural driver supporting natural gas storage market growth across developed and emerging economies. Governments increasingly prioritize strategic gas reserves following supply disruptions, geopolitical tensions, and price volatility experienced in recent energy cycles. Storage infrastructure enables operators to stabilize supply availability during winter demand peaks and unexpected pipeline interruptions.

The expansion of the liquefied natural gas trade has also strengthened storage requirements across importing regions. Countries diversifying supply sources require buffer capacity to manage cargo timing variability and regasification scheduling constraints. This trend is particularly visible in markets transitioning from pipeline dependency toward flexible LNG procurement strategies.

Power sector transformation further reinforces demand. Renewable energy penetration introduces intermittency into electricity systems, increasing reliance on gas-fired generation for balancing operations. Storage facilities allow utilities to maintain dispatch reliability while optimizing fuel procurement costs.

Market Restraints

High Capital Investment & Fluctuating Natural Gas Prices to Restrict Market Expansion

The expansion of the natural gas storage sector faces several limitations, largely influenced by infrastructural, economic, and environmental factors. A significant drawback is the substantial capital investment required for the establishment and upkeep of underground storage facilities, such as depleted reservoirs, aquifers, or salt caverns. These initiatives entail intricate geological evaluations, regulatory clearances, and lengthy construction schedules, which considerably postpone the increase in capacity. Furthermore, the volatility of natural gas prices and market fluctuations discourages funding for large-scale storage, as profitability is largely reliant on seasonal demand variations.

Capital intensity represents one of the most significant constraints affecting natural gas storage market expansion. Developing underground storage facilities requires extensive geological assessment, drilling investment, and long permitting timelines. Salt cavern development and reservoir conversion projects often involve multi-year execution cycles, delaying return on investment and increasing exposure to commodity price uncertainty.

Regulatory complexity also limits project acceleration in several regions. Environmental approvals, methane emission monitoring requirements, and land-use restrictions create additional compliance burdens for operators. Increasing scrutiny related to greenhouse gas emissions has intensified permitting challenges, particularly in mature energy markets pursuing decarbonization targets.

Market economics further introducesThe uncertainty. Storage profitability depends heavily on seasonal price spreads between injection and withdrawal periods. Narrow spreads reduce commercial incentives for infrastructure expansion, discouraging private investment without long-term contracted capacity agreements. Infrastructure aging presents another operational challenge. Many existing facilities in North America and Europe were developed decades ago and require modernization to maintain safety and performance standards. Upgrades increase operational expenditures while regulatory expectations continue rising.

Market Opportunities

Advancements in Digital Monitoring, Pressure Management, and Leak Detection to Create Growth Opportunities

Advancements in digital monitoring, automation, and sensor technology are revolutionizing the efficiency and safety of natural gas storage facilities, driving an excellent market opportunity. Contemporary storage sites are increasingly utilizing real-time data analytics and Internet of Things (IoT) technologies to consistently monitor variables such as pressure, temperature, and gas flow. These digital solutions enable operators to identify irregularities promptly, averting leaks, pressure variations, or equipment failures before they become serious. Cutting-edge leak detection methods, such as fiber-optic sensing and acoustic monitoring, offer immediate notifications, greatly lowering methane emissions and environmental hazards. For instance, AI-driven predictive maintenance tools use equipment performance trends to foresee component degradation or possible system issues, thereby minimizing downtime and prolonging asset longevity.

Energy transition dynamics are creating new expansion pathways across the natural gas storage market. While long-term decarbonization policies evolve, governments continue prioritizing supply reliability and grid resilience. This dual requirement positions storage infrastructure as a strategic buffer supporting both conventional and transitional energy systems.

Emerging economies present significant infrastructure development opportunities. Rapid industrialization and urban energy demand growth require stable gas supply management capabilities. Regions expanding liquefied natural gas import capacity are increasingly investing in integrated storage networks to reduce exposure to supply volatility and maritime disruptions. Hydrogen and low-carbon gas integration represents a longer-term opportunity frontier. Salt cavern formations and depleted reservoirs demonstrate strong technical suitability for hydrogen storage applications. Operators capable of adapting existing assets may unlock future revenue streams linked to clean energy ecosystems.

Market Trends

Global Energy Transition Toward Clean & Resilient Energy Systems is the Key Market Trend

The natural gas storage sector is undergoing a significant transformation, influenced by global shifts toward energy transition, concerns about supply security, and swift technological progress. As nations strive for cleaner and more robust energy solutions, natural gas continues to be vital for maintaining stability, particularly with the rising integration of renewables. For instance, CEDIGAZ reports that global underground working gas storage (UGS) capacity hit about 437 billion cubic meters (bcm) in 2023, a 2% annual increase, which represents the largest growth since 2015. Currently, there are more than 680 storage facilities operating around the globe, with approximately 70 new projects underway, anticipated to contribute an additional 55 bcm in capacity in the coming years.

Structural transformation across global energy systems is reshaping natural gas storage market trends. Storage assets increasingly function as flexibility infrastructure supporting renewable-heavy power grids rather than purely seasonal supply balancing tools. As solar and wind penetration expands, grid operators rely on fast-response gas capacity supported by strategically positioned storage facilities. Digitalization is becoming a defining operational trend. Operators are deploying advanced monitoring systems, predictive maintenance platforms, and reservoir simulation technologies to optimize injection and withdrawal efficiency. Data-driven asset management improves utilization rates while reducing operational risk across aging infrastructure portfolios.

Liquefied natural gas (LNG) integration is also influencing storage strategy. Import-dependent economies increasingly combine regasification terminals with storage hubs to strengthen supply security during geopolitical disruptions or demand spikes. Floating storage solutions and modular LNG infrastructure are gaining relevance in emerging markets. Hydrogen readiness represents another emerging transition theme. Several operators are evaluating repurposing depleted reservoirs and salt caverns for hydrogen or blended gas storage. Although commercialization remains early, infrastructure adaptability is influencing long-term investment planning decisions.

MARKET CHALLENGES:

Environmental Concerns Over Methane Emissions and Groundwater Contamination to Hamper Market Growth

One of the major challenges facing the natural gas storage industry is methane emissions and the potential for groundwater contamination. Methane, the primary component of natural gas, is a potent greenhouse gas with a global warming potential more than 25 times higher than that of carbon dioxide over a 100-year period.

For instance, high-profile incidents, such as the 2015 Aliso Canyon gas leak in California, have heightened public awareness and regulatory scrutiny of methane emissions from storage infrastructure. Additionally, improper site management or geological instability can lead to groundwater contamination, as brine or hydrocarbons may migrate into aquifers, posing health and environmental risks.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Underground Segment to Dominate, Driven by its Ability to Offer a Safe and Economical Method

On the basis of type, the market is classified into underground and above-ground.

Underground Storage

In 2026, the underground segment is anticipated to dominate with a share of 77.97% in 2026. Underground natural gas storage is widely preferred as it offers a safe, efficient, and economical method to align supply with demand, ensuring energy reliability. Storing gas underground in depleted oil or gas fields, aquifers, or salt caverns enables operators to gather gas during low-demand periods (typically in summer) and extract it when demand is high (such as in winter). This seasonal adaptability is essential for utilities and gas providers to maintain a steady supply and stabilize market prices.

Underground storage represents the structural backbone of the global natural gas storage market, accounting for the majority of operational working gas capacity worldwide. These facilities provide large-scale seasonal balancing capability, enabling operators to inject gas during low-demand periods and withdraw volumes during peak consumption cycles. Infrastructure economics strongly favor underground solutions due to lower long-term operating costs compared with surface storage alternatives.

Depleted reservoirs dominate installed capacity because existing geological formations and pipeline connectivity reduce development complexity. Operators leverage prior production data to assess containment reliability and pressure behavior. These sites are particularly suited for seasonal storage rather than rapid cycling operations.

Salt cavern storage is gaining importance due to superior withdrawal and injection flexibility. These facilities support rapid cycling requirements associated with volatile energy markets and gas-fired power balancing. Industrial consumers and trading hubs increasingly depend on cavern storage for short-term supply responsiveness.

Aquifer storage represents a smaller but strategically relevant segment where depleted reservoirs are unavailable. Development costs remain higher because extensive geological validation is required. Operational uncertainty historically limited adoption; however, technological improvements in subsurface monitoring are improving feasibility.

Above-Ground Storage

The above-ground segment is experiencing the fastest growth and is expected to grow at a CAGR of 6.16%. Above-ground natural gas storage is gaining traction due to its increased flexibility, quicker setup, and easier accessibility in comparison to underground storage systems. Unlike underground facilities that depend on certain geological formations and lengthy development periods, above-ground storage, such as pressurized steel tanks, LNG (liquefied natural gas) tanks, and bullet tanks, can be established almost anywhere, provided that safety and space conditions are met.

Above-ground storage solutions serve specialized operational requirements requiring mobility, distribution flexibility, or integration with global gas trade infrastructure.

Liquefied natural gas storage plays an expanding role as international gas trade volumes increase. LNG terminals increasingly integrate large storage tanks to stabilize supply chains between imports and downstream distribution networks. Market demand accelerated following supply diversification efforts across Europe and Asia. LNG storage enables countries with limited pipeline access to maintain supply resilience. Floating storage and regasification infrastructure further expands deployment flexibility.

Compressed natural gas storage serves localized distribution and transportation markets. Industrial facilities and urban gas networks rely on CNG systems for short-duration storage and load balancing. Growth remains linked to decentralized gas usage and mobility applications. Compared with LNG infrastructure, capital requirements are lower, supporting adoption among smaller operators and developing markets.

By End-User

The utility Companies Segment Dominates the Market due to its Ability to provide a Continuous Power Supply.

In terms of end-users, the market is categorized into natural gas producers, utility companies, industrial customers, power generation companies, and others.

Utility Companies

The utility companies segment is projected to dominate in the market, contributing 39.87% globally in 2026, and are set to hold the largest market share of 39.74% share in 2025. Utility companies use natural gas storage primarily to ensure a reliable, continuous, and cost-effective energy supply for their customers throughout the year.

Utility companies account for one of the largest shares of storage utilization due to their responsibility for residential and commercial energy supply reliability. Seasonal heating demand variations require extensive injection planning during lower consumption months. Utilities prioritize dependable withdrawal capability rather than rapid cycling flexibility. Regulatory frameworks in several regions mandate minimum storage levels to prevent supply disruptions. Digital forecasting systems are improving demand prediction accuracy, allowing utilities to optimize storage utilization efficiency and reduce procurement volatility.

Power Generation Companies

The power generation companies are anticipated to grow at the highest CAGR of 5.98% during the forecast period. Natural gas serves as a crucial energy source for power plants, particularly for combined-cycle and peaking facilities, which must quickly respond to fluctuations in electricity demand.

Gas-fired power generation growth significantly influences storage demand patterns. Flexible generation assets increasingly support renewable energy intermittency across modern electricity grids. Power producers require rapid access to fuel supply during renewable output fluctuations. Storage facilities capable of fast withdrawal cycles, therefore, gain strategic importance. As renewable penetration increases, gas storage acts as an indirect stabilizer supporting electricity reliability. This relationship strengthens investment justification even within decarbonization-focused energy systems.

Industrial Customers

Industrial consumers increasingly engage directly with storage capacity procurement as energy price volatility rises. Sectors including chemicals, fertilizers, metals, and manufacturing rely heavily on an uninterrupted gas supply. Direct access to storage improves operational continuity and cost predictability. Industrial clusters located near storage hubs benefit from shared infrastructure models that reduce transportation constraints. Energy-intensive industries also view storage access as protection against geopolitical supply risks affecting pipeline flows or import availability.

To know how our report can help streamline your business, Speak to Analyst

Regional Insights

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America Natural Gas Storage Market Size, 2025 (Billion Cubic Metres (bcm))

To get more information on the regional analysis of this market, Download Free sample

North America Natural Gas Storage Market Analysis:

In 2025, North America generated USD 179.86 bcm, contributing 38.53% to global market revenue, and is projected to grow to USD 186.11 bcm in 2026. The need for natural gas storage in North America is rising due to several significant factors. Seasonal variations have a major impact as gas usage dramatically increases in winter for heating and in summer for electricity production, necessitating storage to align supply with demand.

North America represents one of the most structurally developed natural gas storage markets due to extensive pipeline infrastructure and liberalized gas trading systems. Seasonal demand volatility across residential heating and power generation sustains strong storage utilization. Market activity increasingly emphasizes operational flexibility and rapid cycling capacity. Infrastructure modernization and integration with liquefied natural gas export growth continue influencing long-term natural gas storage market expansion across the region.

United States Natural Gas Storage Market:

In 2026, the U.S. natural gas storage market was valued at 137.56 bcm. The natural gas storage demand in the U.S. is growing owing to rising energy consumption, seasonal fluctuations, and more. In winter, there is a spike in the need for heating, whereas in summer, natural gas is predominantly used for electricity generation, necessitating ample storage reserves to ensure a balance in supply.

- For instance, as stated by the Energy Information Administration (EIA), by the end of the injection season in 2025, inventories are expected to reach nearly 3,980 Bcf, which would be about 5% above the five-year average.

The United States maintains the largest operational natural gas storage network globally, supported by depleted reservoirs and salt cavern infrastructure. Storage plays a central role in balancing shale production variability and regional consumption patterns. Market participants increasingly optimize storage through trading strategies and demand forecasting technologies. Regulatory oversight and grid reliability requirements reinforce continued investment supporting stable natural gas storage market growth nationwide.

Europe Natural Gas Storage Market Analysis:

The Europe market accounted for USD 128.38 bcm in 2025, representing 27.50% of the global industry, and is expected to reach USD 133.66 bcm in 2026. Europe is projected to record a growth rate of 5.12%. In Europe, the natural gas storage market share is driven by concerns over energy security, fluctuations in seasonal demand, and the continent's shift toward more sustainable energy sources. European nations have taken significant steps. For instance, the regulations from the European Union now mandate that storage facilities must be filled to a minimum of 90% capacity prior to winter, resulting in ongoing demand for storage.

Europe’s natural gas storage market has gained strategic importance following supply diversification initiatives and energy security policies. Governments increasingly mandate minimum storage filling targets before winter demand periods. Underground facilities remain dominant, while liquefied natural gas import infrastructure expands storage-linked capacity. Market restructuring and cross-border gas flows are strengthening regional coordination while supporting long-term resilience against supply disruptions.

Germany Natural Gas Storage Market:

Germany is expected to record the valuation of 24.36 bcm. Germany operates one of Europe’s largest storage capacities, reflecting its role as a regional gas distribution hub. Storage facilities stabilize industrial consumption and cross-border energy trade flows. Policy-driven reserve requirements and infrastructure control mechanisms strengthened investment activity after supply volatility periods. Operators increasingly prioritize operational transparency and monitoring technologies to ensure supply continuity and support broader European energy market stability.

United Kingdom Natural Gas Storage Market:

UK market is projected to reach USD 1.38 bcm by 2026, and Russia is expected to record 41.35 bcm in 2025. The United Kingdom's natural gas storage market continues to evolve following infrastructure rationalization and increasing liquefied natural gas dependence. Storage expansion discussions focus on strengthening resilience against seasonal import exposure. Offshore depleted reservoirs present redevelopment opportunities. Market operators emphasize flexibility and short-cycle response capability aligned with fluctuating electricity generation demand linked to renewable energy integration within national energy planning strategies. The Indian market is projected to reach USD 2.87 bcm by 2026.

Asia-Pacific Natural Gas Storage Market Analysis:

Asia Pacific recorded a market size of USD 105.9 bcm in 2025, capturing 22.69% of the global market share, and is projected to reach USD 111.18 bcm in 2026. In the region, China is estimated to reach 67.45 bcm in 2026. Asia-Pacific demonstrates accelerating natural gas storage development driven by urbanization, industrial expansion, and import dependency. Countries increasingly invest in strategic reserves supporting liquefied natural gas supply chains. Infrastructure growth remains uneven due to geological limitations in certain economies. However, rising gas consumption and power sector transitions toward cleaner fuels continue strengthening long-term natural gas storage market investment momentum across the region.

Japan Natural Gas Storage Market:

The Japanese market is projected to reach USD 14.74 bcm by 2026. Japan relies heavily on liquefied natural gas storage due to limited domestic pipeline and underground storage geology. Terminal-based tank infrastructure supports energy security and power generation reliability. Storage optimization increasingly focuses on inventory efficiency and import scheduling. Market participants invest in advanced monitoring systems and operational analytics to maintain supply stability within one of the world’s largest LNG-dependent energy systems.

China Natural Gas Storage Market:

China continues expanding underground storage capacity to balance growing domestic consumption and seasonal heating demand. Government policy strongly supports reserve expansion to improve supply security and reduce import volatility exposure. Depleted reservoirs and salt cavern projects are increasing across major consumption corridors. Infrastructure investment aligns closely with long-term natural gas adoption strategies within industrial and urban energy transition planning.

Latin America and the Middle East & Africa

Latin America accounted for USD 29.62 bcm in 2025, representing 6.35% of the global market share, and is projected to reach USD 29.83 bcm in 2026. Over the forecast period, the Latin America and Middle East & Africa regions are anticipated to show tremendous opportunities for natural gas storage, as countries such as Brazil, Argentina, and the Rest of Latin America are emerging countries. Brazil's energy system relies significantly on hydropower, which is susceptible to drought and fluctuations in seasonal rainfall. Furthermore, the growth of LNG imports and offshore gas production demands infrastructure to handle fluctuating inflows and peak demand. The Latin American market in 2025 is set to record 29.62 bcm in its valuation. In the Middle East and Africa, the natural gas storage market growth is driven by the countries, namely Saudi Arabia, the UAE, Egypt, and South Africa, that are diversifying their energy mix by using more natural gas for power generation, industrial feedstock, and desalination. In this region, GCC reached a valuation of 13.16 bcm in 2025.

Latin America’s natural gas storage market remains comparatively underdeveloped but demonstrates gradual expansion potential. Infrastructure limitations and uneven pipeline connectivity have historically constrained investment. However, rising industrial gas demand and power sector diversification are encouraging storage development initiatives. Liquefied natural gas terminals increasingly serve as interim storage solutions supporting supply reliability across import-dependent economies within the region.

Middle East and Africa

The Middle East & Africa market generated USD 23.04 bcm in 2025, representing 4.94% of the global market landscape, and is expected to reach USD 23.46 bcm in 2026. The Middle East and Africa natural gas storage market is emerging alongside expanding gas production and domestic consumption growth. Producers increasingly evaluate storage to stabilize export commitments and internal supply reliability. Underground reservoir potential exists in several countries, though the investment pace varies. Strategic infrastructure planning linked to industrial diversification continues shaping long-term development opportunities.

Natural Gas Storage Industry Competitive Landscape

Key Industry Players:

Vendors are Focusing on Strategic Partnerships to Maintain Operational Stability

McDermott International, Inc., Enbridge, Inc., NAFTA A.S., and others are acknowledged as major participants in the natural gas storage market, as each firm is actively involved in expanding and modernizing storage capacity, LNG & floating storage expansion, and others.

In August 2025, PetroChina, an oil and gas producer based in China, revealed its intention to purchase three natural gas storage facilities from China National Petroleum Corporation (CNPC) for 40.01 billion yuan ($5.59 billion), excluding tax. This acquisition aims to strengthen the company’s natural gas supply chain and maintain operational stability. The deal encompasses the complete equity interests in Xinjiang Gas Storage, Xiangguosi Gas Storage, and Liaohe Gas Storage, with respective valuations of 17.06 billion yuan (USD 2.39 billion), 9.99 billion yuan ($1.46 billion), and 12.95 billion yuan (USD 1.89 billion).

The natural gas storage industry demonstrates a capital-intensive and infrastructure-driven competitive structure characterized by long asset lifecycles, regulatory oversight, and high entry barriers. Market participation is dominated by integrated energy companies, transmission system operators, and specialized storage infrastructure developers operating under long-term contractual frameworks.

Competition primarily revolves around operational reliability, storage cycling capability, geographic connectivity, and integration with pipeline transmission networks rather than pricing alone. Facilities located near major consumption hubs or trading corridors maintain stronger utilization rates and strategic importance within gas balancing markets.

Underground storage operators continue strengthening portfolio resilience through modernization programs targeting compressor upgrades, leakage monitoring, and automation systems. Salt cavern operators increasingly gain a competitive advantage due to rapid injection and withdrawal capability compared with depleted reservoir facilities. Technology adoption also influences differentiation. Advanced reservoir simulation, predictive maintenance analytics, and remote asset monitoring platforms reduce operational downtime while improving capacity utilization.

LIST OF KEY NATURAL GAS STORAGE MARKET PROFILES:

- McDermott International, Inc. (U.S.)

- Enbridge, Inc. (Canada)

- NAFTA A.S. (Slovakia)

- Gazprom (Russia)

- Royal Vopak N.V. (Netherlands)

- TransCanada Corp. (Canada)

- Uniper (Germany)

- Sempra (U.S.)

- Chart Industries (U.S.)

- Martin Midstream Partners L.P. (U.S.)

Latest Natural Gas Storage Industry Developments:

- In July 2025, the European Parliament approved relaxed rules for natural gas storage refills across the EU, allowing member states a 10-percentage-point deviation from the bloc’s 90% storage target.

- In February 2025, Germany urged the European Union to relax its strict gas storage targets, citing concerns over high costs. The current rules, introduced after the Ukraine war, mandate all EU members to refill storage sites to 90% capacity by November, with interim milestones in February, May, July, and September each year.

- In May 2025, NeuVentus LLC announced an open season for up to 20 billion cubic feet (Bcf) of firm storage capacity offering quick-inject/quick-withdraw capability for LNG export, power generation, industrial, and gas-pipeline customers.

- In April 2025, Ukraine’s state energy company Naftogaz began injecting natural gas into its underground storage facilities after reserves hit record lows in April, aiming to rebuild stocks ahead of winter.

- In November 2024, Enbridge moved to bring a fourth cavern online at its Tres Palacios natural gas storage facility in Texas. The company claims to hold about 622.7 Bcf of net natural gas storage capacity across North America in its integrated assets.

REPORT COVERAGE

The global natural gas storage market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, operational costs, and details on partnerships, increased investments, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.53% from 2026-2034 |

| Unit | Volume (billion cubic metres (bcm)) |

| Segmentation |

By Type

By End-User

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at 484.23 billion cubic metres (bcm) in 2026 and is projected to reach 690.33 billion cubic metres (bcm) by 2034.

In 2025, the market value stood at 179.86 bcm.

The market is expected to exhibit a CAGR of 4.53% during the forecast period (2026-2034).

The utility companies segment led the market by End-User.

Growing adoption of the product in the utility & energy sector to propel market growth.

McDermott International, Inc., Enbridge, Inc., NAFTA A.S., and others are some of the top players in the market.

North America dominated the market in 2025.

Growing energy-security concerns and seasonal/peak demand variability, rising LNG import/export flows, increased gas-fired power to balance renewables favors product adoption.

- 2021-2034

- 2025

- 2021-2024

- 220

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us