Respiratory Drugs Market Size, Share & Industry Analysis, By Product (Bronchodilators, Anti-inflammatory / Controller Drugs, Combination Respiratory Drugs, and Others), By Disease Indication (Asthma, Chronic Obstructive Pulmonary Disease (COPD), Allergic Rhinitis & Chronic Rhinosinusitis, and Others), By Type (Branded and Generic), By Route of Administration (Inhalation, Injectable, Oral, Intranasal, and Others), By Age Group (Pediatric and Adult), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Specialty Pharmacies, and Others), and Regional Forecast, 2026-2034

Respiratory Drugs Market Size and Future Outlook

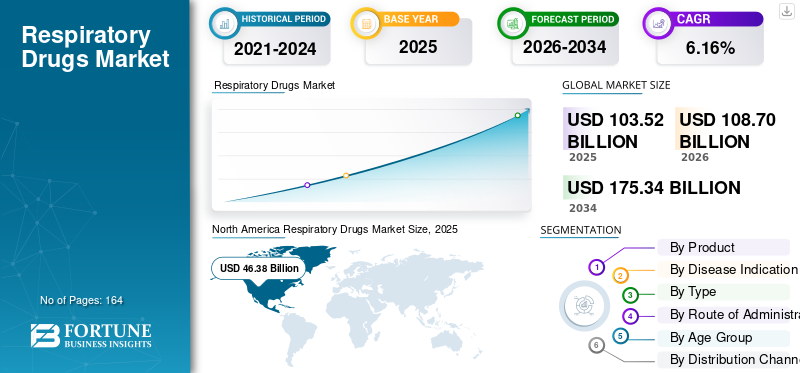

The global respiratory drugs market size was valued at USD 103.52 billion in 2025. The market is projected to grow from USD 108.70 billion in 2026 to USD 175.34 billion by 2034, exhibiting a CAGR of 6.16% during the forecast period. North America dominated the respiratory drugs market with a market share of 44.80% in 2025.

The global market for respiratory medications encompasses pharmaceutical products utilized for treating and managing respiratory ailments. The market is propelled by the significant and escalating prevalence of chronic respiratory conditions, increasing exposure to air pollution and smoking-induced lung harm, higher diagnosis rates, and the ongoing treatment requirements of patients in need of maintenance therapy.

Key players in the global market comprise GSK, AstraZeneca, Boehringer Ingelheim International GmbH, and Sanofi. Their competitive positioning is supported by strong distribution reach as well as continued focus on combination therapies, targeted therapies, and region-specific branded and generic product strategies.

Download Free sample to learn more about this report.

RESPIRATORY DRUGS MARKET TRENDS

Integration of Digital Inhalers and Personalized Treatment Approaches is a Remarkable Market Trend

The incorporation of digital inhalers and tailored treatment strategies is emerging as a significant trend in the respiratory medications market as manufacturers and healthcare providers shift from conventional inhaler distribution to data-driven disease management. Digital inhalers and connected sensors can monitor inhaler usage, timing, technique, and adherence, assisting physicians in determining if inadequate disease control stems from disease severity or improper/irregular medication usage. This facilitates more tailored treatment choices for asthma and COPD, encompassing therapy intensification, evaluation for biologic eligibility, inhaler transitions, and adherence strategies. The trend holds commercial significance as it can enhance patient involvement, boost results, and facilitate value-driven respiratory care frameworks. For pharmaceutical firms, integrating digital inhalers can aid in distinguishing branded inhaler offerings in a market challenged by generic competition. It further facilitates remote observation and at-home chronic respiratory management, which became critical following the COVID-19 pandemic. These factors are poised to support the global respiratory drugs market growth during the forecast period.

- For instance, in October 2025, Aptar Digital Health announced that the U.S. FDA granted 510(k) clearance for HeroTracker Sense, a Bluetooth-enabled connected add-on device for pressurized metered-dose inhalers.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Prevalence of Respiratory Diseases to Propel Market Growth

The increasing prevalence of respiratory diseases significantly contributes to market growth as it broadens the ongoing patient demographic needing consistent therapy. Asthma, COPD, allergic rhinitis, chronic rhinosinusitis, pulmonary fibrosis, and respiratory infections push the ongoing need for bronchodilators, inhaled corticosteroids, combination inhalers, biologics, antifibrotics, and anti-allergic medications. The load is rising due to air pollution, tobacco exposure, workplace dust, allergens, aging demographics, urban growth, and repeated respiratory infections. With the increase in diagnosed and treated patients, there is a growing need for affordable generic inhalers and allergy medications, alongside high-end therapies for severe asthma, COPD, cystic fibrosis, IPF/ILD, and pulmonary hypertension. This directly facilitates increased prescription volumes, broader application of maintenance therapies, and enhanced adoption of specialized respiratory medications. The trend is particularly pronounced in emerging markets, where sizable populations and underdiagnosis provide opportunities for future treatment growth. In general, the increasing prevalence of diseases boosts both the volume base and the value base of the global respiratory medications market. All these factors cumulatively drive the global market growth.

- For instance, in June 2025, WHO/Europe and the European Respiratory Society reported that more than 80 million people in the WHO European Region are affected by chronic respiratory diseases, including asthma, COPD, and other lung conditions, while many more remain undiagnosed.

MARKET RESTRAINTS

High Cost of Advanced Biologic Therapies to Hamper Market Growth

The expensive nature of advanced biologic treatments serves as a market limitation since these therapies are primarily employed for severe asthma, eosinophilic airway disease, COPD with type 2 inflammation, and chronic rhinosinusitis with nasal polyps, where yearly treatment expenses significantly exceed those of standard inhalers or generic maintenance medications. While biologics can lower exacerbations and enhance disease management, their high costs restrict access in budget-conscious healthcare systems and frequently necessitate stringent prior authorization, specialist prescriptions, biomarker assessments, and reimbursement approvals. This hinders patient adoption, particularly in developing markets and public health systems with constrained finances. Elevated out-of-pocket expenses can impact the continuation of treatment when insurance coverage is lacking. Consequently, numerous qualified patients might continue using traditional inhaled treatments or oral corticosteroids rather than transitioning to biologics. The limitation is most pronounced in areas where reimbursement routes for biologics are tight and competition from biosimilars remains sparse. In general, elevated costs limit the addressable treated population for advanced respiratory biologics and slow market expansion.

- For example, in February 2025, the World Health Organization (WHO) stated that biologic medicines have transformed treatment for many chronic and life-threatening diseases, but their high costs have limited accessibility for many patients globally.

MARKET OPPORTUNITIES

Advancements in Inhalation Drug Delivery Systems to Offer Market Growth Opportunities

Advancements in inhalation drug delivery systems are creating a strong market opportunity as respiratory treatment is shifting toward more efficient, patient-friendly, and higher-precision delivery formats. Improved dry powder inhalers, soft-mist inhalers, nebulizers, metered-dose inhalers, and connected delivery platforms can help improve lung deposition, dose consistency, adherence, and ease of use. This is important as many asthma, COPD, cystic fibrosis, pulmonary hypertension, and pulmonary infection therapies depend on correct inhalation technique for clinical benefit. Advanced delivery systems also create opportunities for companies to reformulate existing drugs, develop differentiated branded products, and expand inhaled delivery into newer areas such as biologics, peptides, RNA-based therapies, and specialty pulmonary drugs. For manufacturers, these systems can support lifecycle management, premium positioning, and better patient outcomes. The opportunity is especially relevant as respiratory care increasingly moves toward home-based treatment and long term disease control. All these factors would drive the market growth in the coming years.

- For instance, in June 2025, Cambridge Healthcare Innovations announced Quattrii, a dry powder inhaler engine designed to deliver large volumes of biologic and mRNA molecules in a single inhalation.

MARKET CHALLENGES

Issues Related to Patient Adherence to Long-Term Treatments to Create Challenges for Market Growth

Challenges concerning patient compliance with prolonged treatments persist as a significant obstacle in the respiratory pharmaceuticals sector, as numerous patients with asthma, COPD, cystic fibrosis, IPF/ILD, and pulmonary hypertension need ongoing therapy for many years. Inhaled medications are particularly sensitive to adherence, as patients need to utilize the proper dose, frequency, and inhalation method to gain clinical benefit. Inadequate adherence may result in unmanaged symptoms, flare-ups, emergency room visits, hospital stays, and superfluous treatment increases, undermining real-world results despite the availability of effective medications. It also influences market expansion as low refill rates and therapy cessation diminish the perceived value of maintenance inhalers, controller medications, biologics, and specialty treatments. The difficulty increases in chronic illnesses where patients feel improved and discontinue treatment, encounter significant out-of-pocket expenses, or grapple with complicated multi-drug therapies. Consequently, businesses and healthcare organizations are investing in training, reminders, digital inhaler tracking, and more straightforward dosing formats to enhance adherence. All the factors cumulatively affect the market growth.

- For instance, in 2025, a randomized controlled trial sponsored by Accurx across 89 GP practices in England reported that non-adherence to prescribed preventer inhalers compromises outcomes in asthma and COPD and tested supportive text messages as a scalable way to improve preventer inhaler adherence and symptom control.

Segmentation Analysis

By Product

Higher Use of Fixed-Dose Inhalers and Triple Therapies to Push Combination Respiratory Drugs Segment Dominance

In terms of product, the market is divided into bronchodilators, anti-inflammatory/controller drugs, combination respiratory drugs, respiratory biologics & targeted therapies, upper respiratory & anti-allergic drugs, specialty drugs, and others.

The combination respiratory drugs segment captured the largest respiratory drugs market share in 2025. The segment’s dominance is due to the wide use of fixed-dose inhalers for long-term asthma and COPD control, especially in patients who need more than one mechanism of action to manage symptoms and reduce exacerbations. The combinational therapies segment also gains share as clinicians increasingly prefer combination and triple therapies over standalone bronchodilators or standalone corticosteroids for moderate-to-severe disease management. Additionally, expanding pipeline of these products also supports the segment growth.

- For instance, in March 2025, AstraZeneca announced that Breztri Aerosphere, an inhaled triple-combination therapy, met the primary endpoints in the KALOS and LOGOS Phase III asthma trials and stated that Breztri was already approved for COPD in adults in more than 80 countries, including the U.S., EU, China, and Japan.

The respiratory biologics & targeted therapies segment is anticipated to rise at a CAGR of 10.53% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Disease Indication

Large Patient Pool across Adult and Pediatric Groups to Boost Asthma Segment Dominance

On the basis of disease indication, the market is divided into asthma, chronic obstructive pulmonary disease (COPD), allergic rhinitis & chronic rhinosinusitis, cystic fibrosis, idiopathic pulmonary fibrosis & ILD, respiratory infections, and others.

The asthma segment accounted for the largest global respiratory drugs market share in 2025. The segment’s dominance can be attributed to the very large patient population across both pediatric and adult age groups and requires repeated use of rescue, controller, and maintenance therapies. The segment also has strong commercial value as severe and uncontrolled asthma patients are increasingly treated with premium biologics and targeted therapies. Additionally, rising diagnosis, worsening air pollution, allergen exposure, and increasing awareness of disease control are supporting higher prescription volumes across developed and emerging markets. Furthermore, the segment is set to hold 26.0% share in 2026.

- For instance, in May 2025, AstraZeneca announced positive full results from the BATURA Phase IIIb trial for Airsupra (albuterol/budesonide). In comparison to albuterol alone, the combination showed a 47% decline in the risk of severe exacerbations in mild asthma.

The allergic rhinitis & chronic rhinosinusitis segment is anticipated to grow at a CAGR of 4.56% over the forecast period.

By Type

Premium Product Prices and Physician Preference Pushed the Dominance of Branded Segment

Based on type, the market is classified into generic and branded.

The branded segment dominated the global market in 2025. The segment growth is driven by its high prices of these products, strong physician preference for established branded inhalers and biologics, patent protection, specialty pharmacy distribution, and lifecycle management strategies. Furthermore, the segment is set to hold a share of 67.0% in 2026.

- For instance, in February 2026, GSK reported that in the full-year 2025, Trelegy generated GBP 3.0 billion (USD 4.0 billion) in sales, growing 13%, while respiratory, immunology, and inflammation sales reached GBP 3.8 billion (USD 5.1 billion), growing 18%.

The generic segment is anticipated to rise at a CAGR of 4.74% over the forecast period.

By Route of Administration

Inhalation Segment Led the Market Owing to Extensive Use of Metered-Dose and Dry Power Inhalers

In terms of route of administration, the market is divided into inhalation, injectable, oral, intranasal, and others.

The inhalation segment captured the highest share of the global market in 2025. It remains the preferred route for major respiratory diseases such as asthma and COPD. The segment is supported by the broad use of metered-dose inhalers, dry powder inhalers, soft-mist inhalers, and nebulized therapies across both rescue and maintenance treatment. Additionally, inhalation continues to lead due to high prescription volume, established clinical use, and availability across branded and generic products. Furthermore, the segment is set to hold a share of 44.6% in 2026.

- For instance, in June 2024, Verona Pharma announced that the U.S. FDA approved Ohtuvayre (ensifentrine) for the maintenance treatment of COPD in adults. Ohtuvayre is the first inhaled therapy for COPD with a novel mechanism of action in more than 20 years.

The injectable segment is anticipated to rise at a CAGR of 9.33% over the forecast period.

By Age Group

Adult Segment Dominated the Market due to Large Patient Pool in Adult and Older Patient Population

On the basis of age group, the market is divided into pediatric and adult.

The adult segment captured the highest share of the global market in 2025. The segment growth is driven by large patient pool in adult and older patient population. Moreover, chronic respiratory disease burden rises with age, smoking history, occupational exposure, air pollution, and comorbidities, increasing the need for continuous drug management. The segment also benefits from higher diagnosis rates and stronger access to specialist care among adults in developed markets. Furthermore, the segment is set to hold a share of 84.0% in 2026.

- For instance, in May 2025, GSK announced that the U.S. FDA approved Nucala (mepolizumab) as an add-on maintenance treatment for adult patients with inadequately controlled COPD and an eosinophilic phenotype.

The pediatric segment is anticipated to rise at a CAGR of 5.07% over the forecast period.

By Distribution Channel

High Prescription Volume for Respiratory Drugs to Support Retail Pharmacies & Drug Stores Segment Dominance

Based on distribution channel, the market is segmented into hospital pharmacies, specialty pharmacies, retail pharmacies & drug stores, and online pharmacies.

In 2025, the retail pharmacies & drug stores segment held the leading position in the global market. The segment’s dominance can be attributed to the high prescription volume for various respiratory drugs, easy access to both branded and generic respiratory medicines, broad patient reach and growing demand for frequent refills. In addition, pharmacy-counter affordability programs and repeat prescription services strengthen the role of drug stores in respiratory treatment access. Furthermore, the segment is set to hold a share of 43.5% in 2026.

- For instance, in June 2024, Boehringer Ingelheim announced that its COPD and asthma inhalers became available for USD 35 per month for eligible patients, with the program automatically reducing costs at the pharmacy counter for most eligible patients, including uninsured patients and those with high co-pays.

In addition, the specialty pharmacies segment is projected to witness a CAGR of 7.20% during the forecast period.

Respiratory Drugs Market Regional Outlook

By geography, the market is divided into North America, Latin America, Asia Pacific, Europe, and the Middle East & Africa.

North America

North America Respiratory Drugs Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market reached USD 44.44 billion in 2024 and led the global market. In 2025, the region continued to hold its leading position with a value of USD 46.38 billion. High diagnosed burden of respiratory diseases, high adoption of premium therapies, strong reimbursement coverage, specialty pharmacy networks, early product launches, and higher physician awareness support the regional market growth.

U.S. Respiratory Drugs Market

The U.S. dominated the North America market and can be analytically approximated at around USD 43.51 billion in 2026, accounting for roughly 40.0% of the global market.

Europe

The Europe market size is anticipated to grow at a CAGR of 5.32% during the forecast period. The regional market growth is supported by a large aging population, high COPD prevalence, established inhaler use, and strong public healthcare access across major countries.

U.K. Respiratory Drugs Market

The U.K. market is estimated to reach around USD 3.77 billion in 2026, representing roughly 3.5% of global revenues.

Germany Respiratory Drugs Market

The Germany market size is projected to reach approximately USD 4.42 billion in 2026, equivalent to around 4.1 of global sales.

Asia Pacific

The Asia Pacific market is expected to reach a valuation of USD 30.34 billion by 2026, making it the third largest region in the global industry. Asia Pacific is expected to show strong growth due to its large population base, rising asthma and COPD burden, high pollution exposure, smoking prevalence in several countries, and increasing respiratory infection burden.

Japan Respiratory Drugs Market

The Japan market is estimated to touch around USD 6.87 billion in 2026, accounting for roughly 6.3% of global revenues.

China Respiratory Drugs Market

The China market is projected to reach revenues of around USD 8.52 million in 2026, representing roughly 7.8% of global sales.

India Respiratory Drugs Market

The India market is estimated to touch around USD 3.78 billion in 2026, accounting for roughly 3.5% of global revenues.

Latin America and Middle East & Africa

The Middle East & Africa and Latin America regions are likely to witness slower growth throughout the forecast period. The Latin America market is projected to reach a valuation of USD 3.79 billion by 2026. In the Middle East and Africa region, the GCC market is projected to reach approximately USD 1.00 billion by 2026, representing about 0.9% of global revenues. Prominent factors such as high asthma burden, improving healthcare infrastructure, increasing access to retail pharmacy-based respiratory treatments along with others are boosting the market growth in these regions.

COMPETITIVE LANDSCAPE

Key Industry Players

Broad Respiratory Product Portfolios and Expanding Specialty Pipelines to Drive Leading Players’ Dominance

The global respiratory drugs market features a moderately fragmented structure with the presence of well-established as well as emerging players in the market. Key companies include GSK, AstraZeneca, Sanofi, and Boehringer Ingelheim International GmbH, among others. The considerable revenue of these companies is owing to the presence of blockbuster inhalers, respiratory biologics, cystic fibrosis therapies, antifibrotics, and pulmonary hypertension drugs in their product portfolios, along with established geographical reach and a respiratory pipeline consisting of advanced targeted therapies. Furthermore, these players are also engaged in strategic initiatives such as label expansions, new approvals, partnerships, and portfolio strengthening to expand their market presence over the forecast period.

- For instance, in March 2025, Sanofi and Regeneron announced that Dupixent was approved in Japan as the first-ever biologic medicine for patients with COPD, strengthening their respiratory leadership in a major market.

Additional key contributors include Novartis AG, Vertex Pharmaceuticals Incorporated, Teva Pharmaceutical Industries Ltd., Chiesi Farmaceutici S.p.A., and others. These companies hold broad respiratory drug portfolios and are focusing on launches of novel therapies, expansion of branded and generic inhaler portfolios, and specialty respiratory offerings over the forecast period.

LIST OF KEY RESPIRATORY DRUGS COMPANIES PROFILED

- GSK (U.K.)

- AstraZeneca (U.K.)

- Boehringer Ingelheim International GmbH (Germany)

- Sanofi (France)

- Vertex Pharmaceuticals Incorporated (U.S.)

- Hoffmann-La Roche Ltd (Switzerland)

- Novartis AG (Switzerland)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Viatris Inc. (U.S.)

- Chiesi Farmaceutici S.p.A. (Italy)

KEY INDUSTRY DEVELOPMENTS

- March 2026: The U.S. FDA approved the first generic of Flovent HFA fluticasone propionate inhalation aerosol developed by Glenmark Pharmaceuticals for the maintenance treatment of asthma in patients aged 4 years and older.

- December 2025: Boehringer Ingelheim announced the U.S. FDA approval of JASCAYD/nerandomilast tablets for progressive pulmonary fibrosis (PPF) in adults, following its earlier IPF approval.

- December 2025: GSK announced the U.S. FDA approval of Exdensur / depemokimab as an add-on maintenance treatment for severe asthma with an eosinophilic phenotype in patients aged 12 years and older.

- November 2025: Sanofi and Regeneron announced that Dupixent met all primary and secondary endpoints in a pivotal Phase III study for allergic fungal rhinosinusitis (AFRS), and that the U.S. FDA accepted the sBLA for priority review.

- October 2025: AstraZeneca and Amgen announced the U.S. FDA approval of Tezspire for the add-on maintenance treatment of chronic rhinosinusitis with nasal polyps in patients aged 12 years and older.

REPORT COVERAGE

The global respiratory drugs market analysis encompasses an extensive examination of the market size and projections for all market segments featured in the report. It provides information on the market dynamics and trends that are anticipated to propel the market during the forecast period. It offers insights into crucial elements, such as innovations in products, the regulatory landscape, pipeline analysis, and the introduction of new products. Furthermore, it outlines collaborations, mergers, and acquisitions, along with significant advancements in the market. The global market forecast report additionally offers a comprehensive competitive landscape with details on market share and profiles of major active participants.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.16% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product, Disease Indication, Type, Route of Administration, Age Group, Distribution Channel, and Region |

| By Product |

|

| By Disease Indication |

|

| By Type |

|

| By Route of Administration |

|

| By Age Group |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 103.52 billion in 2025 and is projected to reach USD 175.34 billion by 2034.

In 2025, the North America market value stood at USD 46.38 billion.

The market is expected to exhibit a CAGR of 6.16% during the forecast period of 2026-2034.

By product, the combination respiratory drugs segment led the global market in 2025.

The rising prevalence of respiratory diseases such as asthma and COPD, increasing air pollution levels, and growing geriatric population are key factors driving market expansion.

GSK, AstraZeneca, Boehringer Ingelheim International GmbH, and Sanofi are the prominent players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 164

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us