Specialty Drugs Market Size, Share & Industry Analysis, By Molecule Platform (Biologics, Specialty Small Molecules, Cell & Gene Therapies, Radiopharmaceuticals, and Others), By Disease Indication (Oncology, Autoimmune & Inflammatory Disorders, Rare Diseases/Orphan Disorders, Neurology, Hematology, Infectious Diseases, and Others), By Formulation (Oral and Parenteral {Intravenous (IV), Subcutaneous (SC), Intramuscular (IM), and Others}), By End User (Hospitals, Specialty Clinics & Infusion Centers, Home Care / Home Infusion, and Others), and Regional Forecast, 2026-2034

Specialty Drugs Market Size and Future Outlook

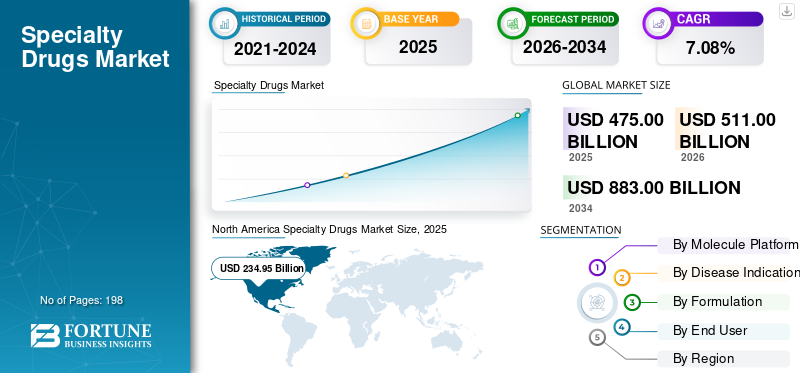

The global specialty drugs market size was valued at USD 475.00 billion in 2025. The market is projected to grow from USD 511.00 billion in 2026 to USD 883.00 billion by 2034, exhibiting a CAGR of 7.08% during the forecast period. North America dominated the global market with a market share of 49.46% in 2025.

The global specialty drugs market encompasses high-cost, high-complexity prescription therapies that require specialized handling, administration, monitoring, reimbursement support, or patient-management services. The market is expanding as the treatment paradigm transitions to targeted and precision therapies for severe and chronic ailments, resulting in increased demand for specialty medications in both hospital and specialty care environments. Market growth is further fueled by the rising use of parenteral therapies, the increasing adoption of gene and cell therapies, and the expanding roles of hospitals, specialty clinics, and infusion centers, along with home care/home infusion in delivering specialty treatments.

Many key industry players, including AbbVie Inc., Merck & Co., Inc., Pfizer Inc., Sanofi, Amgen Inc., Gilead Sciences, Inc., and others, are actively strengthening their specialty drug offerings through investments in research & development, expanding distribution networks, and other strategic initiatives.

Download Free sample to learn more about this report.

SPECIALTY DRUGS MARKET TRENDS

Advancements in Biotechnology and Personalized Medicine are a Significant Trend Observed

Innovations in biotechnology and tailored healthcare are becoming a significant trend in the market. The development of specialty drugs is progressively shifting from general disease management to targeted therapies that focus on particular biomarkers, genes, immune pathways, or specific patient subgroups. This change is boosting the need for biologics, specialty small molecules, cell and gene therapies, radiopharmaceuticals, and treatments linked to companion diagnostics. With an increasing number of patients undergoing testing for genetic mutations, protein levels, or specific disease biomarkers, doctors can choose treatments that better align with the patient’s situation. This enhances treatment accuracy and facilitates premium pricing for advanced specialty medications. The trend is particularly robust in oncology, rare conditions, autoimmune ailments, and hematology, with companies making significant investments in next-generation biologics, targeted cancer treatments, radioligand therapies, and gene therapies. These factors are supporting the overall global specialty drugs market growth.

- For instance, in March 2025, Novartis announced that the U.S. Food and Drug Administration approved Pluvicto, its radioligand therapy, for earlier use before chemotherapy in PSMA-positive metastatic castration-resistant prostate cancer. The company stated that the expanded indication approximately triples the eligible patient population, showing how biomarker-based and targeted specialty therapies are moving earlier in treatment pathways.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand for Targeted Therapies to Boost Market Growth

Rising demand for targeted therapies is a major driver for the global market. Patients with cancers, rare diseases, autoimmune disorders, and hematology conditions increasingly need treatments that act on specific biomarkers, mutations, proteins, or immune pathways instead of using broad, one-size-fits-all therapies. This is increasing the use of specialty biologics, antibody-drug conjugates, targeted small molecules, radiopharmaceuticals, and cell & gene therapies. As diagnostic testing improves, physicians can identify the right patient group and prescribe therapies with better clinical relevance. This creates higher demand for premium specialty drugs, especially in oncology and rare disease care. Targeted therapies also support strong market growth as they are often used in high-value indications, have differentiated clinical benefits, and are supported by companion diagnostics and specialist-led treatment pathways. As a result, the shift toward precision treatment is directly expanding the commercial opportunity for specialty drugs. All these factors cumulatively drive the overall market growth.

- For instance, in May 2025, AbbVie announced that the U.S. FDA granted accelerated approval to EMRELIS for previously treated advanced non-small cell lung cancer patients with high c-Met protein overexpression.

MARKET RESTRAINTS

Complex Regulatory Requirements to Hamper Market Growth

Intricate regulatory demands serve as a limitation for the global market. Specialty medications such as biologics, cell and gene therapies, radiopharmaceuticals, and advanced targeted therapies typically demand more robust clinical evidence, comprehensive safety monitoring, stringent manufacturing regulations, and facility inspections before approval. This extends development schedules and raises the expenses of launching products. Despite encouraging clinical data, companies may encounter setbacks stemming from chemistry, manufacturing, and controls (CMC), product uniformity, quality management systems, or inspection-related issues. Such delays can hinder patient access, delay revenue generation, and raise uncertainty for manufacturers and investors. The limitations are more stringent for cell and gene therapies due to their complex production processes, with regulators thoroughly evaluating manufacturing reliability, long-term safety, and the benefit-to-risk ratio. Consequently, intricate regulatory processes may restrict the pace at which new specialty medications reach the market.

- For instance, in July 2025, Ultragenyx announced that the U.S. FDA issued a Complete Response Letter for its BLA for UX111, an AAV gene therapy for Sanfilippo syndrome type A. The company stated that the CRL cited specific chemistry, manufacturing, and controls (CMC)-related observations. However, the U.S. FDA clinical review acknowledged that the clinical data were robust and the biomarker data were supportive.

MARKET OPPORTUNITIES

Growing Investments in Biologics Development to Offer Market Growth Opportunities

Increasing investments in biologics development are generating a significant market opportunity. Biologics are increasingly essential in specialized therapies, as they are widely used in oncology, autoimmune disorders, rare conditions, neurology, and hematology. With the rise in demand for targeted and advanced therapies, firms are investing in biologics research and development, manufacturing capabilities, and advanced production technologies. This opens the door to introducing additional high-value specialty products and enhancing supply reliability for intricate injectable and infusion therapies. It also facilitates growth in biosimilars, next-generation antibodies, antibody-drug conjugates, and various biologic platforms. Due to the necessity for specialized handling, cold-chain logistics, and clinical oversight, the rise of biologics directly enhances the roles of hospitals, specialty clinics, infusion centers, and specialty pharmacies. As a result, increased investment in biologics is anticipated to enhance both the product pipeline and market access of specialty medications.

- For instance, in September 2025, Amgen announced a USD 650.0 million expansion of its U.S. manufacturing network to increase drug production at its biologics manufacturing facility in Juncos, Puerto Rico, and integrate advanced manufacturing technologies.

MARKET CHALLENGES

Limited Patient Access due to Reimbursement Constraints Poses a Prominent Challenge to Market Growth

Restricted patient access due to reimbursement limitations poses a significant challenge for the global market. Specialty medications typically cost significantly more than traditional drugs due to complex research and development, biologic production, cold-chain logistics, specialized administration, and extensive patient oversight. Due to this significant expense, payers frequently implement prior authorization, step therapy, restricted formularies, outcomes-based contracts, or limited-coverage policies before approving treatment. This can postpone the start of therapy, decrease patient affordability, and restrict adoption even when the medication has significant clinical benefits. The difficulty is particularly apparent in cell and gene therapies, oncology medications, medicines for rare diseases, and expensive biologics, where a single treatment cycle can impose a significant burden on insurers and public payers. Consequently, uncertainty regarding reimbursement may hinder commercial uptake and limit the number of patients able to access advanced specialty medications. This highlights the significance of access support, value-driven agreements, and payer negotiations for future market expansion.

- For instance, in July 2025, CMS announced participation of 33 states, Washington D.C., and Puerto Rico in the Cell and Gene Therapy Access Model to improve Medicaid access to sickle cell disease gene therapies through outcomes-based payment arrangements. The need for such a model shows that high upfront costs and reimbursement complexity remain key barriers to patient access for advanced specialty drugs.

Segmentation Analysis

By Molecule Platform

Strong Clinical Use and Wider Specialty Applications Led to Biologics Segment Dominance

In terms of molecule platform, the global market is segmented into biologics, specialty small molecules, cell & gene therapies, radiopharmaceuticals, and others.

The biologics segment led the global specialty drugs market share in 2025. This is mainly due to their strong clinical benefits, targeted mechanism of action, and established use in chronic diseases that require long-term treatment. Additionally, many leading specialty drugs are monoclonal antibodies, fusion proteins, recombinant proteins, or biosimilars, which increases the revenue contribution of biologics within the overall market. The segment is further supported by high adoption of injectable and infusion-based therapies in hospitals, specialty clinics, and infusion centers. Moreover, growing biosimilar approvals are improving access to biologic treatments while expanding the commercial base of this segment.

- For instance, in April 2025, Biocon Biologics announced that the U.S. FDA approved Jobevne, a biosimilar bevacizumab for intravenous use, expanding its oncology biologics portfolio in the U.S.

The cell & gene therapies segment is anticipated to rise with a CAGR of 13.68% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Disease Indication

High Treatment Burden and Strong Use of Targeted Drugs Supported Oncology Segment Dominance

Based on disease indication, the global market is segmented into oncology, autoimmune & inflammatory disorders, rare diseases/orphan disorders, neurology, hematology, infectious diseases, and others.

The oncology segment accounted for the dominant market share in 2025. This is due to the high global burden of cancer and the strong use of advanced specialty drugs in cancer treatment. The segment growth is mainly driven by the rising adoption of targeted therapies, immunotherapies, antibody-drug conjugates, radiopharmaceuticals, and cell therapies across solid tumors and blood cancers. Additionally, oncology drugs often have high treatment value as they are used in serious and life-threatening conditions where patients require specialist care, biomarker testing, and continuous monitoring. The segment is further supported by frequent product approvals, expanded indications, and strong investments by leading pharmaceutical companies in cancer pipelines. Furthermore, the segment is set to hold 31.8% share in 2026.

- For instance, in October 2025, the U.S. FDA approved Zegfrovy for adults with HER2-mutant non-small cell lung cancer who had received prior systemic therapy.

The rare diseases/orphan disorders segment is anticipated to rise with a CAGR of 8.87% over the forecast period.

By Formulation

Higher Use of Injectable and Infusion-Based Therapies Boosted Parenteral Segment Growth

On the basis of formulation, the market is divided into oral and parenteral.

In 2025, the market share was primarily led by the parenteral segment. This is owing to the fact that specialty drugs are commonly administered through intravenous, subcutaneous, or intramuscular routes as they need controlled delivery, better absorption, and specialist supervision. The segment is also supported by the growing launch of convenient subcutaneous versions of major specialty drugs, which reduce treatment time while keeping the benefits of injectable therapy. Furthermore, the segment is set to hold 63.7% share in 2026.

- For instance, in September 2025, Merck announced that the U.S. FDA approved KEYTRUDA QLEX, a subcutaneous injection formulation of pembrolizumab, for adults across most approved solid tumor indications of IV Keytruda.

The oral segment is anticipated to rise with a CAGR of 6.35% over the forecast period.

By End User

Higher Use of Specialist-Led Treatment Led to Hospitals Segment Dominance

Based on end user, the market is segmented into hospitals, specialty clinics & infusion centers, home care/home infusion, and others.

The hospitals segment dominated the market share in 2025. This is mainly as several specialty therapies require physician supervision, infusion support, emergency management, lab testing, imaging, and regular patient monitoring. Additionally, hospitals are the main treatment setting for complex products such as oncology infusions, CAR-T therapies, gene therapies, radiopharmaceuticals, and high-risk biologics. The segment is further supported by the availability of trained specialists, multidisciplinary care teams, pharmacy departments, cold-chain storage, and reimbursement support services within hospitals. Moreover, newly launched specialty drugs often enter the market through hospital-based administration before shifting to outpatient or home-based models. All these factors support the segment's dominance. Furthermore, the segment is set to hold 48.4% share in 2026.

- For instance, in September 2025, Middlesex Health announced the opening of its first specialty pharmacy at the Middlesex Health Cancer Center in partnership with Clearway Health. The hospital-based specialty pharmacy was designed to improve access to medicines for patients with complex and chronic conditions by providing medication education, prior authorization support, refill reminders, home delivery, adherence support, and co-pay assistance.

In addition, home care/home infusion is projected to withness 8.43% growth rate during the forecast period.

Specialty Drugs Market Regional Outlook

By geography, the market is divided into Latin America, Asia Pacific, Europe, North America, and the Middle East & Africa.

North America

North America Specialty Drugs Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America region dominated the global market and attained USD 217.89 billion in 2024. In 2025, the area maintained its dominance, with USD 234.95 billion. North America is growing strongly due to the high specialty drug adoption, strong reimbursement infrastructure, and early access to advanced therapies. The region also benefits from the strong presence of major pharmaceutical companies, rapid FDA approvals, high biologics and cell therapy penetration, and developed specialty pharmacy networks.

U.S. Specialty Drugs Market

The U.S. market led the North American region and is projected to be approximately USD 233.71 billion in 2026, representing about 45.7% of the global market.

Europe

The market in Europe is set to grow at a CAGR of 6.30% during the forecast period. Europe is growing steadily due to strong public healthcare systems, increasing use of biologics, and rising access to specialty therapies through centralized and national reimbursement pathways. The region is also seeing wider biosimilar adoption, which improves affordability and treatment access.

U.K. Specialty Drugs Market

The U.K. market in 2026 is estimated at around USD 25.30 billion, representing roughly 5.0% of global revenues.

Germany Specialty Drugs Market

The German market size is projected to reach approximately USD 27.34 billion in 2026, equivalent to around 5.4% of global sales.

Asia Pacific

The Asia Pacific specialty drugs market size is expected to reach a valuation of USD 99.91 billion by 2026. Asia Pacific is expected to record strong growth due to rising healthcare spending, improving diagnosis rates, and increasing access to advanced therapies in China, Japan, South Korea, Australia, and India. The region has a large patient pool for cancer, autoimmune diseases, infectious diseases, and chronic disorders, creating high demand potential for specialty drugs.

Japan Specialty Drugs Market

The Japanese market in 2026 is estimated at around USD 22.38 billion, accounting for roughly 4.4% of global revenues.

China Specialty Drugs Market

China’s market is projected to reach revenues of around USD 31.07 billion in 2026, representing roughly 6.1% of global sales.

India Specialty Drugs Market

The Indian market in 2026 is estimated at around USD 10.15 billion, accounting for roughly 2.0% of global revenues.

Latin America and Middle East & Africa

The growth in the Latin America and Middle East & Africa regions is anticipated to be moderate in the coming years. The growth is driven by improving access to biologics, oncology drugs, and specialty therapies in major markets, increasing governments' focus on advanced healthcare services, and the emerging market for biosimilars. The Latin America market in 2026 is estimated at around USD 22.28 billion.

In the Middle East & Africa region, the GCC market is projected to reach approximately USD 7.44 billion by 2026, representing about 1.5% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Strong Specialty Portfolios and Strategic Acquisitions by Leading Players Strengthen Their Market Positions

In terms of the competitive landscape, the global specialty drugs market is moderately consolidated, with major pharmaceutical companies having strong portfolios across various disease indications. Notable players in the market include AbbVie Inc., Merck Co., Inc., Amgen Inc., AstraZeneca, Bristol Myers Squibb, Gilead Sciences, and others. The strong focus of these companies on new product development, strategic collaborations, and regulatory approvals is expected to strengthen their market shares.

Other significant entities include Johnson & Johnson, Novartis AG, Pfizer Inc., F. Hoffmann-La Roche Ltd., Sanofi, and others. Owing to strong R&D investment, global commercial reach, advanced biologics capabilities, and continued focus on specialty drug launches, these players are expected to remain highly competitive in the global market.

- For instance, in November 2024, F. Hoffmann-La Roche Ltd. announced a definitive agreement to acquire Poseida Therapeutics, including cell therapy candidates and platform technologies across oncology, immunology, and neurology.

LIST OF KEY SPECIALTY DRUG COMPANIES PROFILED

- AbbVie Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Sanofi (France)

- Amgen Inc. (U.S.)

- Gilead Sciences, Inc. (U.S.)

- AstraZeneca (U.K.)

- Johnson & Johnson (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- Novartis AG (Switzerland)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Novartis AG received the U.S. FDA approval for Cosentyx for pediatric patients aged 12 years and older with moderate to severe hidradenitis suppurativa, expanding the use of its biologic therapy in inflammatory diseases.

- February 2026: Pfizer received the U.S. FDA full approval for BRAFTOVI in combination with cetuximab and fluorouracil-based chemotherapy for first-line BRAF V600E-mutant metastatic colorectal cancer, strengthening its targeted oncology portfolio.

- February 2026: AstraZeneca’s Calquence plus venetoclax was approved in the U.S. as the first all-oral, fixed-duration BTK inhibitor-based regimen for first-line chronic lymphocytic leukemia and small lymphocytic lymphoma.

- October 2025: Takeda entered a global strategic partnership with Innovent Biologics for next-generation oncology medicines, including IBI363, a bispecific antibody fusion protein, and IBI343, an antibody-drug conjugate.

- October 2025: Bristol Myers Squibb announced the acquisition of Orbital Therapeutics, adding OTX-201, an investigational in vivo CAR-T therapy candidate for autoimmune diseases, to its cell therapy portfolio.

REPORT COVERAGE

The global specialty drugs market analysis includes a thorough evaluation of the market size and forecasts for every segment highlighted in the report. It offers insights into the market dynamics and trends expected to drive the market throughout the forecast period. It provides an understanding of essential factors, including technological progress, product innovations, pipeline analysis, the regulatory environment, and the launch of new products. Additionally, it details partnerships, mergers & acquisitions, as well as key developments in the industry within the market. The global market forecast report also provides an in-depth competitive landscape, including information on market share and profiles of key active players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.08% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Molecule Platform, Disease Indication, Formulation, End User, and Region |

| By Molecule Platform |

|

| By Disease Indication |

|

| By Formulation |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 475.00 billion in 2025 and is projected to reach USD 883.00 billion by 2034.

In 2025, the market value stood at USD 234.95 billion.

The market is expected to exhibit a CAGR of 7.08% during the forecast period of 2026-2034.

By molecule platform, the biologics segment led the market.

Increasing use of parenteral therapies, the growing adoption of cell and gene therapies, and the rising role of hospitals, specialty clinics & infusion centers, and home care/home infusion in specialty treatment delivery are primarily driving market expansion.

AbbVie Inc., Merck & Co., Inc., Pfizer Inc., Sanofi, and Amgen Inc. are some of the prominent players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 198

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us