Sickle Cell Disease Treatment Market Size, Share & Industry Analysis, By Treatment Modality [Bone Marrow Transplant, Blood Transfusion, Pharmacotherapy {Hydroxyurea, and Branded Products (Endari, Adakveo, Oxbryta, Zynteglo, PYRUKYND (Mitapivat), CTX001, Inclacumab, MGTA-145, Vamifeport (VIT-2763), ALXN1820, FT-4202, and GBT021601)}], By End-user [Hospitals, Specialty Clinics, and Others], and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

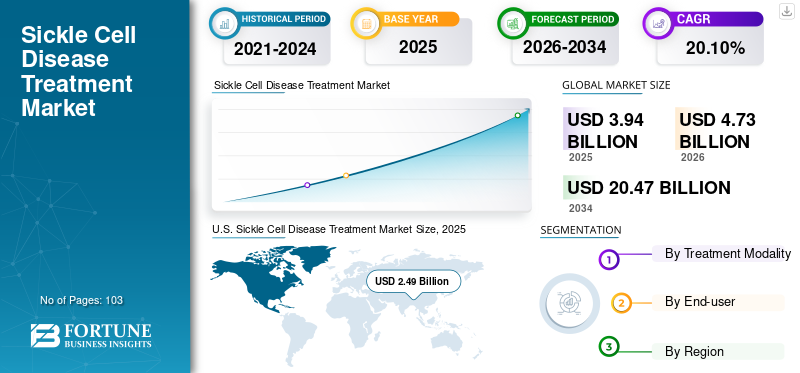

The global sickle cell disease treatment market size was estimated at USD 3.94 billion in 2025 and is projected to reach USD 4.73 billion in 2026 to USD 20.47 billion by 2034, growing at a CAGR of 20.10% from 2026 to 2034. United States dominated the sickle cell disease treatment market with a market share of 63.35% in 2025.

Sickle Cell Disease (SCD) is an inherited disorder causing diseases, such as hemoglobin sickle cell disease, hemoglobin SS disease, sickle cell anemia, and others causing deformation of red blood cells. This leads to early death of cells, causing blood shortage, and also inhibits blood flow, causing blockage. The treatment procedure includes blood transfusions, medication, and bone marrow transplants.

The global sickle cell disease treatment market growth is attributed to the increasing prevalence of SCD, rising awareness regarding the disease, and increasing focus of the key players on launching new effective drugs for sickle cell disease treatment.

- In February 2022, Agios Pharmaceuticals, Inc. announced the U.S. Food and Drug Administration (FDA) approval for its product PYRUKYND (mitapivat) for the treatment of hemolytic anemia in adults with Pyruvate Kinase (PK) deficiency, a rare, debilitating, lifelong hemolytic anemia.

Download Free sample to learn more about this report.

Global Sickle Cell Disease Treatment Market Snapshot & Highlights

Market Size & Forecast:

- 2025 Market Size: USD 3.94 billion

- 2026 Market Size: USD 4.73 billion

- 2034 Forecast Market Size: USD 20.47 billion

- CAGR: 20.10% from 2025–2034

Market Share:

- Region: The United States dominated the market with a 63.35% share in 2025. This is driven by better access to treatment, potential pipeline candidates, strong government support, and rising collaborations to improve disease management.

- By Treatment Modality: The Blood Transfusion segment held the largest market share. The segment's dominance is attributed to its high efficiency in managing severe symptoms of SCD, such as stroke, which increases the demand for this treatment modality.

Key Country Highlights:

- Japan: As part of the fast-growing "Rest of the World" region, Japan's market is driven by an increasing number of clinical trials and the introduction of new therapies, which is expanding the treatment options available in the country.

- United States: The market is fueled by a significant patient population, with almost 100,000 Americans impacted by SCD. The market is also supported by a high number of new drug approvals from the U.S. FDA and a strong pipeline of gene therapies and other novel treatments.

- China: Growth is supported by an increasing prevalence of the disease, rising awareness, and a growing focus from major pharmaceutical companies on expanding their presence and introducing new therapies in the Asia Pacific region.

- Europe: The market is advanced by a growing patient population and favorable reimbursement policies. Key players are also focusing on expanding the availability of their products in the region, such as Novartis AG's efforts to increase access to its Africa Sickle Cell Disease program.

Sickle Cell Disease Treatment Market TRENDS

Increasing Gene Therapy Adoption Bolstered the Development of Effective SCD Treatments

Gene therapy has emerged as the ultimate cure for various chronic diseases. In the case of hereditary diseases, gene therapy is a revolution that targets the root cause of a disease. With increasing research on the correction of genetic mutation for the treatment of the disease, market players have shifted their R&D focus toward gene therapy.

- For instance, in February 2018, David Williams, in collaboration with Boston Children's Hospital, started a clinical study to determine the feasibility and safety of administering a lentiviral gene transfer vector encoding a small hairpin (sh) RNA targeting the γ-globin gene repressor, BCL11A, in patients with severe SCD. The study is currently in the phase 1 trial and is expected to be completed in April 2024.

Similarly, CRISPR Therapeutics and Vertex Pharmaceuticals have been conducting clinical trials on CRISPR-Cas9 gene-edited therapy CTX001. It is currently in phase 3 clinical and is estimated to be completed in October 2024. Positive clinical studies on CTX001 suggest that the pipeline candidate can become a blockbuster drug when it is launched in the market. Due to this factor, the global market is expected to witness growth in the coming years.

Download Free sample to learn more about this report.

SICKLE CELL DISEASE TREATMENT MARKET GROWTH FACTORS

Increasing Prevalence along with High Severity Related to the Disease to Surge the Demand for Effective Treatment Procedures

Globally, millions of people are affected by sickle cell disease. The growing prevalence of sickle cell disease is driving market expansion.

- For instance, in May 2022, SCD impacted almost 100,000 Americans, according to the Centers for Disease Control and Prevention (CDC).

Youngsters and adults with sickle cell disease frequently experience the extreme consequence known as Vaso-occlusive Crisis (VOC). The increasing need for emergency medical care among patients due to sudden acute discomfort instances is boosting market expansion.

- According to the National Center for Biotechnology Information’s (NCBI) research study in 2021, patients who suffer from the disease can encounter up to 18 VOCs yearly.

Increasing emphasis on the introduction of drugs to decrease the acuteness of these illnesses by leading market players is supporting market expansion.

- For instance, in November 2019, the Food and Drug Administration (FDA) accelerated the approval of Pfizer’s Oxbryta, indicated for adult patients who have sickle cell disease and children aged 12 and above. In 2021, the FDA approved the expanded use of drugs for patients aged 4 and older in the U.S.

The increasing prevalence of SCD and the efficacy of the products for the disease treatment in reducing the chances of VOCs are increasing its adoption among patients.

Advent of Novel Treatment Solutions to Contribute to Market Growth

Prior, only bone marrow transplantation and blood transfusion were included in SCD management. The growing incidence of sickle cell disease and increasing awareness about it boosted the adoption of efficient treatment procedures.

Major players increased their focus on the launch of new products for the treatment of this disease and to meet the demands of the patients.

- For instance, in 2017, the FDA approved Emmaus Life Sciences' drug Endari for sickle cell disease patients aged five years and older. Until then, there was limited focus on innovation for developing a treatment for the disease, as Endari was the first branded drug approved in decades.

After the launch of Endari, a few more companies emerged in the market with new product launches, including Oxbryta (Global Blood Therapeutics), Adakveo (Novartis), Zynteglo (bluebird bio, Inc.), and PYRUKYND (Agios Pharmaceuticals, Inc.).

Additionally, by offering quick product approvals, the FDA and European Medicines Agency (EMA) are also playing a major role. The FDA grants fast approval to medications for severe illnesses to address an unmet medical need.

- In November 2019, three months prior to the legally required time for agency action, Global Blood Therapeutics (Pfizer Inc.) reported that the FDA had approved Oxbryta.

The growing prevalence of SCD and the expected new drug introductions are anticipated to foster market growth over the forecast period.

RESTRAINING FACTORS

Lack of SCD Treatment Options in Emerging Countries to Limit Market Growth

The pharmacotherapy of sickle cell disease treatment consists of hydroxyurea and a few branded drugs. Hydroxyurea is considered the first line of disease treatment and is recommended by many healthcare professionals. However, the lack of availability of treatment options in the developing countries across the globe stands out as a restraining factor.

- According to the American Society of Hematology, in the Sub-Saharan Africa region, almost 300,000 babies are born with SCD every year. Despite the inclusion of hydroxyurea in the WHO Model List of Essential Medicines for Children, it remains unavailable in the region. Also, the drug is considered to be too expensive in Africa.

Moreover, blood transfusions for SCD management are also dependent on donor availability. There are chances of inappropriate screening, leading to increased blood transfusion-transmitted infections, even though donors are accessible.

Public and private funding in African countries is insufficient to improve the healthcare facilities and care required by patients suffering from the disease.

Furthermore, combined with the lack of awareness about the disease among the population in emerging economies can limit the global market growth during the forecast period.

SEGMENTATION ANALYSIS

By Treatment Modality Analysis

Blood Transfusion Segment Led Backed by its Efficiency in Treatment Modality for Stroke Management

The market is divided into blood transfusion, bone marrow transplant, and pharmacotherapy, in terms of treatment modality. The pharmacotherapy segment is segregated into branded products and hydroxyurea.

The blood transfusion segment generated the highest revenue in 2022 and is expected to grow at a stagnant CAGR during the forecast period, . Blood transfusion is the most efficient treatment method to manage strokes, which is one of the severe symptoms of SCD. The increasing number of episodes of strokes among SCD patients has increased the blood transfusion treatment demand. This factor is responsible for the segment’s dominance.

Furthermore, the pharmacotherapy segment is expected to grow at the fastest CAGR during the forecast period. The high growth rate of the segment is due to the launch of new branded pharmacotherapy drugs and increasing government initiatives on early launches of these drugs, contributing 45.05% globally in 2026. Moreover, limited treatment options currently available in the market are also responsible for the segment’s growth in the forecast period. The government in countries, such as the U.S., India, and others supports research activities for sickle cell disease treatment through funding and designations such as orphan drugs, fast track, and priority review, among others. These factors are expected to accelerate the introduction of new labeled pharmacotherapy drugs and provide significant momentum to the pharmacotherapy segment.

- For instance, in India, the National Sickle Cell Anaemia Elimination Program introduced in the Union Budget 2023, focused on addressing significant health problems such as sickle cell disease, specifically in the tribal population of the country.

To know how our report can help streamline your business, Speak to Analyst

By End-user Analysis

Hospitals Segment Dominated Attributable to Rising Prevalence of Patients Visiting Hospitals

Based on end-user, the market is segmented into hospitals, specialty clinics, and others.

The hospitals segment held significant global sickle cell disease treatment market share in 2022. The large share of the segment is attributed to the increasing prevalence of SCD and the rising number of hospital admissions for sickle cell disease treatment.

- According to the WHO, around 20-25 million people are living with the disease across the globe. Moreover, the number of patients is projected to increase by 30% by 2050, thereby facilitating the hospital segment’s growth.

The specialty clinics segment is estimated to grow at a significant CAGR during the forecast period. This segment’s growth is attributable to the increasing number of specialty clinics providing sickle cell disease treatment and care.

REGIONAL ANALYSIS

U.S. Sickle Cell Disease Treatment Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

U.S.

U.S. dominated the market with a valuation of USD 2.49 billion in 2025 and USD 3.00 billion in 2026. U.S. dominated the global market with a share of 63.35% in 2025. The dominance of the market in the country is attributed to better access to SCD treatment, potential pipeline candidates, strong government support, and rising collaborations to improve the treatment of the disease.

- In December 2019, Global Blood Therapeutics, Inc. announced a research collaboration with Syros Pharmaceuticals Inc. to develop and commercialize novel therapies for SCD and beta-thalassemia.

Europe

Europe accounted for a significant market share in 2022 and is projected to witness a considerable growth during the forecast period. The market growth in Europe is attributed to favorable reimbursement policies, increasing prevalence of the disease, and increasing market players’ emphasis on the expansion of their offerings in the region.

- According to the data from the European Medicines Agency, in 2019, around 1 in 10,000 people lived with the disease in the European Economic Area (EEA).

Middle East & Africa

The market in the rest of the world is expected to expand at a significant CAGR in the projected years. Market expansion in the region is driven by the highest SCD incidence in the Middle East & Africa, the Mediterranean regions, and South America and rising disposable income. Moreover, the increasing awareness about SCD and the strong pipeline of branded drugs are also expected to fuel the market growth in the region.

KEY INDUSTRY PLAYERS

Companies with Strong Sickle Cell Disease Treatment Sales to Dominate the Competition

Global Blood Therapeutics Inc. (Pfizer Inc.), Novartis AG, and Emmaus Medical, Inc. are the prominent players in the market and captured a considerable global market share in 2022.

Global Blood Therapeutics Inc. (Pfizer Inc.) accounted for a significant market share in 2022 due to the company’s strong sales from Oxbryta for SCD treatment.

- For instance, Oxbryta generated a revenue of USD 195.0 million in 2021, experiencing an increase of 57.5% in its sales from the prior year.

Similarly, Novartis AG held a considerable share of the market in 2022 due to increasing focus on partnerships with several government organizations. This partnership may allow the company to address the unmet needs of the patient population. Moreover, the company’s emphasis on the expansion of the availability of its product globally is also responsible for its significant position in the market.

- In June 2020, Novartis AG announced the expansion of the Africa Sickle Cell Disease program to East Africa with two new memoranda of understanding with the Ministries of Health of Uganda and Tanzania. The program aims to improve and extend the lives of people with SCD in sub-Saharan Africa.

Furthermore, the blood transfusion segment also generated significant revenues due to increasing SCD complications, such as stroke, which can be prevented through blood transfusion therapy.

LIST OF KEY COMPANIES IN SICKLE CELL DISEASE TREATMENT MARKET:

- Bristol-Myers Squibb Company (U.S.)

- Addmedica (France)

- Novartis AG (Switzerland)

- Global Blood Therapeutics, Inc. (Pfizer Inc.) (U.S.)

- Emmaus Medical, Inc. (U.S.)

- bluebird bio Inc. (U.S.)

- Agios Pharmaceuticals, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- March 2023 - AddMedica partnered with Abacus Medicine Pharma Services for the distribution of Siklos (hydroxyurea) in Belgium, the Netherlands, and Luxembourg. The therapy is indicated for patients aged 2 years and above.

- August 2022 - To assist rapid access to ZYNTEGLO, including an advanced, outcomes-based contract offering and a comprehensive patient support program, bluebird bio Inc. released details of its U.S. commercial infrastructure.

- November 2021 – Emmaus Life Sciences, Inc. announced its partnership with UpScript IP Holdings, LLC. (UpScript), to offer telehealth solutions to the patients, expanding access to Endari.

- October 2020 – Novartis AG announced the approval of Adakveo by the European Commission (EC) to prevent recurrent vaso-occlusive crises (VOCs) in sickle cell disease patients aged 16 years and older.

- September 2020 – To dispense Oxbryta in Kuwait, Qatar, Bahrain Saudi Arabia, Oman, and the United Arab Emirates, Global Blood Therapeutics, Inc. made an exclusive agreement with Biopharma-MEA.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

The market research report provides a detailed competitive landscape. It includes the prevalence of sickle cell disease and key industry developments such as partnerships, mergers, and acquisitions. Additionally, it focuses on key points such as new product launches in the market. Furthermore, the report covers regional analysis of different segments and company profiles of key sickle cell disease treatment players, including business overview, financial data, and SWOT analysis for each company. Moreover, the report includes market trends and the impact of COVID-19 on the market. The report consists of quantitative and qualitative insights contributing to the market's growth.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 20.10% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Treatment Modality, End-user, and Geography |

|

By Treatment Modality |

|

|

By End-user

|

|

|

By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 4.73 billion in 2026 and is projected to reach USD 20.47 billion by 2034.

The market is expected to exhibit a CAGR of 20.10% during the forecast period (2026-2034).

The pharmacotherapy segment is set to lead the market by treatment modality.

The key factors driving the market are the wave of innovation in SCD therapeutics, increasing prevalence of SCD, and approval of advanced pharmacotherapy drugs to manage the disease.

Global Blood Therapeutics Inc. (Pfizer Inc.), Novartis AG, and Emmaus Medical, Inc. are the top players in the market.

- 2021-2034

- 2025

- 2021-2024

- 103

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us