Inorganic Acids Market Size, Share & Industry Analysis, By Type (Sulfuric Acid, Phosphoric Acid, Nitric Acid, Hydrochloric Acid, Boric Acid, Hydrofluoric Acid, Sulfamic Acid, Perchloric Acid, and Others), By Application (Fertilizers & Agrochemicals, Chemical Manufacturing, Metal Processing & Electroplating, Petroleum Refining, Glass & Ceramics, and Others), and Regional Forecast, 2026-2034

Inorganic Acids Market Size and Future Outlook

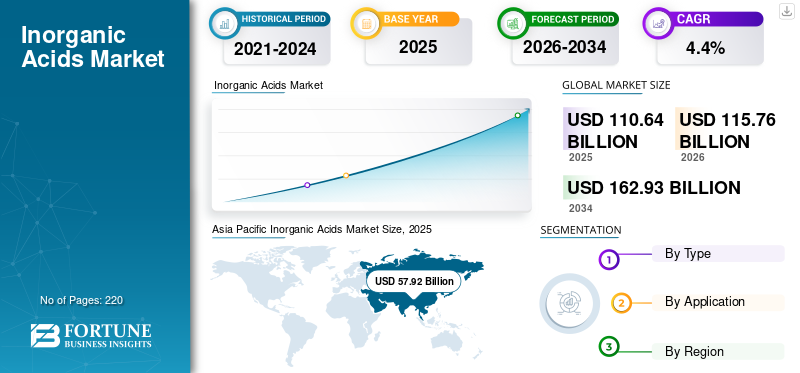

The global inorganic acids market size was valued at USD 110.64 billion in 2025 and is projected to grow from USD 115.76 billion in 2026 to USD 162.93 billion by 2034, exhibiting a CAGR of 4.4% during the forecast period. Asia Pacific dominated the inorganic acids market with a market share of 52.34% in 2025.

Inorganic acids are mineral-based acids derived primarily from inorganic compounds and widely used across industrial manufacturing processes. Key inorganic acids include sulfuric acid, phosphoric acid, nitric acid, hydrochloric acid, boric acid, hydrofluoric acid, sulfamic acid, perchloric acid, and others. These acids serve as essential raw materials in fertilizers, petroleum refining, chemical synthesis, metal treatment, and glass production. Sulfuric acid is the largest-volume product globally due to its extensive use in phosphate fertilizers and industrial processing. Rising global food demand, expanding chemical manufacturing capacity, and infrastructure development are all significantly supporting market growth. Additionally, increasing industrialization in emerging economies continues to drive acid consumption across multiple sectors. As inorganic acids remain fundamental intermediates in industrial chemistry, their demand closely tracks economic and industrial activity, thus reinforcing stable long-term market expansion. The key players operating the market are BASF SE, The Mosaic Company, Nutrien Ltd., Yara International ASA, and OCP Group.

Download Free sample to learn more about this report.

Inorganic Acids Market Trends

Industrial Expansion and Fertilizer Demand Reshaping Production Patterns

The market is evolving alongside agricultural intensification and the expansion of the chemical industry. A major trend is the modernization of acid production facilities to improve energy efficiency and reduce emissions. Increasing demand for phosphate-based fertilizers continues to influence sulfuric and phosphoric acid production volumes. Additionally, petroleum-refining upgrades are boosting demand for hydrochloric and nitric acids. Specialty inorganic acids, such as hydrofluoric and boric acids, are witnessing steady growth driven by demand from semiconductor and glass manufacturing. Governments are also enforcing stricter environmental standards, encouraging the adoption of cleaner production technologies. These operational and regulatory shifts are reshaping manufacturing strategies, thus influencing future growth trajectories in the global market.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Fertilizer Production and Industrial Manufacturing Sustaining Demand Growth

The primary driver of the market is the sustained demand for fertilizers, particularly phosphate-based products. Sulfuric acid is widely used in fertilizer manufacturing, making agriculture a key demand anchor. Additionally, nitric acid plays a vital role in nitrogen-based fertilizers and explosives. Expanding chemical manufacturing industries further consume hydrochloric and sulfuric acids for intermediate production. Growing metal processing activities and petroleum refining capacity also support steady acid consumption. Rapid urbanization and infrastructure development reinforce industrial demand patterns. These interconnected agricultural and industrial factors ensure consistent product consumption, thus maintaining steady inorganic acids market growth.

MARKET RESTRAINTS

Environmental Regulations and Hazardous Handling Requirements Limiting Operational Flexibility

Inorganic acids are hazardous substances requiring stringent safety and environmental controls during production, storage, and transportation. Compliance with emission regulations and waste management standards increases operational costs. Additionally, volatility in raw material and energy prices impacts profitability. Accidental leaks and environmental contamination risks further create regulatory scrutiny. Transportation limitations for highly corrosive acids also constrain supply chain flexibility. These regulatory and operational challenges increase capital expenditure and compliance burdens, hence moderating growth momentum in certain regions.

MARKET CHALLENGES

Sustainability Pressures and Capacity Overhang Negatively Impacting the Market Dynamics

A major challenge facing the market is balancing large-scale production with environmental sustainability goals. Acid manufacturing processes are energy-intensive and generate emissions requiring mitigation technologies. In some regions, overcapacity in sulfuric acid production leads to price competition and margin pressure. Additionally, stricter carbon reduction targets compel producers to invest in cleaner technologies. Ensuring safe storage and transport infrastructure also requires continuous capital investment. These environmental and economic pressures shape competitive strategies, therefore influencing long-term market stability.

MARKET OPPORTUNITIES

Agricultural Intensification and Infrastructure Development Creating Growth Potential

The growing global population and food security concerns create significant opportunities for inorganic acids used in fertilizer. Sulfuric and phosphoric acids remain critical inputs in phosphate fertilizer production. Infrastructure development in emerging economies further increases demand for acids in construction materials and metal processing. Expansion of renewable energy and electronics manufacturing supports specialty acid consumption. Additionally, industrial diversification in Asia, the Middle East & Africa opens new production and export opportunities. Technological advancements in acid recovery and recycling processes also create avenues for efficiency-driven growth. These structural economic drivers support long-term expansion, therefore strengthening investment potential in the market.

Research and Development

R&D efforts focus on improving production efficiency, reducing emissions, and enhancing acid recovery systems. Advanced catalyst technologies and waste heat recovery systems are gaining adoption. Innovations in recycling and the integration of the circular economy support sustainable growth.

Segmentation Analysis

By Type

Fertilizer Production Driving Volume Dominance of Sulphuric Acid Segment

Based on type, the market is segmented into sulfuric acid, phosphoric acid, nitric acid, hydrochloric acid, boric acid, hydrofluoric acid, sulfamic acid, perchloric acid, and others.

Sulfuric acid holds the largest inorganic acids market share globally due to its critical role in phosphate fertilizer production. It is also widely used in petroleum refining, wastewater treatment, and metal processing. The acid’s strong dehydrating and oxidizing properties make it a versatile industrial intermediate. Growing global food demand and agricultural intensification are driving significant increases in sulfuric acid consumption. Additionally, its use in chemical synthesis and battery manufacturing reinforces steady industrial demand. Large-scale production capacity and integrated supply chains sustain its cost competitiveness. These structural agricultural and industrial applications ensure sustained high-volume consumption, thus maintaining sulfuric acid’s dominant market position.

Phosphoric acid is primarily used in the production of phosphate fertilizers such as DAP and MAP. Rising global population and food security concerns drive demand for high-yield agricultural inputs. In addition to fertilizers, phosphoric acid is used in food-grade applications and beverage processing. Industrial uses include detergents and surface treatment chemicals. Increasing agricultural modernization in emerging economies supports consistent consumption. Although production volumes are lower than those of sulfuric acid, a strong linkage to fertilizer demand ensures stability. These agricultural and food-related drivers sustain steady growth, hence reinforcing phosphoric acid’s importance in the market. The segment is growing at a CAGR of 4.8% during the forecast period.

By Application

To know how our report can help streamline your business, Speak to Analyst

Global Food Security and Yield Improvement Driving Dominant Demand from Fertilizers & Agrochemicals Segment

In terms of application, the market is segmented into fertilizers & agrochemicals, chemical manufacturing, metal processing & electroplating, petroleum refining, glass & ceramics, and others.

Fertilizers & agrochemicals represent the largest application segment for inorganic acids. Sulfuric, phosphoric, and nitric acids are essential in producing phosphate and nitrogen fertilizers. The growing global population and the need to increase agricultural productivity significantly support demand. Developing regions investing in agricultural modernization further reinforce consumption. Seasonal planting cycles and government subsidy programs influence production volumes. Despite fluctuations in raw-material prices, fertilizer demand remains structurally strong. These agricultural fundamentals sustain large-scale acid consumption, thus maintaining fertilizers as the dominant application segment.

The chemical manufacturing segment is growing at a CAGR of 4.7% during the forecast period. Inorganic acids serve as key intermediates in the synthesis of dyes, pigments, plastics, detergents, and specialty chemicals. Expanding industrial output in emerging economies supports steady acid consumption. Chemical diversification and downstream integration enhance production stability. Additionally, growth in specialty chemicals and pharmaceuticals increases demand for high-purity acids. Continuous chemical processing operations ensure consistent usage levels. These industrial manufacturing requirements create sustained demand, hence reinforcing chemical manufacturing as a core application segment.

INORGANIC ACIDS MARKET REGIONAL OUTLOOK

By geography, the market is segmented into Asia Pacific, North America, Europe, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Inorganic Acids Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the global market and was stood at USD 57.92 billion in 2025 due to strong fertilizer production and rapid industrialization. China and India represent major consumers and producers of sulfuric, phosphoric, and nitric acids, supported by large-scale agricultural activity and government-backed food security initiatives. Expanding chemical manufacturing hubs and further growth in steel production further reinforce demand for hydrochloric and sulfuric acids. Additionally, semiconductor and electronics manufacturing in China, Japan, and South Korea increases specialty acid consumption, including hydrofluoric acid. Infrastructure development and urbanization also contribute to metal processing and refining activity. Strong domestic production capacity and integrated supply chains enhance cost competitiveness across the region. These structural agricultural and industrial drivers collectively sustain high consumption levels, thereby reinforcing Asia Pacific’s leadership in the global market.

China Inorganic Acids Market

The China market reached a valuation of USD 28.07 billion in 2025, accounting for approximately 25.4% of regional revenues. Growth is driven by large-scale fertilizer production, strong chemical manufacturing capacity, expanding semiconductor, and metal processing industries.

To know how our report can help streamline your business, Speak to Analyst

North America

North America market is mature yet stable market, driven by advanced manufacturing and consistent agricultural output. The U.S. plays a key role in fertilizer production, supporting the consumption of sulfuric and nitric acids. Additionally, strong chemical manufacturing, petroleum refining, and metal processing industries sustain steady demand for hydrochloric and sulfuric acids. Environmental regulations have encouraged modernization of production facilities, leading to improved process efficiency and emission control. The electronics and aerospace industries also support specialty acid demand.

U.S. Inorganic Acids Market

The U.S. market was valued at USD 15.48 billion in 2025, accounting for approximately 14.0% of North America revenues. Stable fertilizer production, advanced petroleum refining operations, and strong chemical manufacturing output fuel growth.

Europe

In Europe, the market is expected to be shaped by stringent environmental regulations and advanced industrial activity. Germany, France, and the U.K. maintain strong chemical manufacturing and engineering sectors, supporting demand for sulfuric, nitric, and hydrochloric acids. Fertilizer consumption remains stable due to agricultural requirements, although sustainability policies influence production practices. The increased focus on green chemistry and emission-reduction technologies has led to the modernization of acid manufacturing facilities.

Germany Inorganic Acids Market

Germany’s market reached a valuation of USD 3.45 billion in 2025, accounting for approximately 3.1% of regional demand. High-value chemical production, advanced engineering industries, and specialty acid consumption drive demand.

Latin America and Middle East & Africa

Latin America demonstrates moderate growth in the market, primarily driven by agricultural expansion and mining operations. Brazil and Argentina are major fertilizer-consuming countries, supporting demand for sulfuric and phosphoric acids. The mining sector also relies on sulfuric acid for metal extraction processes, particularly copper and other base metals. On the other hand, the Middle East & Africa region is witnessing steady growth, supported by petrochemical expansion and the development of fertilizer production capacity. GCC countries are investing in downstream chemical manufacturing, including sulfuric and phosphoric acid production linked to phosphate reserves. Growing infrastructure and refining projects further increase hydrochloric and sulfuric acid consumption. In Africa, agricultural modernization initiatives are gradually boosting demand for fertilizer-related acids. Additionally, mining activities in selected countries contribute to sulfuric acid usage.

GCC Inorganic Acids Market

The GCC market was valued at USD 3.34 billion in 2025, accounting for approximately 7.0% of Latin America revenues. Expansion is driven by phosphate-based fertilizer production, petrochemical diversification, and downstream chemical investments.

Competitve Landscape

Key Industry Players

Vertical Integration and Feedstock Access Strengthening Market Positioning

The global inorganic acids market is characterized by the presence of large, vertically integrated chemical and fertilizer producers. Competition is driven primarily by access to raw materials such as sulfur, phosphate rock, and ammonia, along with energy cost efficiency. Major players operate integrated production facilities that link acid manufacturing with downstream fertilizer and chemical operations, providing cost advantages. Regional producers compete based on export capacity and feedstock availability. Environmental compliance and emission control technologies increasingly influence competitive positioning. High capital intensity and strict safety regulations create strong entry barriers, therefore reinforcing the dominance of established multinational producers in the global market.

LIST OF KEY INORGANIC ACIDS COMPANIES PROFILED IN REPORT

- BASF SE (Germany)

- The Mosaic Company (U.S.)

- Nutrien Ltd. (Canada)

- Yara International ASA (Norway)

- OCP Group (Morocco)

- CF Industries Holdings, Inc. (U.S.)

- Sinopec Corporation (China)

- Solvay S.A. (Belgium)

- ICL Group Ltd. (Israel)

- Raviraj Group (India)

KEY INDUSTRY DEVELOPMENTS

- March 2026: ICL Group announced the opening of a new specialty fertilizer manufacturing facility in India through its Growing Solutions division. The plant is designed to produce advanced water-soluble fertilizers and specialty nutrition products tailored to local agricultural needs. The investment strengthens ICL’s presence in the Indian market and enhances its ability to serve regional farmers with customized crop nutrition solutions. The facility supports the company’s strategy to expand its specialty fertilizer portfolio and reinforce its global supply network.

- April 2025: BASF announced plans to expand its sulfuric acid regeneration capacity at its Ludwigshafen site in Germany. The investment will increase processing capacity for spent sulfuric acid from chemical and refining customers. The project includes construction of a new regeneration plant and is expected to start up in 2027. BASF stated that the expansion will support growing customer demand while contributing to resource efficiency by recovering sulfuric acid for reuse in production processes.

- January 2025: Dyno Nobel is investing USD 8 million in a new tertiary abatement project at its Louisiana, Missouri facility to significantly reduce greenhouse gas (GHG) emissions. The project is part of Dyno Nobel's commitment to sustainability and aims to reduce operational GHG emissions. The abatement system is designed to convert nitrous oxide emissions from nitric acid manufacturing into nitrogen and oxygen.

- November 2023: Enaex S.A. has announced that they are the first manufacturing company to produce carbon-neutral ammonium nitrate in Latin America. The company has implemented significant improvements at its nitric acid plant near Cuzco in Peru to reduce greenhouse gas emissions.

- October 2023: CF Industries plans a USD 75 million investment in its Donaldsonville Nitrogen Complex in Louisiana, aiming to boost production of both merchant-grade nitric acid and Diesel Exhaust Fluid (DEF). The project focuses on upgrades to the Nitric Acid No. 3 plant and improvements to the DEF Unit. Specifically, the Nitric Acid plant will be modified to produce 65% nitric acid, an increase from the current 60% strength.

- July 2023: Nutrien has successfully completed a turnaround project at its Geismar, Louisiana nitrogen facility, aiming to ensure reliable operations and contribute to a more sustainable future. In addition to the direct economic and operational benefits, a voluntary environmental abatement project undertaken during the turnaround is expected to reduce CO2e emissions by approximately 200,000 tons per year, from the highest production levels at the nitric acid manufacturing unit.

- January 2023: BASF monomers division, which includes MDI, TDI, propylene oxide, caprolactam, adipic acid, polyamide 6 and 6.6, and nitric acid, is planning to expand its product portfolio with a lower CO2 footprint. This expansion will help the company reach net-zero CO2 emissions by 2050.

REPORT COVERAGE

The global inorganic acids market research report provides a detailed analysis of the market and highlights key aspects, including leading companies, products, and market trends. Also, it offers insights into market trends and highlights vital industry developments. In addition to the factors mentioned above, the report encompasses various factors contributing to the market's growth in recent years. It further includes historical data & forecasts revenue growth at global, regional, and country levels and analyzes the industry's latest market dynamics and opportunities.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion) and Volume (Million Tons) |

| Growth Rate | CAGR of 4.4% from 2026 to 2034 |

| Segmentation | By Type, Application, and Region |

| By Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 110.64 billion in 2025 and is projected to reach USD 162.93 billion by 2034.

In 2025, the Asia Pacific’s market size stood at USD 57.92 billion.

Registering a CAGR of 4.4%, the market will exhibit steady growth during the forecast period (2026-2034).

The fertilizers & agrochemicals segment led the market in 2025.

Fertilizer production and industrial manufacturing sustaining demand growth.

BASF SE, The Mosaic Company, Nutrien Ltd., Yara International ASA, and OCP Group are the major players in the market.

Asia Pacific held the highest market share in 2025.

Growing agriculture industry to aid product adoption.

- 2021-2034

- 2025

- 2021-2024

- 220

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us