Integrated Air and Missile Defense Market Size, Share & Industry Analysis, By Platform (Land-Based, Naval-Based, and Airborne / Space-Enabled Sensing), By Component (Sensors & Radar, Battle management / C2, Launchers, Interceptors & Effectors, and Others), By Threat type (Aircraft & Helicopters, UAS / Loitering Munitions, Cruise missiles, Ballistic missiles, and Others), By Range layer (VSHORAD, SHORAD, Medium range, and Long range / Upper Tier), By End User (Homeland Defense, Military Base Defense, Expeditionary / Force protection, and Others), and Regional Forecast, 2026-2034

Integrated Air and Missile Defense Market Size and Future Outlook

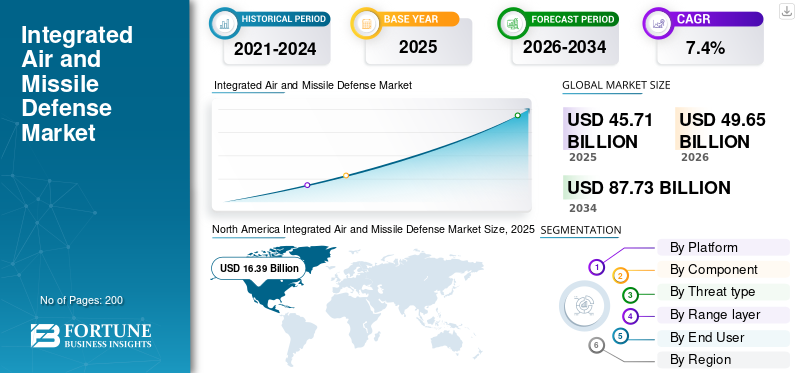

The global integrated air and missile defense market size was valued at USD 45.71 billion in 2025. The market is projected to grow from USD 49.65 billion in 2026 to USD 87.73 billion by 2034, exhibiting a CAGR of 7.4% during the forecast period. North America dominated the integrated air and missile defense market with a market share of 35.85% in 2025.

The Integrated Air and Missile Defense (IAMD) market covers the systems, sensors, interceptors, radars, and command networks used to detect, track, and defeat a wide range of aerial threats. It brings together ground based assets with terrestrial, airborne and space-enabled sensing to counter aircraft, UAVs, cruise missiles, and ballistic threats across medium range and long range layers. The market growth is being driven by rising missile threats, stronger demand for layered defense, and defense modernization programs across North America, the Middle East, and Asia Pacific.

Key players in this market are Lockheed Martin and Rafael Advanced Defense Systems, these companies are changing the market through system upgrades, integration work, and advanced air defense programs. Lockheed Martin is making air and missile defense systems that are more connected and work together by integrating interceptors and battle networks. Rafael advanced defense systems, provides missile defense systems that have been proven to work against rockets, UAVs, and cruise missiles. Major Players focus on system development and are pushing the market toward more integrated, multi-layer, and operationally responsive solutions.

Download Free sample to learn more about this report.

INTEGRATED AIR AND MISSILE DEFENSE MARKET TRENDS

Shift toward Networked, Multi-Layer, and 360-Degree Defense Architecture is Becoming a Major Trend

One of the significant trends in the global market is the shift from stand-alone interceptor systems toward fully networked architectures that connect sensors, radars, launchers, interceptors, and battle management into one operational framework. Defense agencies increasingly want systems that can fuse terrestrial, airborne and space-enabled inputs, improve target discrimination, and support layered defense against aerial threats ranging from drones and cruise missiles to ballistic targets across medium range and long range engagement layers. Resulting, market demand is steadily shifting toward open-architecture command-and-control, integrated fire control, and multi-domain interoperability rather than isolated hardware procurement alone.

In September 2025, the U.S. Missile Defense Agency and the U.S. Army issued the Record of Decision to implement the Enhanced Integrated Air and Missile Defense (EIAMD) system on Guam, describing it as a persistent 360-degree layered Integrated Air Missile Defense capability.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rapid Growth in Ballistic, Cruise Missile, and Drone Threats is Accelerating Market Growth

A major driver for the global integrated air and missile defense market growth is the rise in complex aerial threat environments, where militaries now need to defend against ballistic missiles, cruise missiles, UAVs, and increasingly maneuverable long-range weapons within the same battle space. That threat mix is pushing procurement away from stand-alone air defense units toward networked, layered defense architectures that combine sensors, command systems, and interceptors across short, medium, and long-range engagement layers. Moreover, the market is growing as countries no longer want isolated missile defense systems, they look for systems with integrated, multi-layer protection that can respond faster and cover more threat types at once.

In January 2026, the U.S. Defense Security Cooperation Agency announced a possible USD 9.0 billion Foreign Military Sale to Saudi Arabia for PATRIOT Advanced Capability-3 Missile Segment Enhancement missiles and related equipment.

MARKET RESTRAINTS

High Integration Complexity and Rising Lifecycle Costs are Restraining Faster Deployment of Integrated Air and Missile Defense Systems

The sheer complexity of integrating radars, launchers, interceptors, sensors, and command networks into one reliable operational architecture is a major restraint in the global market. Countries need layered defense against aerial threats, but building a system that links ground based assets with terrestrial, airborne and space-enabled sensing is expensive, technically challenging, and time-consuming. Furthermore, the market growth is restrained by the buyers need for interoperability across legacy and new platforms, resulting in delay procurement, testing, and full-scale fielding of air and missile defense systems.

In June 2025, the U.S. Government Accountability Office reported that the Army’s air and missile defense modernization efforts had grown from USD 8.8 billion to USD 11.8 billion in budget requests from fiscal 2021 to 2025, while also noting that the Army had not fully applied leading product-development practices across these efforts.

MARKET OPPORTUNITIES

Multinational Modernization and Export-Led Procurement Programs are Creating a Strong Market Opportunity

Major opportunity in the global market lies in the growing number of allied countries moving to modernize air defense through interoperable, multi-layer, and open-architecture systems. This creates opportunity for both new interceptor and radar sales, and also for battle management software, sensor fusion, command networks, launcher integration, and long-term upgrade programs. Moreover, the opportunity is growing as more countries now want scalable integrated air missile defense architectures that can connect legacy assets with newer missile defense systems across short-, medium-, and long range layers.

MARKET CHALLENGES

Cost-Exchange Imbalance Against Low-Cost Drones and Saturation Attacks is Emerging as a Major Challenge for Market Growth

A major challenge in the global market is the growing misalliance between low-cost incoming threats and the high cost of defeating them with premium interceptors. Additionally, as drones are becoming more affordable, networked, and available at scale, militaries are being forced to invest highly to protect critical assets, putting pressure on procurement budgets and complicating force planning. This challenge is becoming more serious since modern air and missile defense systems must now preserve high-end interceptors for aircraft, cruise missiles, and ballistic threats but also find economical ways to defeat mass, low-cost aerial attacks.

Impact of the Current War

Ongoing Missile and Drone Warfare is Accelerating Demand for Layered, Combat-Ready Integrated Air and Missile Defense Systems

The ongoing Russia-Ukraine war and continued missile and drone exchanges in the Middle East are pushing the market toward faster procurement, tighter system integration, and deeper interceptor inventories. Buyers are now placing more importance on 360-degree coverage, sensor-to-shooter connectivity, multi-layer engagement, and the ability to counter mixed salvos of ballistic missiles, cruise missiles, and drones in the same battle space.

Under its new 2025 policy, NATO is treating air and missile defense as a 24/7 job, in peacetime, a crisis, or active conflict. NATO are strengthening their shield to protect against threats coming from any direction, at any time, while U.S. military support to Ukraine in January 2025 included air defense system components, radars, and equipment to integrate Western launchers, missiles, and radars with Ukraine’s systems.

Segmentation Analysis

By Platform

Due to Territorial Defense Requirements, Wide Deployment Flexibility, and Layered Architecture Advantages, Land-Based Segment Dominated

In terms of platform, the market is categorized into land-based, naval-based, and airborne / space-enabled sensing.

The land-based segment dominated the market in 2025 since major countries build their core air and missile shield around ground-deployed radars, launchers, interceptors, and command networks that can protect territory, population centers, military bases, and strategic infrastructure on a persistent basis. NATO describes IAMD as a continuous mission to safeguard forces, territory, and populations, while the Missile Defense Agency’s THAAD and Ground-based Midcourse Defense programs show land-based systems remain central to both regional and homeland protection. As a result, land-based platforms remains most scalable and procurement-friendly option for layered defense compared with naval or airborne deployments.

The airborne / space-enabled sensing segment is expected to grow at a CAGR of 9.5% over the forecast period.

By Component

Due to their Mission-Critical Kill Function, High Unit Value, and Recurring Replenishment Demand, Interceptors & Effectors Segment Dominated

On the basis of component, the market is classified into sensors & radar, battle management / c2, launchers, interceptors & effectors, services & sustainment, and others.

The interceptors & effectors segment held the largest integrated air and missile defense market share in 2025, as it represents the part of the architecture that neutralizes the incoming threat. Radars, launchers, and command systems enable detection and engagement, procurement budgets are focus most heavily by interceptor rounds and effectors as they are high-value items, must be stocked across multiple threat layers, and require replenishment as operational demand rises. In modern air and missile defense, this component remains central to defeating ballistic missiles, cruise missiles, UAVs, and other aerial threats, resulting it consistently attracts the largest share of combat-relevant spending.

In January 2026, the U.S. Defense Security Cooperation Agency approved a possible sale to Saudi Arabia of PATRIOT Advanced Capability-3 Missile Segment Enhancement (PAC-3 MSE) missiles and related equipment for an estimated USD 9.0 billion.

The battle management / C2 segment is expected to show the fastest growth, registering a CAGR of 8.6% over the forecast period.

By Threat type

Due to their strategic threat profile, higher interception complexity, and sustained homeland and regional defense investment, the Ballistic missiles segment dominates

By threat type, the market is segmented into aircraft & helicopters, UAS / loitering munitions, cruise missiles, ballistic missiles, and hypersonic threats.

The ballistic missiles segment dominated the market in 2025, since these threats sit at the top of national defense priorities and require the most specialized detection, tracking, and interception architecture. Unlike many other aerial threats, ballistic missiles demand dedicated early-warning, discrimination, command-and-control, and layered interceptor systems across ground based and wider terrestrial, airborne and space-supported networks. This keeps procurement focused on ballistic missile defense programs, especially in countries that are building multi-layer shields for strategic assets, homeland protection, and high-value military infrastructure. The central role of systems such as THAAD and Aegis Ballistic Missile Defense shows the reason ballistic missile defense continues to command a leading share within the broader integrated air and missile defense market.

The UAS / loitering munitions is the fastest growing segment and is expected to grow at a CAGR of 12.0% across the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Range layer

Due to Strategic Homeland and Theater Defense Needs, and Priority Funding Against Advanced Missile Threats, Long Range / Upper Tier Segment Dominated

Based on range layer, the market is segmented into, VSHORAD, SHORAD, medium range, and long range / upper tier.

The long range / upper tier segment dominated the market in 2025, owing to its importance in the strategic core of national defense planning. These systems are built to address high-consequence missile threats over larger defended areas, and they attract stronger budget priority as governments view upper-tier protection as important for safeguarding critical territory, military infrastructure, and population centers. Systems such as THAAD, along with long-range discrimination and battle-management architecture, prove this layer remains central to modern integrated air missile defense planning.

In September 2025, the U.S. Missile Defense Agency and the U.S. Army issued the Record of Decision to implement the Enhanced Integrated Air and Missile Defense (EIAMD) system on Guam, aimed at delivering a persistent 360-degree layered Integrated Air and Missile Defense capability against rapidly evolving regional missile threats.

VSHORAD is the fastest growing segment in market and is expected to grow at a CAGR of 9.4% during the forecast period.

By End User

National Territory Protection Priorities, Strategic Asset Coverage Needs, and Sustained Government Funding, Resulted in Homeland Defense Segment Dominance

Based on end user, the market is segmented into homeland defense, military base defense, expeditionary / force protection, and strategic asset defense.

The homeland defense segment dominated the market in 2025, the dominance is attributed to governments placing the highest priority on protecting national territory, population centers, critical infrastructure, and command networks from high-consequence aerial threats. This end-user segment receives stronger and more consistent funding than expeditionary or site-specific missions since it sits at the core of sovereign defense planning. It also drives demand for layered defense architectures that combine ground based interceptors, radars, and command systems with terrestrial, airborne and space-enabled sensing to counter ballistic missiles, cruise missiles, and other long-range threats.

Strategic asset defense segment is expected to show the fastest market growth, registering a CAGR of 7.9% over the forecast period.

Integrated Air and Missile Defense Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Middle East, and rest of the world.

North America

North America Integrated Air and Missile Defense Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the Integrated Air and Missile Defense market in 2025, as the region, led mainly by the U.S., combines active homeland missile defense deployment with continuous modernization across sensors, interceptors, battle management, and layered regional protection. The U.S. Missile Defense Agency states that the Ground-based Midcourse Defense system is deployed in Alaska and California to defend the U.S. homeland against intermediate- and long-range ballistic missile threats, while the Guam EIAMD program is adding a persistent 360-degree layered defense architecture against evolving missile threats. The region also benefits from a dense industrial base anchored by major suppliers such as RTX, Lockheed Martin, and Northrop Grumman, keeping North America at the center of development, integration, and procurement activity.

U.S. Integrated Air and Missile Defense Market

Based on the strong contribution of North America to the market and the dominance of U.S. within the region, the U.S. market stood at around USD 15.77 billion in 2025, growing at a CAGR of 6.1% over the forecast period.

Europe

Europe held around 24.98% share of global market in 2025. Europe remains a structurally strong market for integrated air and missile defense as procurement is increasingly being shaped by NATO-wide interoperability and collective protection requirements, not only by national modernization plans. NATO’s 2025 IAMD Policy formalizes a 360-degree approach to defending Alliance territory, populations, and forces, while Germany says the European Sky Shield Initiative now brings together 23 European states to strengthen common air defense. Resulting, demand is centered on interoperable land-based systems, shared missile procurement, and integrated command-and-control architecture.

France Integrated Air and Missile Defense Market

France market reached approximately USD 1.13 billion in 2025, equivalent to around 9.86% of Europe revenues.

Russia Integrated Air and Missile Defense Market

The Russian market is rapidly evolving, driven by the need to counter advanced drones, cruise missiles, and saturation attacks, with key systems including the S-350 Vityaz and S-400 Triumph being modernized and deployed, as a result Russia market stood at around USD 2.46 billion in 2025, representing roughly 21.53% of Europe revenues.

Asia Pacific

Asia Pacific is one of the most important growth regions in the market, and is anticipated to grow at a CAGR of 7.3% over the forecast period, the regional militaries invest in layered defenses against more complex missile and air-breathing threats. Japan’s Ministry of Defense says its IAMD structure already links Aegis-equipped destroyers, PAC-3, and the JADGE command network, while Australia describes enhanced all-domain IAMD as critical and is fielding AIR6500, NASAMS, and a medium-range ground-based air defense layer. That mix makes the region especially important for battle-management systems, sensors, and both inner- and middle-layer interceptor solutions.

China Integrated Air and Missile Defense Market

The Chinese market is rapidly expanding, driven by regional security concerns, high-tech modernization, and a 7.2% defense budget increase, with 2025 revenues stood at around USD 3.62 billion, representing roughly 32.88% of the global sales.

Japan Integrated Air and Missile Defense Market

The Japanese market stood at around USD 2.22 billion in 2025, accounting for roughly 20.21% of Asia Pacific revenues.

Middle East

The Middle East region is anticipated to show second fastest growth with a CAGR of 8.1% during the forecast period, remaining one of the most operationally important IAMD markets since demand is driven by recurring missile and drone threat exposure rather than by long-cycle modernization alone. For instance, in January 2026, U.S. approvals reflect that urgency, Saudi Arabia’s possible PAC-3 MSE package was valued at USD 9.0 billion. Kuwait received approvals in 2025 and 2026 for PATRIOT missile upgrade, Build 8.1, and sustainment-related support. As a result, the region continues to favor layered, ground based missile defense, interceptor replenishment, and high-readiness support architecture.

Saudi Arabia Integrated Air and Missile Defense Market

The Saudi Arabia market stood at around USD 1.69 billion in 2025, accounting for roughly 30.47% of Middle East revenues.

Rest of the World

Rest of the World (Africa and Latin America) holds a comparatively smaller market share but is expected to grow at a highest CAGR of 11.5% during the forecast period. Latin America and Africa remain smaller and opportunity market, with demand focused in sovereignty protection, surveillance, point defense, and critical-asset security rather than broad upper-tier shield deployment. Brazil’s government says its current defense-industrial push includes radars, satellites, and rockets, and the Brazilian Air Force highlighted air-defense operations for the July 2025 BRICS summit, showing that Latin American demand is present even if it is narrower than in the larger IAMD regions. On the African side, SIPRI says military expenditure in Africa rose 11% between 2015 and 2024, but the region still trails Europe, Asia and Oceania, and the Middle East in aggregate spending momentum, which helps explain the more fragmented pace of IAMD adoption.

Latin America Integrated Air and Missile Defense Market

The market in Latin America reached around USD 0.81 billion in 2025, accounting for roughly 60.34% of revenues.

Africa Integrated Air and Missile Defense Market

The Africa market stood at around USD 0.53 billion in 2025 and is expected to reach USD 1.47 billion in 2034, representing roughly 39.66% of revenues in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Integrated Architecture Leadership and Combat-Proven Performance are Shaping Competitive Landscape Market

The competitive landscape is led by companies that can deliver more than a single subsystem. Companies with integrated capabilities in sensors, radars, battle-management systems, and interceptors, led the market, as customers increasingly demand full, layered defense solutions over standalone products. That dynamic keeps competition concentrated around firms such as Lockheed Martin, RTX, Northrop Grumman, and Rafael Advanced Defense Systems.

These players are driving the market through active upgrades and production expansion. Lockheed Martin received a USD 9.8 billion U.S. The Army awarded a PAC-3 MSE production contract in September 2025. RTX began producing LTAMDS in April 2025. Northrop Grumman's IBCS remains central to integrated battle management. Meanwhile, Rafael successfully completed upgrade tests for David's Sling in August 2025, these developments show that the market is being shaped by interoperability, readiness, and multi-layer air and missile defense capability.

LIST OF KEY INTEGRATED AIR AND MISSILE DEFENSE COMPANIES PROFILED IN REPORT

- Northrop Grumman Corporation (U.S.)

- Lockheed Martin Corporation (U.S.)

- RTX Corporation (U.S.)

- BAE Systems plc. (U.K.)

- Thales S.A. (France)

- Leonardo S.p.A. (Italy)

- Israel Aerospace Industries Ltd. (Israel)

- Rafael Advanced Defense Systems Ltd. (Israel)

- MBDA (France)

- Kongsberg Defence & Aerospace AS (Norway)

- Elbit Systems Ltd. (Israel)

- Saab AB (Sweden)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Rafael Advanced Defense Systems, together with Israel’s IMDO and the U.S. Missile Defense Agency, completed a complex David’s Sling test series focused on future-threat readiness, with the company stating that the effort enabled a significant upgrade to Israel’s air and missile defense architecture.

- January 2026: The U.S. State Department approved a possible Foreign Military Sale to Saudi Arabia for 730 PAC-3 MSE missiles and related equipment, with an estimated value of USD 9.0 billion.

- September 2025: The U.S. Army awarded Lockheed Martin a USD 9.8 billion contract for the production of 1,970 PAC-3 MSE interceptors and associated hardware, marking the largest contract in Lockheed Martin Missiles and Fire Control history.

- August 2025: The U.S. Army announced a successful LTAMDS missile flight test in which the radar, working through IBCS, detected, tracked, and enabled the intercept of an air-breathing threat using a PAC-3 MSE interceptor, demonstrating 360-degree engagement capability.

- August 2025: The U.S. State Department approved a possible Foreign Military Sale to Denmark for IBCS-enabled PATRIOT and related equipment for up to USD 8.5 billion, with an estimated sale value of USD 3.2 billion.

- June 2025: The U.S. Missile Defense Agency announced that the Long Range Discrimination Radar (LRDR) in Alaska successfully tracked a live ICBM-representative target in its first such flight test, strengthening the U.S. layered missile defense architecture.

- April 2025: The U.S. State Department approved a Foreign Military Sale to Kuwait for PATRIOT Post-Deployment Build 8.1 and related equipment, valued at USD 425 million.

- April 2025: RTX’s Raytheon announced that LTAMDS had transitioned from prototype to production after achieving Milestone C, making it an official U.S. Army program of record for integrated air and missile defense.

REPORT COVERAGE

The global integrated air and missile defense market analysis provides an in-depth study of market size, company profiling & forecast by all the market segments included in the report. It includes details on the market dynamics and trends that are expected to drive the market during the forecast period. It offers information on the technological advances, new product launches, key industry experts’ developments, and details on strategic partnerships, mergers & acquisitions. The research report also encompasses detailed competitive landscape with information on the market share and profiles of market key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.4% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

By Segmentation

|

By Platform

|

|

By Component

|

|

|

By Threat type

|

|

|

By Range layer

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value will account for USD 49.65 billion in 2026 and is projected to reach USD 87.73 billion by 2034.

In 2025, North Americas market value stood at USD 16.39 billion.

The market is expected to exhibit a CAGR of 7.4% during the forecast period.

The land-based segment led the market by platform.

Rapid growth in ballistic, cruise missile, and drone threats is accelerating demand for layered integrated air and missile defense systems.

Top players in the market include Northrop Grumman, Lockheed Martin, RTX, Rafael Advanced Defense Systems Ltd., BAE Systems, MBDA, and Thales.

North America held the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us