Intercity and Transit Bus Market Size, Share & Industry Analysis, By Bus Type (Intercity Buses and Transit Buses), By Propulsion (ICE, Hybrid, and Electric), By Seating Capacity (Up to 30 seats, 31-50 seats, 51-70 sears, and Above 70 seats), By Bus Length (Up to 9 meters, 9-12 meters, 12-14 meters, and Above 14 meters), By Powertrain Configuration (Front-engine, Mid-engine, Rear-engine, and In-wheel motor), By Ownership (Public and Private), and Regional Forecast, 2026-2034

Intercity and Transit Bus Market Size and Future Outlook

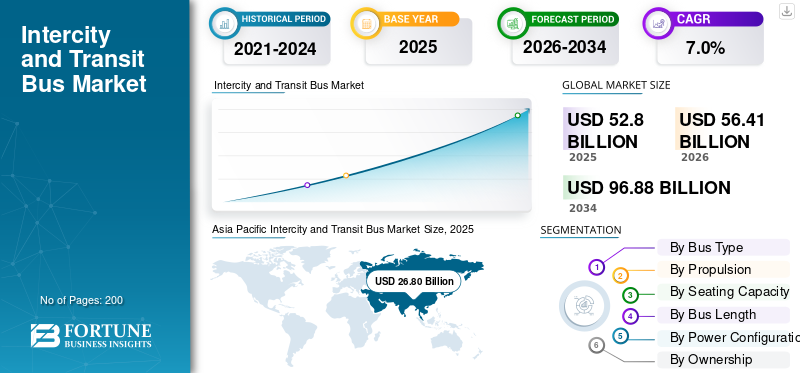

The global intercity and transit bus market size was valued at USD 52.80 billion in 2025. The market is projected to grow from USD 56.41 billion in 2026 to USD 96.88 billion by 2034, exhibiting a CAGR of 7.0% during the forecast period. Asia Pacific dominated the intercity and transit bus market with a market share of 50.75% in 2025.

The global market represents the production and sale of buses used for scheduled passenger transportation within cities and between urban centers. These vehicles support public transit, regional mobility, and long-distance passenger movement, forming a critical backbone of transportation systems worldwide. Intercity buses primarily serve medium- to long-distance routes, while transit buses operate on urban and suburban networks offering frequent stops and high passenger turnover.

The market size is shaped by rapid urbanization, population growth, and increasing reliance on organized bus service networks to reduce congestion and improve mobility access. Governments across regions are prioritizing investments in public transportation infrastructure to support sustainable urban development and reduce dependency on private vehicles. As a result, the market is projected to grow steadily during the forecast period.

A key transformation in the industry is the growing focus on electric and hybrid buses, driven by stricter emission regulations and rising awareness of carbon emissions. The adoption of electric buses is particularly strong in city transit fleets, where predictable routes and depot-based operations support electrification. Meanwhile, intercity buses continue to rely largely on conventional powertrains due to range and infrastructure considerations, though hybrid adoption is increasing.

Technological advancements such as advanced battery systems, telematics, and driver assistance features are enhancing vehicle efficiency and safety. Additionally, buses offer cost-effective passenger mobility, making them attractive for governments and private operators alike.

Leading key players including Tata Motors, Daimler Buses, Volvo Group, and BYD are investing in product innovation, electrified platforms, and regional manufacturing expansion to strengthen market share. These strategic initiatives indicate a competitive and evolving market landscape.

Download Free sample to learn more about this report.

INTERCITY AND TRANSIT BUS MARKET TRENDS

Integration of Advanced Technologies in Public Buses Pose as Market Trend

OEMs are increasingly integrating digital systems, battery optimization software, and connectivity features into buses. These technological advancements improve fleet efficiency, safety, and lifecycle performance, supporting long-term market growth.

- For instance, BYD introduced upgraded battery management systems in its electric city buses in 2023.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Government-led Investments in Public Transit Propel Market Growth

Strong investments in public transportation infrastructure by governments are a major driver of the global intercity and transit bus market growth. Public funding programs support fleet renewal, expansion of bus networks, and procurement of low-emission vehicles. These initiatives increase rising demand for new buses, particularly in urban transit systems, while supporting the adoption of electric buses to reduce carbon emissions and improve air quality.

- For instance, India’s Ministry of Heavy Industries approved large-scale funding for electric bus deployment under national urban mobility programs.

MARKET RESTRAINTS

High Upfront Cost of Advanced Buses Limits Adoption

Despite strong growth demand, the high upfront cost of electric and technologically advanced buses remains a key restraint. Electric buses require higher capital investment than conventional models, creating affordability challenges for smaller municipalities and private operators. Limited charging infrastructure further constrains deployment, particularly outside major cities.

- For instance, The International Energy Agency notes that electric buses remain cost-intensive despite falling battery

MARKET OPPORTUNITIES

Electrification of Urban Fleets Creates Long-Term Market Growth Opportunities

The accelerating adoption of electric buses presents a significant opportunity for market participants. Cities targeting zero-emission mobility are transitioning large transit fleets to electric models, creating sustained demand for OEMs. This shift enhances market size and opens opportunities for technology suppliers and infrastructure providers.

- For instance, the European Commission mandates zero-emission city bus procurement targets for member states.

MARKET CHALLENGES

Lack of Widespread Charging and Hydrogen Infrastructure Pose as Significant Challenges

The lack of widespread charging and hydrogen infrastructure poses a significant challenge, particularly outside developed markets. This limits the pace of electric and hybrid buses adoption and slows penetration in emerging economies.

- For instance, the World Bank highlights infrastructure gaps affecting public transport electrification in developing regions.

Segmentation Analysis

By Bus Type

Intercity Buses Dominate Due to Extensive Use in Regional and Private Operations

On the basis of bus type, the market is segmented into intercity buses and transit buses.

Intercity buses dominate due to their extensive use in regional travel and private operations. Rising passenger movement and affordability compared to rail transport support demand growth.

- For instance, in July 2023, FlixBus expanded intercity routes across Central Europe to meet rising passenger demand.

The intercity buses segment is expected to grow at a CAGR of 7.5% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Propulsion

ICE Buses Leads Due to Lower Upfront Costs and Established Fueling Infrastructure

On the basis of propulsion, the market is trifurcated into ICE, hybrid, and electric.

ICE buses dominate the market due to lower upfront costs, established fueling infrastructure, and suitability for intercity and rural routes where electric charging networks remain limited.

- For instance, in March 2024, Tata Motors announced fresh diesel and CNG bus orders from Indian state transport undertakings.

The electric segment is expected to grow at a CAGR of 9.5% over the forecast period.

By Seating Capacity

51-70 Seats Lead Due to Operational Flexibility, Passenger Capacity, and Suitability

On the basis of seating capacity, the market is segmented into up to 30 seats, 31-50 seats, 51-70 seats, and above 70 seats.

The 51–70 seat segment dominates as it offers optimal passenger capacity, operational flexibility, and suitability for both transit and intercity routes without requiring articulated configurations.

- For instance, in September 2023, Volvo Buses highlighted strong demand for its 55-seater bus platforms across Europe.

The above 70 seats segment is expected to grow at a CAGR of 6.9% over the forecast period.

By Bus Length

9-12 Meters Segment Dominates Due to Versatility Across Urban and Suburban Routes

On the basis of bus length, the market is segmented into up to 9 meters, 9-12 meters, 12-14 meters, and above 14 meters.

The 9-12 meters segment dominates due to its versatility across urban and suburban routes, ease of maneuverability, and compatibility with both conventional and electric powertrains.

- For instance, in May 2024, Daimler Buses reported continued demand for 12-meter Mercedes-Benz Citaro buses in Europe.

The above 14 meters segment is expected to grow at a CAGR of 9.1% over the forecast period.

By Powertrain Configuration

Rear-engine Buses Lead Due to Better Weight Distribution and Flexible Interior Layouts

On the basis of powertrain configuration, the market is segmented into front-engine, mid-engine, rear-engine, and in-wheel motor.

Rear-engine buses dominate as they provide lower cabin noise, better weight distribution, and flexible interior layouts, making them preferred for modern transit and intercity applications.

- For instance, in October 2023, Scania reaffirmed rear-engine layouts as standard across its city and intercity bus range.

The in-wheel motor segment is expected to grow at a CAGR of 9.8% over the forecast period.

By Ownership

Public Operators Segment Leads Due to Large-scale Government Procurement

On the basis of ownership, the market is bifurcated into public and private.

Public operators dominate the market due to large-scale government procurement, fleet renewal programs, and investments in public transportation infrastructure supporting urban mobility.

- For instance, in February 2024, Transport for London announced additional funding for zero-emission bus procurement.

The public segment is expected to grow at a CAGR of 7.4% over the forecast period.

Intercity and Transit Bus Market Regional Outlook

By region, the global market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Intercity and Transit Bus Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant intercity and transit bus market share in 2025, valuing at USD 26.80 billion, and also maintained the leading share in 2024, with USD 25.76 billion. Asia Pacific dominates the global market due to large population bases, rapid urbanization, and extensive public transport networks. Countries such as China and India procure buses at scale, supporting both volume and market share growth. Strong government backing and accelerated adoption of electric buses further strengthen regional leadership.

- For instance, in May 2025, under India’s PM e-Drive Scheme, Delhi, Bengaluru, and Hyderabad were allocated 10,900 new electric buses to accelerate sustainable public transportation.

China Intercity and Transit Bus Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues recorded at around USD 15.20 billion, representing roughly 28.8% of the global market.

India Intercity and Transit Bus Market

India’s market size in 2025 was around USD 4.35 billion, accounting for roughly 8.2% of global revenues.

Europe

Europe is estimated to reach USD 13.09 billion in 2026 and secure the position of the second-largest region in the market. Europe’s market growth is driven by emission regulations and zero-emission mandates. Public authorities prioritize electric fleets, supporting consistent demand across transit networks.

Germany Intercity and Transit Bus Market

Germany’s market value in 2025 was around USD 3.00 billion, accounting for roughly 5.7% of global revenues.

U.K. Intercity and Transit Bus Market

The U.K. market in 2025 was valued at around USD 2.05 billion, accounting for roughly 3.9% of global revenues.

North America

North America is projected to record a growth rate of 6.3% in the coming years, and reach a valuation of USD 8.91 billion by 2026. The North America market grows steadily through fleet replacement and electrification initiatives. Federal funding supports transit upgrades, particularly in the U.S., where cities invest in cleaner bus fleets and modern bus service systems.

U.S. Intercity and Transit Bus Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market was analytically approximated at around USD 6.60 billion in 2025, representing roughly 12.5% of the global market.

Rest of the World

The rest of the world region, including the Middle East & Africa, experiences gradual growth supported by urban expansion and improving public transport infrastructure.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Innovation on Technology, Cost, and Service Capabilities Shapes Competitive Bus Landscape

The competitive landscape of the global market is characterized by the presence of global OEMs and strong regional manufacturers competing on technology, cost, and service capabilities. Major key players focus on portfolio diversification, especially in electric and hybrid buses, to address evolving regulatory and customer requirements.

Companies are actively investing in modular platforms that support multiple propulsion types, enabling flexibility across markets. Expansion of local manufacturing facilities helps OEMs reduce costs, meet localization norms, and improve delivery timelines. Strategic partnerships with battery suppliers, charging infrastructure providers, and technology firms further enhance competitive positioning.

Another key strategy is long-term supply contracts with public transport authorities, which provide predictable volumes and improve market share stability. OEMs are also strengthening aftersales networks to differentiate themselves in a market where lifecycle cost plays a critical role.

- For instance, in January 2024, Volvo Buses announced a strategic shift toward electrified city buses in Europe, focusing on partnerships for battery supply and system integration.

LIST OF KEY INTERCITY AND TRANSIT BUS COMPANIES PROFILED

- Tata Motors (India)

- Daimler Buses (Germany)

- Volvo Group (Sweden)

- BYD (China)

- Scania (Sweden)

- Yutong Bus (China)

- Alexander Dennis (U.K.)

- Iveco Bus (Italy)

- MAN Truck & Bus (Germany)

- Solaris Bus & Coach (Poland)

KEY INDUSTRY DEVELOPMENTS

- February 2026: LeafyBus partnered with Eicher Trucks & Buses to deploy 100 electric intercity sleeper buses across key national corridors in India. The collaboration focuses on reducing operating emissions while scaling sustainable long-distance mobility. The initiative highlights growing interest in electrifying intercity bus services, traditionally dominated by diesel-powered fleets.

- January 2026: Dubai’s Roads and Transport Authority placed an order for 40 electric buses from Zhongtong as part of its broader 735-vehicle public transport renewal program. The procurement supports Dubai’s clean mobility strategy and reflects increasing adoption of electric transit buses in the Middle East, driven by sustainability targets and urban air-quality improvement initiatives.

- November 2025: Wrightbus announced a second-generation Electroliner with improved LFP battery technology extending range up to 275 mi to support expanded urban operations.

- September 2025: Wrightbus StreetDeck hydroliner FCEV progress: Wrightbus launched the next-gen hydroliner FCEV with enhanced fuel cell capabilities, showcasing hydrogen adoption in transit.

- June 2025: Over 2,000 electric buses served more than 100 routes by mid-2025 as London accelerates zero-emission targets for city transit.

- April 2024: First Bus aimed to have over 600 zero-emission buses on UK roads, including fully electric and hydrogen units across multiple cities.

- March 2024: Volvo launches the BZR electric bus platform: Volvo introduced its BZR (and BZRLE) electric bus chassis in European markets to serve high-capacity transit and intercity applications.

REPORT COVERAGE

The global intercity and transit bus market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.0% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Bus Type, Propulsion, Seating Capacity, Bus Length, Powertrain Configuration, Ownership, and Region |

| By Bus Type |

|

| By Propulsion |

|

| By Seating Capacity |

|

| By Bus Length |

|

| By Powertrain Configuration |

|

| By Ownership |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 52.80 billion in 2025 and is projected to reach USD 96.88 billion by 2034.

In 2025, the market value stood at USD 26.80 billion.

The market is expected to exhibit a CAGR of 7.0% during the forecast period.

Intercity buses segment led the market by bus type.

The government-led investments in public transit is driving the global market.

Tata Motors, Daimler Buses, Volvo Group, and BYD are some of the top players in the market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us