Internet of Military Things (IoMT) Market Size, Share, Industry Analysis and Russia-Ukraine War Impact Analysis, By Solution (Hardware, Software, and Services), By Type (Smart Helmets, IoT Wearables, Smart Weapons, and Connected Vehicles), By Application (Training and Simulation, Health Monitoring, Real-time Fleet Management, Inventory Management, Equipment Maintenance, and Others), By Technology (Artificial Intelligence, Edge Computing, Sensors, and Communication Networks), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

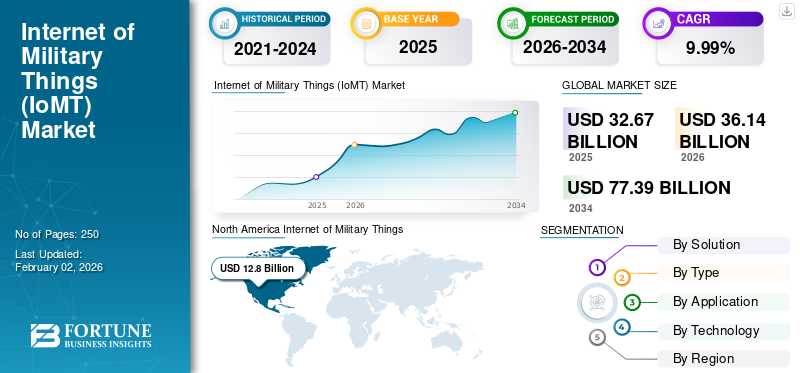

The global Internet of Military Things (IoMT) market size was valued at USD 32.67 billion in 2025 and is projected to grow from USD 36.14 billion in 2026 to USD 77.39 billion by 2034, exhibiting a CAGR of 9.99% during the forecast period. North America dominated the internet of military things (IoMT) market with a market share of 39.19% in 2025.

The Internet of Military Things (IoMT) encompasses the integration of interconnected devices, sensors, and networks into military operations, enabling enhanced situational awareness, improved decision-making, and optimized resource management. IoMT involves a diverse range of applications, including battlefield management, logistics tracking, surveillance, smart weapons, and soldier health monitoring. This market is driven by the increasing need for modernized defense systems, enhanced operational efficiency, and reduced human risk in dangerous environments. The IoMT market is evolving rapidly with advancements in artificial intelligence, machine learning, cloud computing, and cybersecurity technologies, all of which contribute to more sophisticated and robust military applications.

The COVID-19 pandemic had a mixed impact on the market. While the initial disruptions in the supply chain and manufacturing activities posed challenges, the pandemic also highlighted the importance of remote monitoring, automation, and data-driven decision-making in critical situations. This spurred increased investment in IoMT solutions for applications such as remote healthcare for military personnel, border security, and disaster response. Furthermore, the pandemic accelerated the adoption of digital technologies within the defense sector, which acted as a catalyst for market growth.

Key players in the IoMT market include prominent defense contractors and technology companies such as General Dynamics Corporation, Thales Group, Raytheon Technologies Corporation, BAE Systems, Lockheed Martin Corporation, Northrop Grumman Corporation, and IBM Corporation. These companies are actively involved in developing and deploying IoMT solutions for various military applications, focusing on areas such as secure communication networks, sensor integration, data analytics, and AI-powered decision support systems. The market is characterized by intense competition, with companies vying for government contracts and strategic partnerships to expand their market presence.

Download Free sample to learn more about this report.

Internet of Military Things (IoMT) Market Key Takeaways

- 2025 Market Size: USD 32.67 billion

- 2026 Market Size: USD 36.14 billion

- 2034 Forecast Market Size: USD 77.39 billion

- CAGR: 9.99% from 2026–2034

- North America dominated the Internet of Military Things (IoMT) market with a market share of 39.19% in 2025.

- The hardware segment led the market with a 44.88% share in 2026.

- The sensors segment accounted for 33.91% of the global market share in 2026.

North America

The region generated USD 12.8 billion in 2025 and is projected to reach USD 14.07 billion in 2026, supported by strong defense investments, AI-enabled military systems, and connected battlefield technologies.

Europe

Europe recorded USD 7.05 billion in 2025 and is expected to reach USD 7.8 billion in 2026, driven by military modernization programs, secure defense networks, and increased regional defense spending.

Asia Pacific

The market reached USD 8.9 billion in 2025 and is projected to grow to USD 9.97 billion in 2026, fueled by defense digitization, border surveillance initiatives, and the adoption of connected military platforms.

U.S.

The U.S. remains the largest IoMT market globally, supported by battlefield digitization and programs such as JADC2, with the market projected to reach USD 12.53 billion by 2026.

Japan

Japan continues to expand IoMT adoption through defense modernization and advanced surveillance capabilities, with the market projected to reach USD 2.07 billion by 2026.

Read More

RUSSIA-UKRAINE WAR IMPACT

Internet of Military Things (IoMT) Demand Has Risen Globally Due to Russia-Ukraine War

The ongoing Russia‑Ukraine conflict has acted as both a crucible and accelerator for IoMT technologies. Ukraine has rapidly adapted civilian tech including commercial drones and sensor networks into battlefield IoMT deployments, driving innovation in situational awareness, autonomous targeting, and battlefield software solutions.

- For instance, Ukrainian Delta situational awareness system gathers drone feeds, sensor data, satellite imagery and allied inputs into a unified, real‑time battlefield map, enabling coordination and target acquisition at unprecedented speeds even identifying up to 1,500 enemy targets daily during counteroffensive operations in mid‑2022.

Western defense contractors and tech firms such as Palantir, Microsoft, Amazon, and Auterion have partnered with Ukraine, delivering cloud‑native AI tools, drone “strike kits,” and battlefield data platforms under Pentagon and NATO-backed contracts.

- For instance, Auterion, is delivering ~33,000 AI-enhanced drone kits to Ukrainian forces by the end of 2025 to support jamming‑resistant drone operations with NATO-level tomes of battlefield testing happening live in Ukraine. Millions of Starlink terminals over 47,000-50,000 have been deployed in Ukraine for military connectivity, though reliance on a single provider has exposed strategic vulnerability when outages or executive decisions disabled operations temporarily.

On the adversary side, Russia’s deployment of electronic‑warfare systems such as the Borisoglebsk‑2 has targeted communications, GPS, and drone operations forcing greater investment in hardened, jam‑resistant IoMT platforms. Russia also launched cyberattacks on Ukrainian satellite systems (e.g. the Viasat KA‑SAT network) and telecom infrastructure (e.g. Kyivstar), disrupting communications and exposing critical cybersecurity vulnerabilities in interconnected systems.

These wartime deployments are provoking broader global demand for battlefield-tested IoMT solutions. Governments globally are now viewing Ukraine as a live “lab” for battlefield IoMT innovation encouraging accelerated procurement cycles, collaboration with startups/tech firms, and experimentation with autonomous systems, drone swarms, and integrated ISR platforms.

INTERNET OF MILITARY THINGS (IoMT) MARKET TRENDS

Securing Enhanced Operational Efficiency with Connected Systems Has Emerged as a Market Trend

The market is witnessing a significant trend of enhancing operational efficiency through connected systems. Modern militaries are increasingly leveraging connected devices and sensors to streamline logistics, improve situational awareness, and optimize resource utilization. This trend is driven by the need to reduce costs, improve decision-making speed, and enhance overall operational effectiveness.

- For example, real-time tracking of military assets using IoT sensors allows for more efficient supply chain management and reduced downtime. Similarly, networked sensors deployed on the battlefield provide commanders with a comprehensive view of the operational environment, enabling more informed and timely decisions.

The rise of 5G technology is further accelerating this trend, providing high bandwidth and low latency necessary for supporting a large number of connected devices in demanding military environments. Furthermore, the integration of AI and machine learning algorithms is enabling advanced data analytics, allowing military personnel to extract valuable insights from the vast amounts of data generated by IoMT devices. The convergence of these technologies is transforming military operations, driving a shift toward more agile, efficient, and responsive defense systems.

MARKET OPPORTUNITIES

Endeavors to Enhance Battlefield Superiority through Advanced Tech to Unlock New Growth Opportunities

A key market opportunity within the Internet of Military Things (IoMT) lies in enhancing battlefield superiority through advanced technologies. The ability to gather and analyze real-time data from a multitude of sources, including sensors, drones, and wearable devices, provides military commanders with unprecedented situational awareness. This real-time data, coupled with advanced analytics and AI-powered decision support tools, enables faster and more informed decision-making, leading to a significant tactical advantage. The IoMT also facilitates the development of autonomous systems, such as unmanned aerial vehicles (UAVs) and robots, which can perform dangerous tasks, reducing human risk.

Furthermore, IoMT solutions can enhance soldier lethality and survivability by providing soldiers with advanced communication systems, wearable sensors, and augmented reality (AR) interfaces. This allows soldiers to access real-time information, communicate effectively, and operate more effectively in complex and challenging environments. By embracing IoMT technologies, military organizations can gain a significant edge in terms of operational effectiveness, agility, and force protection, driving the demand for advanced IoMT solutions.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Need for Modernizing Defense Operations through Real-Time Intelligence and Automation to Spur Market Growth

The Internet of Military Things (IoMT) market growth is significantly driven by the increasing need for real-time intelligence and automation in modern warfare. Traditional military operations often rely on outdated methods of intelligence gathering and decision-making, which can be slow and inefficient. IoMT technologies provide military commanders with real-time situational awareness, enabling them to make faster and more informed decisions. The need to modernize defense systems is another key driver of the IoMT market.

Military organizations are increasingly investing in advanced technologies to maintain a competitive edge and respond to evolving threats. IoMT solutions offer a cost-effective way to enhance military capabilities and improve operational effectiveness. The increasing adoption of autonomous systems, such as drones and robots, is also driving the demand for IoMT technologies. These autonomous systems require robust communication networks, sensors, and data analytics capabilities, which are provided by IoMT solutions. Furthermore, the growing emphasis on force protection and risk reduction is driving the adoption of IoMT technologies.

MARKET RESTRAINTS

Security and Interoperability Concerns to Hamper the Market Growth

The market faces significant restraints due to security and interoperability concerns. The interconnected nature of IoMT devices and systems creates vulnerabilities to cyberattacks and data breaches, which can compromise sensitive military information and disrupt critical operations. Ensuring the security of IoMT devices and networks requires robust cybersecurity measures, including encryption, authentication, and intrusion detection systems.

Another major restraint is the lack of interoperability between different IoMT devices and systems. Military organizations often use a variety of devices from different vendors, which may not be compatible with each other. This lack of interoperability can hinder data sharing and collaboration, limiting the effectiveness of IoMT solutions. Furthermore, regulatory compliance and data privacy regulations pose additional challenges for the IoMT market. Military organizations must ensure that their IoMT systems comply with applicable regulations regarding data security, privacy, and export control. Overcoming these restraints is crucial for the widespread adoption of IoMT technologies in the defense sector.

MARKET CHALLENGES

Complex Integration of Modern Solutions with Legacy Systems to Create Challenges for Market Growth

A major challenge for the market is the integration of new IoMT solutions with existing legacy systems. Many military organizations rely on outdated infrastructure and technologies, which may not be compatible with modern IoMT devices and networks. Integrating these legacy systems with new IoMT solutions can be complex and costly, requiring significant modifications and upgrades.

Another significant challenge is managing the vast amounts of data generated by IoMT devices. Military organizations must have the infrastructure and expertise to collect, store, process, and analyze this data effectively. This requires investments in advanced data analytics tools, cloud computing infrastructure, and skilled data scientists. Furthermore, training military personnel to operate and maintain IoMT devices and systems is a major challenge. The implementation of IoMT solutions requires new skill sets and training programs to ensure that military personnel can effectively utilize and support these technologies.

SEGMENTATION ANALYSIS

By Solution

Hardware Segment Dominates the Market Due to its Foundational Role in the Internet of Military Things (IoMT)

By solution, the market is classified into hardware, software, and services.

The hardware segment led the global internet of military things (IoMT) market in 2026, accounting for 44.88% of the total market share. Hardware is a key aspect of the IOMT, providing the building blocks for sophisticated military capabilities. This segment, encompassing sensors, communication devices, and computing modules, forms the foundation for collecting, processing, and sharing information across the IoMT landscape.

The service segment is projected to be the fastest-growing in the market. Services play a critical role in the IOMT market, encompassing maintenance, integration, consulting, and training. These services ensure that IOMT systems function effectively, remain secure, and adapt to evolving military needs, facilitating the seamless integration of technology within military operations.

By Type

Smart Helmets Segment Leads the Market Due to Soldier Safety and Situational Awareness

By type, the market is classified into smart helmets, IoT wearables, smart weapons, and connected vehicles.

The smart helmets segment held the largest market share in 2026, accounting for 35.40% of the total market share. Smart helmets, equipped with advanced sensors and communication capabilities, are gaining traction for enhancing soldier safety and situational awareness. They provide real-time data on environmental conditions, vital signs, and threat assessments, contributing to improved decision-making on the battlefield.

The IoT wearables segment is the fastest-growing segment. IoT wearables, including smartwatches and fitness trackers, are emerging as valuable tools for monitoring soldier health, tracking location, and enhancing communication. Their compact form factor and connectivity features make them ideal for integration into military operations, improving performance.

By Technology

Sensors Segment Leads the Market Due to Rising Usage

Based on technology, the market is divided into artificial intelligence, edge computing, sensors, and communication networks

The sensors segment dominated the market in 2026, accounting for 33.91% of the total market share. Sensors provide crucial data for decision-making. The increasing use of sensors that offer precise environmental readings, threat detection, and physiological data is driving segment growth.

The AI segment is the fastest-growing category in the market. AI is revolutionizing the IoMT solutions by enabling intelligent data analysis, autonomous systems, and enhanced decision-making. The integration of AI algorithms into IoMT devices is improving threat detection, resource management, and battlefield effectiveness, contributing to market growth.

To know how our report can help streamline your business, Speak to Analyst

By Application

Training and Simulation Segment Depicts the Largest Share Due to Significance of Realistic Simulations and Personalized Learning

Based on application, the market is categorized into training and simulation, health monitoring, real-time fleet management, inventory management, equipment maintenance, and others.

The training and simulation segment held the largest market share in 2026, accounting for 30.73% of the total market share. Training and simulation solutions play a pivotal role in preparing soldiers for complex battlefield scenarios. IoMT-enabled training tools provide realistic simulations, personalized learning experiences, and real-time feedback, leading to improved soldier skills and combat effectiveness.

The health monitoring segment is the fastest-growing segment in the market. Wearable sensors are increasingly being integrated into military applications to monitor soldiers' health in real-time, providing valuable data for prevention. This segment offers early detection of fatigue, stress, and injuries, which are critical in maintaining mission readiness and soldier safety.

INTERNET OF MILITARY THINGS (IoMT) MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, and the rest of the world.

North America

North America Internet of Military Things (IoMT) Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America maintained a strong presence in the global market, reaching USD 12.8 billion in 2025, accounting for 39.19% share, and is expected to reach USD 14.07 billion in 2026. This is driven by heavy investments in advanced defense technologies, edge computing, cyber-secure communication, and connected battlefield solutions. The region benefits from a mature defense ecosystem, strong R&D funding, and active collaborations between the U.S. Department of Defense and top-tier defense contractors. The integration of AI-enabled drones, autonomous platforms, and predictive maintenance systems is accelerating. Canada also shows increasing adoption, especially in Arctic surveillance and secure logistics.

The U.S. represents the largest single market for IoMT globally. Its focus on multi-domain operations, battlefield digitization, and real-time ISR systems is propelling adoption. Key programs by the U.S. Department of Defense, such as Joint All-Domain Command and Control (JADC2), have triggered large-scale deployment of interconnected drones, wearables, sensors, and autonomous vehicles. Major companies such as Raytheon, Northrop Grumman, and L3Harris are actively involved. The U.S. also leads in defense-tech innovation, often piloting technologies years ahead of global peers. The demand is projected to grow consistently due to ongoing modernization efforts. The US market is projected to reach USD 12.53 billion by 2026.

Europe

In 2025, Europe generated USD 7.05 billion, contributing 21.57% to global market revenue, and is projected to grow to USD 7.8 billion in 2026. Europe is the second-largest IoMT market. Nations such as Germany, the U.K., France, and Italy are rapidly modernizing their military infrastructures by adopting AI, IoT-enabled ISR systems, and secure battlefield networks. The Russia-Ukraine war has been a major catalyst, pushing EU nations to accelerate digitization and invest in smarter, more autonomous systems. Programs such as the European Defence Fund and IRIS² satellite initiative further support regional demand. European defense contractors are increasingly partnering with AI and IoT startups to integrate scalable IoMT solutions into NATO frameworks and national defense strategies. The UK market is projected to reach USD 2 billion by 2026, while the Germany market is projected to reach USD 1.76 billion by 2026.

Asia Pacific

The Asia Pacific market accounted for USD 8.9 billion in 2025, representing 27.23% of the global industry, and is expected to reach USD 9.97 billion in 2026. Asia Pacific is the fastest-growing IoMT market. Rising geopolitical tensions and defense modernization in countries such as China, India, Japan, South Korea, and Australia are driving demand. These nations are adopting connected platforms for border surveillance, real-time threat monitoring, and unmanned systems integration. Government-backed defense digitization programs and AI initiatives are accelerating the use of IoMT in training, logistics, and command operations. The region’s focus on indigenous manufacturing and public-private defense tech partnerships is further fueling innovation and deployment across multiple military domains. The Japan market is projected to reach USD 2.07 billion by 2026, the China market is projected to reach USD 4.01 billion by 2026, and the India market is projected to reach USD 2.69 billion by 2026.

Rest of the World

Rest of the World accounted for USD 3.92 billion in 2025, representing 12.01% of the global market share, and is projected to reach USD 4.3 billion in 2026. The rest of the world represents a less but steadily growing IoMT demand. The Middle East leads within this group due to high defense spending in the UAE, Israel, and Saudi Arabia, with investments in drone surveillance, border control, and secure communication systems. In Africa and Latin America, the adoption is slower but growing, mainly driven by counter-terrorism and border security needs. These regions are investing in basic sensor integration, predictive maintenance, and logistics management, supported by foreign military aid and partnerships with Western defense tech suppliers.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players Shaping the Internet of Military Things (IoMT) Landscape to Propel Market Growth

Key players span major defense contractors, BAE Systems, Northrop Grumman, L3Harris, Thales, L3Harris Technologies, Inc., AIRBUS, Cisco Systems, Inc., IBM among others. Many engage in hardware delivery and strategic collaboration with governments and tech alliances to co‑develop AI‑enabled IoMT systems.

LIST OF KEY COMPANIES PROFILED

- BAE Systems (U.K.)

- Boeing (U.S.)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman (U.S.)

- Safran (France)

- Thales (France)

- L3Harris Technologies, Inc. (U.S.)

- AIRBUS (France)

- Cisco Systems, Inc. (U.S.)

- IBM (U.S.)

KEY INDUSTRY DEVELOPMENTS

- June 2025 - The European Union and Canada formalized a security and defense partnership during their 20th summit. Both parties entered into a significant Security and Defence Partnership aimed at enhancing Canada's role in the swiftly changing defense framework of Europe. Additionally, they have consented to promptly initiate discussions regarding a new bilateral agreement that would enable Canada to participate in SAFE, Europe's collaborative arms procurement initiative.

- March 2025 - Scale AI announced a partnership with the Department of Defense for a prominent AI agent initiative, marking a notable step in the contentious application of artificial intelligence within the military. The AI powerhouse, known for supplying training data to major AI entities such as OpenAI, Google, Microsoft, and Meta, received a prototype contract from the Defense Department for "Thunderforge," the DOD's leading program aimed at employing AI agents in U.S. military planning and operations.

- June 2024 - T-Mobile announced that it has been selected as a wireless solutions provider by the U.S. Department of the Navy for the USD 2.67 billion Spiral 4 contract. This new agreement will enable all Department of Defense agencies to order wireless services and equipment from T-Mobile over the next decade.

- January 2024 - AAR CORP., a prominent supplier of aviation services to both commercial and government entities, MROs, and OEMs, declared a new multi-year contract with Ontic. This agreement grants AAR the distribution rights to deliver a targeted range of military products to the U.S. government, ensuring exclusivity on certain components.

- June 2023 - BT secured a five-year agreement with the British Army to provide a managed Wi-Fi service at 162 new army locations in the U.K., aiming to create future 'smart bases'. The company is currently engaged in developing a 'smart base' at the British Army facility in Larkhill, located in Wiltshire, southwest England, which will feature fibre broadband and private 5G.

REPORT COVERAGE

This research report on the Internet of Military Things (IoMT) provides an extensive market analysis, pinpointing major players, product categories, and essential applications. Additionally, it outlines market trends and notable industry advancements. Furthermore, the report emphasizes several factors that have contributed to the expansion of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE AND SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 9.99% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation

|

By Solution

|

|

By Type

|

|

|

By Application

|

|

|

By Technology

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says the market value stood at USD 32.67 billion in 2025 and is estimated to reach USD 77.39 billion by 2034.

The market will grow steadily at a CAGR of 9.99% during the projection period of 2026-2034.

By solution, the hardware segment is the leading segment in this market.

BAE Systems (U.K.), Boeing (U.S.), Lockheed Martin Corporation (U.S.), Northrop Grumman (U.S.), Safran (France), Thales (France), and L3Harris Technologies, Inc. (U.S.) are some of the leading players in the market.

North America accounts for the largest share in the global market.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us