Interventional Cardiology Devices Market Size, Share & Industry Analysis, By Product (Coronary Stents {Bare-metal Stent (BMS), Drug-eluting Stent (DES), Others}, Structural Heart Devices {Heart Valves, Occluders & Others}, Angioplasty Balloons, Catheters {Diagnostic Catheters (Angiography, IVUS, Others), Treatment Catheters (Atherectomy, Thrombectomy, Ablation, Others)}, Embolic Protection Devices, and Others), By End User (Hospitals & ASCs, and Catheterization Labs & Others), and Regional Forecasts, 2026-2034

KEY MARKET INSIGHTS

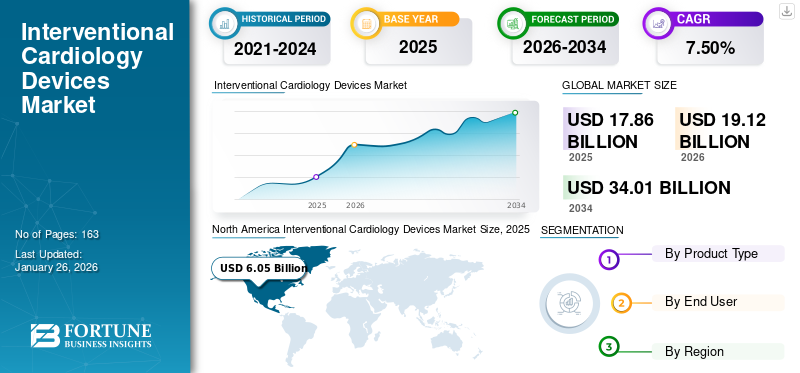

The interventional cardiology devices market size was valued at USD 17.86 billion in 2025. The market is projected to grow from USD 19.12 billion in 2026 to USD 34.01 billion by 2034, exhibiting a CAGR of 7.50% during the forecast period. North America dominated the Interventional Oncology Market with a market share of 33.90% in 2025. Moreover, the U.S. interventional cardiology devices market size is projected to grow significantly, reaching an estimated value of USD 9.37 billion by 2034, driven by rising incidence of coronary heart diseases and key players focusing on launching new products.

Interventional surgeries require specialized devices to repair damaged or weakened vessels, narrowed arteries, or other affected parts of the heart structure non-surgically. Thus, interventional cardiology devices, such as coronary stents, cutting balloon catheters, and Percutaneous Transluminal Coronary Angioplasty (PTCA), are used to perform minimally invasive surgeries across hospitals or cardiac catheterization labs. The prevalence of Cardiovascular Diseases (CVDs), such as coronary heart disease, stroke, and atrial fibrillation, is increasing globally. The surge in environmental risk factors, such as pollution, and biological factors, such as alcohol consumption, unhealthy diet, tobacco use, smoking, and others, are responsible for the rising incidence of cardiovascular diseases.

- According to the data published by World Health Organization (WHO), cardiovascular diseases are the leading cause of death worldwide, with around 17.9 million deaths reported globally.

- According to an article published by the American College of Cardiology in April 2021, around half of the deaths globally occur by cardiovascular disease in Asia. The deaths reported by cardiovascular disorders in Asia increased from 5.6 million to 10.8 million from 1990 to 2019.

- According to statistics published by the Centers for Disease and Prevention (CDC), in 2020, about 20.1 million U.S. adults aged above 20 suffered from Coronary Artery Disease (CAD).

Moreover, there is an increasing emphasis of healthcare providers toward shorter hospital stays and fewer postoperative complications. This is leading to an increase in the number of cardiovascular surgeries based on interventional techniques that are minimally invasive.

- According to data published by Yale Medicine, in the U.S., around 900,000 Percutaneous Interventions (PCIs) are performed every year.

The key players are now focusing on the production and launch of advanced devices to meet the growing demand for minimally invasive devices globally.

- For example, in July 2021, Medtronic announced the launch of Prevail Drug-Coated Balloon (DCB) catheter and reception of the C.E. mark in Europe. The drug-coated balloon is used during Percutaneous Coronary Intervention (PCI) procedures in patients with Coronary Artery Disease (CAD).

Thus, the aforementioned factors, along with the rising focus of key industry players on introducing new devices, and the availability of reimbursement coverage for interventional devices in developed countries are expected to drive the market growth.

The COVID-19 pandemic negatively affected the market in 2020. COVID-19 had a significant effect on all elective surgical procedures across the globe, significantly affecting the global market. As medical facilities struggled with surging volumes of patients suffering from COVID-19 infection, coronary and structural heart disease treatments were postponed.

However, in 2021 substantial rebounds in all elective and interventional surgeries, including coronary procedures, were reported in several countries across the globe. Moreover, post-pandemic, the high preference of healthcare professionals toward interventional procedures, owing to non-invasive and infection control among patients, will further propel the market growth.

Download Free sample to learn more about this report.

Global Interventional Cardiology Devices Market Snapshot & Highlights

Market Size & Forecast:

- 2025 Market Size: USD 17.86 billion

- 2026 Market Size: USD 19.12 billion

- 2034 Forecast Market Size: USD 34.01 billion

- CAGR: 7.50% from 2026–2034

Market Share:

- North America dominated the interventional cardiology devices market with a 33.90% share in 2025, driven by the rising incidence of coronary heart diseases, favorable reimbursement policies, and key players' emphasis on launching advanced products.

- By product, coronary stents are expected to retain the largest market share owing to their widespread adoption in emerging nations and extensive government-led procurement programs focused on cost-effective distribution.

Key Country Highlights:

- United States: Increasing preference for minimally invasive cardiac procedures and strategic product launches by key players are driving the market.

- Europe: High prevalence of structural heart diseases and affordable interventional devices compared to other regions support strong demand.

- China: Government initiatives for centralized bulk purchasing of coronary stents and domestic manufacturing expansion are bolstering market growth.

- Japan: Rising adoption of advanced interventional techniques and regulatory approvals for innovative cardiology devices are propelling demand.

Interventional Cardiology Devices Market Trends

Shifting Preference Toward Minimally Invasive Procedures Globally to Offer Market Growth Opportunities

The global prevalence of cardiovascular diseases is high, affecting around one-third of the population. Moreover, the morbidity and mortality rates in the population suffering from cardiovascular diseases are rising globally. Thus, these factors have increased the need and demand for various cardiac procedures across the globe.

- According to the American Heart Association (AHA), in 2020, it was reported that around 1.5 million patients undergo cardiac surgeries every year across the world.

- As per data published by Lifespan Health System, around 500,000 open heart surgeries are performed each year in the U.S.

Similarly, the introduction of reimbursement policies for percutaneous interventional surgeries by companies in ASCs, Office Based labs (OBLs), and Cath labs across developed countries is increasing. This led to their high preference for interventional surgeries in other settings, owing to its cost-effectiveness with the provision of early reimbursement, further reinforcing the market.

- According to an article published by tctMD, in January 2020, Centers for Medicare & Medicaid Services (CMS) announced reimbursement of PCI in OBLs and Ambulatory Surgical Centers (ASCs). Thus, the CMS will now offer reimbursement for certain angioplasty and stenting procedures performed outside the hospital outpatient setting.

- As per Stifel, Nicolaus & Company, coronary intervention coupled with pacemaker procedures represented about 566,000 Medicare procedures performed in Hospital Outpatient Divisions (HOPD) in 2018.

Moreover, the advantages offered by minimally invasive cardiac procedures, such as smaller incisions, quick recovery, and lower infection rates over other heart surgeries, are responsible for healthcare professionals' growing recommendation of minimally invasive cardiac procedures to patients.

- According to the data published by Healthcare Quality Improvement Partnership Ltd., in 2020, it was reported that around 100,294 percutaneous coronary intervention procedures were performed in the U.K.

- According to the data published by NCBI in 2020, it was reported that around 250,000 percutaneous coronary intervention procedures were performed in Japan.

Furthermore, the adoption of minimally invasive cardiac-related surgeries has become a noticeable trend in several countries. This is mainly due to the fact that minimally invasive surgeries provide faster recovery, reduce blood usage, shorten the hospital stay, and lower the overall treatment cost.

- For instance, as per data published by the National Center for Biotechnology Information (NCBI) in September 2023, the adoption rate for minimally invasive mitral valve surgery (MIMVS) varies across the globe is significantly increasing. Germany and Vietnam have a higher adoption rate of 55% and 50% for MIMVS. At the same time, the U.S. and U.K. have implemented this approach in 23% and 8% of cases, respectively.

Download Free sample to learn more about this report.

Interventional Cardiology Devices Market Growth Factors

Rising Product Launches by Key Players across Emerging Nations to Augment Market Growth

Emerging nations such as China, India, and Brazil suffer from a high burden of cardiovascular diseases such as valvar defects, and atrial stenosis posing high demand for interventional cardiology devices for treatment. Thus, major medical device players are investing in R&D to manufacture and launch innovative products to meet this growing demand across these countries.

- In December 2021, Translumina, a global developer and manufacturer of innovative cardiovascular medical devices used in interventional cardiology, announced the establishment of Asia’s Largest Heart Valve manufacturing facility in Vizag, India.

Partnership among major players to conduct several clinical trials on interventional devices is increasing. Similarly, rising approval by regulatory authorities for these interventional devices manufactured by domestic players across developing countries will further propel the market.

- For instance, in October 2023, Medinol announced the U.S. FDA approval of Elunir-Perl drug-eluting stent. The device is used in the treatment of coronary artery disease.

- In March 2021, B. Braun SE partnered with Infraredx to implement an Investigational Device Exemption (IDE) clinical trial for the SeQuent Please ReX drug-coated PTCA balloon catheter. This partnership aimed to offer technologically advanced catheters for treating coronary artery disease among patients.

- In April 2022, Biosensors International Group, Ltd. received Japanese PMDA approval for BioFreedom Ultra and BioFreedom devices used for coronary vascular applications.

Moreover, the interventional cardiology devices industry players are emphasizing acquisitions and collaborations with other manufacturers to meet the growing demand for interventional cardiac procedures at hospitals and ambulatory surgery centers and expand their cardiovascular product portfolio across emerging nations.

- In March 2021, Medtronic announced the launch of its Chameleon Percutaneous Transluminal Angioplasty (PTA) balloon catheter across countries such as Italy, Portugal, South Africa, and Turkey. The device enables the infusion of diagnostic or therapeutic fluids via the integrated injection port proximal to the balloon.

Therefore, the above factors, coupled with new product launches and their expansion across developing countries, further drive the market growth.

RESTRAINING FACTORS

Product Recalls by Market Players to Restrict the Adoption of Interventional Cardiology Devices

The events of product defects are increasing across the globe representing serious health hazards. This has led to the voluntary recall of products by regulatory agencies considering the safety of patients. The most common reasons for product recalls of interventional devices were quality issues, sterility concerns, and mislabeling. Furthermore, several cardiac interventional device manufacturing companies are announcing a recall for their products due to their life-threatening adverse effects hindering market growth.

- For instance, in July 2023, Abbott issued a recall for its cardiac catheter utilized in left atrial appendage occlusion procedures, citing a risk of air embolism that could lead to cardiac stroke or death.

- According to a study by JAMA, in January 2023, 156 medical devices approved via the 510(k) pathway that was subjected to a class 1 recall between 2017 and 2021 were studied. Out of all, nearly 30.0% of the recalled devices were in the cardiovascular space.

- In April 2022, Medtronic recalled about 6,000 IN.PACT Admiral Drug-Coated Balloons due to loss of sterility and potential damages.

- In December 2021, Arrow International, LLC, a subsidiary of Teleflex Inc., recalled around 2,132 Arrow AutoCAT 2 AC3 intra-aortic balloon pumps in the U.S. for unexpectedly short battery run times.

Similarly, several key players ceased the sales and distribution of particular devices owing to their recall and potential life-threatening effects, further hampering the market growth.

- In June 2022, Medtronic ceased sales and distribution of the HeartWare Ventricular Assist Device (HVAD) system due to multiple issues and death reports of 14 patients. The FDA had announced a recall of the HVAD pump implant kit in March 2021 owing to 29 complaints, including reports of 19 serious injuries and two deaths among patients.

Moreover, complications associated with the use of interventional cardiology procedures, such as hematoma, vascular complications, myocardial infarction, and radiation injury, further restrain the adoption of interventional cardiology devices.

- As per tctMD estimates, in January 2023, the FDA evaluated approximately 30 medical devices per year as part of the more-rigorous Premarket Approval (PMA) process.

- According to the data stated by NCBI in 2022, around 5.0% risk of radial artery occlusion was observed due to cardiac catheters after transradial access in the U.S.

Thus, the increasing incidence of clinical adverse events attributed to high-risk medical devices, their recalls, and rigorous approval processes for new devices may restrain the market growth.

Interventional Cardiology Devices Market Segmentation Analysis

By Product Analysis

Rising Demand for Coronary Stents across Emerging Nations will Boost the Segment Growth

Based on product, the market is segmented into coronary stents, structural heart devices, angioplasty balloons, catheters, embolic protection devices, and others.

By product, the coronary stents segment accounted for the highest global market 38.55% share in 2025. The segment is further divided into bare-metal stent (BMS), drug-eluting stent (DES), and others. The highest share was attributable to the rising demand for stents across emerging nations, such as China and India, and rising government initiatives for distributing interventional cardiology devices amongst the population.

- The Coronary Stents segment is expected to hold a 38.55% share in 2025.

- According to an article published by XINHUANET.com in January 2021, an estimated 1.5 million coronary stents are used in China annually.

- As per data published by the State Council of China, in November 2020, more than 400 health institutions across China participated in the centralized procurement, including those that usually purchase more than 500 coronary stents a year. The bulk-buying program is part of government-led efforts to address inflated prices and other issues in distributing pricey medical supplies.

On the other hand, the structural heart devices segment is expected to grow at a comparatively higher CAGR during the forecast period. The segment's growth is attributed to the rising prevalence of valvar devices, and extensive product launches across developing countries by key corporations are likely to contribute to the segment growth.

- In January 2022, Medtronic plc, a global leader in healthcare technology, announced that the National Medical Products Administration (NMPA) had approved the CoreValve Evolut PRO TAVR system for the treatment of aortic stenosis for symptomatic patients in China who are at high or extreme risk for open heart surgery.

The structural heart devices segment is further divided into heart valves and occluders & others. The heart valves segment dominated the market in 2023 due to the increasing awareness of non-invasive valvar surgeries amongst the population and favorable reimbursement scenarios for structural heart procedures and devices across developed nations.

- As per data revealed by Frontiers Media S.A. in May 2022, more than 306,000 patients with aortic stenosis underwent Transcatheter Aortic Valve Replacement (TAVR) in the U.S.

Moreover, the angioplasty balloons segment is expected to grow at a substantial CAGR over the forecast period. This is owing to high potential advantages compared to other interventional devices in non-invasive cardiology surgeries.

To know how our report can help streamline your business, Speak to Analyst

By End User Analysis

Surge in the Number of Patients visiting Hospitals & Ambulatory Surgical Centers to Propel Growth

Based on end user, the market is segmented into hospitals & ASCs and catheterization labs & others.

By end user, the hospitals & ambulatory surgical centers segment is anticipated to hold a dominant market share of 66.21% in 2026. The highest share was attributed to increasing hospital expenditures and the number of hospitals performing interventional surgeries. Moreover, the rising number of patients visiting hospitals for coronary procedures fuels the segment growth.

- According to UCSanDiegoHealth, in February 2021, about 717,000 adult patients underwent cardiac surgeries in the U.S. hospitals in 2020.

The catheterization labs & others segment is expected to register at a moderate CAGR during the forecast period. The growth is due to the rising number of catheterization laboratories across several countries and the increasing accessibility of treatment options for patients suffering from coronary or structural heart disorders.

- For instance, Koninklijke Philips N.V. announced the completion of 1,000th active Cath lab (interventional suite) installations in India in December 2021. Also, over the next few years, Philips announced to double the number of active cath labs in India, focusing on improving access to quality cardiac and neurovascular care in tier 2 and tier 3 cities.

REGIONAL INSIGHTS

Based on region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America Interventional Cardiology Devices Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

In 2025, North America generated USD 6.05 billion, contributing 33.90% to global market revenue, and is projected to grow to USD 6.47 billion in 2026. The higher dominance was due to the rising incidence of coronary heart disease amongst the population and the increasing emphasis of key players on launching and expanding new products in the region. Moreover, the rising number of diagnoses and treatments of coronary diseases among the population further propelled regional growth. The U.S. market is projected to reach USD 6.18 billion by 2026.

- In June 2021, Abbott announced that its XIENCE family of stents received the U.S. Food and Drug Administration (FDA) approval for High Bleeding Risk (HBR) patients in the U.S. In addition to the HBR indication, Abbott had also received FDA and European CE Mark approval for its next-generation XIENCE Skypoint stent. XIENCE Skypoint allows physicians to treat larger blood vessels through improved stent expansion that can open clogged vessels more effectively.

Europe

The Europe market accounted for USD 5.12 billion in 2025, representing 28.60% of the global industry, and is expected to reach USD 5.47 billion in 2026. Also, the presence of low-cost interventional devices compared to other nations led to a surge in the number of interventional procedures in the region, further propelling regional growth. In addition, increasing regulatory approvals and product launches across the region is also responsible for regional growth. The UK market is projected to reach USD 0.68 billion by 2026, while the Germany market is projected to reach USD 1.52 billion by 2026.

- For instance, in January 2024, Reflow Medical, Inc. announced that its Bare Temporary Spur Stent System had been granted the CE Mark certification in the European Union. This device aims to address de novo or restenotic lesions in the infrapopliteal arteries by utilizing a commercially available drug-coated balloon to improve drug absorption.

- According to the data published by Innovate Healthcare in 2021, it was reported that the cost of bare metal stents in Germany was around USD 120 as compared to USD 670 in the U.S.

Asia Pacific

Asia Pacific recorded a market size of USD 3.87 billion in 2025, capturing 21.70% of the global market share, and is projected to reach USD 4.17 billion in 2026. The higher CAGR was attributed to the increasing patient population for minimally invasive procedures and rising clinical trials on developing advanced and effective devices across Asia Pacific countries. The Japan market is projected to reach USD 0.47 billion by 2026, the China market is projected to reach USD 0.98 billion by 2026, and the India market is projected to reach USD 0.79 billion by 2026.

Middle East & Africa and Latin America

The Middle East & Africa market generated USD 1.3 billion in 2025, representing 7.30% of the global market landscape, and is expected to reach USD 1.39 billion in 2026. Latin America accounted for USD 1.52 billion in 2025, representing 8.50% of the global market share, and is projected to reach USD 1.62 billion in 2026. The Middle East & Africa and Latin America regions are projected to grow at a considerable CAGR owing to the rising number of coronary vascular surgeries and the high demand for non-invasive heart procedures during the forecast period.

List of Key Companies in Interventional Cardiology Devices Market

Strong Focus on Organic Strategies by Major Players to Expand Product Portfolio

Edwards Lifesciences, Medtronic, and Abbott are the prominent players in the global market and captured a significant share in 2024. The higher share was attributable to the increasing focus on introducing new products by key players. Similarly, rising approvals of interventional cardiology devices from various regulatory authorities across the globe are responsible for the company's growth.

- In September 2022, Edwards Lifesciences Corporation received the U.S. FDA approval for SAPIEN 3 Ultra RESILIA valve used for heart valve replacement.

Other major players operating in the market, such as Abbott, are focusing on developing technologically advanced devices to treat various heart diseases in pediatric patients. Also, key players are adopting several organic and inorganic growth strategies to establish their foothold in the market and further expand the company’s product portfolio.

- In September 2022, Abbott announced the three-year data on Amplatzer Piccolo occluder showing positive results in treating Patent Ductus Arteriosus (PDA) in premature babies. This is the first minimally invasive transcatheter treatment approved to treat PDA in premature babies.

- In February 2022, Boston Scientific Corporation acquired Baylis Medical Company Inc., which offers guidewires and sheaths to support catheter-based left heart procedures. This helps the company strengthen its position in the interventional devices market.

Similarly, rising emphasis on collaborations, R&D investments, and the conduction of clinical trials is the key factor responsible for the growth of other players in the market. Moreover, the global presence of these key players and the extensive distribution network across emerging nations will further augment the global interventional cardiology devices market growth.

LIST OF KEY COMPANIES PROFILED:

- Edward Lifesciences (U.S.)

- Boston Scientific Corporation (U.S.)

- Abbott (U.S.)

- Medtronic (Ireland)

- BIOTRONIK SE & Co. KG (Germany)

- iVascular (Spain)

- Terumo Corporation (Japan)

- Teleflex Incorporated (U.S.)

- B. Braun SE (Germany)

- Alvimedica (Turkey)

KEY INDUSTRY DEVELOPMENTS:

- December 2022: Boston Scientific Corporation acquired a major share of Acotec Scientific Holdings, a Chinese medical technology company that provides various solutions for interventional procedures. This acquisition helped Boston Scientific Corporation expand its product portfolio and market in China

- August 2022: Medtronic acquired Affera Inc., a prominent company in healthcare technology. Through this acquisition, Medtronic added products such as Sphere-9 cardiac diagnostic & ablation catheter and Affera Prism-1 cardiac mapping.

- November 2021: B. Braun SE partnered with REVA Medical to distribute Fantom Encore, a bioresorbable scaffold used for coronary interventions.

- September 2021: Abbott acquired Walk Vascular, LLC to provide unique vascular devices and improve patient care. The minimally invasive aspiration thrombectomy system is designed to remove blood clots. Walk Vascular, LLC is now a part of Abbott’s cardiovascular product portfolio.

- September 2021: Boston Scientific Corporation acquired Devoro Medical, Inc., which develops the WOLF thrombectomy platform. This acquisition helps the company to expand its peripheral interventions product portfolio and provides physicians with new options to improve thrombectomy procedures.

REPORT COVERAGE

The research report provides a detailed market analysis and focuses on crucial aspects such as leading players, products, and major indications of the market. Additionally, it offers insights into market trends, and key industry developments such as mergers, partnerships, & acquisitions. In addition to the factors mentioned above, the report includes factors that have contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

CAGR of 7.50% from 2026-2034 |

|

Segmentation |

By Product

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the market is projected to grow from USD 19.12 billion in 2026 to USD 34.01 billion by 2034.

Registering a CAGR of 7.50%, the market will exhibit steady growth over the forecast period (2026-2034).

The coronary stents segment is expected to lead this market during the forecast period.

The rising prevalence of coronary vascular diseases and the increasing R&D for technologically advanced products across the globe are the key factors driving the market growth.

Medtronic, Edward Lifesciences, and Abbott are major players in the global market.

Growing prevalence of valvar disorders and surge in number of minimally invasive surgeries across globe are expected to drive the adoption of interventional devices.

- 2021-2034

- 2025

- 2021-2024

- 163

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us