IoT Insurance Market Size, Share & Industry Analysis, By Insurance Type (Life and Health Insurance, Property & Casualty Insurance (Residential, Commercial & Industrial, Automotive and Others) and Others) By Distribution (Direct Channels (E-Commerce and Own Sales Force) and Indirect Channels (Agents/Brokers, Retailers and Banks and Others), By End User (Individuals, SMEs, Large Scale Enterprises and Government), and Regional Forecast, 2026-2034

IoT INSURANCE MARKET SIZE AND FUTURE OUTLOOK

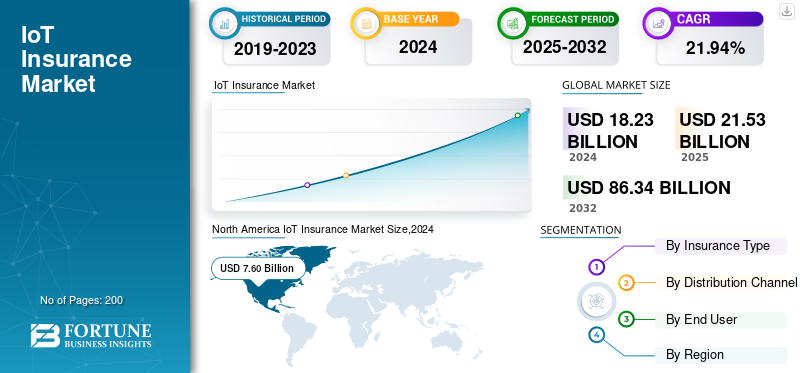

The global IoT insurance market size was valued at USD 21.53 billion in 2025. The market is projected to grow from USD 25.76 billion in 2026 to USD 135.32 billion by 2034, exhibiting a CAGR of 23.00% during the forecast period. North America dominated the global IoT insurance market with a market share of 42.20% in 2025.

The IoT insurance refers to the insurance solutions that utilizes Internet of Things devices including telematics, sensors, wearables and smart home tools to collect real-time data and assess risk accurately.

The market is growing rapidly owing to the rising adoption of connected devices, enhanced risk prevention, demand for personalized premiums, advancements in AI and analytics and insurer’s demand for reducing fraud and operational costs.

Few key players operating in the market include Allianz SE, AXA SA, Munich Re, Ping An Insurance, Zurich Insurance Group, Prudential plc, and others. these companies are adopting strategies such as partnerships with tech firms, expanding smart homes insurance solutions and others to sustain the market competition.

Download Free sample to learn more about this report.

IoT Insurance Market Key Takeaways

- 2025 Market Size: USD 21.53 billion

- 2026 Market Size: USD 25.76 billion

- 2034 Forecast Market Size: USD 135.32 billion

- CAGR: 23.00% from 2026–2034

- North America dominated the IoT insurance market with a 42.20% share in 2025.

- Property & Casualty Insurance is projected to account for 42.19% of the market in 2026.

- Indirect Channels are expected to lead with a 63.52% global market share in 2026.

North America

North America generated USD 9.08 billion in 2025, accounting for 42.20% of the global market.

Europe

Europe held a 26.60% market share in 2025, reaching USD 5.74 billion in revenue.

Asia Pacific

Asia Pacific accounted for 21.80% of the global market in 2025, valued at USD 4.68 billion.

U.S.

The market is projected to reach USD 9.34 billion by 2026, supported by strong IoT adoption and advanced insurance infrastructure

Japan

The market is projected to reach USD 0.81 billion by 2026, driven by smart city initiatives and growing connected device adoption.

Read More

MARKET DYNAMICS

Market Drivers

Rising Adoption of Connected Devices & IoT Ecosystems Drives the Market Development

The growing adoption of connected devices as well as IoT ecosystems is driving IoT insurance market growth. It offers insurers access to ongoing and high quality data. With connected cars, wearable health devices and smart home systems becoming a mainstream, insurers are capable of monitoring real-time behavior, offer higher accurate and personalized policies and detect risks early. This high data environment aids in reducing claims through proactive alerts, enables usage based insurance models and improves the underwriting precision. The expansion of IoT ecosystems also enhances the customer demand for responsive and smart insurance solutions, thus accelerating innovation in the market.

Market Restraints

Data Privacy, Security, and Regulatory Concerns to Deters the Market Growth

Data privacy, regulatory and security concerns restraints the market growth. Insurers rely on continuous data collection from wearable, sensors, and telematics, but handling this sensitive information tends to create high risks of breaches, misuses, and unauthorized access. Consumers often hesitate to share data due to fear of discrimination and surveillance during premium pricing. Moreover, stringent regulations such as GDPR and growing data protection laws augments the compliance burdens, thus hampering the market growth.

Market Opportunities

Integration of AI and Predictive Analytics with IoT Platforms Offers Lucrative Growth Opportunities

Integrating predictive analytics and AI with IoT platforms creates a lucrative opportunity by transforming how insurers manage and assess risks. By combining the real time data with advanced AI models, insurers are able to accurately predict potential losses, prevent incident priory and detect anomalies. This rapid shift from reactive claims handling to proactive risk mitigation tends to reduce the costs, enable development of personalized insurance based products and enhance customer trust.

IoT INSURANCE MARKET TRENDS

Shift toward Usage-Based and Behavior-Based Insurance Models Has Emerged as a Prominent Market Trend

One of the major trend reshaping the market is rapid shift toward usage and behavior based insurance models. Insurers are using data from connected cars, smart home devices and wearables to assess the risk based on real time behavior rather than a broad demographic profiles. This allows for a highly personalized premiums that reflects the actual driving habits, home safety patterns or health indicators. This approach improves the pricing accuracy, reduces claim frequency and encourages safer behavior.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Insurance Type

Growing Demand for Real-Time Monitoring of Assets Boosts Property and Casualty Segment Growth

Based on insurance type, the market is segmented into life and health insurance, property & casualty insurance and others. the property & casualty insurance segment is further divided into residential, commercial & industrial, automotive, and others.

In 2024, property and casualty insurance segment held the largest IoT Insurance market share and with a revenue of USD 9.25 billion. IoT devices allows for a real-time monitoring of assets, thus enhancing claim management and reducing risks especially for automotive, property and commercial insurance. These factors collectively drive the segmental growth. The Property & Casualty Insurance segment is projecteed to dominate the market with a share of 42.19% in 2026.

Similarly, life and health insurance segment held highest CAGR of 23.0% in 2024. This regional growth is due to growing adoption of wearable health devices and connected wellness platforms. These aid insurers to customize the policies and help in leading healthier lifestyles.

By Distribution Channel

Increasing Demand to Balance Regulatory Compliance and Digital Innovation Drives Hybrid Segment Growth

Based on distribution channel, the market is divided into on direct and indirect channels. The direct channel is further sub-segmented into ecommerce and own sales force, whereas the indirect channels are divided into agents/brokers, retailers and banks, and others.

Among these, indirect channels segment dominated the market with a revenue share of USD 11.75 billion in 2024. This growth is attributed to insurers leveraging intermediaries including agents, aggregators, and brokers to distribute IoT based policies. These aid in educating customers, offering personalized advisory services and managing complex products that are crucial for driving a large scale adoption across different sectors. The Indirect Channels segment is expected to lead the market, contributing 63.52% globally in 2026.

The direct channels segment held highest CAGR of 23.1% in 2024. This growth is due to insurers embracing digital transformations and moving toward mobile apps and online platforms. Additionally, the rise of connected devices, customer demand for transparency and real time risk assessment also accelerate the shift toward self-service models and direct the policy purchases.

By End User

Extensive Adoption of Connected Devices to Drive Segment Growth of Individuals

The market is divided into Individuals, SMEs, large scale enterprises, and government, based on end user.

Among these, the individual segment dominated the market with a revenue share of USD 9.33 billion in 2024. This growth is due to consumers adopting connected devices including wearables, smart home systems and connected vehicles rapidly. This enables a real time monitoring personalized insurance offerings and risk prevention, thus driving a high demand for IoT based personal coverage. The Individuals segment will account for 50.39% market share in 2026.

Large scale enterprises segment held highest CAGR of 25% in 2024. This segmental growth is due to its rapid integration of IoT solutions into operations for fleet management, asset tracking, and workplace safety. Additionally, the use of IoT-based data analytics enables insurers to provider dynamic and customized policies that improve risk management and operational efficiency for corporate clients.

To know how our report can help streamline your business, Speak to Analyst

IoT INSURANCE MARKET REGIONAL OUTLOOK

Geographically the market is segmented into North America, Europe, Asia Pacific, South America and Middle East & Africa.

North America

In 2025, the North America market stood at USD 9.08 Billion, representing 42.20% of global demand, and is projected to grow to USD 10.9 Billion in 2026. This growth is attributed to the strong presence of wide insurers, high adoption of connected devices across different industries, and advanced IoT infrastructure. Additionally, the U.S.’s focus on data driven risk assessment and prior regulatory aids in widespread implementation of IoT-based insurance solutions. The U.S. market is projected to reach USD 9.34 billion by 2026.

North America IoT Insurance Market Size,2025 (USD billion)

To get more information on the regional analysis of this market, Download Free sample

Europe

The Europe region captured 26.60% of the global market in 2025, generating USD 5.74 Billion in revenue, and is projected to reach USD 6.71 Billion in 2026. This growth is attributed to the growing adoption of connected cars and smart home technologies, advanced digital infrastructure, strong regulatory support for telematics and rapid shift of insurers toward personalized and data-driven products. The UK market is projected to reach USD 1.96 billion by 2026, while the Germany market is projected to reach USD 1.29 billion by 2026.

Asia Pacific

Asia Pacific maintained a strong presence in the global market, reaching USD 4.68 Billion in 2025, accounting for 21.80% share, and is expected to reach USD 5.73 Billion in 2026. This growth is due to expanding smart city initiatives, rapid digital transformation and growing use of IoT devices across countries such as Japan, China, and India. Additionally, surging awareness of risk prevention and augmenting investments from insurers in connected technologies further fuel the regional market expansion. The Japan market is projected to reach USD 0.81 billion by 2026, the China market is projected to reach USD 2.67 billion by 2026, and the India market is projected to reach USD 0.50 billion by 2026.

South America and Middle East & Africa

The Middle East & Africa market accounted for USD .63 Billion in 2025, representing 2.90% of the global industry, and is expected to reach USD .76 Billion in 2026. This growth is due to the increase in telematics-based auto insurance due to risk assessment and cost-cutting measures. Additionally, precise risk assessment is significant across the region due to high accident rates and difficulties with road safety. GCC countries are predicted to have a market share of USD 0.26 billion by 2025.

Latin America

In 2025, Latin America represented USD 1.41 Billion, accounting for 6.50% of the worldwide market, and is projected to grow to USD 1.66 Billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Are Focusing on Innovation to Sustain their Market Positions

The mobile banking industry is combined with key players including Allianz SE, AXA SA, Munich Re, Ping An Insurance, Zurich Insurance Group, Prudential plc, Allstate Insurance Company, Progressive Corporation, Generali Group, and others operating in it. These firms are aiming to adopt new technologies and innovations to sustain competition and maintain its positions.

LIST OF KEY IoT INSURANCE COMPANIES PROFILED

- Allianz SE (Germany)

- AXA SA (France)

- Munich Re (Germany)

- Ping An Insurance (China)

- Zurich Insurance Group (Switzerland)

- Prudential plc (U.K.)

- Allstate Insurance Company (U.S.)

- Progressive Corporation (U.S.)

- Generali Group (U.S.)

- Admiral Group (U.K.)

- Lemonade (U.S.)

- Octo Group SpA (U.K.)

KEY INDUSTRY DEVELOPMENTS

- In May 2024, Cosmo Connected, a Parisian startup pioneering in connected helmets with integrated automatic brake lights, turn signals, fall detection, and SMS alerts, launched an innovative new line called "Cosmo Care". This line offers users the option to benefit from a Cosmo Fusion connected helmet and provides insurance coverage for each user regardless of their micromobility vehicle. The embedded Internet of Things (IoT) in the Cosmo Fusion helmet allows for tracking the user's movements and certifying accidents to offer multimodal insurance coverage, provided by Allianz Partners, a world leader in insurance and assistance services.

- In October 2023, Nirvana Insurance, provider of modern insurance for physical operations, today announced a USD 57 million Series B funding round. Lightspeed Venture Partners reaffirmed its commitment to Nirvana by returning to lead the round, with additional participation from General Catalyst and Valor Equity Partners. The new funding positions Nirvana to continue helping fleets utilize their IoT and sensor data to access insurance cost savings and customized risk management solutions.

- In May 2023, Sky and Zurich announced the launch of an innovative smart home protection service, offering customers comprehensive home insurance and smart home tech that work together in one simple app. In a unique combination, Sky Protect will let customers insure their homes and keep an eye on them, helping to spot small problems before they become big ones.

REPORT COVERAGE

The global report provides a detailed analysis of the market and focuses on key aspects such as prominent companies, deployment modes, types, and end users of the product. Besides this, it offers insights into the IoT Insurance market trends and highlights key industry developments and market share analysis for key companies. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

Attribute |

Details |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Growth Rate |

CAGR of 23.00% from 2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Insurance Type, Distribution Channel, End User and Region |

|

By Insurance Type |

|

|

By Distribution Channel |

|

|

By End User |

|

|

By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 21.53 billion in 2025 and is projected to reach USD 135.32 billion by 2034.

The market is expected to exhibit steady growth at a CAGR of 23.00% during the forecast period.

Rising Adoption of Connected Devices & IoT Ecosystems drives the market growth.

Allianz SE, AXA SA, Munich Re, Ping An Insurance, Zurich Insurance Group, Prudential plc, Allstate Insurance Company, Progressive Corporation, Generali Group are some of the top players in the market.

The North America region held the largest market share.

North America was valued at USD 9.08 billion in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us