IVD Contract Manufacturing Market Size, Share & Industry Analysis By Product Type (Instruments, and Consumables), By Technology (Immunodiagnostics, Clinical Chemistry, Molecular Diagnostics, Hematology, and Others), By Service Type (Manufacturing Services, Assay Development Services, and Others), By End User (Medical Device Companies, Pharmaceutical & Biotechnology Companies, Academic & Research Institutes, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

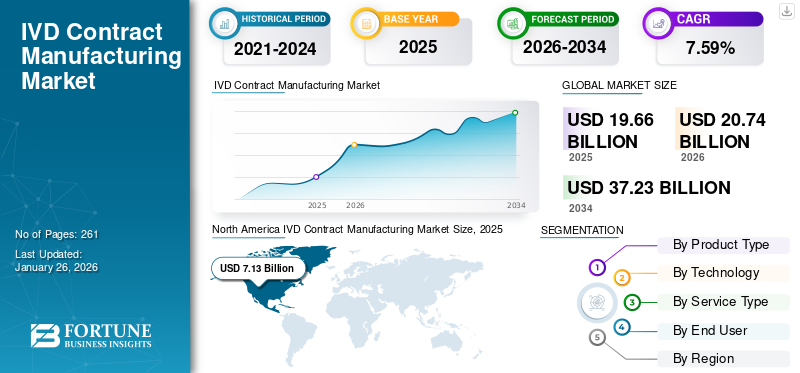

The global IVD contract manufacturing market size was valued at USD 19.66 billion in 2025 and is projected to grow from USD 20.74 billion in 2026 to USD 37.23 billion by 2034, exhibiting a CAGR of 7.59% during the forecast period. North America dominated the IVD contract manufacturing market with a market share of 36.26% in 2025.

IVD contract manufacturing involves outsourcing the design, development, and production of in vitro diagnostic (IVD) devices to specialized third-party manufacturers. The growing burden of chronic diseases, such as infectious diseases and others, is resulting in an increasing number of patient visits and demand for diagnostic tests globally. The growing demand for diagnostic tests and a preference toward outsourcing manufacturing among medical device companies is supporting the demand for IVD contract manufacturing, thereby contributing to the market penetration rate for these services.

- For instance, according to data published by the Centers for Disease Control & Prevention (CDC) in 2019, approximately 10.2 million patients visited physician offices for infectious diseases and parasitic diseases in the U.S.

Furthermore, the increasing cost pressures on manufacturers and the complexity of newer diagnostics, including multiplex assays and others, are likely to drive the outsourcing of in-vitro diagnostics globally. This, along with an increasing focus on improving their contract manufacturing services among key players, including Thermo Fisher Scientific Inc., Nova Biomedical, and others, is expected to drive the global market growth.

Download Free sample to learn more about this report.

IVD CONTRACT MANUFACTURING MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 19.66 billion

- 2026 Market Size: USD 20.74 billion

- 2034 Forecast Market Size: USD 37.23 billion

- CAGR: 7.59% from 2026–2034

- North America dominated the IVD contract manufacturing market with a market share of 36.26% in 2025.

- The consumables segment held the largest market share 66.96% in 2026.

- The immunodiagnostics segment dominated the market in 2025. In 2026.

North America

In 2025, North America generated USD 7.13 billion, contributing 36.26% to global market revenue, and is projected to grow to USD 7.55 billion in 2026.

Europe

The Europe market accounted for USD 6.16 billion in 2025, representing 31.33% of the global industry, and is expected to reach USD 6.49 billion in 2026.

Asia Pacific

Asia Pacific recorded a market size of USD 4.11 billion in 2025, capturing 20.91% of the global market share, and is projected to reach USD 4.33 billion in 2026.

U.S.

In 2026, the U.S. market is estimated to reach USD 6.42 billion.

Japan

Market growth is supported by an aging population, increasing demand for accurate diagnostic testing, advanced laboratory capabilities, and continued investments in healthcare innovation.

Read More

Market Dynamics

Market Drivers

Increasing Demand for IVD Diagnostics to Augment Market Growth

The increasing disease burden of chronic conditions, including infectious diseases, diabetes, and others, among the patient population is a major factor contributing to the growing number of IVD tests in the market.

- For instance, according to the 2024 data published by the International Diabetes Federation (IDF), about 589 million adults are living with diabetes globally.

Moreover, the growing awareness programs about early detection and screening of disorders among patients are also boosting the number of IVD tests globally. An increasing number of IVD tests, along with rising complexity in newer diagnostics, is increasing the reliance of original equipment manufacturers on specialized contract manufacturers in the market.

Therefore, the growing disease burden, coupled with the rising demand for IVD diagnostics and improved diagnostic technology, is anticipated to fuel the penetration rate, thereby contributing to the global IVD contract manufacturing market growth.

Market Restraints

Concerns Associated with Intellectual Property (IP) Risks to Hamper Market Growth

There is an increasing demand for IVD contract manufacturing for diagnostic products among the original equipment manufacturers. However, intellectual property concerns are expected to hinder the IVD contract manufacturing landscape in the market. The original equipment manufacturers share highly sensitive information, such as assay formulations, process parameters, reagent compositions, and software codes, with contract manufacturers, which increases risks related to misuse of intellectual property or potential loss of confidential data.

The globalization of manufacturing further increases complexity, as many IVD CMOs operate through facilities in the Asia Pacific or other regions, where enforcement of IP laws may vary. Moreover, the stringent regulatory laws, particularly those enforced by the U.S. Food and Drug Administration (FDA) and the European Union’s General Data Protection Regulation (GDPR), make it more challenging to exchange clinical and technical data during manufacturing and validation.

- For instance, according to data published by The HIPAA Journal in 2025, approximately 41.2% of all third-party breaches affect healthcare organizations.

Therefore, all the above-mentioned factors, coupled with the complexity of newer diagnostics, are primarily responsible for the limited outsourcing of these products, which is further anticipated to hamper market growth.

Market Opportunities

Expansion in Emerging Countries to Create Lucrative Opportunities

There is an increasing prevalence of chronic conditions, leading to a growing focus on developing healthcare infrastructure, particularly in emerging markets such as Brazil, Mexico, and others. The rapid rise in disease screening programs, diagnostic awareness, and healthcare spending has significantly increased the demand for IVD devices, including clinical chemistry and molecular diagnostics, among others.

Furthermore, increasing strategic initiatives among governmental and non-governmental organizations to promote domestic manufacturing through public-private collaborations, among others, is also expected to boost the demand for contract manufacturing of these products in the market.

- According to 2025 data, the Indian Government has released programs such as the Production-Linked Incentive (PLI) scheme for medical devices, which offers financial rewards for domestic manufacturing of diagnostic products in India.

Other Prominent Opportunities

- Rising global demand for precision diagnostics and personalized medicine will drive long-term opportunities for contract manufacturing services.

- Growing trend of outsourcing non-core manufacturing operations to specialized IVD service providers for cost and quality optimization.

- Advancements in microfluidics, biosensors, and molecular diagnostics will create new avenues for contract manufacturing partnerships.

Market Challenges

Stringent Regulatory Requirements to Limit Market Growth

There is a rising demand for in-vitro diagnostic contract manufacturing services among the original equipment manufacturers globally. However, distinct regulatory frameworks, submission formats, and post-market obligations make it challenging for contract manufacturers serving several geographies globally.

Additionally, limited review capacity and the continuous evolution of regulatory laws, including the FDA’s Quality Management System Regulation (QMSR) harmonization and Europe’s evolving IVDR transition timeframe, require manufacturing companies to revise their procedures and redesign instruments and consumables to maintain conformity.

- For instance, according to the 2024 data published by the European Commission, it was reported that only 12 notified bodies are designated under the IVDR, compared to 22 notified bodies designated under Directive 98/79/EC. Therefore, limited review capacity and stringent laws are expected to limit the market penetration rate of these services.

Therefore, regulatory diversification creates challenges for expanding business across various geographies due to difficulties in maintaining validation systems, documentation, and other requirements, especially among mid-sized and small firms, thereby hampering the adoption rate in the market.

Other Prominent Challenges

- High initial investment requirements for automation, validation, and advanced manufacturing facilities.

- Dependence on limited suppliers for critical raw materials, such as enzymes and antibodies, affects supply chain stability.

- Limited scalability for small and medium-sized contract manufacturers serving global clients.

IVD Contract Manufacturing Market Trends

Increasing Technological Advancements to Boost Services Demand

There is an increasing focus on integrating technology into IVD contract manufacturing devices across production processes. The integration of automation, digitization, and smart manufacturing technologies, among others, is reshaping the global industry landscape. The adoption of advanced technologies, such as robotics and real-time data analytics, among others, is enabling contract manufacturers to improve the quality, reproducibility, precision, and scalability of these products.

Additionally, the contract manufacturers are also deploying machine learning and artificial intelligence tools to detect anomalies and optimize process parameters. These technology updates enhance consistency and productivity, enabling key companies to offer advanced manufacturing capabilities and align with global regulatory requirements, thereby expected to fuel demand for these services in the market.

- According to data published by the Mayo Clinic in 2025, it was reported that more than 50% of surgical pathology cases were being digitized and interpreted by pathologists through digital pathology.

Other Prominent Trends

- Rising demand for molecular diagnostic assays and point-of-care (POC) testing solutions is driving contract manufacturing partnerships.

- Increased focus on regulatory compliance, particularly for ISO 13485-certified facilities and FDA-approved manufacturing capabilities.

- Expansion of contract manufacturing capacities to accommodate the rapid production of diagnostic reagents and consumables post-pandemic.

- Emergence of strategic collaborations between IVD developers and contract manufacturers to shorten product launch timelines.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Product Type

Increasing Product Approvals for Consumables Led to Segment Dominance

Based on product type, the market is bifurcated into instruments and consumables.

To know how our report can help streamline your business, Speak to Analyst

The consumables segment held the largest market share 66.96% in 2026. The growth is primarily due to the increasing number of diagnostic tests, such as those for infectious diseases, resulting in a rising demand for consumables globally. This, along with the increasing focus of key players toward receiving product approvals for consumables such as test cartridges, among others, is further expected to support the segmental growth.

- In February 2025, Visby Medical received U.S. FDA approval for its point-of-care respiratory health test, manufactured through contract manufacturers, with the aim of strengthening its product portfolio.

By Technology

Increasing Prevalence of Chronic Diseases Led to Dominance of Immunodiagnostics Segment

Based on technology, the market is segmented into immunodiagnostics, clinical chemistry, molecular diagnostics, hematology, and others.

The immunodiagnostics segment dominated the market in 2025. In 2026, the segment is anticipated to dominate with a 34.00% share. The dominant share is primarily due to the growing prevalence of chronic disorders such as diabetes, infectious disorders, and cardiovascular disorders, further resulting in an increasing number of immunodiagnostics tests globally. This, along with growing partnerships between OEMs and contract manufacturers to develop novel products, is anticipated to contribute to the segmental growth in the market.

- For instance, according to 2024 data published by the Centers for Disease Control & Prevention (CDC), it was reported that about 1 in 20 adults has coronary artery disease (CAD).

The molecular diagnostics segment is expected to grow at a CAGR of 7.4% over the forecast period.

By Service Type

Establishment of New Facility Led to Dominance of Manufacturing Services Segment

On the basis of service type, the market is segmented into manufacturing services, assay development services, and others.

The manufacturing services segment dominated the global market and held a 71.98% share in 2026. The growth is attributed to the rising prevalence of chronic conditions, including infectious diseases and autoimmune disorders, which in turn drives an increasing demand for contract manufacturing services in the market. This, along with the growing focus of market players on establishing new facilities to provide novel manufacturing services to OEMs, thereby supporting segmental growth.

- For instance, in July 2022, SCIENION established a new facility offering ISO5 cleanrooms for critical contract manufacturing services, addressing the rapidly growing demand for diagnostic assays in point-of-care and point-of-need formats.

The segment of assay development services is set to flourish with a growth rate of 7.5% across the forecast period.

By End User

Increasing Number of Medical Device Companies Led to Segmental Dominance

Based on end user, the market is divided into medical device companies, pharmaceutical & biotechnology companies, academic & research institutes, and others.

The medical device companies segment dominated the market in 2025. The growing prevalence of chronic diseases, increasing test volumes, and the growing number of medical device companies are some of the vital factors supporting segmental growth in the market. Furthermore, the segment is set to hold a 60.22% share in 2026.

- For instance, according to 2025 statistics published by AdvaMed, there are about 6,500 medical device companies in the U.S.

In addition, the end users of pharmaceutical & biotechnology companies are projected to grow at a CAGR of 7.5% during the study period.

IVD Contract Manufacturing Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America IVD Contract Manufacturing Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, North America generated USD 7.13 billion, contributing 36.26% to global market revenue, and is projected to grow to USD 7.55 billion in 2026. The dominance of the region is due to distinct factors, including the growing prevalence of chronic conditions, the rising number of IVD tests such as clinical chemistry tests and others, developed healthcare infrastructure, the strong regulatory frameworks supporting outsourcing partnerships among the key players, and others. In 2026, the U.S. market is estimated to reach USD 6.42 billion.

- For instance, according to data published by the National Institutes of Health (NIH) in 2024, approximately 3.3 billion in-vitro diagnostic tests are performed annually in the U.S.

Europe & Asia Pacific

The Europe market accounted for USD 6.16 billion in 2025, representing 31.33% of the global industry, and is expected to reach USD 6.49 billion in 2026. Asia Pacific recorded a market size of USD 4.11 billion in 2025, capturing 20.91% of the global market share, and is projected to reach USD 4.33 billion in 2026. Other regions, such as Europe and the Asia Pacific, are expected to witness considerable growth during the forecast period. During the study period, the European region is projected to record a growth rate of 6.4% and reach a valuation of USD 6.16 billion in 2025. An increasing number of IVD tests, growing technological advancements, a robust diagnostic ecosystem, an increasing number of CROs, improving healthcare infrastructure, increasing government initiatives, and others are some of the crucial factors contributing to the growth of the market. Backed by these factors, countries such as the U.K. are expected to record the valuation of USD 1.04 billion, Germany to record USD 1.41 billion, and France to record USD 1.18 billion in 2026. After Europe, the market in the Asia Pacific is estimated to reach USD 4.11 billion in 2025 and secure the position of the third-largest region in the market. In the region, India is estimated to reach USD 0.66 billion while China is estimated to reach USD 1.43 billion in 2026.

Latin America and Middle East & Africa

Latin America accounted for USD 1.5 billion in 2025, representing 7.60% of the global market share, and is projected to reach USD 1.57 billion in 2026. The Middle East & Africa market generated USD 0.77 billion in 2025, representing 3.90% of the global market landscape, and is expected to reach USD 0.8 billion in 2026. Over the study period, the Latin America and Middle East & Africa regions are expected to witness considerable growth in this market. The Latin America market in 2025 is expected to reach a valuation of USD 1.50 billion. The growing prevalence of chronic conditions, increasing awareness about early disease diagnosis, and improvements in healthcare infrastructure are boosting the adoption of contract manufacturing services in these regions. In the Middle East & Africa, GCC is set to attain the value of USD 0.42 billion in 2025.

Competitive Landscape

Key Industry Players

Growing Number of Partnerships Among Key Players to Support their Dominance

A robust and diversified service portfolio for IVD Contract Manufacturing services, along with a strong brand presence globally, is one of the vital factors supporting the dominance of these companies in the market. Thermo Fisher Scientific Inc., Argonaut Manufacturing Services Inc., and other prominent players are expected to be in the market in 2024. Moreover, the increasing focus of key players toward acquisitions and partnerships among other players is likely to support the global IVD contract manufacturing market share.

- For instance, in January 2025, Argonaut Manufacturing Services Inc., a contract development and manufacturing organization serving the biopharma and life sciences industries, collaborated with Akoya Biosciences Inc. to develop IVD assays.

Other key players, including IVD Technologies and others, are also growing in the market, primarily driven by their increasing establishment of facilities to enhance their brand presence and strengthen their market position.

List of Key IVD Contract Manufacturing Companies Profiled

- Thermo Fisher Scientific Inc. (U.S.)

- IVD Technologies (U.S.)

- Argonaut Manufacturing Services Inc. (U.S.)

- Bio-Techne (U.S.)

- Invetech (Australia)

- Merck KGaA (Germany)

- Fujirebio (Japan)

- Celestica Inc. (Canada)

KEY INDUSTRY DEVELOPMENTS

- October 2025 – Reghelps SRC, a contract research organization (CRO), launched its comprehensive clinical research services for global medical device and in-vitro diagnostic device (IVD) manufacturers in India. This helped the company to increase its brand presence.

- October 2025 – Lords Mark Industries Ltd, a contract manufacturing organization, received orders for its range of surgical consumables, orthopaedic supports, and hygiene products.

- April 2025 – T&D Diagnostics collaborated with Genenest, a Noida-based biotech company, to manufacture its diagnostic range in India, aiming to strengthen its presence. Under this strategic partnership, Genenest will be an exclusive manufacturer in India for T&D’s Starkwert range of products.

- September 2025 – STRATEC, a contract research organization, attended the MEDICA conference in Germany with an aim to increase its brand presence in the market.

- November 2021 – Biofortuna, a specialist contract development and manufacturing partner, has doubled its manufacturing capacity. This helped the company increase its global brand presence.

REPORT COVERAGE

The market report provides a detailed global IVD contract manufacturing market analysis, focusing on key aspects such as leading companies, product types, technologies, service types, and end-users. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.59% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Product Type · Instruments · Consumables By Technology · Immunodiagnostics · Clinical Chemistry · Molecular Diagnostics · Hematology · Others By Service Type · Manufacturing Services · Assay Development Services · Others By End User · Medical Device Companies · Pharmaceutical & Biotechnology Companies · Academic & Research Institutes · Others By Region · North America (By Product Type, By Technology, By Service Type, By End User, and by Country) o U.S. (By Product Type) o Canada (By Product Type) · Europe (By Product Type, By Technology, By Service Type, By End User, and by Country/Sub-region) o U.K. (By Product Type) o Germany (By Product Type) o France (By Product Type) o Italy (By Product Type) o Spain (By Product Type) o Scandinavia (By Product Type) o Rest of Europe (By Product Type) · Asia Pacific (By Product Type, By Technology, By Service Type, By End User, and by Country/Sub-region) o China (By Product Type) o Japan (By Product Type) o India (By Product Type) o Australia (By Product Type) o Southeast Asia (By Product Type) o Rest of Asia Pacific (By Product Type) · Latin America (By Product Type, By Technology, By Service Type, By End User, and by Country/Sub-region) o Brazil (By Product Type) o Mexico (By Product Type) o Rest of Latin America (By Product Type) · Middle East & Africa (By Product Type, By Technology, By Service Type, By End User, and by Country/Sub-region) o GCC (By Product Type) o South Africa (By Product Type) o Rest of the Middle East & Africa (By Product Type) |

Frequently Asked Questions

The global IVD contract manufacturing market size was valued at USD 19.66 billion in 2025 and is projected to grow from USD 20.74 billion in 2026 to USD 37.23 billion by 2034, exhibiting a CAGR of 7.59% during the forecast period.

In 2025, the North America regional market value stood at USD 7.13 billion.

Growing at a CAGR of 7.59%, the market will exhibit steady growth over the forecast period (2026-2034).

By product type, the consumables segment is the leading segment in this market.

The increasing outsourcing of IVD diagnostics is one of the major factors driving the market's growth.

Thermo Fisher Scientific Inc., and Argonaut Manufacturing Services Inc., are the major players in the global market.

North America dominated the market share in 2025.

The growing prevalence of chronic conditions, the increasing complexity of newer diagnostics, and other factors are some of the key factors expected to boost the adoption of these services globally.

- 2021-2034

- 2025

- 2021-2024

- 261

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us