Carbon Prepreg Market Size, Share & Industry Analysis, By Resin Type (Epoxy-based Carbon Prepreg, Phenolic-based Carbon Prepreg, BMI and polyimide based Prepreg, and Thermoplastic Carbon Prepreg (PEEK, PEKK, and PPS)), By End-Use Industry (Aerospace & Defence, Automotive & Transportation, Wind Energy, Sporting Goods, Industrial, and Others), and Regional Forecast, 2026-2034

Carbon Prepreg Market Overview

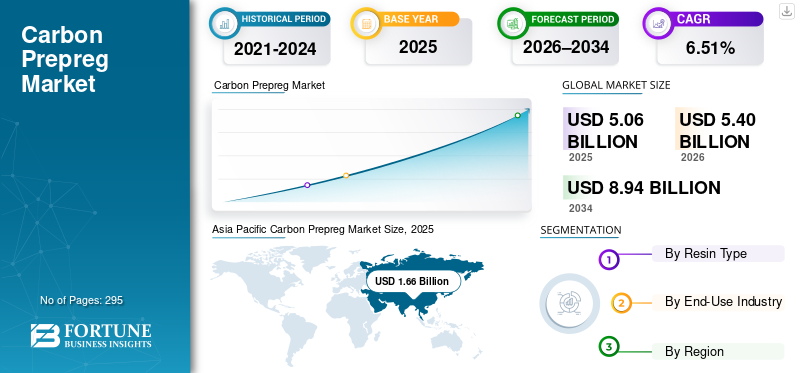

The global carbon prepreg market size was valued at USD 5.06 billion in 2025. The market is projected to grow from USD 5.40 billion in 2026 to USD 8.94 billion by 2034, exhibiting a CAGR of 6.51% during the forecast period. Asia Pacific dominated the carbon prepreg market with a market share of 32.80% in 2025.

Carbon prepreg, also known as pre-impregnated carbon fiber, is a semi-finished composite material in which carbon fiber reinforcements are pre-impregnated with a precisely controlled amount of resin, typically epoxy, phenolic, BMI, polyimide, or thermoplastic matrices during manufacture. Structural lightweighting needs, renewable energy scale-up, and performance-critical manufacturing requirements drive product demand.

Aircraft OEMs continue to prioritize weight reduction and structural efficiency to meet fuel-efficiency and emissions targets. Carbon prepregs provide consistent mechanical performance, tight tolerances, and certification reliability, therefore maintaining structural demand across commercial aircraft, defense platforms, UAVs, and space applications.

- For instance, more than 50% of the Boeing 787 and Airbus A350 XWB airframes are made of carbon fiber Hexcel is a major supplier to both programs and was awarded a contract by Airbus to supply the primary structure prepreg, made with Hexcel carbon fiber, for the A350 XWB program.

Many key industry players, including Hexcel Corporation, Toray Advanced Composites, Teijin Composites, SGL Carbon, and Advanced Composites Group, operating in the market, are focusing on developing innovative products to meet the rising demand.

Download Free sample to learn more about this report.

CARBON PREPREG MARKET TRENDS

Shift Toward Out-of-Autoclave (OOA) Prepregs is the Latest Market Trend

The shift toward Out-of-Autoclave (OOA) prepregs has emerged as one of the most significant recent trends in the market, driven by the need to reduce manufacturing cost, cycle time, and capital intensity.

Traditionally, carbon prepregs, especially in aerospace, have relied on autoclave curing, which requires high-pressure vessels, long cure cycles, and substantial energy consumption. These factors limit production scalability and make prepregs economically viable only for high-value, low-volume applications. OOA prepregs are engineered to cure under vacuum and oven conditions, eliminating the need for autoclaves while still achieving aerospace-grade mechanical performance and void control.

Advances in resin chemistry, fiber wet-out control, and prepreg architecture have significantly narrowed the performance gap between autoclave and OOA systems. As a result, OOA prepregs are increasingly being adopted in aerospace secondary structures, UAVs, defense platforms, wind energy components, and industrial applications, where cost efficiency and throughput are critical.

This shift enables manufacturers to reduce capital expenditure, shorten production cycles, and increase flexibility in part sizes and facility layouts. Moreover, OOA prepregs improve accessibility for emerging composite users, accelerating adoption beyond traditional aerospace programs. Therefore, the transition to OOA prepregs represents a structural change that expands the addressable market for carbon prepregs while preserving performance reliability.

- For instance, Boeing and Spirit AeroSystems have been working with OOA prepreg systems (such as those from Hexcel & Solvay) for secondary and large structures that do not require autoclave processing. These materials help reduce tooling costs and cycle times for parts such as access panels, fairings, and control surfaces. Hexcel and Solvay both highlight OOA prepregs on their product pages, noting that they are used in Boeing programs.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Need for Higher-Capacity Onshore and Offshore Turbines to Boost Market Growth

The global wind energy sector is undergoing a structural transition toward larger, higher-capacity onshore and offshore turbines, fundamentally reshaping blade design and material requirements. Next-generation turbines increasingly feature rotor diameters of 160-220 meters, significantly increasing bending loads, gravitational forces, and cyclic fatigue stresses acting on the blades.

At these dimensions, glass fiber-based composites approach their performance limits, as further increases in laminate thickness result in excessive blade weight, higher deflection, and reduced fatigue life. Carbon prepregs, therefore, become critical in spar caps and other high-load structural zones, as they offer a superior stiffness-to-weight ratio, enabling longer blades without proportional weight penalties. This shift represents a structural necessity rather than a discretionary material upgrade for next-generation turbine designs.

As offshore wind installations expand and average blade lengths continue to increase, carbon prepregs are transitioning from a niche reinforcement material to a core structural component in modern wind turbine blades.

Aerospace Lightweighting and Fuel-Efficiency Requirements to Bolster Market Growth

The aerospace industry continues to face increasing pressure to improve fuel efficiency, reduce operating costs, and meet stricter emission targets. Aircraft weight reduction remains one of the most effective levers to achieve these objectives, directly influencing fuel burn, payload capacity, and lifecycle emissions. Carbon prepregs are central to this strategy, as they enable the manufacture of lightweight, high-strength structures with exceptional fatigue resistance and dimensional stability.

Modern commercial and military aircraft programs rely heavily on pre-impregnated carbon fiber for primary and secondary structural components, including fuselage sections, wings, control surfaces, and empennage structures. Unlike alternative composite formats, prepregs offer precise fiber–resin control, repeatable quality, and certification reliability, which are critical in safety-critical aerospace applications.

MARKET RESTRAINTS

High Material and Processing Costs To Hamper The Market Growth

One of the primary restraints on market growth is the high total cost of materials and processing compared to alternative composite and metallic solutions. Carbon prepregs incorporate high-cost carbon fiber and specialty resin systems, controlled impregnation processes, stringent quality assurance, and cold-chain logistics, all of which elevate their delivered cost.

In addition to material pricing, traditional prepreg processing often requires autoclave curing, long cycle times, and capital-intensive equipment, increasing manufacturing complexity and limiting scalability. These cost and infrastructure requirements restrict product adoption in price-sensitive, high-volume applications such as mass-market automotive, construction, and general industrial components, where lower-cost glass composites or metals remain more economical.

MARKET OPPORTUNITIES

Expansion of Thermoplastic and Out-of-Autoclave Prepregs May Create Lucrative Growth Opportunities

Advancements in thermoplastic resin systems and out-of-autoclave (OOA) prepreg technologies are creating significant opportunities for the carbon prepreg market growth by lowering processing costs and expanding the addressable end-use applications. Thermoplastic carbon prepregs such as PEEK, PEKK, and PPS offer faster cycle times, weldability, and recyclability, making them better suited for automotive, industrial, and high-rate aerospace applications compared to traditional thermoset prepregs.

At the same time, OOA prepregs reduce reliance on capital-intensive autoclaves by enabling curing under vacuum and oven conditions. This improves manufacturing economics, allows larger part sizes, and reduces barriers for new composite users. As a result, carbon prepregs become viable for industrial automation, energy infrastructure, advanced mobility platforms, and cost-sensitive wind applications.

These technologies do not just replace existing prepreg demand but unlock new use cases where pre-impregnated carbon fiber were previously cost-prohibitive. Therefore, the continued development and qualification of thermoplastic and OOA prepregs represent a major opportunity to expand both the volume base and the geographic reach of the market over the medium- to long-term.

MARKET CHALLENGES

Supply Chain Complexity and Shelf-Life Constraints Pose a Critical Challenge to Market Growth

A major challenge facing the market is the complexity of storage, handling, and logistics, particularly for thermoset-based prepregs. Most carbon prepregs require refrigerated storage and controlled out-life management to prevent premature resin curing or performance degradation. This creates additional operational costs and inventory risks for manufacturers, distributors, and end users.

For high-volume or geographically dispersed production environments such as wind blade manufacturing or emerging industrial applications, maintaining a cold-chain infrastructure can be logistically demanding and economically burdensome. Limited shelf life also restricts flexibility in production planning, increases material waste, and complicates scaling in regions with less-developed composite infrastructure.

Although advances in OOA and thermoplastic prepregs are gradually alleviating some of these constraints, qualification cycles and process changes take time, particularly in regulated industries. Therefore, supply chain and shelf-life management remain a persistent challenge, slowing adoption and limiting the speed at which pre-impregnated carbon fiber can penetrate cost-sensitive and high-throughput applications despite strong underlying demand drivers.

Segmentation Analysis

By Resin Type

Epoxy-based Carbon Prepregs Segment Led due to Excellent Fatigue Resistance

Based on resin type, the market is segmented into epoxy-based carbon prepreg, phenolic-based carbon prepreg, BMI and polyimide based Prepreg, and thermoplastic carbon prepreg.

The epoxy-based carbon prepregs segment accounted for the largest carbon prepreg market share in 2025 due to their broad applicability, balanced performance characteristics, and established manufacturing ecosystem. Epoxy resin systems offer an optimal combination of high mechanical properties, excellent fatigue resistance, good thermal stability, and strong fiber adhesion, making them suitable for a wide range of structural and semi-structural applications.

BMI and polyimide based Prepreg, including vinyl ester systems, are used in applications where chemical resistance, corrosion protection, and cost considerations are important.

The thermoplastic carbon prepreg segment is anticipated to grow at a CAGR of 7.44% over the forecast period.

By End-Use Industry

To know how our report can help streamline your business, Speak to Analyst

Wind Energy Segment Led the Market Due To Structural Shift Toward Onshore And Offshore Wind Turbines

Based on end-use industry, the market is segmented into aerospace & defence, automotive & transportation, wind energy, sporting goods, industrial, and others.

The wind energy segment accounted for the dominant market share in 2025 and is expected to grow at the highest CAGR. This dominance is primarily driven by the structural shift toward larger onshore and offshore wind turbines, which require materials with superior stiffness-to-weight ratios to withstand higher bending moments and fatigue loads.

Aerospace & defence is the second-leading segment in the market. It represents the second-leading segment of the market, supported by the structural integration of prepregs in modern aircraft and defense platforms. Carbon prepregs are widely used in primary and secondary aircraft structures, including fuselages, wings, control surfaces, and empennage sections, due to their high strength, fatigue resistance, and dimensional stability.

Carbon Prepreg Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Carbon Prepreg Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific is estimated to reach USD 1.78 billion in 2026 and secure its position as the largest region in the market, driven primarily by the rapid expansion of wind energy capacity, growing aerospace manufacturing activity, and the increasing localization of composite material supply chains.

The region leads global wind energy installations, particularly in China and India, where the shift toward larger onshore and offshore turbines is driving higher product consumption in blade spar caps and structural reinforcements. This wind-led volume growth provides a strong base for market expansion. In parallel, Asia Pacific is witnessing steady growth in domestic aerospace and defense programs, including commercial aircraft, UAVs, and military platforms, which rely on carbon prepregs for lightweight and high-performance structures.

Japan Carbon Prepreg Market

The Japanese market in 2026 is estimated at around USD 0.18 billion, accounting for roughly 3.4% of global revenues. Japan represents a strategically important and high-value market within the Asia Pacific pre-impregnated carbon fiber landscape, driven primarily by its advanced aerospace ecosystem, strong materials manufacturing base, and leadership in high-performance composites.

China Carbon Prepreg Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.72 billion, representing roughly 13.4% of global sales. China represents the largest and fastest-growing carbon prepreg market in the Asia Pacific, driven primarily by its dominant wind energy sector, expanding domestic aerospace programs, and rapid localization of composite material supply chains.

To know how our report can help streamline your business, Speak to Analyst

India Carbon Prepreg Market

The Indian market in 2026 is estimated at around USD 0.29 billion, accounting for roughly 5.3% of global revenues. India represents a high-growth but still developing market, driven primarily by wind energy expansion, defense modernization, and increasing demand for advanced composites in industrial applications.

North America

North America is expected to hold a significant share in 2026, valued at around USD 1.63 billion. North America is expected to be the second-leading region in the market. North America has a strong presence in advanced air mobility, space launch vehicles, and defense modernization programs, which further support high-performance prepreg consumption. Aerospace & defense is the primary demand anchor in the region, supported by large commercial aircraft programs, military platforms, UAVs, and space systems.

U.S. Carbon Prepreg Market

The U.S. market can be analytically approximated at around USD 1.35 billion in 2026, accounting for roughly 25.0% of global sales. The U.S. accounts for the dominant share of the North American market, driven by its large-scale aerospace and defense ecosystem, advanced composite manufacturing base, and presence of leading prepreg suppliers. The U.S. hosts major commercial aircraft OEMs, defense contractors, and space companies, including Boeing, Lockheed Martin, Northrop Grumman, SpaceX, and Spirit AeroSystems, all of which rely extensively on pre-impregnated carbon fiber for structural and semi-structural components.

Europe

Europe is projected to grow at a CAGR of 6.22% over the coming years and reach a valuation of USD 1.59 billion by 2026. The region represents a structurally important and balanced market for carbon prepregs, driven by the dual influence of offshore wind energy expansion and a mature aerospace manufacturing ecosystem. The region accounts for a significant share of global carbon prepreg consumption, with demand spread across wind energy, aerospace & defence, automotive, and industrial applications.

U.K Carbon Prepreg Market

The U.K. market in 2026 is estimated at around USD 0.21 billion, representing roughly 4.0% of global revenues.

Germany Carbon Prepreg Market

Germany’s market is projected to reach approximately USD 0.35 billion in 2026, equivalent to around 6.5% of global sales.

Latin America and the Middle East & Africa

Latin America represents a small but fast-growing market, driven primarily by wind energy expansion and selective aerospace and industrial applications. The region’s demand is concentrated in countries such as Brazil and Mexico, where increasing investments in onshore wind energy are driving the adoption of pre-impregnated carbon fiber in spar caps and high-load blade sections for larger turbines. The Latin American market is set to reach a valuation of USD 0.23 billion in 2026. In the Middle East & Africa, the growth is supported by defense, aerospace, and early-stage renewable energy initiatives. Demand is primarily concentrated in the Gulf Cooperation Council (GCC) countries and South Africa, where investments in defense modernization, UAVs, and aerospace structures drive the use of high-spec carbon prepregs.

The Middle East & Africa reached USD 0.16 billion in 2025.

GCC Carbon Prepreg Market

The GCC market is projected to reach around USD 0.07 billion in 2026, representing roughly 0.03% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Moderately Consolidated Market with High Entry Barriers Favoring Established Players to Propel Market Progress

The market is moderately consolidated, with a limited number of technologically advanced, vertically integrated manufacturers. High entry barriers, including capital-intensive production processes, stringent certification requirements, long qualification cycles, and close OEM relationships, restrict new entrants and reinforce the dominance of established players. Hexcel Corporation, Toray Advanced Composites, Teijin Composites, SGL Carbon, and Advanced Composites Group are the largest players in the market.

Other notable players in the global market include Solvay S.A., Chomarat, Mitsubishi Chemical Group, and Solvay Composite Materials.

LIST OF KEY CARBON PREPREG COMPANIES PROFILED

- Hexcel Corporation (U.S.)

- Toray Industries, Inc. (Japan)

- Solvay S.A. (Belgium)

- Teijin Limited (Japan)

- Mitsubishi Chemical Group Corporation (Japan)

- SGL Carbon (Germany)

- Gurit Holding AG (Switzerland)

- Chomarat Group (France)

- Advanced Composites Group Ltd. (U.K.)

- Park Aerospace Corp. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Gurit announced a major long-term supply agreement for core material kits with one of the world’s leading wind turbine OEMs. The agreement secures continuous deliveries over the next five years, providing a stable and predictable business outlook for both parties. The contract is expected to generate approximately USD 325 million in net sales for Gurit over the full term, subject to the OEM’s demand levels.

- December 2025: Toray Industries, Inc. announced that it would implement price increases across its TORAYCA product portfolio, including carbon fiber, prepregs, fabrics, laminates, and other intermediate materials. The price adjustments, ranging from 10% to 20%, will take effect on shipments beginning in January 2026.

- May 2025: Hexcel Corporation and Specialty Materials announced a significant advancement in the development of a new high-modulus carbon fiber technology by Specialty Materials using Hexcel materials. Specialty Materials’ Hy-Bor technology combines Hexcel’s high-modulus carbon fiber with boron fiber, resulting in substantially improved compression strength and enabling a new class of advanced materials for airframe manufacturers and defense applications.

- September 2024: Hexcel announced the successful transition of its winter sports industry production to the new HexPly Nature bio-derived product range. This significant move includes the full conversion of HexPly M78.1-LT prepregs to the more sustainable HexPly Nature version, reflecting the company’s ongoing commitment to environmental sustainability and innovation.

- July 2024: Toray Composite Materials America, Inc., a leading producer and supplier of carbon fiber and prepreg materials, announced the signing of a memorandum of understanding (MOU) to designate Elevated Materials as a repurposing service provider for its Tacoma, Washington, facility. Under the three-year agreement, Elevated Materials would repurpose Toray’s scrap prepreg materials, including slit-edge waste and full-width prepreg sheets.

- March 2024: The Mitsubishi Chemical Group (MCG Group) announced that it has developed a carbon fiber prepreg material incorporating plant-derived resin, further expanding its BiOpreg portfolio. The company is introducing the BiOpreg #400 series, which includes both glass fiber and carbon fiber prepregs, and would begin sample production and evaluation of these products.

- October 2021: Teijin Limited announced that its carbon fiber subsidiary, Renegade Materials Corporation, a leading U.S.-based supplier of high-temperature thermoset prepregs, resins, and adhesives for the aerospace industry, plans to expand its prepreg production capacity by approximately 2.5 times.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.51% from 2026 to 2034 |

|

Unit |

Value (USD Billion) Volume (Kiloton) |

|

Segmentation |

By Resin Type, End-Use Industry, and Region |

|

By Resin Type |

· Epoxy-based Carbon Prepreg · Phenolic-based Carbon Prepreg · BMI and polyimide-based Prepreg · Thermoplastic Carbon Prepreg (PEEK, PEKK, and PPS) |

|

By End-Use Industry |

· Aerospace & Defence · Automotive & Transportation · Wind Energy · Sporting Goods · Industrial · Others |

|

By Region |

· North America (By Resin Type, End-Use Industry, and Country) o U.S. (By End-Use Industry) o Canada (By End-Use Industry) · Europe (By Resin Type, End-Use Industry, and Country) o Germany (By End-Use Industry) o U.K. (By End-Use Industry) o France (By End-Use Industry) o Italy (By End-Use Industry) o Rest of Europe (By End-Use Industry) · Asia Pacific (By Resin Type, End-Use Industry, and Country) o China (By End-Use Industry) o Japan (By End-Use Industry) o India (By End-Use Industry) o South Korea (By End-Use Industry) o Rest of Asia Pacific (By End-Use Industry) · Latin America (By Resin Type, End-Use Industry, and Country) o Brazil (By End-Use Industry) o Mexico (By End-Use Industry) o Rest of Latin America (By End-Use Industry) · Middle East & Africa (By Resin Type, End-Use Industry, and Country) o GCC (By End-Use Industry) o South Africa (By End-Use Industry) o Rest of Middle East & Africa (By End-Use Industry) |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 5.06 billion in 2025 and is projected to reach USD 8.94 billion by 2034

In 2025, the market value in the Asia Pacific stood at USD 1.66 billion.

The market is expected to grow at a CAGR of 6.51% over the forecast period (2026-2034).

By resin type, the epoxy-based carbon prepreg segment led the market.

Growing need for higher-capacity onshore and offshore turbines is the key driver of the market.

Hexcel Corporation, Toray Advanced Composites, Teijin Composites, SGL Carbon, and Advanced Composites Group are the major players in the global market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 295

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us