Lactate Monitoring Devices Market Size, Share & Industry Analysis, By Product Type (Lactate Meters (Handheld/Portable Lactate Meters, & Benchtop/Standalone Lactate Analyzers) and Consumables (Test Strips, Calibration Solutions & Reagents, Lancets, & Others), By Technology (Electrochemical Lactate Detection, Optical Lactate Detection, & Others), By Application (Clinical & Medical Applications, Sports & Fitness Applications, & Others), By End-user (Hospitals & Specialty Clinics, Sports Institutes & Professional Training Centers, & Others), and Regional Forecast, 2026-2034

Lactate Monitoring Devices Market Size and Future Outlook

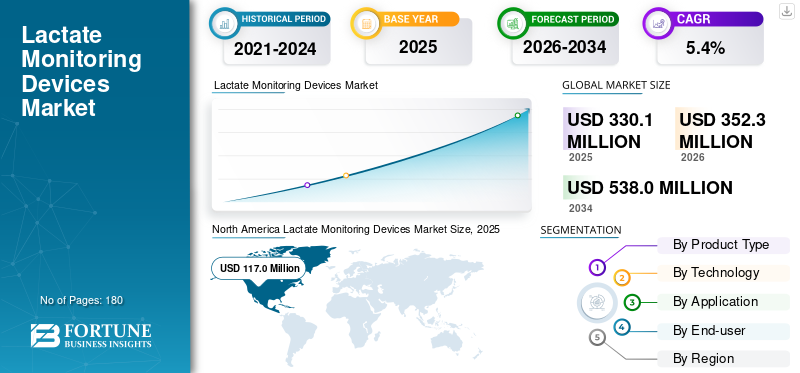

The global lactate monitoring devices market size was valued at USD 330.1 million in 2025. The market is projected to grow from USD 352.3 million in 2026 to USD 538.0 million by 2034, exhibiting a CAGR of 5.4% during the forecast period. North America dominated the lactate monitoring devices market with a market share of 35.44% in 2025.

The global lactate monitoring devices market covers point-of-care lactate meters, emerging wearable lactate systems, and the recurring consumables that keep these platforms running, such as strips, reagents/calibrators, lancets, and sensor-related disposables. Clinically, lactate is a fast proxy for tissue hypoperfusion and metabolic stress, so it is routinely used in emergency departments, ICUs, and peri-operative settings to help triage and monitor high-risk patients. Demand is rising as hospitals push for quicker decision-making at the bedside and as healthcare systems manage heavy acute-care volumes, reflecting the scale of potential testing environments. Alongside clinical demand, performance sports continue to adopt lactate monitoring to personalize training zones, while the steady progress of wearable biosensing is expanding the addressable base, illustrated by ongoing innovation in continuous, non-invasive biomarker sensing.

Furthermore, Werfen, Danaher, Siemens Healthineers, and Abbott held the largest market share, driven by increased investments and strategic initiatives, including new product launches, collaborations, and partnerships.

Download Free sample to learn more about this report.

Download Free sample to learn more about this report.

LACTATE MONITORING DEVICES MARKET TRENDS

Connected, Multi-Parameter, and Non-Invasive POCT Evolution is a Key Market Trend

Buyers increasingly expect POCT devices to behave as modern clinical tools: connected results, traceable operators, and workflows that fit busy wards. This is pushing vendors toward platforms that resemble glucose testing, such as simple strips, quick turnaround, and minimal blood volume, while also emphasizing accuracy claims suitable for critical decisions.

In CE markets, combined lactate plus hematology/hematocrit point-of-care systems highlight another trend: hospitals require clinical value per device footprint, particularly in sepsis screening and trauma workflows where multiple parameters are relevant. Meanwhile, in sports science, the story is moving from occasional lactate checks to continuous feedback loops. Reviews of sweat-lactate wearables underscore the appeal of non-invasive monitoring for long-duration assessments and lower infection risk, while also highlighting where validation and standardization are still needed before broad mainstream adoption.

MARKET DYNAMICS

MARKET DRIVERS

Faster Sepsis Recognition and Critical-Care Workflows to Drive the Market Growth

In acute care, lactate has become a practical tool for identifying early deterioration and tracking responses to fluids, oxygenation, and other interventions. The burden of sepsis and shock reinforces the clinical rationale. For instance, in 2025, the CDC notes that at least 1.7 million adults in the U.S. develop sepsis each year, and many of these patients are evaluated in time-sensitive settings where a quick lactate value can influence escalation decisions. As patient volumes normalize, post-pandemic and ED/ICU pathways focus on speed. Point-of-care meters and small-footprint analyzers are gaining appeal as they reduce wait times associated with central-lab routing and can be used near the patient with minimal sample volume.

On the supply side, established manufacturers continue to position lactate for frontline use. Companies highlight their heritage in lactate testing from hospital analyzers, translating it into portable formats for near-patient measurement, reinforcing buyer confidence in accuracy and reliability. Health systems’ broader activity rebound also supports consumables demand, underscoring the scale of inpatient throughput that can sustain routine lactate utilization in acute pathways.

MARKET RESTRAINTS

Method Standardization, Reimbursement Variability, and Platform Substitution to Limit Market Growth

Lactate is measured across multiple platforms, such as handheld strips, benchtop analyzers, blood gas systems, and central lab chemistry. Many hospitals already have entrenched workflows. This creates a practical headwind for pure-play lactate meters, even when clinicians value rapid lactate. Procurement teams may prefer consolidating testing onto existing systems, especially if blood gas analyzers are already embedded in ED/ICU routines.

In addition, lactate results must be consistent across operators and environments. Temperature, sample handling, and calibration practices can introduce variability, leading some sites to be cautious about expanding decentralized testing without strong quality controls. That burden often falls on POCT coordinators who must manage training, competency, and connectivity, work that is easier to justify in large hospitals than in smaller facilities. Operational risk is also a concern in high-throughput settings: Nova’s instruction materials emphasize infection-control awareness and disinfection practices as lactate meter components can be infectious, underscoring the workflow discipline required for safe scale-up.

Moreover, pricing pressure is significant. Consumables drive lifetime economics, and they are the first place hospitals negotiate. When tendering compresses strip pricing, suppliers may struggle to defend premium positioning unless they bundle connectivity, workflow, or multi-analyte value, an approach witnessed in combined lactate/hematology point-of-care propositions offered in CE markets.

MARKET OPPORTUNITIES

Expanding Wearable and Portable Lactate Monitoring Adoption Creates Growth Opportunities

The biggest opportunity lies in the area where lactate data is useful and easy to collect. Sports and fitness use lactate thresholds to fine-tune endurance programming. The adoption remains uneven as finger-prick spot checks are inconvenient at scale. Wearables that continuously estimate lactate from sweat or interstitial signals can lower that friction and shift lactate from an occasional test to a frequent insight, especially for elite teams and endurance communities. Although clinical-grade wearables are still in development, the growing interest in consumer biosensing is beneficial.

In parallel, humanitarian and remote-care contexts offer another opportunity; procurement catalogs used in field operations list portable lactate analyzers for point-of-care use, indicating demand where lab infrastructure is limited and rapid decisions matter. These efforts drive lactate monitoring devices market growth.

MARKET CHALLENGES

Clinical Validation, Comparability Across Matrices, and Scaled Adoption Outside Top Hospitals Challenges Market Growth

Rolling out lactate testing across busy hospitals requires effort. In clinical settings, test results can vary due to staff using different sampling techniques, improper device cleaning between patients, or failure to follow quality checks. As a result, many healthcare settings are hesitant to expand testing unless they can ensure adequate training and oversight. Manufacturers must design devices and instructions that ensure infection control and safe handling, as blood-based testing poses contamination risks and requires strict disinfection routines.

Wearable devices add another layer of complexity. Many systems focus on sweat lactate. However, sweat readings don’t map neatly to what clinicians rely on. Additionally, values can shift with hydration, temperature, skin differences, and exercise intensity. Developers must demonstrate accuracy and consistency under real-world conditions.

Moreover, adoption is often slowed by practical buying decisions. Hospitals prefer not to switch once a testing platform is standardized, as contracts, staff competency, and IT connectivity are tied to that ecosystem. Procurement teams may continue using existing devices, even if new ones are superior, unless the advantages are evident and the total costs are justifiable.

Segmentation Analysis

By Product Type

Recurring Use of Consumables in Several Healthcare Settings to Drive the Segment Growth

Based on product type, the market is segmented into lactate meters and consumables.

Additionally, lactate meters are further classified into handheld/portable lactate meters, benchtop/standalone lactate analyzers, and wearable lactate meters. Similarly, consumable is further segmented into test strips, calibration solutions & reagents, lancets, and others.

To know how our report can help streamline your business, Speak to Analyst

Consumables segment accounted for the largest lactate monitoring devices market share, as lactate monitoring is a repeat-testing workflow; strips and reagents are purchased continuously. At the same time, meters are replaced on multi-year cycles. In hospitals, serial lactate checks are common when clinicians track response to therapy in suspected sepsis, shock, or trauma, thereby the ongoing cost base naturally tilts toward consumables. Wearable systems also reinforce consumables' share over time, as disposable sensor elements and adhesives are regularly replaced.

Additionally, the lactate meters segment is projected to grow at a CAGR of 3.9% during the forecast period.

By Technology

Wide Utilization of Electrochemical Lactate Detection to Propel the Segment Growth

By technology, the market is classified into electrochemical lactate detection, optical lactate detection, microdialysis-based monitoring, and others.

Electrochemical lactate detection segment dominates, as it has proven performance in compact, low-power devices and pairs well with strip-based workflows at the point of care. This technology supports fast turnaround and small sample volumes, traits repeatedly emphasized in handheld meter positioning. Electrochemical approaches also scale well in clinical settings where operators vary, as test steps can be standardized and controlled through strip chemistry and calibration routines. Moreover, the segment is projected to hold a 77.4% share in 2026.

Additionally, the optical lactate detection segment is estimated to grow at a CAGR of 13.8% during the forecast period.

By Application

Rising Disease Prevalence to Propel the Clinical & Medical Applications Segment Growth

By application, the market is classified into clinical & medical applications, sports & fitness applications, and research applications.

Clinical & medical applications account for the largest market share, as lactate is closely linked to time-critical decision-making in emergency and critical care. The sepsis burden alone creates substantial testing demand. Moreover, the segment is projected to hold an 84.8% share in 2026.

Additionally, the sports & fitness applications segment is estimated to grow at a CAGR of 11.6% during the forecast period.

By End-user

Advanced Healthcare Infrastructure in Hospitals & Specialty Clinics to Propel the Segment Growth

On the basis of end-user, the market is classified into hospitals & specialty clinics, sports institutes & professional training centers, homecare settings, and others.

Hospitals & specialty clinics segment dominates the market, as they concentrate the highest-acuity cases in which lactate changes management, such as sepsis screening, trauma, shock, and peri-operative monitoring. They also have the infrastructure to run POCT programs, enabling broad deployment. Furthermore, the segment is set to hold 79.9% share in 2026.

In addition, the sports institutes & professional training centers segment is projected to grow at a CAGR of 12.0% during the forecast period.

Lactate Monitoring Devices Market Regional Outlook

Based on geography, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America Lactate Monitoring Devices Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America

North America held the largest revenue share valued at USD 110.3 million in 2024, and maintained its leading position in 2025 with USD 117.0 million. The regional market growth is driven by high-acuity care pathways that use lactate to triage and monitor rapidly deteriorating patients, especially in emergency and intensive care settings. The region also benefits from deep adoption of point-of-care testing, strong purchasing power, and a large installed base that continuously drives demand for consumables. In addition, the region’s high healthcare spending intensity supports faster uptake of newer device formats and connectivity features,which typically translates into higher utilization of rapid diagnostics and better-funded POCT programs.

U.S. Lactate Monitoring Devices Market

In 2026, the U.S. market is expected to represent USD 113.9 million, capturing 32.3% of total global revenue.

Europe

Europe is expected to achieve a 16.4% growth rate in the coming years, the second-highest globally, reaching USD 107.4 million by 2026. Europe’s market is supported by a large hospital activity base and continued emphasis on standardizing acute-care pathways across countries, which keeps lactate testing relevant in suspected sepsis, shock, trauma, and peri-operative care. Growth is further supported by investments in digital health infrastructure and POCT governance in larger systems. However, tender-based procurement and pricing pressure can moderate revenue growth even when test volumes rise.

U.K. Lactate Monitoring Devices Market

The U.K. market is projected to reach USD 18.1 million by 2026, accounting for 5.1% of the global market revenue.

Germany Lactate Monitoring Devices Market

Germany's market is anticipated to reach about USD 20.2 million by 2026, representing roughly 5.7% of global revenue.

Asia Pacific

In 2026, the Asia Pacific market is expected to be valued at USD 48.9 million, ranking as the third-largest globally. Asia Pacific’s market growth is typically faster, as the region continues to expand critical care capacity and improve access to rapid diagnostics across large, diverse healthcare systems. This increases the addressable base for lactate meters and their consumables. While per-capita spending is lower than in North America and Western Europe, utilization growth is often stronger due to improving hospital infrastructure, rising awareness of sepsis and shock management, and the expansion of emergency care networks in urban centers.

Japan Lactate Monitoring Devices Market

Japan is projected to generate approximately USD 14.6 million in revenue by 2026, contributing nearly 4.1% to the global market.

China Lactate Monitoring Devices Market

China’s market is likely to reach approximately USD 31.9 million by 2026, contributing about 9.1% to global revenues.

India Lactate Monitoring Devices Market

India is expected to contribute approximately USD 11.8 million to the market by 2026, corresponding to about 3.4% of global revenues.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa are anticipated to experience moderate market growth, with Latin America expected to reach around USD 17.3 million by 2026. Latin America’s growth is driven by the gradual expansion of hospital diagnostic capability, modernization of emergency and critical care services in major cities, and the increasing penetration of point-of-care tools, where laboratory turnaround times can be a constraint. Middle East & Africa growth is shaped by a mix of high-investment pockets, especially in Gulf countries and resource-constrained systems elsewhere, creating a two-speed adoption curve. In GCC markets, investments in tertiary hospitals, emergency medicine, and specialty centers support the adoption of point-of-care diagnostics. In many African markets, demand for lactate monitoring is often linked to improving acute care capabilities and infection management programs.

GCC Lactate Monitoring Devices Market

By 2026, the GCC market is expected to generate approximately USD 4.2 million in the market, accounting for nearly 1.2% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Robust Product Innovation to Reinforce the Market Position of Prominent Players

The global lactate monitoring devices market remains moderately fragmented, with a mix of established and emerging players. Key players such as Werfen, Danaher, Siemens Healthineers, and Abbott held the largest market share. These players compete heavily on turnaround time, analytical reliability, automated quality management, connectivity, and total cost of ownership, and they benefit from high switching costs once a hospital standardizes platforms.

Moreover, Other key players, such as F. Hoffmann-La Roche AG, Nova Biomedical, EKF Diagnostics, and ARKRAY, compete on simplicity, portability, sports/performance usability, and low cost per test, often winning in decentralized settings where fast lactate is needed without investing in larger systems. Over the next decade, competition is expected to intensify around wearable/continuous lactate, creating room for challengers while the hospital core remains concentrated.

LIST OF KEY LACTATE MONITORING DEVICES COMPANIES PROFILED

- Werfen (Spain)

- Danaher (U.S.)

- Siemens Healthineers (Germany)

- Abbott (U.S.)

- F. Hoffmann-La Roche AG (Switzerland)

- Nova Biomedical (U.S.)

- EKF Diagnostics (U.K.)

- ARKRAY (Japan)

- OPTI Medical Systems (U.S.)

- EDAN Instruments (China)

KEY INDUSTRY DEVELOPMENTS

- July 2025: Werfen announced the expansion of commercialization for the GEM Premier 7000 with the iQM3 blood gas testing system, following its success in North America. Building on strong clinical adoption and recognition in the U.S. and Canada, the system is now available in Europe.

- May 2025: Werfen achieved Silver Winner status in the prestigious Edison Awards’ Emergency and On-Site Health Solutions category for its GEM Premier 7000 with Intelligent Quality Management 3 (iQM3) blood gas testing system. This honor reinforces the breakthrough represented by this first-of-its-kind innovation, offering hemolysis detection at the point of care.

- December 2024: Getinge and 908 Devices announced their collaboration to integrate Getinge’s bioreactors with 908 Devices’ MAVEN for automated control of glucose and lactate levels in cell cultures. The combined solution will help scientists measure critical process parameters in bioreactors, enabling continuous, real-time analysis without manual sampling.

- August 2024: Researchers from NUS Institute for Health Innovation & Technology (iHealthtech) and the Flexible Electronics Department of A*STAR’s Institute of Materials Research and Engineering (A*STAR’s IMRE) developed a wearable, stretchable sensor for quick, continuous, and non-invasive detection of solid-state skin biomarkers.

- July 2024: Werfen introduced the GEM Premier 7000 with Intelligent Quality Management 3 (iQM3) at the Association for Laboratory Medicine (ADLM) Annual Meeting (formerly the American Association for Clinical Chemistry), which has received 510(k) clearance by the U.S. Food and Drug Administration.

- July 2024: EKF Diagnostics Holdings plc announces the launch of its new Biosen C-Line, an advanced version of its industry-leading rapid benchtop glucose and lactate analyzer.

- January 2024: Abbott introduced Lingo across the U.K. It is a pioneering biowearable device and app designed to help people improve their overall health and wellbeing.

REPORT COVERAGE

The report provides an in-depth analysis of all market segments, highlighting key drivers, trends, opportunities, restraints, and challenges. It also provides insights into technological advancements, key industry developments, company market share analysis, and profiles of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.6% from 2026 to 2034 |

| Unit | Value (USD Million) |

| By Device Type |

|

| By Indication |

|

| By End-user |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 330.1 million in 2025 and is projected to reach USD 538.0 million by 2034.

In 2025, the North American market value stood at USD 117.0 million.

The market is expected to exhibit a CAGR of 5.4% during the forecast period.

The consumables segment led the market by product type.

The key factors driving the market are rising disease burden and unaddressed functional needs.

Werfen, Danaher, Siemens Healthineers, and Abbott are some of the major players in the market.

North America dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us