Lactose-Free Products Market Size, Share & Industry Analysis, By Product Type (Milk [Plain, Low-fat, Flavored, Functional, and Others], Yogurt [Spoonable, Drinking, and Others], Cheese [Cheddar, Mozzarella, Parmesan, Cream Cheese, and Others], Frozen Desserts, and Others), By Nature (Organic and Conventional), By Packaging Type (Bottles, Cartons, Tubs, and Others), By Distribution Channel (Food Service and Retail [Supermarkets/Hypermarkets, Convenience Stores, Online Retail and Others]), and Regional Forecast, 2026-2034

Lactose-Free Products Market Size and Future Outlook

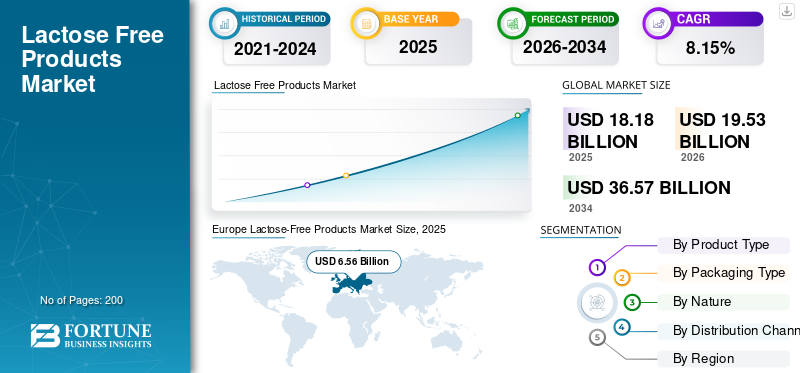

The global lactose-free products market size was valued at USD 18.18 billion in 2025. The market is projected to grow from USD 19.53 billion in 2026 to USD 36.57 billion by 2034, exhibiting a CAGR of 8.15% during the forecast period. Europe dominated the lactose free products market with a market share of 36.08% in 2025.

Lactose-free products include dairy and dairy-alternative offerings such as milk, yogurt, ice cream, cheese, and desserts that are processed to remove lactose while retaining nutritional value. Demand is driven by the rising prevalence of lactose intolerance, growing awareness of digestive health, and the increasing adoption of specialized dietary products across both developed and emerging economies. The market is further supported by innovation in plant-based formulations, enzyme-treated dairy products, and clean-label offerings that target consumer health consciousness.

The global market is led by key companies, including Nestlé S.A., Danone S.A., Arla Foods amba, Lactalis Group, and The Coca-Cola Company (Fairlife). These companies compete through product innovation, expansion of lactose-free dairy products, strategic partnerships, and investments in functional nutrition.

Download Free sample to learn more about this report.

Lactose-Free Products Market Trends

Rising Prevalence of Lactose Intolerance and Digestive Health Awareness to Shape Industry Trends

Consumers are increasingly shifting toward lactose-free and digestive-friendly food products due to growing awareness of gastrointestinal health and intolerance-related issues. This trend is particularly prominent in Asia Pacific and Latin America, where lactose intolerance rates are significantly higher. Manufacturers are responding by expanding lactose-free dairy lines, introducing fortified and functional variants, and improving taste profiles to match conventional dairy products.

- For instance, in November 2025, Remilk and Gad Dairies launched "The New Milk," a precision-fermented, cow-free dairy milk that matches traditional milk in taste, texture, and nutrition. This innovative milk uses real milk proteins produced through fermentation, making it lactose-free and 75% lower in sugar.

MARKET DYNAMICS

Market Drivers

Download Free sample to learn more about this report.

Rising Global Demand for Functional and Specialized Dairy Products to Support Market Growth

The increasing demand for functional and specialized food products is driving the lactose-free products market growth. Consumers are actively seeking products that address specific dietary needs, such as those for lactose intolerance, digestive sensitivity, and gut health. Moreover, rising disposable incomes, urbanization, and increasing penetration of modern retail formats are further accelerating the product adoption globally.

- According to the World Bank Data, India’s GDP per capita reached around USD 2,694 in 2024, with continued steady growth supported by economic expansion and urbanization.

Market Restraints

High Production Costs and Limited Consumer Awareness in Emerging Markets to Restrict Growth

The production of lactose-free products involves enzymatic processing, specialized filtration, and quality control measures, leading to higher costs compared to conventional dairy products. These cost pressures often translate into premium pricing, limiting accessibility in price-sensitive markets.

Limited awareness regarding lactose intolerance and the availability of alternatives in developing regions restricts widespread adoption. Supply chain challenges, including cold storage requirements and shorter shelf life for certain products, further constrain market expansion.

- According to the Tetra Pak Dairy Processing Handbook, lactose-free dairy requires lactase enzyme treatment and ultrafiltration, increasing production costs by approximately 20–30% compared to conventional dairy.

Market Opportunities

Growing Demand from Foodservice and Institutional Channels to Expand Market Reach

The increasing incorporation of lactose-free options in foodservice, hospitality, and institutional catering is opening new revenue streams for manufacturers. Restaurants, cafes, hotels, and airlines are expanding their menus to include lactose-free milk, desserts, and beverages to cater to dairy-sensitive consumers. This trend is particularly strong in urban markets, where consumers expect inclusive menu offerings, thereby accelerating B2B demand for lactose-free products.

- USDA Economic Research Service (ERS) data show that food-away-from-home (FAFH) spending has become a dominant component of total food expenditure, frequently surpassing 50% in developed economies such as the U.S.

SEGMENTATION ANALYSIS

By Product Type

Milk Segment Dominated Market Due to Its High Consumption and Everyday Usage Across Households

Based on product type, the market is segmented into milk, yogurt, cheese, frozen desserts, and others.

The milk segment dominated the market, valued at USD 12.28 billion in 2025, driven by its staple nature, widespread consumer acceptance, and strong penetration across both developed and emerging markets. Lactose-free milk serves as the primary substitute for conventional dairy, making it the most accessible and frequently purchased category. Within this segment, plain and low-fat variants account for a significant share due to their alignment with daily dietary consumption.

The cheese segment is projected to grow at the fastest CAGR of 10.13% during the forecast period, supported by increasing demand for premium dairy products, rising adoption in foodservice applications, and expanding availability of lactose-free specialty cheese products, including mozzarella, parmesan, and cream cheese.

To know how our report can help streamline your business, Speak to Analyst

Conventional Segment Dominated Market Due to Its Affordability and Wider Availability

Based on nature, the market is bifurcated into organic and conventional.

The conventional segment dominated the global market, reaching USD 14.87 billion in 2025, owing to its cost-effectiveness, large-scale production, and widespread availability across retail channels. Conventional lactose-free products cater to a broader consumer base, particularly in price-sensitive markets where affordability remains a key purchasing factor.

The organic segment is expected to grow at the fastest CAGR of 8.94% during the forecast period, driven by increasing consumer preference for clean-label, chemical-free, and sustainably sourced food products.

By Packaging Type

Cartons Segment Dominated Market Due to Extended Shelf Life and Efficient Storage

Based on packaging type, the market is segmented into bottles, cartons, tubs, and others.

The cartons segment held the leading position, valued at USD 8.83 billion in 2025, supported by its ability to extend product shelf life, maintain product freshness, and offer cost-effective transportation and storage. Carton packaging is widely used for lactose-free milk and beverages, making it the most preferred format among manufacturers and retailers.

The tubs segment is projected to grow at the fastest CAGR of 9.52% during 2026–2034, driven by increasing consumption of lactose-free yogurt, desserts, and ready-to-eat products.

By Distribution Channel

Retail Segment Dominated Market Due to the Strong Presence of Supermarkets and Hypermarkets

Based on distribution channel, the market is categorized into food service and retail, with retail further segmented into supermarkets/hypermarkets, convenience stores, online retail, and others.

The retail segment dominated the global lactose-free products market share, accounting for USD 14.98 billion in 2025, supported by extensive distribution networks, strong shelf visibility, and consumer preference for in-store purchases of dairy products.

The food service segment is expected to witness the fastest CAGR of 9.57% during 2026–2034.

Lactose-Free Products Market Regional Outlook

Regionally, the market is studied across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Europe

Europe Lactose-Free Products Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe accounted for the largest market share, valued at USD 6.56 billion in 2025, and is projected to reach USD 12.56 billion by 2034, registering a CAGR of 7.56% (2026–2034). The region benefits from well-established dairy consumption, strong regulatory frameworks, and high adoption of lactose-free and organic dairy products.

Germany Lactose-Free Products Market

Germany is one of the leading markets in Europe, valued at approximately USD 1.45 billion in 2025, supported by high consumption of lactose-free milk and yogurt, along with the strong presence of domestic dairy producers.

U.K. Lactose-Free Products Market

The U.K. market was valued at approximately USD 1.32 billion in 2025, driven by increasing demand for functional, plant-based, and lactose-free dairy alternatives among health-conscious consumers.

North America

North America was valued at USD 5.29 billion in 2025 and is projected to reach USD 10.92 billion by 2034, growing at a CAGR of 8.47% (2026–2034). Growth in the region is primarily driven by high awareness of lactose intolerance, strong demand for functional and digestive health products, and widespread availability of lactose-free dairy across retail and foodservice channels.

U.S. Lactose-Free Products Market

The U.S. dominates the North American market, valued at approximately USD 4.14 billion in 2025, supported by increasing consumption of lactose-free milk, yogurt, and protein-enriched dairy beverages.

Asia Pacific

Asia Pacific was valued at USD 4.26 billion in 2025 and is projected to reach USD 9.76 billion by 2034, growing at the fastest CAGR of 9.72% (2026–2034). Growth is driven by high lactose intolerance prevalence, rapid urbanization, and increasing disposable income across emerging economies.

China Lactose-Free Products Market

China represents the largest market in the region, valued at approximately USD 1.46 billion in 2025, supported by increasing awareness of digestive health and rising demand for specialized dairy nutrition.

South America and Middle East & Africa

South America was valued at USD 1.22 billion in 2025 and is projected to reach USD 2.05 billion by 2034, registering a CAGR of 5.98% (2026–2034). Growth is supported by improving retail infrastructure, rising health awareness, and increasing adoption of specialized dairy products.

The Middle East & Africa market was valued at USD 0.85 billion in 2025 and is projected to reach USD 1.28 billion by 2034, expanding at a CAGR of 4.70% (2026–2034). Growth is driven by urbanization, increasing demand for digestive health products, and rising dependence on packaged dairy.

Brazil Lactose-Free Products Market

Brazil dominates the regional market, valued at approximately USD 0.71 billion in 2025, driven by strong dairy consumption and increasing demand for lactose-free milk and yogurt products.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Product Innovation, Functional Nutrition, and Global Portfolio Expansion

The global lactose-free products market is moderately consolidated, with a mix of multinational dairy corporations and specialized nutrition companies competing through product innovation, geographic expansion, and strong brand positioning. Leading players are increasingly expanding their lactose-free portfolios across milk, yogurt, cheese, and other functional dairy categories to meet rising demand for digestive-friendly, clean-label products. Companies are also investing in advanced enzyme-processing technologies and plant-based integrations to enhance product quality and diversify their offerings.

Key Players in the Market

|

Rank |

Company Name |

|

1 |

Nestlé S.A. |

|

2 |

Danone S.A. |

|

3 |

Arla Foods amba |

|

4 |

Lactalis Group |

|

5 |

The Coca-Cola Company |

List of Key Lactose-Free Products Companies Profiled

- Nestlé S.A. (Switzerland)

- Danone S.A. (France)

- Arla Foods amba (Denmark)

- Lactalis Group (France)

- The Coca-Cola Company (U.S.)

- Valio Ltd. (Finland)

- FrieslandCampina (Netherlands)

- Fonterra Co-operative Group Limited (New Zealand)

- Saputo Inc. (Canada)

- Organic Valley (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Horizon Organic recently launched no-added-sugar, lactose-free 1% lowfat chocolate milk boxes. These shelf-stable, single-serve products (8 fl oz each) use organic milk, organic cocoa, and plant-based sweeteners such as stevia and monk fruit, delivering full chocolate flavor without added sugars.

- June 2025: Daiya launched Chipotle Cheddar Shreds and Pepper Jack Slices to expand its plant-based cheese lineup with spicy, dairy-free options. These use a proprietary Oat Cream™ blend for creamy meltability, targeting flexitarians and flavor seekers in tacos, burgers, and grilled cheese.

- January 2025: RIND by Dina & Joshua, a Brooklyn-based vegan cheese brand, launched ALPINE SVVISS in the U.S. This cashew-based, artisan Swiss-style cheese mimics the nutty, savory profile of traditional Swiss, made gluten-free, cholesterol-free, and Kosher Pareve certified.

- June 2024: Violife launched Canada’s first 100% dairy-free cream cheese block, called the Creamy Block. This plant-based innovation from the UK's leading dairy-free brand mimics traditional cream cheese's rich, tangy profile using coconut oil, potato starch, and lentil protein, making it whippable, spreadable, and bakeable for recipes such as cheesecakes or bagels.

- August 2023: Skyrrup, an Indian dairy brand under Bharat Skyr & Doodh Products, launched its lactose-free Greek yogurt to target health-conscious consumers, particularly those with lactose intolerance. Made from A2 cow milk, it offers high protein (around 7.5g per serving), probiotics, low fat, no added sugars or preservatives, and a creamy texture achieved by straining whey.

REPORT COVERAGE

The global lactose-free products market industry report analyzes the market in depth and highlights crucial aspects such as global market overview, trends, market dynamics, prominent companies, investment in research and development, and end-use. Besides this, the report also provides insights into the global market analysis and highlights significant industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.15% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Product Type

|

|

By Packaging Type

|

|

|

By Nature

|

|

|

By Distribution Channel

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market was valued at USD 18.18 billion in 2025 and is anticipated to reach USD 36.57 billion by 2034.

At a CAGR of 8.15%, the global market will exhibit steady growth over the forecast period.

By packaging type, the cartons segment led the market.

Europe held the largest market share in 2025.

Rising global demand for functional and specialized dairy products is expected to support market growth.

Nestle S.A., Danone S.A., Arla Foods amba, Lactalis Group, and The Coca-Cola Company are the leading players in the market.

Rising prevalence of lactose intolerance and digestive health awareness to shape industry trends.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Jun 2026)

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us