Leadless Pacemakers Market Size, Share & Industry Analysis, By Device Type (Single-Chamber Leadless Pacemakers and Dual-Chamber Leadless Pacemakers), By Indication (Atrial Fibrillation with Bradycardia, Sinus Node Dysfunction, Atrioventricular (AV) Block, and Others), By End-user (Hospitals and ASCs, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

Leadless Pacemakers Market Size and Future Outlook

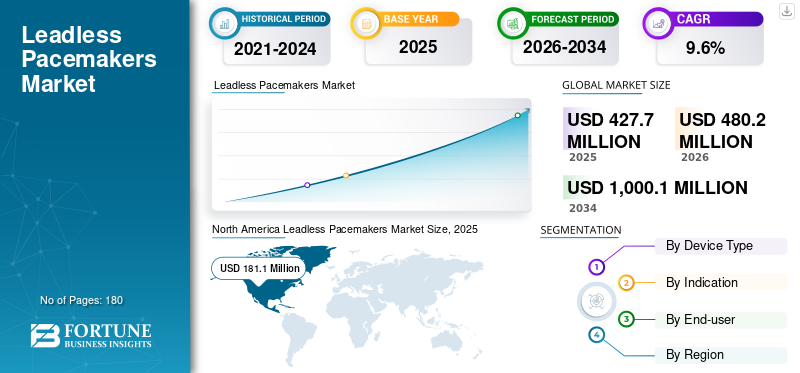

The global leadless pacemakers market size was valued at USD 427.7 million in 2025. The market is projected to grow from USD 480.2 million in 2026 to USD 1,000.1 million by 2034, exhibiting a CAGR of 9.6% during the forecast period. North America dominated the leadless pacemakers market with a market share of 42.34% in 2025.

Leadless pacemakers are miniaturized cardiac rhythm devices implanted directly inside the heart via a catheter, eliminating the surgical pocket and transvenous leads used in traditional systems. By removing leads, which are a common source of infection and mechanical failure, these devices are increasingly considered for patients who need pacing but are at higher risk of lead- or pocket-related complications. Market growth is being propelled by an aging population, expanding electrophysiology (EP) capability, and steady product improvements that make leadless therapy suitable for more patients. The technology has also moved beyond early single-chamber use cases toward broader indications as manufacturers add longer battery life, better sensing, and atrioventricular (AV) synchrony features.

Medtronic plc and Abbott held the largest share of the global leadless pacemakers market, driven by the presence of other players and market consolidation.

Download Free sample to learn more about this report.

LEADLESS PACEMAKERS MARKET TRENDS

Growing Clinical Evidence to Boost Market Growth

A clear trend is the move from novelty to evidence-driven adoption: clinical study activity and post-approval outcomes reporting are expanding, helping physicians clarify which patient profiles benefit most from leadless systems and how to manage follow-up. Abbott's Aveir DR i2i study registered on ClinicalTrials.gov reflects this push to quantify the safety and effectiveness of dual-chamber leadless pacing in a structured, multi-center setting.

In practice, high-visibility procedures often catalyze local adoption; for example, reports of early Aveir DR implants outside the U.S. highlight how flagship hospitals use these cases to build patient awareness and physician confidence. At the same time, manufacturers are positioning leadless systems as part of a broader rhythm-management ecosystem that includes programming tools and follow-up pathways.

Another emerging trend is a gradual convergence of leadless pacing with more physiologic pacing expectations, meaning hospitals increasingly evaluate complication avoidance, and how well leadless systems meet real-world pacing needs across AV block and sinus node dysfunction populations.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Clinical and Economic Push to Avoid Lead-Related Complications to Boost Market Development

Demand for leadless pacemakers is rising as they remove two persistent pain points of conventional pacing: the surgical pocket and the transvenous lead. In day-to-day practice, leads and pockets can be associated with infection risk, venous obstruction, lead dislodgement, insulation failure, and the need for revision procedures, events that are stressful for patients and also costly for hospitals and payers. By placing the device directly inside the heart through a minimally invasive catheter-based approach, leadless systems can shorten recovery time for suitable patients, reduce visible scarring, and simplify post-implant care in many cases.

This clinical value is reinforced by the reality that the pacing-eligible population is expanding as societies age and bradyarrhythmias are diagnosed more frequently through better screening and monitoring. At the same time, health systems are under pressure to improve outcomes while controlling complications and readmissions, which favors therapies that can lower downstream procedural burden. As evidence and physician familiarity increase, leadless pacing is being adopted earlier in the treatment pathway for selected patient groups, supporting steady growth in both procedure volume and device revenue.

MARKET RESTRAINTS

High Cost Price to Limit Market Growth

Despite strong momentum, leadless pacemakers still face real-world constraints that slow universal substitution of conventional devices. Clinically, patient selection remains tighter than for transvenous systems as leadless therapy historically served primarily right-ventricular pacing needs, while many patients benefit from more complex pacing strategies. Although dual-chamber leadless systems broaden candidacy, adoption takes time as implant workflows, troubleshooting, and follow-up protocols must mature across community hospitals and emerging markets.

On the economic side, leadless devices command a premium price. They can face procurement scrutiny, especially when reimbursement is bundled when diagnosis-related group (DRG) payments are pressured, or when hospital capital committees prioritize "standard of care" devices.

Additionally, training and proctoring requirements can be a gating factor for lower-volume centers, and some geographies experience limited access to EP labs equipped and staffed for advanced pacing implants. These frictions can be witnessed even when headline approvals occur, but early commercial expansion depends on site readiness and rollout pace.

MARKET OPPORTUNITIES

Dual-chamber Leadless Systems to Create Significant Growth Opportunities

The most meaningful opportunity over the next decade is the shift from a niche "selected patient" therapy to a more mainstream pacing option as dual-chamber leadless systems scale. Dual-chamber capability matters as it targets a much larger pool of bradycardia patients who need coordination between the atria and ventricles. For instance, in July 2023, the FDA approved Abbott's Aveir DR, the world's first dual-chamber leadless pacemaker system, marking a pivotal expansion point for the category.

Early real-world ramp signals are also emerging, a milestone that typically precedes broader contracting and training waves. Beyond the U.S., there is opportunity in markets where EP capabilities are expanding, and large tertiary hospitals are adopting global standards of minimally invasive cardiac care, often supported by physician-to-physician education and center-of-excellence models. As device platforms mature and battery longevity improves, stakeholders may also re-evaluate long-term value, such as fewer lead revisions, and fewer pocket issues, which can strengthen the reimbursement narrative and improve procurement acceptance.

MARKET CHALLENGES

Lack of Trained Implanters to Complicate Market Growth

Leadless pacemakers simplify some aspects of implantation but introduce new operational challenges. Scaling the market requires more trained implanters, consistent proctoring availability, and standardized complication management across diverse hospital settings. Long-term device management is another hurdle: as patient needs evolve, clinicians must plan for retrieval, replacement, or "device stacking" strategies, and the optimal approach can vary by patient anatomy, device generation, and implant duration.

Health systems also need robust follow-up infrastructure to ensure device checks, symptom monitoring, and coordination with broader AF and heart-failure care pathways. Epidemiology adds pressure, and the growing AF population increases the pool of patients who may progress to bradycardia-related pacing needs, stretching specialist capacity in many regions. Finally, global uptake remains uneven as the market depends heavily on EP lab availability, cath-lab scheduling, and payer willingness to fund a premium device category. These constraints are often most acute outside major urban referral centers.

Segmentation Analysis

By Device Type

Single-Chamber Leadless Pacemakers Leads due to Well-Defined and Common Clinical Need

Based on device type, the market is segmented into single-chamber leadless pacemakers and dual-chamber leadless pacemakers.

To know how our report can help streamline your business, Speak to Analyst

The single-chamber leadless pacemakers segment maintain the largest share, as it addresses a well-defined and common clinical need, right ventricular pacing for patients where single-chamber therapy is appropriate, including many cases of AF-with-bradycardia. The segment also benefit from longer market presence and broader physician familiarity, anchored by earlier regulatory clearances.

The dual-chamber leadless pacemakers segment is projected to grow at a CAGR of 17.6% during the forecast period.

By Indication

Rising Case of Atrial Fibrillation with Bradycardia to Propel the Segment Growth

By indication, the market is classified into atrial fibrillation with bradycardia, sinus node dysfunction, atrioventricular (AV) block, and others.

Atrial fibrillation with bradycardia holds a major share as many AF (atrial fibrillation) patients require ventricular rate support without needing atrial pacing, making them a natural fit for single-chamber leadless therapy. The underlying epidemiology is large and expanding. Clinically, leadless devices can be attractive in AF patients with higher infection risk or limited venous access, where avoiding a pocket and lead system is meaningful. As health systems push earlier diagnosis and integrated AF management, a steady pipeline of bradycardia-associated cases supports procedure growth. Moreover, the segment is projected to hold an 40.7% share in 2026.

The sinus node dysfunction segment is estimated to grow at a CAGR of 10.7% during the forecast period.

By End-user

Growing Need for Advanced Cardiac Teams Boost the Hospitals & ASCs Segment Growth

On the basis of end-user, the market is classified into hospitals and ASCs, specialty clinics, and others.

Hospitals and ASCs account for the majority of market share as these implants require sterile cath/EP lab environments, imaging guidance, and access to advanced cardiac teams who can manage peri-procedural complications. Furthermore, the segment is set to hold a 87.0% share by 2026.

The specialty clinics segment is projected to grow at a CAGR of 14.8% during the forecast period.

Leadless Pacemakers Market Regional Outlook

Based on geography, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America held the largest market share in 2024, at USD 161.7 million, and reached USD 181.1 million in 2025. Growth in the region is supported by a large, steadily expanding pool of pacing candidates driven by population aging, high diagnosis rates for bradyarrhythmias, and strong electrophysiology (EP) infrastructure. Hospitals and ASCs in the U.S. and Canada typically have broad access to catheter labs, experienced implanters, and follow-up services, which accelerates adoption of newer pacing approaches. The region also benefits from comparatively favorable reimbursement pathways for advanced cardiac devices, enabling faster conversion from transvenous systems to leadless options, especially for patients at higher risk of pocket- or lead-related complications.

North America Leadless Pacemakers Market Size, 2025 (USD million)

To get more information on the regional analysis of this market, Download Free sample

U.S. Leadless Pacemakers Market

In 2026, the U.S. market is forecasted to represent USD 182.8 million, capturing 38.1% of total global revenue.

Europe

Europe is expected to achieve a 8.2% growth rate in the coming years, the second-highest globally, reaching USD 130.8 million by 2026. Europe's leadless pacemakers market growth is anchored by a high prevalence of cardiovascular disease in an aging population and long-standing use of pacemaker therapy across major markets such as Germany, the U.K., France, Italy, and Spain. Adoption is propelled by the region's strong tertiary-care footprint and EP capability, particularly in Western and Northern Europe, where many hospitals have the expertise to implement newer implant techniques.

U.K. Leadless Pacemakers Market

The U.K. market is projected to reach USD 20.8 million by 2026, accounting for 4.3% of the global market revenue.

Germany Leadless Pacemakers Market

Germany's market is forecasted to reach about USD 23.4 million by 2026, representing roughly 4.9% of global revenue.

Asia Pacific

In 2026, the market in Asia Pacific is predicted to be valued at USD 111.0 million, ranking as the third-largest globally. The region is expected to be the fastest-growing region, as it combines a large patient base with improving diagnostics and expanding access to cardiac care. Rapid population aging in countries such as Japan and China, the broader detection of arrhythmias due to expanded monitoring, and increased investment in hospital infrastructure are lifting pacing procedure volumes.

Japan Leadless Pacemakers Market

Japan is projected to generate approximately USD 25.8 million in revenue by 2026, contributing nearly 5.4% to the global market.

China Leadless Pacemakers Market

China's market is forecast to reach approximately USD 31.6 million by 2026, contributing about 6.6% to global revenues.

India Leadless Pacemakers Market

India is forecasted to contribute approximately USD 11.5 million to the market by 2026, corresponding to about 2.4% of global revenues.

Latin America and Middle East & Africa

Both Latin America and the Middle East & Africa are anticipated to witness moderate leadless pacemakers market share, with Latin America expected to reach around USD 19.7 million by 2026. Growth in Latin America is driven by the gradual expansion of interventional cardiology and EP services, particularly in Brazil and Mexico, along with a rising chronic disease burden and improving diagnosis of rhythm disorders. Additionally, growth in the Middle East & Africa is primarily supported by capacity building in tertiary hospitals, especially across the GCC, and by rising cardiovascular risk factors associated with urbanization and lifestyle shifts.

GCC Leadless Pacemakers Market

By 2026, the GCC is expected to generate approximately USD 7.8 million in the market, accounting for nearly 1.6% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Robust Product Innovation to Reinforce the Market Position of Prominent Players

The competitive landscape is highly concentrated and technology-led. In 2025, the market remains a two-player commercial arena, with Medtronic's Micra platform as the long-established volume leader and Abbott's AVEIR platform expanding rapidly as it broadens its indication coverage, especially with dual-chamber leadless pacing now available in the U.S.

Moreover, other key players, such as Boston Scientific, BIOTRONIK SE & Co. KG, CAIRDAC, and Celtro GmbH, compete through ongoing technological advancements and the development of products in clinical trials.

LIST OF KEY LEADLESS PACEMAKERS MARKET COMPANIES PROFILED

- Medtronic plc (Ireland)

- Abbott (U.S.)

- Boston Scientific (U.S.)

- BIOTRONIK SE & Co. KG (Germany)

- CAIRDAC (France)

- Celtro GmbH (Germany)

KEY INDUSTRY DEVELOPMENTS

- January 2026: BIOTRONIK announced the successful first-in-human implantations of its LivIQ leadless pacemaker system. This was part of the BIO|CONCEPT.LivIQ study is a pre‑market clinical investigation designed to evaluate the system's preliminary safety and performance.

- December 2024: Abbott announced the successful completion of the world's first in-human leadless left bundle branch area pacing (LBBAP) procedures using the company's investigational AVEIR Conduction System Pacing (CSP) leadless pacemaker system, as part of a feasibility study.

- September 2024: Boston Scientific announced late-breaking data from the MODULAR ATP clinical trial investigating the pacing performance of the company's Empower leadless pacemaker. The data were delivered at the 2024 European Society of Cardiology (ESC) congress.

- June 2024: Abbott announced it has received CE Mark in Europe for the AVEIR dual chamber (DR) leadless pacemaker system, the world's first dual chamber leadless pacemaker that treats people with abnormal or slow heart rhythms.

- July 2023: Abbott announced that the U.S. Food and Drug Administration (FDA) has approved the AVEIR dual chamber (DR) leadless pacemaker system, the world's first dual chamber leadless pacing system that treats people with abnormal or slow heart rhythms.

- May 2023: Medtronic plc announced it has received U.S. Food and Drug Administration (FDA) approval of its Micra AV2 and Micra VR2, the next generation of its industry-leading miniaturized, leadless pacemakers.

REPORT COVERAGE

The report provides an in-depth analysis of all market segments, highlighting key drivers, trends, opportunities, restraints, and challenges. It also provides insights into technological advancements, key industry developments, company market share analysis, and profiles of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.6% from 2026 to 2034 |

| Unit | Value (USD Million) |

| Segmentation | By Device Type, Indication, End-user, and Region |

| By Device Type |

|

| By Indication |

|

| By End-user |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 427.7 million in 2025 and is projected to reach USD 1,000.1 million by 2034.

In 2025, North America’s market value stood at USD 181.1 million.

The market is expected to exhibit a CAGR of 9.6% during the forecast period (2026-2034).

The single-chamber leadless pacemakers segment leads the market by device type.

The key factors driving the market is the growing clinical evidence.

Medtronic plc and Abbott are some of the major players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us