Lutein Market Size, Share & Industry Analysis, By Source (Natural and Synthetic), By Form (Liquid, Powder, and Beadlet), and By Application (Food & Beverages, Dietary Supplements, Personal Care & Cosmetics, Animal Feed, and Pharmaceuticals), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

KEY MARKET INSIGHTS

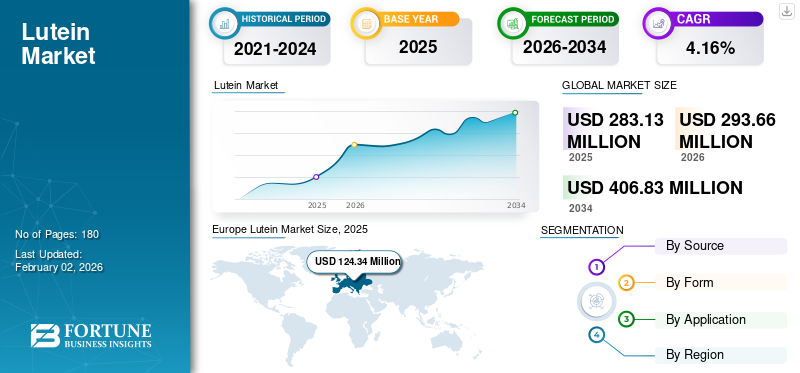

The global lutein market size was valued at USD 283.13 million in 2025. The market is projected to grow from USD 293.66 million in 2026 to USD 406.83 million by 2034, exhibiting growth at a CAGR of 4.16% during the forecast period. Europe dominated the lutein market with a market share of 43.91% in 2025.

A few key players in the market include DSM-Firmenich, Kemin Industries, Inc., Lycored, and others.

Lutein, a xanthophyll carotenoid, is a type of pigment found in microorganisms and plants. Although it is naturally present in plants, it can also be developed synthetically by chemical synthesis. Common sources of xanthophyll carotenoids include spinach, kale, corn, and egg yolks. Similarly, other carotenoids also impart natural color and several health advantages. This ingredient particularly helps in enhancing eye health and protects individuals from vision loss. Moreover, supplementing this ingredient in the diet boosts cognitive performance and minimizes the risk of liver cancer. Additionally, it assists in reducing cancers and promotes cardiovascular health. With respect to regional consumption, Europe and North America are recognized as the biggest consumers of carotenoids.

The rising use of carotenoids in the pharmaceuticals sector and the surging popularity of smart food packaging propel the growth of the global market.

Download Free sample to learn more about this report.

Lutein Market Takeaways

- 2025 Market Size: USD 283.13 million

- 2026 Market Size: USD 293.66 million

- 2034 Forecast Market Size: USD 406.83 million

- CAGR: 4.16% from 2026–2034

- Europe dominated the lutein market with a 43.91% share in 2025.

- Europe remained the largest regional market, valued at USD 124.34 million in 2025.

- Asia Pacific is projected to expand steadily, reaching USD 57.48 million in 2026.

North America

North America accounted for 29.93% of global revenue in 2025, reaching USD 84.73 million.

Europe

Europe led the global market in 2025 with USD 124.34 million in revenue and a 43.91% market share.

Asia Pacific

Asia Pacific generated USD 55.0 million in 2025 and is projected to reach USD 57.48 million in 2026.

U.S.

The country remained the key contributor to North America's lutein market growth, supported by strong demand for nutritional supplements and eye health products.

Japan

Japan continued to support Asia Pacific market expansion through growing consumer awareness of preventive healthcare and functional ingredients.

Read More

Global Lutein Industry Key Takeaways

Market Size & Forecast:

- 2025 Market Size: USD 283.13 million

- 2026 Market Size: USD 293.66 million

- 2034 Forecast Market Size: USD 406.83 million

- CAGR: 4.16% from 2026–2034

Market Share:

- Europe led the lutein market in 2025 with a 43.91% share, driven by high consumer health awareness and widespread adoption of carotenoid-enriched foods and supplements.

- By source, the synthetic segment dominated due to its cost-effectiveness, consistency, and large-scale industrial usability, whereas natural lutein is the fastest-growing segment, fueled by rising demand for naturally derived ingredients.

- By form, powder remains the most popular product form, attributed to its stability, ease of handling, and long shelf life, while liquids are expected to achieve higher growth during the forecast period due to faster absorption and rapid action.

- By application, the food & beverages sector led the market, leveraging lutein as a functional ingredient and natural colorant, whereas the personal care & cosmetics segment is projected to register the fastest growth, driven by increasing demand for organic and functional skincare products.

Key Country Highlights:

- Europe: Consumer focus on health, prevention of macular degeneration, and strong functional food industry support market growth.

- United States: Rising preference for plant-based ingredients, fortified foods, and preventive healthcare fuels lutein demand, with significant adoption in the animal feed sector.

- China & India (Asia Pacific): The region is the fastest-growing market, supported by rising chronic health issues, increased awareness of functional foods, and growing e-commerce penetration.

- South America: Market expansion is in its early stages, with growth supported by increasing lutein production and the development of functional cosmetics.

- Middle East & Africa: The market is nascent but expected to grow steadily due to rising disposable income and expanding carotenoid production.

MARKET DYNAMICS

Market Driver

Growing Awareness of Potential Benefits of Product to Fuel Market Momentum

The rising awareness of the health benefits associated with carotenoids is a key factor driving the market's potential. Most consumers are recognizing the role of carotenoids in overall health & well-being, leading to a greater demand for carotenoid-rich supplements and foods. Predominantly, this carotenoid plays a remarkable role in protecting consumers against cataracts and age related macular degeneration (AMD). Moreover, it can aid in reducing diabetic retinopathy, which is a major complication of diabetes that damages the retina’s blood vessels. This carotenoid minimizes the risk of heart ailments and enhances the function of the endothelium. Besides this, the intake of carotenoids potentially decreases the chances of neurodegenerative diseases. Thus, the companies are responding to this awareness by introducing new carotenoid-enriched products.

Market Restraints

Price Fluctuations in Raw Ingredients and Regulatory Hurdles Inhibit Market's Growth

One critical difficulty experienced by carotenoid producers is price variations in raw materials. Lutein is mainly sourced from marigold flowers, and their production is vulnerable to pests, climatic changes, and an imbalance in seasonal supply and demand. These uncertainties can directly affect the raw material availability and prices of carotenoids. Such price fluctuations fuel the overall cost of carotenoid production and extraction, complicating price forecasting and minimizing producers’ margins. As a result, the aforementioned factors hamper the industry's growth.

Regulatory hurdles are another major challenge in the global market. Stringent regulations can often restrict health claims that can be made about lutein supplements, leading to compliance issues for producers. Moreover, variations in regional differences in approved claims and inconsistencies in labeling requirements further impede the global market expansion.

Market Opportunity

Improved Usage of Carotenoids in Active Packaging Unlock Growth Possibilities

The increased use of carotenoids in active packaging creates various growth opportunities in the market. Active packaging primarily encompasses components that interact with the environment and food to improve product quality. Carotenoids, when used in packaging materials, act as antioxidants and neutralize reactive oxygen species that lead to food spoilage. Moreover, incorporating carotenoids in packaging slows down the oxidation process and lengthens the shelf life of the finished item. This delay in oxidation preserves the nutritional value, color, and freshness of end products. Additionally, the carotenoids can be utilized in colorimetric active packaging, where the carotenoid's color depicts the food's freshness and quality.

Lutein Market Trend

Rising Inclination Toward Functional Cosmetics is the Current Industry Trend

Functional cosmetics are emerging as a notable trend in the personal care & cosmetics industry, driven by consumer demand for holistic and natural solutions. Lutein, a natural carotenoid, aligns perfectly with this trend. This ingredient is known for its antioxidant properties, which aids in skin smoothness, elasticity, and hydration. Moreover, carotenoids offer anti-aging advantages and protect the skin against UV light. Additionally, the usage of carotenoids brightens the skin and minimizes oxidative stress. Besides this, carotenoids can filter blue light, emitted from electronic devices, and reduce the chances of premature aging. Recognizing these multifaceted benefits, cosmetic companies are developing carotenoid-enriched product formulations, targeting consumers seeking advanced, naturally derived skincare solutions.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Source

Synthetic Segment Dominated the Market Owing to Its Affordability

On the basis of source, the market is divided into synthetic and natural. The synthetic segment held the dominant lutein market share in 2025. Synthetic carotenoids are preferred in many applications due to their consistency and purity. Moreover, these ingredients are economical compared to natural procurement and can be utilized for large-scale industrial applications. Additionally, synthetic production methods help reduce the risk of contamination associated with environmental factors in natural sourcing, contributing to the segment's growth.

The natural segment emerged as the fastest-growing and is anticipated to maintain this growth trajectory in the near term. The rising trend of naturally sourced ingredients and increasing availability is fueling the segment's potential.

By Form

Powder is the Leading Product Form Due to Its Easy Handling

Based on form, the market is segmented into powder, liquid, and beadlet. The powder segment dominated the global market. Compared to other forms, powders possess a prolonged shelf life and are less susceptible to microbial contamination. Moreover, these ingredients can be easily transported, handled, and mixed into food & beverages, animal feed, and cosmetic formulations. Additionally, powders are more stable in nature compared to liquids and beadlets. Thus, these advantages facilitate the usage of powdered carotenoids.

The liquid category is likely to hold the highest CAGR during the forecast period. Liquid carotenoids offer rapid action and have a faster absorption rate compared to other forms. Similarly, powders, liquid ingredients are also stable in nature, driving their utilization rate.

By Application

Food & Beverages Segment Led due to Rising Usage of Lutein

Based on application, the market is distributed into food & beverages, dietary supplements, personal care & cosmetics, animal feed, and pharmaceuticals. The food & beverages sector led the global industry in 2024. Lutein is widely utilized as a functional ingredient in the food and beverage sector due to its various health advantages. Moreover, it is used as a natural food colorant in the processed food industry, which makes it a desirable natural substitute for artificial colorants. Additionally, it is used in food fortification, where it can be added to yoghurts such as baked snacks to help fulfill individual nutrient requirements.

The personal care & cosmetics segment is the fastest-growing and is predicted to expand at the highest pace in the coming years. The surging beauty from within trend and growing demand for organic cosmetics are key factors propelling the segment's growth.

Lutein Market Regional Outlook

Based on region, the market is segmented into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Europe

Europe Lutein Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Europe maintained a strong presence in the global market, reaching USD 124.34 million in 2025, accounting for 43.91% share, and is expected to reach USD 128.78 million in 2026. Europe led the global market in 2026 and consumers in the region are concerned about their health and seek products that promote overall well-being. This growing awareness fuels the usage of natural ingredients, including carotenoids, in the food sector. Moreover, the increasing prevalence of macular degeneration (AMD) is another factor promoting the use of lutein. The region also benefits from a robust functional food industry that leverages carotenoids to enhance the nutritional value of various food items. Besides this, the rising clean-label trend and increasing incorporation in dietary supplements bolster the region's potential. Thus, the above-mentioned advantages stimulate the sales of carotenoid-rich end products.

North America

North America secured the second position in the market, holding a significant share, driven by a rising preference for plant-based ingredients and surging demand for fortified foods. In today's hectic schedule, more than half of the American population relies on packaged food items to avoid the hassle of cooking. To maintain a healthy lifestyle, consumers are seeking carotenoid-fortified packaged food that provides health advantages, along with convenience. Moreover, the adoption of advanced technology for carotenoid extraction adds to the lutein market growth. Additionally, the surging emphasis on preventive healthcare further drives the consumption of carotenoids. The North America region captured 29.93% of the global market in 2025, generating USD 84.73 million in revenue, and is projected to reach USD 87.58 million in 2026.

The U.S. is the leading consumer of lutein in North America. The surging health consciousness and improved use of carotenoids in the animal feed sector boost market growth.

Asia Pacific

Asia Pacific is the fastest-growing segment and is predicted to gain momentum in the upcoming years. The growth is backed by the improving adoption of functional food ingredients and the expanding development of the e-commerce sector. Compared to other regions, Asia Pacific has a higher prevalence of chronic ailments affecting millions of individuals. In order to curb these health challenges, consumers in the region are seeking safer options that can provide health advantages without adverse side effects. This situation drives the utilization rate of carotenoids in the market. Moreover, the increasing aging population in China and India further boosts the demand for carotenoids. In 2025, Asia Pacific generated USD 55 million, contributing 19.43% to global market revenue, and is projected to grow to USD 57.48 million in 2026.

South America

South America is in its nascent stage and is expected to witness significant growth in the future. The increasing lutein production and the expanding functional cosmetics sector are boosting the market's potential.

Middle East & Africa

The Middle East & Africa are also at a nascent stage of development and are predicted to maintain steady growth in the near term, driven by surging disposable income and growing carotenoid players. Middle East & Africa recorded a market size of USD 4.63 million in 2025, capturing 1.64% of the global market share, and is projected to reach USD 4.81 million in 2026.

Latin America

The Latin America market generated USD 14.43 million in 2025, representing 5.10% of the global market landscape, and is expected to reach USD 15.01 million in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Players Focus on New Product Launches to Strengthen their Market Position

The key players in the market include Kemin Industries, Inc., Lycored, and DSM-Firmenich. These companies are focusing on launching new products that provide several health benefits. Such strategic product launches help them attract greater consumer interest and improve their position in the market.

List of Key Lutein Companies Profiled

- Kemin Industries, Inc. (U.S.)

- Lycored (U.S.)

- Vidya Pvt. Ltd. (India)

- Allied Biotech Corporation (Taiwan)

- DSM-Firmenich (Switzerland)

- Divi's Nutraceuticals (U.S.)

- OmniActive Health Technologies (U.S.)

- Fenchem (China)

- Xi'an Healthful Biotechnology Co., Ltd (China)

- ZMC (China)

KEY INDUSTRY DEVELOPMENTS

- July 2025: Vytanutra, a health & wellness company in the U.S., launched LiqLutein, a cutting-edge supplement designed to promote visual wellness. The supplement comprises a 10:2 ratio of zeaxanthin to lutein and is fortified with Vitamin A, zinc, and flaxseed oil.

- July 2025: The Korean Advanced Institute of Science and Technology (KAIST) announced the news of developing a high-yield and safe microbial strain for efficient production of lutein as compared to traditional methods.

- June 2025: OmniActive Health Technologies, a U.S.-based specialty botanical ingredients producer, announced that the U.S. Food and Drug Administration, a government agency, acknowledged its lutein "Lutemax Free" for its utilization in infant formula. This component is manufactured from marigold flowers, grown from non-GMO seeds.

- April 2025: Focus Vitamins, a nutraceutical firm in the U.S., introduced "Focus Lutein," an eye health supplement developed to defend against age-related visual decline and support long-term vision. The supplement features meso-zeaxanthin, zeaxanthin, and others and is widely available across the U.S.

- October 2023: OmniActive, an ingredients distributor in the U.S., unveiled a campaign, "Lutein for Every Age," to enhance the awareness of macular carotenoids in children's brain and eye health. This initiative highlighted zeaxanthin's and other carotenoids’ potential in brain and eye health.

REPORT COVERAGE

The market research report includes quantitative and qualitative insights into the market. It also offers a detailed market analysis of the market sizing and growth rate for all possible market segments. Key insights in the market report include an overview of related markets, a competitive landscape, recent industry developments such as mergers & acquisitions, the regulatory environment in critical countries, and current market trends.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Million) |

|

Growth Rate |

CAGR of 4.16% from 2026 to 2034 |

|

Segmentation |

By Source

|

|

By Form

|

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 283.13 million in 2025.

The market is expected to grow at a CAGR of 4.16% during the forecast period.

By source, the synthetic segment led the market.

Growing awareness of the potential benefits of lutein is a key factor driving the market's momentum.

Lycored, DSM-Firmenich, and Kemin Industries, Inc., are a few of the top players in the market.

Europe dominated the lutein market with a market share of 43.91% in 2025.

Improved usage of carotenoids in active packaging unlocks growth possibilities.

- 2021-2034

- 2025

- 2021-2024

- 180

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us