Single Cell Analysis Market Size, Share & Industry Analysis, By Offering (Products { Instruments, and Consumables [Kits, and Reagents]}, and Services), By Technique (Flow Cytometry, Next Generation Sequencing (NGS), PCR, and Others), By Cell Type (Human Cells, Animal Cells, and Microbial Cells), By Application (Therapeutic, Diagnostic, and Others), By End User (Pharmaceutical & Biotechnology Companies, Academic & Research Institutes, Diagnostic Laboratories, and Others), and Regional Forecast, 2026-2034

Single Cell Analysis Market Size and Future Outlook

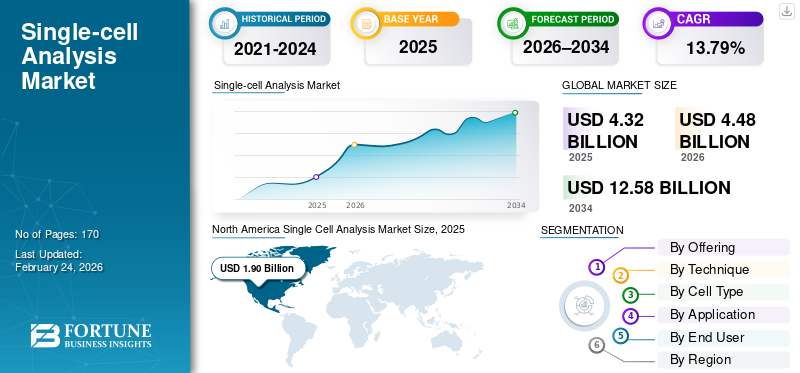

The global single cell analysis market size was valued at USD 4.32 billion in 2025. The market is projected to grow from USD 4.48 billion in 2026 to USD 12.58 billion by 2034, exhibiting a CAGR of 13.79% during the forecast period. North America dominated the single cell analysis market with a market share of 43.98% in 2025.

The single cell analysis market is anticipated to witness accelerating growth due to the increasing prevalence of cancer, expanding pipelines for precision medicine that extensively utilize single cell analysis, technological advancements with greater sensitivity, and new product launches, collectively driving market growth.

Emphasizing these key drivers, many companies are investing in the market and launching innovative products to scale their operations and strengthen their market position.

- For instance, in October 2024, Parse Biosciences launched the Parse GigaLab to scale single-cell sequencing to billions of cells per year. The GigaLab leveraged the company’s Evercode single cell technology, with a scaled-up workflow and expanded automation. Such developments are anticipated to boost the overall market growth.

Furthermore, leading players in the single-cell analysis industry, such as Thermo Fisher Scientific Inc., 10x Genomics, BD, and Parse Biosciences, are directing their resources toward research and development, expanding their offerings, and strengthening their market positions.

Download Free sample to learn more about this report.

Single Cell Analysis Market Key Takeaways

- 2025 Market Size: USD 4.32 billion

- 2026 Market Size: USD 4.48 billion

- 2034 Forecast Market Size: USD 12.58 billion

- CAGR: 13.79% from 2026-2034

- North America dominated the single cell analysis market with a 43.98% share in 2025.

- The services segment is projected to grow at a CAGR of 18.56% during the forecast period.

- The flow cytometry segment is projected to grow at a CAGR of 12.45% during the forecast period.

North America

North America maintained its leading position with a market value of USD 1.90 billion in 2025.

Europe

Europe is projected to reach USD 0.92 billion in 2026, supported by steady market expansion.

Asia Pacific

Asia Pacific is estimated to reach USD 1.33 billion in 2026, securing its position as the third-largest regional market.

U.S.

The market is estimated to reach USD 1.78 billion in 2026, accounting for approximately 39.66% of the global market.

Japan

The market is estimated at USD 0.32 billion in 2026, representing around 7.22% of the global market.

Read More

SINGLE CELL ANALYSIS MARKET TRENDS

Shift Toward AI-integrated Multiomics is a Significant Market Trend Observed

A prominent emerging global trend in single cell analysis is the shift toward AI-integrated multiomics. Comprehensive studies of single cells provide researchers with a more precise and complete overview, reducing the risk. Multiomics, when combined with automation, enables easier workflows and improves reproducibility across sites. Automated, integrated clinical runs also minimize hands-on time and shorten the path from tissue to interpretable data, enhancing lab productivity and utilization of high-value instruments.

As demand for platforms that deliver multi-layer data without complex manual integration steps rises, the market is anticipated to grow.

- For instance, in August 2025, 10x Genomics, Inc. launched the Xenium Protein platform, which enables simultaneous RNA and protein detection in the same cell and on the same tissue section, all in a single automated run. Such developments are expected to boost market growth.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Oncology and Immunology Research Needs Fuels Market Growth

Rising oncology and immunology research are among the major factors driving the global single cell analysis market growth. The market offers distinct insights into disease progression. When researchers can separate cells one by one, they can observe cellular heterogeneity, which helps explain relapse and treatment failure in some cases. The approach also helps map immune cell types and activation states, enhancing understanding of immunotherapies. This creates demand for platforms that can profile large numbers of cells quickly and repeatedly, supporting stronger biomarker discovery and better patient stratification. The result is higher spending on single-cell instruments, assays, and analysis workflows across pharmaceutical and biotechnology companies and research centers.

Underscoring the varied applications, key players are focusing on strategic collaborations to strengthen their market positions.

- For instance, in January 2026, 10x Genomics, Inc. collaborated with the Cancer Research Institute (CRI) to advance the frontiers of immuno-oncology through high resolution molecular data and AI. Such developments are expected to drive market growth.

MARKET RESTRAINTS

High Cost of Single-Cell Analysis Per Study to Restrict Market Growth

High total cost per single-cell study acts as a major factor restraining market growth. The high cost of these single-cell analysis workflows can be attributed to high-value consumables, sequencing depth, and the compute/storage required for large datasets. Even when an instrument is already installed, the ongoing per-sample cost can reduce run frequency, slowing consumables pull-through and delaying broader adoption. As a result, demand concentrates in well-funded centers of excellence and larger pharma, while smaller labs rely more on shared cores or outsourcing. This factor adversely affects the market by slowing overall market adoption.

- For instance, in September 2020, Single Cell Discoveries BV published a blog post stating that single cell RNA sequencing reagent costs are 10 to 20 times higher than those for traditional bulk RNA sequencing.

MARKET OPPORTUNITIES

Expansion of Cell & Gene Therapy Pipelines to Offer Market Growth Opportunity

The expansion of cell & gene therapy pipelines creates a strong market opportunity for single-cell analysis, driven by advanced therapies. As more CAR-T, gene-edited, and other engineered cell therapies move into clinical and commercial stages, developers must prove cell identity, purity, potency signals, and safety-relevant attributes before release. Single-cell tools help teams detect rare but critical subpopulations that can impact efficacy and adverse events. This level of resolution improves CMC decision-making, supports stronger regulatory submissions, and reduces batch failure risk by catching issues earlier. As a result, the demand for global single-cell analysis increases. Additionally, recurring use of assay kits and analysis software used across development, comparability, and manufacturing QC supports growth.

- For instance, in August 2024, Mission Bio released data from scientists at Genentech’s Analytical Development Group, showcasing the successful use of Mission Bio’s Tapestri single-cell multiomic assay for the analytical characterization and safety assessment of an ex vivo T-cell therapy platform. Such developments offer market growth opportunities.

MARKET CHALLENGES

Lack of Standardization Poses a Critical Challenge to Market Growth.

Lack of standardization is a market challenge as single-cell results can vary based on factors such as platform chemistry, capture method, sequencing depth, and QC thresholds used during analysis. When labs use different pipelines and reference controls, the same sample can produce different results, making cross-study comparisons harder and slowing decision-making. This forces teams to spend extra time on normalization, reprocessing, and validation before they can trust results for translational work or clinical hypotheses. Overall, the absence of common QC metrics and reference standards creates friction, increases total project costs, and slows the scale-up of single-cell programs.

- For instance, in June 2019, the National Institutes of Health (NIH) published an article titled ‘Current best practices in single‐cell RNA‐seq analysis: a tutorial’ that acknowledged the lack of standardization due to the relative immaturity of the field.

Segmentation Analysis

By Offering

Innovative Product Launches to Support the Leading Position and Boost Segmental Growth

Based on the offering, the market is categorized into products and services.

Among these, the product segment accounted for the largest single cell analysis market share in 2025. This growth is driven by primary physical workflow, ranging from specialized instruments to consumables and kits, generating recurring revenue. Vendors also package workflows into standardized products that reduce setup effort and improve reproducibility, which assists in scaling market growth.

Furthermore, strategic collaborations among key companies and the innovative product launch support market growth.

- For instance, in October 2024, 10x Genomics, Inc. launched two new Chromium products intended to democratize access to single-cell analysis. The GEM-X Flex and GEM-X Universal Multiplex introduced significant improvements in performance, workflow, and cost effectiveness. Such developments are expected to drive the segment's growth.

The services segment is expected to grow at a CAGR of 18.56% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Technique

Various Advantages Offered by the NGS Technique to Lead Segmental Growth

Based on the technique, the market is segmented into flow cytometry, Next-Generation Sequencing (NGS), PCR, and others.

In 2025, the Next-Generation Sequencing (NGS) segment dominated the market as it delivers high-dimensional gene expression and has varied applications in oncology and immunology. The NGS technique is also well integrated with multiomics, making it a preferred alternative for discovery and target validation. These advantages, along with innovative product launches, reinforce the leading share and support growth.

- For instance, in June 2025, Avance Biosciences launched its Next-Generation Sequencing (NGS) Center of Excellence to enhance the company's sequencing capabilities across all phases of drug development.

The flow cytometry segment is projected to grow at a CAGR of 12.45% during the forecast period.

By Cell Type

High Clinical Relevance of Human Cells to Drive the Segmental Growth

Based on cell type, the market is segmented into human cells, animal cells, and microbial cells.

By cell type, the human cells segment dominated the global market. High-value translational clinical trials that study patient tumors, immune profiling, and disease tissue mapping primarily require human cells. Funding and pharmaceutical collaborations are heavily concentrated in human biology, which further adds to the dominant share. This combination of clinical relevance and high investment makes human cells the dominant cell type. Additionally, the presence of approved products for single-cell analysis in adults reinforces the segment's dominance.

- For instance, in April 2025, 10x Genomics and Ultima Genomics partnered with Arc Institute to accelerate the development of the Arc Virtual Cell Atlas. This Virtual Cell Atlas comprises over 300 billion human cells. It offers advanced tools that make collecting single-cell data faster, more scalable, and more affordable for scientists working to improve human health.

In addition, the animal cells segment is projected to grow at a CAGR of 12.08% during the forecast period.

By Application

Increasing Therapeutic Applications to Lead Segmental Growth in Market

Based on the application, the market is segmented into therapeutic, diagnostic, and others.

In 2025, the therapeutic segment dominated the market as single-cell approaches reduce risk in drug development by identifying target cell populations, resistance mechanisms, and immune interactions that bulk methods can miss. Therapeutic teams also use single-cell to track how drugs change cell states over time, enabling better dose and patient stratification decisions. Underscoring these advantages, many key companies are also focusing on new product launches in the segment.

- For instance, in June 2025, Mission Bio launched its single-cell genotype and targeted gene expression assay, expanding the capabilities of its Tapestri Platform to become the only commercial solution that delivers simultaneous genotype and targeted gene expression profiling from over 10,000 single cells. The assay is leveraged for Phase 2 or 3 trials to home in on patients most likely to benefit from a cancer therapy, which will be unveiled at the European Hematology Association (EHA) meeting in Milan, Italy.

In addition, the diagnostic segment is projected to grow at a CAGR of 17.91% during the forecast period.

By End User

Higher Precision Provided by Single Cell Analysis in Research to Place academic & research institutes in a Leading Position.

Based on the end user, the market is segmented into pharmaceutical & biotechnology companies, academic & research institutes, diagnostic laboratories, and others.

In 2025, the academic & research institutes segment dominated the market as they are the primary end users, with universities and research institutes running a high number of exploratory studies. Academic groups also lead large-scale consortium projects and atlas-building efforts that require high-throughput and repeated runs. They frequently receive grant funding marked for omics platforms and data generation, supporting sustained usage. This volume-driven role supports the segment's growth. Underscoring these advantages, many key companies are launching innovative products based on research.

- For instance, in February 2025, Scale Biosciences announced the availability of its QuantumScale Single Cell RNA kits, a set of next-generation single-cell products that can capture and process 84,000 to 4 billion cells without specialized partitioning instrumentation. The platform offered a cost-effective single-cell solution on the market, priced per cell, sample, and experiment.

The pharmaceutical & biotechnology segment is projected to grow at a CAGR of 16.81% during the forecast period.

Single Cell Analysis Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Single Cell Analysis Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 1.89 billion and maintained its leading position in 2025 at USD 1.90 billion. The market in North America is expected to grow significantly over the forecast period, driven by new product launches, expanding genomics and proteomics pipelines, and increasing research investment in cell therapy and gene therapy in the region.

U.S. Single Cell Analysis Market

Given North America’s substantial contribution and the U.S. dominance in the region, the U.S. market can be estimated at around USD 1.78 billion in 2026, accounting for roughly 39.66% of the global market.

Europe

Europe is projected to grow at 12.10% over the coming years, the second-highest among all regions, and reach a valuation of USD 0.92 billion by 2026. The area is expected to experience robust growth driven by strong academic consortia, national health research programs, and translational hubs that increasingly rely on single-cell and spatial profiling to understand complex diseases and guide precision medicine.

U.K Single Cell Analysis Market

The U.K. market in 2026 is estimated at around USD 0.14 billion, representing roughly 3.18% of the global market.

Germany Single Cell Analysis Market

Germany’s market is projected to reach approximately USD 0.24 billion in 2026, equivalent to around 5.31% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 1.33 billion in 2026 and secure the position of the third-largest region in the market. The region’s expanding biotech base and rising oncology burden are increasing demand for deeper tumor and immune profiling to improve drug development and translational studies. Such factors are driving market growth in the region.

Japan Single Cell Analysis Market

The Japanese market in 2026 is estimated to be around USD 0.32 billion, accounting for approximately 7.22% of the global market.

China Single Cell Analysis Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.45 billion, representing approximately 10.02% of global sales.

India Single Cell Analysis Market

The Indian market in 2026 is estimated at around USD 0.11 billion, accounting for roughly 2.44% of global revenue.

Latin America and the Middle East & Africa

The Latin America and the Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.16 billion in 2026. The region is experiencing market growth driven by increased government support. In the Middle East & Africa, the GCC market is set to reach USD 0.06 billion in 2026.

South Africa Single Cell Analysis Market

The South African market is projected to reach approximately USD 0.02 billion by 2026, accounting for roughly 0.43% of the global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on New Product Launches by Key Players to Propel Market Progress

The global single cell analysis market is highly consolidated, with companies such as Thermo Fisher Scientific Inc., 10x Genomics, Parse Biosciences, and BD. Illumina, Inc. holds a significant market share. Strategic partnerships, expanding pipelines, technological advancements, and increased investments in the sector drive these companies' market share gains.

- For instance, in July 2024, Illumina, Inc. acquired Fluent BioSciences, a developer of an emerging single-cell technology. The development added new capabilities to key growth areas and advances our multiomics growth strategy. Such developments aimed to drive market growth.

Other notable players in the global market include Standard BioTools, Bruker Spatial Biology, Agilent Technologies, Inc., and Bio-Rad Laboratories, Inc. These companies are expected to prioritize technological advancements, strategic collaborations, and new product launches to strengthen their market positions.

LIST OF KEY SINGLE CELL ANALYSIS COMPANIES PROFILED

- Thermo Fisher Scientific Inc. (U.S.)

- 10x Genomics(U.S.)

- BD. (U.S.)

- Parse Biosciences (U.S.)

- Illumina, Inc. (U.S.)

- Standard BioTools (U.S.)

- Bruker Spatial Biology, Inc. (U.S.)

- Agilent Technologies, Inc. (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- Takara Bio Inc. (Japan)

KEY INDUSTRY DEVELOPMENTS

- February 2026: 10x Genomics, Inc. collaborated with PharosAI, a research consortium, to build a comprehensive multimodal cancer dataset and pair it with advanced AI models and analytical capabilities.

- November 2025: BioSkryb Genomics introduced a new single-cell analysis service called ResolveSEQ MRD, which enabled detailed classification and characterization of Measurable Residual Disease (MRD) in blood cancers.

- November 2025: QIAGEN acquired Parse Biosciences, a leading provider of instrument-free single-cell research solutions. The development expanded the company’s portfolio into the fast-growing single cell sequencing market.

- February 2025: Atrandi Biosciences, a next-generation single-cell analysis technology company, received a USD 25.0 billion investment. This investment accelerated the company’s expansion into the U.S. market, supported the growth of its Semi-Permeable Capsule (SPC) technology, and advanced new product development to enable breakthrough scientific discoveries.

- June 2024: Singleron Biotechnologies' partnership with the Human Cell Atlas (HCA) to help accelerate the adoption of single-cell sequencing globally. Singleron will facilitate access to its single-cell analysis platform via the HCA network by providing discounted rates for HCA collaborating members.

- March 2021: Beckman Coulter Life Sciences launched the next-generation CytoFLEX SRT Benchtop Cell Sorter. The development displayed new technologies to automate and simplify sort setup and stream maintenance, bringing the power of single-cell analysis to more laboratories.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 13.79% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Offering, Technique, Cell Type, Application, End User, and Region |

| By Offering |

|

| By Technique |

|

| By Cell Type |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 4.32 billion in 2025 and is projected to reach USD 12.58 billion by 2034.

In 2025, the North America market value stood at USD 1.90 billion.

The market is expected to grow at a CAGR of 13.79% over the forecast period of 2026-2034.

By offering, the products segment led the market in 2025.

Technological advancements, the rising prevalence of cancer, and an expanding pipeline of cell and gene therapy therapeutics are the key factors driving the market.

Thermo Fisher Scientific Inc., 10x Genomics, Parse Biosciences, and BD, Inc. are the major players in the global market.

North America dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 170

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us