Food Safety Testing Market Size, Share & Industry Analysis, By Test Type {Pathogen (E.Coli, Salmonella, Listeria, and Others), Genetically Modified Organism, Allergen, Mycotoxin, Chemical and Pesticides, and Others}, By Food Tested (Meat, Poultry & Seafood, Dairy Products, Processed Foods, Fruits & Vegetables, and Others), By Technology (Traditional, Rapid (Rapid PCR, Lateral Flow Immunoassay (LFIA), Rapid ELISA, Rapid Resolution Liquid Chromatography, and Others), and Molecular (PCR Test, ELISA Test, NGS, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

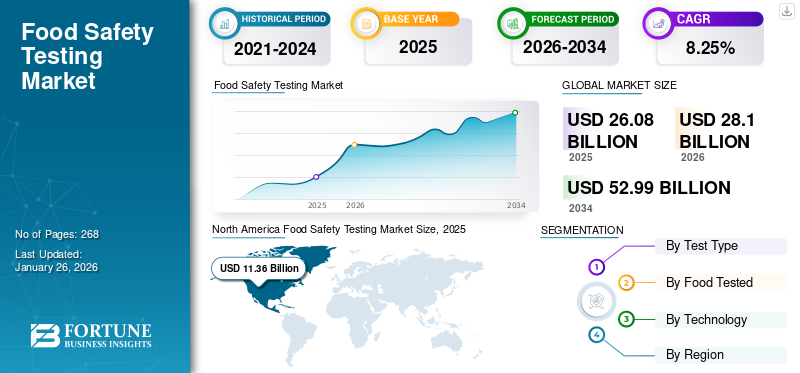

Food Safety Testing Market Size & Global Trends

The global food safety testing market size was valued at USD 26.08 billion in 2025. The market is projected to grow from USD 28.10 billion in 2026 to USD 52.99 billion by 2034, exhibiting a Compound Annual Growth Rate (CAGR) of 8.25% during the forecast period 2025-2032. North America dominated the food safety testing market with a market share of 43.57% in 2025.

Some of the key players operating in the market include SGS S.A., Eurofins Scientific SE, Bureau Veritas, Intertek Group PLC Solutions, Thermo Fisher Scientific Inc., and others.

Food safety testing is a crucial part of the supply chain to ensure that the food is safe for human consumption. It involves scientific methods to evaluate the microbiological, physical, or chemical composition of a food product, certifying that it meets safety standards. Food trade is growing among countries, either to fulfil their domestic needs due to limited agricultural outputs or to export excess food products to other countries and generate income from favorable trade activity. The growing need for imported food and beverages will create demand for more safety testing methods to support public health, driving market growth.

Download Free sample to learn more about this report.

Food Safety Testing Market Key Takeaways

- 2025 Market Size: USD 26.08 Billion

- 2026 Market Size: USD 28.10 Billion

- 2034 Forecast Market Size: USD 52.99 Billion

- CAGR: 8.25% from 2026–2034

- North America dominated the food safety testing market with a 43.57% share in 2025.

- The pathogen segment is projected to account for a 61.60% share in 2026.

- The meat, poultry & seafood segment is projected to hold a 32.24% share in 2026.

Asia Pacific

Asia Pacific generated USD 4.85 billion in 2025 and is projected to reach USD 5.25 billion in 2026.

North America

North America generated USD 11.36 billion in 2025 and is projected to reach USD 12.26 billion in 2026.

Europe

Europe accounted for USD 8.24 billion in 2025 and is expected to reach USD 8.86 billion in 2026.

U.S.

The food safety testing market is projected to reach USD 9.95 billion in 2026.

Japan

The food safety testing market is projected to reach USD 0.69 billion in 2026.

Read More

FOOD SAFETY TESTING MARKET TRENDS

Development of Innovative Portable Food Testing Equipment to Support Market Growth

There is a growing demand for advanced food safety testing technologies with higher accuracy and portability among consumers. Traditionally, the inspection of adulterated food items requires access to specialized laboratories, which turns out to be costly and time-consuming. With an aim to address these challenges, increased funding from the government and private sectors has supported technological advancements, leading to the development of the latest portable testing devices that help minimize overall testing costs. These handheld devices can examine the samples on-site, thus avoiding the need for transportation to a quality testing laboratory. Moreover, with the use of ultraviolet, infrared, or other combinations of sensors, these compact devices can easily detect adulterants, contaminants, and allergens in food items. For instance, in July 2023, Bia Analytical, a prominent leader of food authentication laboratories in the U.K., announced its partnership with trinamiX (a specialist in cutting-edge sensors) to launch a portable testing solution that will be capable of identifying cases of food fraud. The device will be integrated with the mobile app, enabling users to obtain accurate and immediate results. North America witnessed a growth from USD 9.80 Billion in 2023 to USD 10.55 Billion in 2024.

Download Free sample to learn more about this report.

Impact of Tariff War

Although the ongoing tariff war involving the U.S. may not have a direct impact on the market, it is expected to influence the production, availability, and cost of essential materials in the future. Several types of machinery and equipment essential for food safety testing are traded internationally, and their availability could be affected by supply chain disruptions caused by trade restrictions. Such disruptions can lead to an increase in testing costs, which, in turn, can increase the overall cost of final products in the market. Moreover, due to the price hike, the number of tests conducted on food products can also become limited, thereby increasing the risk of foodborne illnesses.

- The U.S. Food and Drug Administration (FDA) inspects around 1% to 2% of imported goods annually. As a result, high tariff charges on these imported goods can increase the overall cost of the products.

Market Dynamics

MARKET DRIVERS

Growing Cases of Food Fraud/Adulteration to Increase Demand for Food Safety Testing

In recent years, food safety violations and adulterations have increased significantly across the globe. The expansion and increasing complexities of the food value chain have introduced greater uncertainties in the journey of food products, from source to store shelves. As a result, customers are increasingly questioning food product labels, product authenticity, and ingredient integrity. These growing concerns regarding safety have prompted stricter national regulations globally and driven prominent players in the food processing business to demand more efficient food monitoring systems.

Increasing Incidence of Foodborne Illnesses Among People to Support Market Growth

The market is witnessing an upsurge, primarily due to the growing incidence of foodborne illnesses across the globe. Foodborne diseases are mainly associated with the consumption of contaminated food (infected with different pathogens and toxins), raising major concerns among consumers. In response, growing consumer awareness regarding food safety and quality is prompting governments to implement stricter regulatory frameworks. Moreover, the growing cases of adulteration for making a profit and the procurement of food from unsafe sources further elevate the risk of foodborne ailments, thus fueling the demand for testing procedures.

MARKET RESTRAINTS

High Equipment Costs and Limited Manpower Availability May Affect Market Growth

Some of the major factors affecting market growth are the high cost of equipment and the lack of skilled manpower to operate such advanced machines. Traditional equipment, such as Liquid Chromatography Mass Spectrometry (LCMS), Gas Chromatography Mass Spectrometry (GCMS), and others, is highly advanced and technical. This equipment requires certified engineers for their maintenance. Moreover, as most of these tools are imported, maintenance centers are confined, specifically to Tier 1 and metropolitan cities, especially in developing markets such as India. This limited availability can lead to delays in service, leading to major operational losses.

MARKET OPPORTUNITIES

Expansion in New Markets to Support Market Growth

Emerging markets, including South America, Asia Pacific, and the Middle East & Africa, are anticipated to experience high growth in the global food safety testing market in the future. However, as compared to Asia Pacific, South America, and the Middle East & Africa are still in the early stages of development. Yet significant growth is expected in these regions over the next few years. Major factors, such as growing food safety concerns and the rising government funding for building new food testing labs, encourage testing companies to expand their services.

MARKET CHALLENGES

Rising Risk of Pathogens to Challenge Market Development

With the continuous evolution of the food supply chain, the risk of emerging novel pathogens is increasing rapidly. Current food testing equipment and techniques may not be effective in identifying and detecting such pathogens, thereby increasing the risk of foodborne illness among the population. Hence, there is an urgent need to develop innovative testing techniques capable of detecting, tracking, and quantifying sources of food contamination and assessing the associated risks to consumers.

Segmentation Analysis

By Test Type

Pathogen Segment Leads Owing to Growing Incidence of Food-related Diseases

Based on test type, the market is classified into pathogen, genetically modified organism, allergen, mycotoxin, chemical and pesticides, and others.

The pathogen segment accounts for the majority of the market share. Pathogens are one of the leading causes of foodborne illnesses globally, with a expected share of 61.60% in 2026. There is a growing need to detect the presence of such organisms in food and reduce the incidence of food-related diseases. This has led to increasing investment in pathogen and microbiological testing of food products.

Among the different pathogens, Salmonella testing accounts for the largest market share. It is one of the major foodborne disease-causing organisms that cause food-related illness globally, prompting food safety agencies to test food products to ensure they are free of such microorganisms. E. coli ranks as the second most tested foodborne pathogen, followed by other microorganisms.

Genetically Modified Organisms (GMOs) testing of food products, such as cereals, fruits, and vegetables, has grown steadily in recent years. With the continuous increase in the number of GMO crop cultivations globally, several countries are increasing GMO testing to ensure food safety and regulatory compliance.

Mycotoxin testing is another critical method used to ensure that the food is safe for human consumption. It detects harmful antigens that may have carcinogenic, teratogenic, nephrotoxic, and hepatotoxic effects, which may negatively impact food safety and the health of consumers.

The chemicals and pesticides segment is projected to grow rapidly during the forecast period. The majority of agricultural products and animal farms use different chemicals and pesticides to improve farm productivity and get better crop yields. Using such products in cattle and crops can lead to the accumulation of chemical residue and negatively impact human health upon consumption. As there is a growing urgency to examine food items globally, the demand for pesticide and chemical residue testing is increasing rapidly.

Higher consumption of fruits, vegetables, and processed foods is also prompting manufacturers to label their products, indicating the presence of different allergens in food products. Hence, investment in allergen testing has grown in recent years, with the market projected to grow steadily during the forecast period.

- The allergen segment is expected to hold a 4.77% share in 2024.

Other types of testing, such as determining the presence of additives and dyes in food products, are also growing rapidly across the globe.

To know how our report can help streamline your business, Speak to Analyst

By Food Tested

Meat, Poultry & Seafood Segment to Dominate Owing to High Frequency of Testing for Pathogens

Based on food tested, the market is segmented into meat, poultry & seafood, dairy products, processed foods, fruits & vegetables, and others.

The meat, poultry & seafood segment is expected to lead the market, contributing 32.24% globally in 2026. These products are among the most frequently tested food products for pathogens, chemicals, or allergens to ensure they are safe for human consumption.

The testing of processed food products is also increasing rapidly in several countries. The segment is projected to register the second-fastest growth during the forecast period. With rising disposable incomes, changing dietary lifestyles, and increasing urbanization, the consumption of packaged foods has increased significantly in recent years. Regulatory bodies globally are placing a strong emphasis on chemical contaminant testing, microbiological safety testing, allergen testing, and other assessments to ensure compliance with labeling and packaging standards for processed and packed items.

Fruits and vegetables are another major food category experiencing increasing consumption across the world. Fruits, including nuts, are becoming popular among consumers due to their high fiber and nutrition content. These products are becoming popular among vegan and vegetarian consumers as well. As chemicals and pesticides are mainly used for improving crop yield and killing pests, the need for testing these products for chemical residues is growing. The growing demand for natural food products is prompting several countries to implement rigorous testing, supporting strong growth in the future.

Dairy products, such as cheese, milk, and butter, are widely consumed across different countries and may contain different pathogens and chemical residues. The segment is expected to register steady growth in the future as these products are regularly tested to ensure safety. Hence, stringent food safety regulations are adopted by countries to check and ensure that it is safe for consumption. Among other products, cereals, spices, and honey are regularly traded and tested to ensure that they meet the safety standards established by different countries.

By Technology

Traditional Segment Leads Market Due to Reliable Detection

Based on technology, the market is classified into traditional, rapid, and molecular.

The traditional segment is anticipated to hold a dominant market share of 43.02% in 2026. These tests are generally time-consuming and require expensive instruments to generate conclusive results. They involve the use of culture media to isolate and grow bacteria present in the food samples. Despite the time-consuming process, conventional tests offer higher accuracy than rapid tests.

Rapid testing of food products is gaining prominence in several countries as it is more economical and generates results more quickly than other traditional tests. One of the major disadvantages associated with rapid tests is their lower level of accuracy than conventional tests. Hence, food test equipment manufacturers are investing in developing newer and faster methods to test and detect abnormalities in food samples. Hence, this technology is expected to attain the fastest global food safety testing market growth.

Molecular testing technologies, a crucial type of food safety testing, are also growing in popularity and represent the second fastest-growing segment. These techniques are suitable for detecting new pathogens, and they are highly sensitive and specific to different microorganisms that can be present in food samples. Hence, several new approaches such as PCR Test, ELISA Test, NGS, and others are gaining popularity in the market.

Food Safety Testing Market Regional Outlook

The market is segmented into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Food Safety Testing Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market accounted for USD 11.36 billion in 2025, representing 43.57% of the global industry, and is expected to reach USD 12.26 billion in 2026. In North America, the U.S. imports the most seafood and poultry products. To control and regulate the quality of the seafood imported into the country, the Federal Meat Inspection Act (FMIA) mandates that all meat sold commercially must be scrutinized and approved to ensure that it is unadulterated, healthy, and properly branded. The U.S. market is projected to reach USD 9.95 billion by 2026.

The U.S. is one of the world’s leading food-importing countries, mainly due to its robust consumer demand and financial strength, which create an insatiable desire for an assorted range of international food commodities. According to the USDA data, in the year 2023, the U.S. imported agriculture commodities worth USD 195.30 billion when the country's population was 334.90 million. This marks a 36.19% increase compared to 2020, when imports stood at USD 143.40 million. To regulate and control these heavy volumes of imports, government agencies are proactively implementing measures to control the increasing incidence of foodborne pathogens.

Europe

Europe recorded a market size of USD 8.24 billion in 2025, capturing 31.61% of the global market share, and is projected to reach USD 8.86 billion in 2026. Europe is expected to grow at a stable pace during the forecast period. According to a recent report by the Centers for Disease Control (CDC) and the World Health Organization (WHO), nearly 40% of food contamination in Europe occurs within households. Chemical safety issues, including veterinary drug residues & pesticides, environmental pollutants, and mycotoxins, are prominently found in food products. Incidents of excessive pesticide residues and acute poisoning due to the use of illegal veterinary drugs have impacted the food industry significantly. In response, market players are engaged in the production and marketing of test kits and products to help food producers detect dangerous and unintended substances in food products. The UK market is projected to reach USD 1.63 billion by 2026, while the Germany market is projected to reach USD 2.22 billion by 2026.

Asia Pacific

In 2025, Asia Pacific represented USD 4.85 billion, accounting for 18.59% of the worldwide market, and is projected to grow to USD 5.25 billion in 2026. The food industry is one of the fastest-growing industries globally, and countries such as China, India, and Japan, among the most populous in the region, have high levels of food importation and domestic production, necessitating extensive food testing. Some of the most notable government bodies governing food safety are FSSAI in India, the Ministry of Health, Labor, and Welfare in Japan, and the State Council in China. Manufacturers increasingly recognize that consumers demand accreditation before purchasing their products. Hence, they are trying to achieve different certifications to align with shifting consumer purchasing behavior. The Japan market is projected to reach USD 0.69 billion by 2026, the China market is projected to reach USD 2.04 billion by 2026, and the India market is projected to reach USD 0.62 billion by 2026.

- In April 2025, the Government of India announced plans to establish 100 food testing labs across the country to ensure high food quality. These labs will carry out regular surveillance, inspection, and monitoring of food samples to ensure food safety.

South America

The market in South America is still in the early stages of growth, however, the need for a robust food testing infrastructure is expected to rise significantly in the future. In response to the urgent need for food safety and security, many organizations are working on improving the network of food safety labs in the region. Countries are also engaging in regional partnerships to improve food safety standards and ensure food security collaboratively.

Middle East & Africa

Middle East & Africa contributed 2.09% to the global market in 2025, with a valuation of USD 0.55 billion, and is projected to reach USD 0.58 billion in 2026. Food safety testing has become increasingly important in the region. A region often challenged by poor healthcare facilities and vulnerable to the rapid spread of diseases. However, the food safety and security systems in most African countries are usually weak and fragmented, making them ineffective in protecting the health of consumers and improving the competitiveness among food manufacturers. Active execution of food regulation and the enactment of foodborne illness observation systems require rigorous and competent food analysis proficiency at national and regional levels.

Latin America

The Latin America market was valued at USD 1.08 billion in 2025, capturing 4.14% of global revenue, and is estimated to reach USD 1.15 billion in 2026.

Competitive Landscape

Key Market Players

Key Players Focus on Acquisitions to Expand Their Market Reach

This market exhibits a moderately consolidated structure with a mix of large established players and smaller regional companies. The market is expected to witness further consolidation as major players increasingly engage in acquisitions of smaller companies to expand their market reach. Companies such as SGS S.A., Eurofins Scientific S.E., Bureau Veritas, Intertek Group, and ALS Ltd. are focusing on mergers and acquisitions and establishing new laboratories to increase their footprint in the global marketplace.

Major Players in the Food Safety Testing Market

|

Rank |

Company Name |

|

1 |

SGS S.A. |

|

2 |

Eurofins Scientific SE |

|

3 |

Bureau Veritas |

|

4 |

Intertek Group PLC Solutions |

|

5 |

Thermo Fisher Scientific Inc. |

SGS S.A., Eurofins Scientific SE, Bureau Veritas, Intertek Group PLC Solutions, and Thermo Fisher Scientific Inc. are the largest players in the market. The global food safety testing market is semi-consolidated, with the top 5 players accounting for around significant portion of the market.

LIST OF KEY FOOD SAFETY TESTING COMPANIES PROFILED

- ALS Limited (Australia)

- AsureQuality Ltd (New Zealand)

- Bio-Rad Laboratories, Inc. (U.S.)

- Bureau Veritas (France)

- Deibel Laboratories (U.S.)

- Eurofins Scientific SE (Luxembourg)

- Intertek Group PLC Solutions (U.K.)

- Mérieux NutriSciences (U.S.)

- SGS S.A. (Switzerland)

- Thermo Fisher Scientific Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2025: QIAGEN launched an innovative instrument named QIAsymphony Connect that can be used to prepare samples and expand its reach to consumers. The product can be used for oncology and genomics

- March 2025: Test kit manufacturing company Gold Standard Diagnostics Horsham, launched the new ABRAXIS Dicamba ELISA Plate Test Kit in the market. It can be used to assess water, durum wheat, and soil samples and quantify the antibodies present in them.

- September 2024: AREX Biosciences launched a new ELISA series, developed to measure pathogen proteins and provide effective sample assessment.

- June 2024: ArcticZymes Technologies launched a new ELISA test kit named SAN HQ 2.0 ELISA kit. This test kit is designed to detect and quantify SAN HQ 2.0 enzyme in samples.

- February 2024: BioMérieux, a leading manufacturer of in vitro diagnostics, entered into a strategic collaboration with the Center for Food Safety and Applied Nutrition (CFSAN), U.S. Food and Drug Administration (FDA), and others to develop innovative tools to identify and combat foodborne pathogens.

REPORT COVERAGE

The report includes quantitative and qualitative insights into the market. It also offers a detailed regional analysis of the market share, market statistics, regional forecast, and growth rate for all possible market segments. This market analysis report provides various key insights into the market, food safety testing industry, an overview of related markets, the competitive landscape, recent industry developments, such as mergers & acquisitions, the regulatory scenario in critical countries, and key industry trends.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.25% from 2026 to 2034 |

|

Segemntation |

By Test Type, Food Tested, Technology, and Region |

|

Unit |

Value (USD Billion) |

| Segmentation: |

By Test Type

By Food Tested

By Technology

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the market size was valued at USD 26.08 billion in 2025.

Recording a CAGR of 8.25%, the market is expected to exhibit promising growth during the forecast period of 2026-2034.

By test type, the pathogen segment leads the market.

The increasing incidence of foodborne illnesses is a key factor driving market growth.

SGS S.A., Eurofins Scientific SE, and Bureau Veritas are a few of the leading players in the market.

Asia Pacific is expected to register the highest CAGR during the forecast period.

Development of innovative portable food testing equipment to support market growth.

- 2021-2034

- 2025

- 2021-2024

- 268

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us