Meat Processing Equipment Market Size, Share & Industry Analysis, By Equipment Type (Cutting & Slicing Equipment, Grinding & Mixing Equipment, Massaging & Tumbling Equipment, Tenderizing Equipment, Filling & Stuffing Equipment, Smoking & Cooking Equipment, Dicing & Portioning Equipment and Other Processing Equipment), By Automation Level (Manual, Semi-Automated, and Fully Automated) By Meat Type (Pork, Beef & Veal, Poultry, Mutton / Lamb, and Others), and Regional Forecast, 2026-2034

Meat Processing Equipment Market Size and Future Outlook

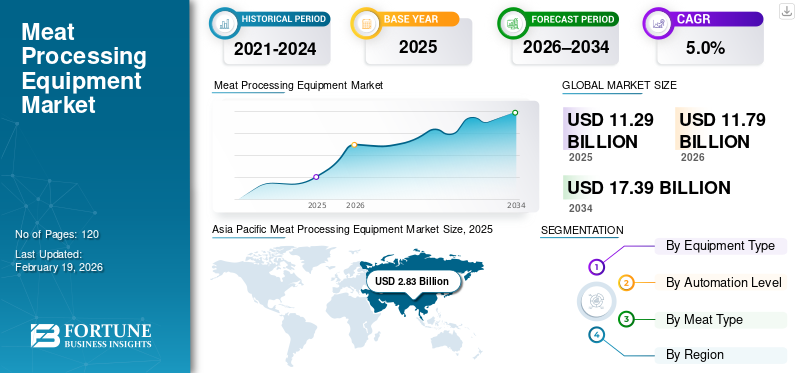

The global meat processing equipment market size was valued at USD 11.29 billion in 2025. The market is projected to grow from USD 11.79 billion in 2026 to USD 17.39 billion by 2034, exhibiting a CAGR of 5.0% during the forecast period. Asia Pacific dominated the meat processing equipment market with a market share of 25.07% in 2025.

Meat processing equipment refers to industrial machinery used for slaughtering, cutting, deboning, grinding, mixing, portioning, filling, cooking and further processing of meat to ensure efficiency, hygiene, and product consistency.

Meat processing equipment is witnessing steady and structurally driven growth as the market for expands and processors across poultry, pork, and red meat invest in automation-led capacity expansion, yield optimization and compliance-driven modernization. Rising labor shortages, shifting consumer preferences and evolving consumer demands for processed meat and value-added, ready-to-cook products are accelerating replacement of manual and semi-automated machinery with integrated, high-throughput lines. In parallel, tighter hygiene and food safety requirements and the need for resilient supply chain operations are strengthening investment across the processing equipment industry.

- For instance, during IFFA 2025, several leading manufacturers including JBT Marel and GEA Group introduced next-generation meat processing solutions focused on higher automation, vision-guided cutting, and end-to-end line integration, reflecting industry demand for scalable and data-enabled processing infrastructure.

JBT Marel, GEA Group, Middleby (Food Processing Equipment Group), BAADER, and Handtmann are among the key players holding a significant share of the market. Their competitive positioning is supported by broad portfolios spanning primary processing, cutting and deboning, grinding and mixing, forming and filling, and cooking and smoking equipment, along with the ability to deliver turnkey processing lines.

Download Free sample to learn more about this report.

MEAT PROCESSING EQUIPMENT MARKET TRENDS

Migration from Monolithic Control Architectures to Modular, Software-Defined Controller Platforms is Emerging Market Trend

Meat processors are shifting from standalone machines to integrated, automated processing lines to address aging equipment, labor shortages and stricter food safety requirements. To enable gradual modernization, manufacturers are offering modular, retrofit-ready systems with hygienic, automation-ready designs, allowing brownfield plants to upgrade incrementally while improving throughput, yield, and operational efficiency without major production disruptions.

- For instance, in April 2025, Handtmann Group announced enhancements to its filling and portioning systems portfolio, emphasizing modular machine design, higher automation compatibility, and improved integration with upstream grinding and downstream cooking processes to support flexible, line-level upgrades in meat processing plants.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

OEM Portfolio Expansion Enabling End-to-End Meat Processing Solutions Drives Market Growth

Strategic portfolio expansion by leading equipment manufacturers is driving meat processing equipment market growth. Meat processors increasingly favor suppliers capable of delivering end-to-end solutions spanning chilling, cutting, portioning and further processing, reducing system integration complexity and improving operational efficiency. This shift is encouraging OEMs to strengthen downstream and complementary process capabilities through acquisitions, supporting investments in both greenfield facilities and phased upgrades at existing plants.

- For instance, in August 2025, Middleby Corporation acquired Frigomeccanica S.p.A., expanding its capabilities in industrial chilling and cooling systems and strengthening its integrated offering for meat and protein processors seeking higher efficiency and tighter process control.

MARKET RESTRAINTS

Biological Variability and Yield Risk Limiting Standardization of Advanced Processing Equipment is a Key Market Restraint

Unlike most industrial manufacturing, meat processing is constrained by biological variability in raw material size, texture, fat content, and bone structure, which limits the effectiveness of standardized, high-speed automated equipment. Variations in livestock genetics, feeding practices, and regional slaughter standards often require frequent equipment recalibration or manual intervention, reducing achievable automation levels and yield consistency. For processors operating with variable raw material quality, the risk of yield loss or product damage can delay adoption of advanced cutting, deboning, and portioning systems, particularly where return on investment is highly sensitive to yield performance.

MARKET OPPORTUNITIES

Industrialization of Small and Regional Meat Processors Unlocking New Equipment Demand

A growing opportunity for the market lies in the industrialization of small and regional processors, particularly in poultry, processed meat, and fresh-cut segments. Regulatory tightening around food safety, traceability, and hygiene standards is pushing smaller processors to upgrade from manual or semi-manual operations to basic industrial processing equipment, including compact cutting, grinding, filling, and cooking systems. This shift is creating demand for cost-optimized, modular, and space-efficient equipment that can deliver compliance and throughput improvements without the scale or complexity of large industrial lines, especially in emerging markets and decentralized processing hubs.

- For instance, in June 2024, BAADER Group highlighted the introduction of compact and modular processing solutions aimed at small and mid-sized meat processors, enabling compliance with hygiene standards while supporting gradual automation and capacity expansion in regional processing facilities.

MARKET CHALLENGES

Fragmented Regulatory and Export Certification Requirements Challenges Market Growth

Meat processing equipment manufacturers and processors face challenges arising from fragmented regulatory, religious and export certification requirements across regions and end markets. Equipment often needs to be customized to comply with varying food safety standards, animal welfare regulations, and halal or kosher processing rules, and export-market inspection protocols. This lack of harmonization increases engineering complexity, extends lead times, and limits standardization of equipment platforms. For processors serving multiple domestic and export markets, frequent equipment modifications and validation adjustments can slow deployment and raise operational risk, discouraging investment in highly specialized or single-purpose processing systems.

Segmentation Analysis

By Equipment Type

Cutting & Slicing Equipment Dominates as Yield Control Support Meat Processing Lines

The market, based on equipment type, is segmented into cutting & slicing equipment, grinding & mixing equipment, massaging & tumbling equipment, tenderizing equipment, filling & stuffing equipment, smoking & cooking equipment, dicing & portioning equipment and other processing equipment.

Cutting and slicing equipment holds highest meat processing equipment market share as it forms the operational backbone of meat processing plants and it directly determines yield recovery, trim efficiency, and portion consistency across poultry, pork, and red meat applications. These systems are often the first major processing step where value optimization occurs, making them a strategic investment priority for processors. Advancements in vision-guided cutting, automated blade positioning, and real-time yield monitoring are further elevating the importance of cutting and slicing solutions, particularly in high-throughput and export-oriented facilities where even minor yield improvements translate into significant margin gains.

Distributed Control Systems (DCS) offer centralized control, high system availability, and advanced process optimization, making them well suited for large-scale, continuous industrial operations. These systems enable integrated control of complex processes, safety functions, and real-time diagnostics, which is critical in industries such as oil & gas, chemicals, power generation, and water & wastewater treatment. Programmable Logic Controllers (PLC) continue to see widespread adoption owing to their flexibility, reliability, and suitability for discrete manufacturing environments. PLCs enable fast, deterministic control of machinery and production lines and are extensively used in automotive manufacturing, packaging, food & beverage processing, and material handling.

- For instance, in February 2024, Provisur Technologies highlighted yield-optimization–focused slicing and further processing solutions at Anuga FoodTec 2024, underscoring processor demand for precision-driven cutting technologies.

Filling, stuffing, and portioning equipment is becoming increasingly critical as meat processors expand production of processed, portion-controlled, and convenience-oriented meat products. These systems enable consistent product shaping, accurate weight control, and standardized output, supporting both retail and foodservice requirements. Integration with upstream grinding and mixing and downstream thermal processing is further increasing their strategic relevance, as processors seek to streamline workflows, reduce manual handling, and enhance line-level efficiency.

To know how our report can help streamline your business, Speak to Analyst

By Automation Level

Fully Automated Systems Dominates Due to its Extensive Adoption

Based on automation level, the meat processing equipment market is segmented into manual, semi-automated, and fully automated.

Fully automated equipment accounts for the largest share of the market, driven by its extensive adoption in large-scale poultry, pork, and red meat processing facilities. These systems enable high line speeds, consistent product quality, and improved yield while significantly reducing reliance on manual labor. Fully automated solutions are increasingly deployed across cutting and deboning, portioning, filling, and thermal processing operations, making them a cornerstone of industrial meat processing modernization.

Semi-automated equipment is expected to witness strong growth of 4.8%, particularly among mid-sized processors and facilities undergoing phased upgrades. These systems offer a balance between productivity gains and capital efficiency, allowing processors to improve consistency and hygiene while retaining some manual intervention for product handling and quality control.

By Meat Type

Poultry and Pork Processing Driving Scale, While Red Meat Supports Value and Product Diversity

Based on meat type, the market is segmented into poultry, pork, beef & veal, mutton/lamb, and others.

Poultry processing accounts for the largest market share, driven by high consumption volumes, shorter production cycles, and greater penetration of industrial-scale processing facilities. Poultry plants typically operate at higher line speeds and throughput levels, requiring extensive deployment of cutting, deboning, portioning, marination, and thermal processing equipment. The standardized size profile and processing characteristics of poultry further support higher automation adoption, reinforcing sustained investment in modern processing lines.

Pork processing also represents a major segment of the market, supported by strong consumption across Europe and Asia Pacific and widespread use of pork in processed meat products. Pork processing facilities demand a broad mix of equipment, including cutting, grinding, filling, smoking and cooking systems, particularly for sausages, cured meats and value-added formats. The versatility of pork as a raw material drives continuous equipment upgrades to support product differentiation, formulation control and portion consistency.

Beef & veal processing, contributes significantly to market value due to higher equipment complexity and yield sensitivity. Beef processing requires robust cutting, deboning, and tenderizing solutions capable of handling variability in carcass size and texture. Investments in beef processing equipment are often focused on yield optimization, portion accuracy, and premium product quality, particularly in export-oriented and branded meat operations. Mutton/lamb and other meat types characterized by regional consumption patterns and selective industrialization. Equipment demand in these categories is driven by niche processing requirements and regional export markets, with processors favoring flexible and adaptable machinery to accommodate diverse carcass characteristics and lower processing volumes.

Meat Processing Equipment Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America

Asia Pacific Meat Processing Equipment Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market accounted for over USD 2.95 billion revenue in 2025, supported by a highly industrialized meat sector and strong demand for poultry, beef, and pork. Large, vertically integrated processors and high per-capita meat consumption sustain investments in cutting, deboning, portioning, and further processing equipment. Labor shortages, strict food safety regulations, and retailer quality standards are accelerating automation upgrades. Ongoing plant modernization, growth in value-added meat products, and investments in cold-chain and export facilities continue to drive steady equipment demand across the U.S., Canada and Mexico.

U.S. Meat Processing Equipment Market

U.S. to dominate the North American market with an estimated revenue of about USD 2.39 billion in 2026, supported by its large-scale, highly industrialized meat processing industry and strong demand across poultry, beef, and pork segments. The presence of vertically integrated processors, extensive cold-chain infrastructure, and high per-capita meat consumption drives continuous investment in cutting, deboning, portioning, grinding, and further processing equipment. The U.S. also leads in the adoption of automation, vision-guided processing, and digitally enabled production lines, particularly in high-throughput poultry and red meat facilities. Ongoing modernization of aging plants, expansion of value-added and ready-to-eat meat production, and stringent food safety and quality standards continue to reinforce demand for advanced meat processing equipment nationwide.

Europe

The European market dominates due to highly developed and regulation-driven meat processing industry, particularly across pork and processed meat segments. Strong demand from industrial meat processors, coupled with stringent food safety, animal welfare and sustainability regulations, is driving continuous investment in hygienic, energy-efficient and automation-ready equipment. Countries such as Germany, France, Italy, Spain and the Netherlands lead adoption, supported by advanced processing infrastructure and export-oriented production. Ongoing modernization of aging facilities and expansion of value-added meat processing continue to underpin steady market growth across Europe.

U.K. Meat Processing Equipment Market

The U.K. market in 2026 is estimated at around USD 0.30 billion, representing roughly 4.5% of global revenues.

Germany Meat Processing Equipment Market

Germany’s market is projected to reach approximately USD 0.81 billion in 2026, equivalent to around 3.9% of global sales.

Asia Pacific

Asia Pacific remains the fastest-growing market, generating revenue of USD 2.83 billion in 2025 globally. Market growth is driven by rapid industrialization of meat production, rising protein consumption, and increasing penetration of organized food processing. China, Japan, South Korea, and ASEAN countries are key contributors, supported by expanding poultry and pork processing capacity and growing demand for processed and convenience meat products. The region is witnessing a structural shift from manual and semi-manual operations toward industrial-scale, hygienic, and automated processing lines, particularly in China and Southeast Asia.

China Meat Processing Equipment Market

China’s market is projected to remain the dominant in the region, with 2026 revenues estimated at around USD 1.10 billion, representing roughly 9.3% of global sales.

Japan Meat Processing Equipment Market

The Japan market in 2026 is estimated at around USD 0.31 billion, accounting for roughly 2.6% of the global market.

India Meat Processing Equipment Market

The India market in 2026 is estimated at around USD 0.38 billion, accounting for roughly 3.2% of global revenues.

Middle East & Africa

The Middle East & Africa market is driven by food security initiatives, rising protein consumption, and increasing industrialization of meat processing, particularly across the GCC and North Africa. Government-backed investments in poultry and red meat self-sufficiency, along with growing demand for halal-certified and processed meat products, are supporting capacity expansion and modernization of processing facilities. The GCC benefits from high-capex, automation-intensive projects, while North Africa and Sub-Saharan Africa are witnessing gradual upgrades from manual to industrial processing, sustaining demand for cutting, grinding, filling and thermal processing equipment across the region.

GCC Meat Processing Equipment Market

The GCC market is projected to reach around USD 0.42 billion in 2026, representing roughly 3.6% of the global market.

South America

The South America market is supported by the region’s role as a major global producer and exporter of beef and poultry, particularly in Brazil and Argentina. Strong export demand, coupled with compliance requirements for international food safety and traceability standards, is driving investments in industrial-scale cutting, deboning, grinding and thermal processing equipment. While automation adoption varies across the region, large export-oriented processors are increasingly modernizing facilities to improve yield, consistency, and operational efficiency. Gradual upgrades in domestic processing infrastructure and expanding value-added meat production continue to support steady equipment demand across South America.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Integrated Processing Solutions and Automation-Ready Equipment Portfolios Leads to Increased Market Competition

The market is moderately consolidated, characterized by the presence of a limited number of global manufacturers offering broad, end-to-end processing portfolios spanning cutting and deboning, grinding and mixing, filling and portioning, and thermal processing. Leading players such as JBT Marel, GEA Group, Middleby Corporation (Food Processing Equipment Group), BAADER Group, and Handtmann hold strong positions, supported by deep application expertise, established customer relationships with large meat processors, and the ability to deliver turnkey and line-integrated solutions.

Competitive differentiation is increasingly driven by automation readiness, yield optimization, hygienic design, and digital process integration, rather than standalone machine performance. Manufacturers are focusing on developing modular equipment platforms that support phased upgrades, line-level integration, and compatibility with vision systems, robotics, and data-driven process control. This approach allows processors to modernize brownfield facilities while minimizing disruption and improving operational efficiency.

- For instance, at IFFA 2025, multiple global meat processing equipment manufacturers highlighted modular and integrated processing solutions aimed at improving yield, hygiene compliance, and line efficiency, reflecting industry-wide focus on scalable automation and end-to-end processing capabilities.

LIST OF KEY MEAT PROCESSING EQUIPMENT COMPANIES PROFILED

- JBT Marel (U.S.)

- GEA Group (Germany)

- BAADER (Germany)

- Bettcher Industries (U.S.)

- Duravant (U.S.)

- The Middleby Corporation (U.S.)

- Multivac Group (Germany)

- Handtman group (Germany)

- VEMAG Gmbh (Germany)

- RISCO S.p.A. (Italy)

KEY INDUSTRY DEVELOPMENTS

- November 2024: The Middleby Corporation completed its acquisition of all of the capital stock of Gorreri Food Processing Technology (“Gorreri”), a one of the prominent manufacturer of equipment for the baked goods industry, located near Parma, Italy.

- June 2024: Handtmann Group announced the expansion of its processing and portioning systems capabilities through investments in its Food Processing division, aimed at strengthening solutions for sausage, formed meat, and value-added protein products, supporting growing demand for integrated filling, portioning, and downstream processing

- May 2024: GEA Group highlighted continued development of its food and meat processing technologies, focusing on energy-efficient thermal processing, hygienic equipment design, and integrated solutions aligned with sustainability and food safety requirements.

- March 2024: Multiple global meat processing equipment manufacturers, including leading cutting, portioning, and thermal processing suppliers, showcased advanced processing solutions at Anuga FoodTec 2024, emphasizing yield optimization, hygienic design, and modular line integration for industrial meat processors.

- January 2024: JBT Corporation and Marel announced a definitive agreement to acquire, creating a global leader in food and meat processing equipment with an expanded portfolio spanning poultry, meat, and prepared foods, strengthening capabilities in integrated processing lines and automation-ready solutions.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.0% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Equipment Type, Automation Level, Meat Type, and Region |

|

By Equipment Type |

· Cutting & Slicing Equipment · Grinding & Mixing Equipment · Massaging & Tumbling Equipment · Tenderizing Equipment · Filling & Stuffing Equipment · Smoking & Cooking Equipment · Dicing & Portioning Equipment · Other Processing Equipment |

|

By Automation Level |

· Manual · Semi-Automated · Fully Automated |

|

By Meat Type |

· Pork · Beef & Veal · Poultry · Mutton / Lamb · Others |

|

By Region |

· North America (By Equipment Type, By End Use Industry, and Country) o U.S. (By Equipment Type) o Canada (By Equipment Type) o Mexico (By Equipment Type) · Europe (By Equipment Type, By End Use Industry, and Country/Sub-region) o Germany (By Equipment Type) o U.K. (By Equipment Type) o France (By Equipment Type) o Spain (By Equipment Type) o Italy (By Equipment Type) o BENELUX (By Equipment Type) o Nordics (By Equipment Type) o Russia (By Equipment Type) o Rest of Europe · Asia Pacific (By Equipment Type, By End Use Industry, and Country/Sub-region) o China (By Equipment Type) o Japan (By Equipment Type) o India (By Equipment Type) o South Korea (By Equipment Type) o ASEAN (By Equipment Type) o Oceania (By Equipment Type) o Rest of Asia Pacific · South America (By Equipment Type, By End Use Industry, and Country/Sub-region) o Brazil (By Equipment Type) o Argentina (By Equipment Type) o Rest of South America · Middle East & Africa (By Equipment Type, By End Use Industry, and Country/Sub-region) o GCC Countries (By Equipment Type) o South Africa (By Equipment Type) o North Africa (By Equipment Type) o Israel (By Equipment Type) o Rest of Middle East & Africa |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 11.79 billion in 2026 and is projected to reach USD 17.39 billion by 2034.

In 2025, the North America market value stood at USD 2.95 billion.

The market is expected to exhibit a CAGR of 5.0% during the forecast period of 2026-2034.

By meat type, the pork is expected to dominate the market.

Rising process complexity and automation intensity across industries driving demand for advanced meat processing equipment.

JBT Marel, GEA Group, BAADER, Bettcher Industries, Duravant, The Middleby Corporation are the major players in the global market.

Europe dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us