Medical Nutrition Products Market Size, Share & Industry Analysis, By Product (Enteral Nutrition {Oral and Tube Feeding} and Parenteral Nutrition {PPN and TPN}), By Age, By Form (Liquid and Powder), By Therapeutic Area (Cardiovascular Disorders, Diabetes, Gastrointestinal Disorders, Oncology, and Others), By Caloric Density (1.0 to 2.0 kcal/ml), By Nutrition Composition (Processed Foods & Real Food), By End-user (Homecare Settings {Homecare Companies and Pharmacies/Retail Channel}, Hospitals & ASCs, Specialty Clinics, Nursing Homes/Senior Homes, and Others), & Regional Forecast, 2026-2035

Medical Nutrition Products Market Size and Future Outlook

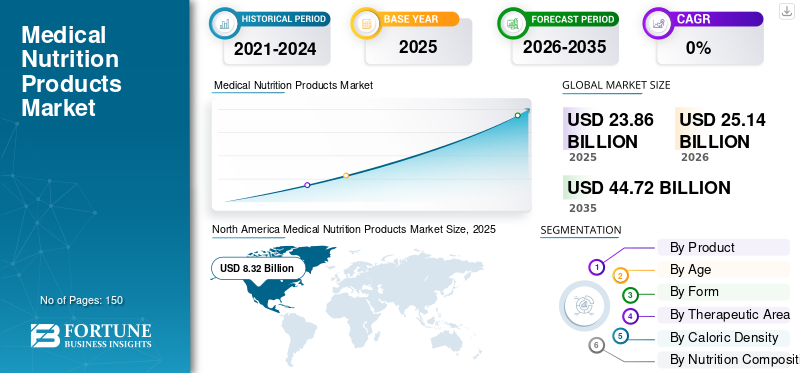

The medical nutrition products market size was valued at USD 23.86 billion in 2025. The market is projected to grow from USD 25.14 billion in 2026 to USD 44.72 billion by 2035, exhibiting a CAGR of 6.6% during the forecast period. North America dominated the medical nutrition products market with a market share of 34.87% in 2025.

Medical nutrition refers to specially formulated nutritional products designed for the dietary management of patients under medical supervision. These products are developed to address specific health conditions, including malnutrition, metabolic disorders, gastrointestinal diseases, oncology-related complications, and neurological conditions amongst others. The market growth is attributed to the increasing burden of chronic diseases, rising geriatric population, and growing awareness of evidence-based nutritional therapies. In addition, the expanding home care nutrition sector, advancements in personalized and disease-specific formulation science, and increasing integration of digital health tools are also projected influence market growth.

- For instance, in November 2023, Danone S.A. launched Fortimel in China, expanding its adult medical nutrition portfolio with a range of formulations specifically designed to address post-surgical recovery and disease-related nutritional requirements in adults.

Furthermore, many key industry players, such as Abbott Laboratories, B. Braun SE, Nestlé S.A., Danone S.A., and Baxter operating in the market, are focusing on developing various innovative technologies to offer better products with improved accuracy and efficiency.

Download Free sample to learn more about this report.

Medical Nutrition Products Market Key Takeways

- 2025 Market Size: USD 23.86 billion

- 2026 Market Size: USD 25.14 billion

- 2034 Forecast Market Size: USD 44.72 billion

- CAGR: 6.6% from 2026–2034

- North America dominated the medical nutrition products market with a 34.87% share in 2025.

- The enteral nutrition segment is expected to account for the largest market share in 2026.

- The 1.1–1.5 kcal/ml segment dominated the global market in 2025.

North America

North America remained the leading regional market, reaching an estimated value of USD 8.32 billion in 2026.

Europe

Europe is projected to grow at a CAGR of 7.1% and reach USD 7.20 billion by 2026.

Asia Pacific

Asia Pacific is expected to reach USD 5.68 billion in 2026, making it the third-largest regional market.

U.S.

U.S. The market is estimated to reach approximately USD 7.98 billion in 2026, supported by strong demand for clinical nutrition products.

Japan

Japan The market is estimated at approximately USD 0.97 billion in 2026, driven by an aging population and increasing nutritional care needs.

Read More

MEDICAL NUTRITION PRODUCTS MARKET TRENDS

Rising Adoption of Personalized and Disease-Specific Medical Nutrition Formulations is Emerging Market Trend

The market is witnessing a substantial shift toward personalized and targeted medical nutrition, with formulations being tailored to patient-specific parameters. In addition, healthcare providers are increasingly recognizing that standardized nutritional products are insufficient for patients with complex or multiple comorbidities, and are therefore driving demand for disease-specific formulas. Moreover, advances in nutrigenomics and microbiome research are enabling companies to develop next-generation products that support immune response, reduce inflammation, and enhance recovery outcomes. Also, companies are also focusing on improving palatability, tolerability, and patient compliance through innovations, further supporting this market trend.

- For instance, in November 2021, Abbott announced launch of Similac 360 Total Care with exclusive blend of five HMO prebiotics. The new system is designed for immune system and brain development.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Prevalence of Chronic Diseases and Malnutrition to Accelerate Market Growth

A major driver of this market is the increasing global prevalence of chronic diseases, including cancer, diabetes, cardiovascular disorders, renal disease, and gastrointestinal conditions, all of which significantly harm the ability of patients to meet their nutritional requirements through conventional dietary intake. Moreover, malnutrition associated with chronic illness is a well-established clinical problem that leads to poorer treatment outcomes, prolonged hospital stays, increased complication rates, and higher healthcare costs. As healthcare systems globally are placing greater emphasis on early nutritional screening and intervention, the demand for clinically validated medical nutrition products is growing. In addition, the surging geriatric population is further compounding this demand.

MARKET RESTRAINTS

High Cost of Specialized Medical Nutrition Products and Reimbursement Limitations to Deter Market Growth

High cost of specialized medical nutrition products is one of the prominent factors deterring the market growth. Disease-specific and personalized nutritional formulations, particularly those incorporating novel bioactive ingredients, immunonutrients, or advanced lipid systems, carry significantly higher price points compared to standard nutritional supplements. In addition product acquisition costs, limited reimbursement coverage for oral nutritional supplements and home enteral nutrition across several major markets, remains a persistent barrier to patient access and market penetration.

MARKET OPPORTUNITIES

Expanding Home Care Nutrition Sector and Digital Health Integration to Offer Lucrative Market Growth Opportunities

Increasing emphasis on shifting nutritional care from hospital to home settings offers lucrative opportunities for medical nutrition products market growth. As healthcare systems globally are focusing on reducing inpatient hospitalization costs and supporting longer-term disease management in community settings, the home enteral and parenteral nutrition segment is experiencing substantial growth. Moreover, home care nutrition patients require ongoing product supplies, clinical monitoring, and dietitian support, creating high-value, recurring revenue streams for medical nutrition providers. This creates opportunities for companies to develop integrated care models that combine product supply with digital monitoring platforms, telehealth dietitian consultations, and remote dose adjustment capabilities. As competition among medical nutrition companies increases, offering end-to-end home nutrition solutions that enhance patient adherence, clinical outcomes, and caregiver convenience is becoming an important strategic priority.

- For instance, in May 2021, Danone introduced its new digital platform to healthcare professionals for research & development of medical nutrition.

MARKET CHALLENGES

Ensuring Regulatory Compliance Across Diverse Global Markets to Pose a Critical Challenge to Market Growth

Managing regulatory compliance across diverse and often inconsistent global regulatory frameworks for medical nutrition products is posing a critical challenge to the market. Medical nutrition products occupy a complex regulatory space that sits between pharmaceutical drugs and conventional food products, and the classification, labeling, clinical evidence requirements, and reimbursement eligibility criteria vary significantly across markets including the U.S., European Union, Japan, China, and emerging economies. Also, companies seeking to launch disease-specific formulations or novel ingredient systems must navigate country-specific approval pathways, clinical substantiation requirements, and post-market surveillance obligations that can significantly extend time-to-market and increase compliance costs.

Medical Nutrition Products Market Segmentation Analysis

By Product

Clinical Versatility and Broad Patient Applicability of Enteral Nutrition to Drive Segment Growth

Based on the product, the market is divided into enteral nutrition and parenteral nutrition.

The enteral nutrition segment is anticipated to account for the largest medical nutrition products market share. The segment growth is attributed to the extensive use of enteral nutrition in managing a broad spectrum of clinical conditions, including critical illness, cancer, neurological disorders, and gastrointestinal diseases. In addition, enteral nutrition also offers significant clinical advantages over parenteral alternatives, including a lower risk of systemic infection, better preservation of gut mucosal integrity, improved tolerability for long-term use, and substantially lower administration costs. Besides, technological developments in enteral delivery systems is also expected to boost segment growth during the forecast period.

- For instance, in March 2025, Nutrisens Group announced the acquisition of Brazilian Prediet Medical Nutrition, which manufactures oral and enteral nutrition products across powder, liquid, and tube feeding formats.

The parenteral nutrition segment is anticipated to rise with a CAGR of 5.9% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Age

Higher Prevalence of Lifestyle-Related and Recovery-Based Nutritional Needs Among Adults to Boost Segment Growth

Based on age, the market is segmented into pediatric and adults.

In 2025, the adults segment dominated the global market. This is due to adult patients represent the largest and most diverse demographic requiring medical nutrition intervention. In addition, the wide range of product availability for adult nutrition is also projected to boost segment growth.

The pediatric segment is anticipated to rise with CAGR of 5.0% over the forecast period.

By Form

Ready-to-Use Convenience and Superior Clinical Sterility of Liquid Form to Accelerate Segment Growth

Based on form, the market is segmented into liquid and powder.

In 2025, the liquid segment dominated the global market. They offer immediate readiness for clinical use without requiring reconstitution, minimizing preparation time, reducing the risk of mixing errors, and ensuring consistent nutrient concentration in every serving. Moreover, in hospital and acute care settings where infection control and workflow efficiency are critical priorities, ready-to-use liquid formulations are the preferred format for both enteral tube feeding and oral supplementation, as they eliminate the handling and sterility risks associated with powder reconstitution.

The powder segment is anticipated to rise with CAGR of 6.0% over the forecast period.

By Therapeutic Area

High Nutritional Burden of Cancer Treatment and Disease-Specific Formulation Demand to Drive Oncology Segment Growth

Based on therapeutic area, the market is segmented into cardiovascular disorders, diabetes, gastrointestinal disorders, kidney disorders, neurological disorders, oncology, and others.

In 2025, the oncology segment dominated the global market. This is due to increasing demand for cancer and its associated treatments, including chemotherapy, radiotherapy, and surgery. In addition, oncology patients frequently require specialized nutritional support across all phases of the cancer care pathway, from pre-operative optimization and active treatment support to post-treatment recovery and palliative care, generating sustained and high-volume demand for disease-specific medical nutrition products.

- For instance, the International Agency for Research on Cancer (IARC) reported an estimated 20 million new cancer cases globally in 2022.

The gastrointestinal disorders segment is anticipated to rise with CAGR of 6.8% over the forecast period.

By Caloric Density

Broad Clinical Applicability and Tolerance Profile of Standard-Density Formulations (1.1–1.5 kcal/ml) to Support Segment Dominance

Based on caloric density, the market is segmented into 1.0 kcal/ml or below, 1.1 – 1.5 kcal/ml, 1.6 – 2.0 kcal/ml, and above 2.0 kcal/ml.

In 2025, the 1.1–1.5 kcal/ml segment dominated the global market. Standard-density formulations in this range hold the highest market share as they represent the most widely prescribed caloric concentration across the broadest range of clinical indications and patient populations. In addition, these formulations are suitable for the majority of enterally-fed patients in hospital, long-term care, and home settings. Such benefits are estimated to drive segment growth.

The above 2.0 kcal/ml segment is anticipated to rise with CAGR of 7.4% over the forecast period.

By Nutrition Composition

Established Clinical Evidence Base and Formulation Consistency of Processed Medical Nutrition to Drive Segment Growth

Based on nutrition composition, the market is segmented into processed food and real food.

In 2025, the processed food segment dominated the global market. They are manufactured under stringent pharmaceutical-grade quality standards that ensure precise, consistent nutrient concentrations, guaranteed microbiological safety, and validated shelf life. Moreover, the extensive clinical evidence base supporting processed formulations across multiple therapeutic indications, combined with their compatibility with enteral feeding systems, long shelf life, and established reimbursement frameworks in most markets, makes them the default prescribing standard for the majority of healthcare professionals globally.

The real food segment is anticipated to rise with CAGR of 8.1% over the forecast period.

By End-User

Availability of Superior Clinical Infrastructure and High Patient Volume in Hospitals & ASCs to Boost Segment Growth

Based on end-user, the market is segmented into homecare settings, hospitals & ASCs, specialty clinics, nursing homes/senior homes, and others.

In 2025, hospitals & ASCs held highest market share. They manage the largest and most clinically complex patient populations requiring medical nutrition intervention, including critically ill patients, surgical recovery cases, oncology patients, and individuals with advanced chronic disease. In addition, hospital formulary systems, nutrition support teams, and standardized enteral and parenteral nutrition protocols drive high-volume and consistent utilization of medical nutrition products across acute care settings. Furthermore, the segment is set to hold 37.8% share in 2026.

In addition, homecare settings segment is projected to grow at a CAGR of 7.3% during the study period.

Medical Nutrition Products Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Medical Nutrition Products Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valuing at USD 7.82 billion, and also maintained the leading share in 2025, with USD 8.32 billion. The market in North America is expected to increase due to aging population, higher survival rates for chronic-disease patients, and telehealth adoption.

U.S. Medical Nutrition Products Market

Based on North America’s strong contribution, the U.S. market can be analytically approximated at around USD 7.98 billion in 2026, accounting for roughly 31.7% of global sales.

Europe

Europe is projected to record a growth rate of 7.1% in the coming years, which is the second highest among all regions, and reach a valuation of USD 7.20 billion by 2026. The region is estimated to witness considerable market growth due to increasing awareness of the benefits of medical foods, and a growing patient population of chronic diseases.

U.K. Medical Nutrition Products Market

The U.K. market in 2026 is estimated at around USD 0.84 billion, representing roughly 3.4% of global revenues.

Germany Medical Nutrition Products Market

Germany’s market is projected to reach approximately USD 1.64 billion in 2026, equivalent to around 6.5% of global sales.

Asia Pacific

Asia Pacific is estimated to reach USD 5.68 billion in 2026 and secure the position of the third-largest region in the market. Aging population coupled with rising prevalence of malnutrition is expected to drive regional growth.

Japan Medical Nutrition Products Market

The Japan market in 2026 is estimated at around USD 0.97 billion, accounting for roughly 3.8% of global revenues.

China Medical Nutrition Products Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 1.78 billion, representing roughly 7.1% of global sales.

India Medical Nutrition Products Market

The India market in 2026 is estimated at around USD 0.69 billion, accounting for roughly 2.8% of global revenues.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 1.90 billion in 2026. In the Middle East & Africa, the Saudi Arabia is set to reach a value of USD 0.58 billion in 2026.

South Africa Medical Nutrition Products Market

The South Africa market is projected to reach around USD 0.23 billion in 2026, representing roughly 0.92% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Growing Number of Product Launches and Collaborations by Key Players to Boost Market Competition

The medical nutrition products market holds a semi-consolidated market structure, constituting prominent players such as Abbott Laboratories, B. Braun SE, Nestlé S.A., Danone S.A., and Baxter. The significant market share of these companies is due to numerous strategic activities, including distribution collaborations and implementation of new programs.

- For instance, in April 2026, Nestlé S.A. joined the Microbiome Therapeutics Innovation Group (MTIG) with an aim to accelerate development and expand patient access to life‑changing microbiome medicines.

Other notable players in the global market Fresenius Kabi AG, Reckitt Benckiser Group PLC, Addus HomeCare, Inc., Medtrition Inc., and Ajinomoto Co., Inc. These companies are expected to prioritize collaborations to increase their share during the forecast period.

LIST OF KEY MEDICAL NUTRITION COMPANIES PROFILED

- Abbott Laboratories (U.S.)

- Braun SE (Germany)

- Nestlé S.A. (Switzerland)

- Danone S.A. (France)

- Baxter (U.S.)

- Fresenius Kabi AG (Germany)

- Reckitt Benckiser Group PLC (U.K.)

- Addus HomeCare, Inc. (U.S.)

- Medtrition Inc. (U.S.)

- Ajinomoto Co., Inc. (Japan)

KEY INDUSTRY DEVELOPMENTS

- July 2025: Danone announced the acquisition of Kate Farms, a U.S.-based pioneer in plant-based clinical nutrition. The strategic step was taken to expand Danone's North America Medical Nutrition business with organic, plant-based enteral and oral nutrition products.

- June 2025: Fresenius Kabi announced the expansion of its Enteral Nutrition Research and Development center in Gurugram, India, equipped with advanced laboratories and specialized infrastructure.

- March 2025: Nutrisens Group announced the acquisition of Prodiet Medical Nutrition, a Brazil-based manufacturer specializing in oral and enteral nutrition products in powder, liquid, and tube feeding formats.

- November 2023: Danone S.A. announced the launch of Fortimel in China, expanding its adult medical nutrition portfolio with post-surgical recovery and disease-specific formulations.

- December 2022: Abbott Laboratories announced a USD 536 million investment to build a new specialty and metabolic powder nutritional manufacturing facility in Bowling Green, Ohio.

REPORT COVERAGE

The global medical nutrition products market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments and investments by key regions. The global market research report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2035 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2035 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.6% from 2026-2035 |

| Unit | Value (USD Billion) |

| Segmentation | By Product, Age, Form, Therapeutic Area, Caloric Density, Nutrition Composition, End-User, and Region |

| By Product |

|

| By Age |

|

| By Form |

|

| By Therapeutic Area |

|

| By Caloric Density |

|

| By Nutrition Composition |

|

| By End-User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 23.86 billion in 2025 and is projected to reach USD 44.72 billion by 2035.

In 2025, the North America market value stood at USD 8.32 billion.

The market is expected to exhibit a CAGR of 6.6% during the forecast period of 2026-2035.

By product, the enteral nutrition segment is expected to lead the market.

Rising prevalence of chronic conditions and rising awareness about benefits of medical nutrition are driving market expansion.

Abbott, B. Braun SE, Nestlé, Danone, and Baxter are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us