Medication Management Software Market Size, Share & Industry Analysis, By Type (Standalone and Integrated), By Application (Computerized Physician Order Entry (CPOE), Clinical Decision Support System Solutions, Software Modernization and Integration, Inventory Management Systems, Prescription Processing Software, Medication Administration Record (MAR) Software, and Others), By Deployment (On-Premise, Cloud-Based, and Hybrid), By End User (Healthcare Payers, Healthcare Providers, Pharmacies, and Others), and Regional Forecast, 2026-2034

Medication Management Software Market Size and Future Outlook

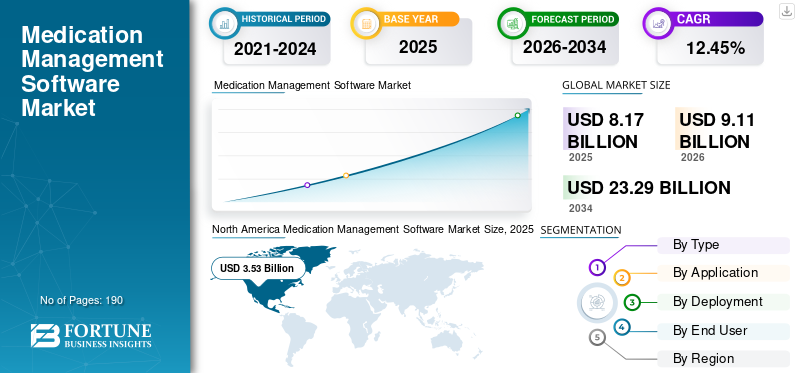

The global medication management software market size was valued at USD 8.17 billion in 2025. The market is projected to grow from USD 9.11 billion in 2026 to USD 23.29 billion by 2034, exhibiting a CAGR of 12.45% during the forecast period. North America dominated the medication management software market with a market share of 43.21% in 2025.

The global market is poised for growth as healthcare settings increasingly adopt technologies to optimize operations. Such management software streamlines the entire medication process from prescription to drug administration. By integrating intelligent medication safety checks and automated systems, prescription errors can be significantly reduced, adverse effects minimized, and medication adherence tracked, thereby enhancing patient safety and outcomes. The varied application of such management software in the healthcare setting boosts global market growth.

Furthermore, innovative product launches in the market that optimize workflows drive market growth.

- For instance, in May 2025, Omnicell, Inc. launched new products designed to streamline workflows and enhance inventory visibility and management in perioperative and clinic settings. These products, which leverage RFID tracking and intelligent software workflows, expand Omnicell’s connected platform, intended to automate medication management processes and deliver intelligent insights to drive clinical and operational outcomes across all settings of care. Such developments are anticipated to boost the overall market growth.

Furthermore, leading players in the industry, such as BD, Omnicell, Inc., Baxter International Inc., and Wolters Kluwer N.V., are directing their resources toward research and development, expanding their offerings, and strengthening their market positions.

Download Free sample to learn more about this report.

Medication Management Software Market Key Takeaways

- 2025 Market Size: USD 8.17 billion

- 2026 Market Size: USD 9.11 billion

- 2034 Forecast Market Size: USD 23.29 billion

- CAGR: 12.45% from 2026–2034

- North America dominated the medication management software market with a 43.21% share in 2025.

- The integrated segment accounted for the largest share of the global market in 2025.

- The hybrid segment is projected to grow at a 12.34% CAGR during the forecast period.

North America

North America led the market with USD 3.53 billion in 2025.

Europe

Europe is projected to reach USD 2.33 billion in 2026 at a 10.39% CAGR.

Asia Pacific

Asia Pacific is estimated to reach USD 2.05 billion in 2026.

U.S

The U.S. market is estimated at USD 3.60 billion in 2026, accounting for 39.52% of global revenue

Japan

The Japan market is projected to reach USD 0.50 billion in 2026, representing 5.44% of global revenue.

Read More

MEDICATION MANAGEMENT SOFTWARE MARKET TRENDS

Medication Safety Analytics and Surveillance Becoming a Core Application is Observed as a Prominent Market Trend

A significant market trend observed in the global market is an increasing focus on safety analytics and surveillance. Medication safety analytics and surveillance are becoming a core application for healthcare providers. As drug regimens get more complex and care teams face workload constraints, dispensing logs becomes inconsistent, the need for software that continuously monitors risk signals increases. These developments also improve standardization in health care and reduce practice variance. As a result, buyers increasingly treat surveillance as a necessity within medication management software suites.

Emphasizing the increasing demand for safety analytics, numerous solutions providers are launching updates in these applications to strengthen their market position.

- For instance, in June 2025, Wolters Kluwer N.V. introduced updates to its Sentri7 Drug Diversion and Sentri7 Pharmacy solutions, reinforcing its commitment to innovation in medication safety, compliance, and patient care. These improvements equipped clinical teams with data-driven insights to streamline workflows for drug diversion and medication management. Such developments are expected to boost market growth.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Focus on Reducing Errors in Medication Management to Drive Demand and Boost Market Growth

Increasing focus on patient safety and error reduction is a key market driver. Medication errors are one of the preventable events in care delivery. Providers are undertaking initiatives to reduce harm. As treatment pathways become more complex, the risk of wrong dose, or missed administration rises. Such management software reduces this risk by embedding standardized workflows and automated checks at the point of prescribing and verification. It also strengthens execution by improving the efficiency of orders that are administered, and documented. As these outcomes directly impact quality ratings, litigation exposure, and operational cost, safety-led investments continue to expand global medication management software market demand.

- For instance, at the July 2025 Epic European Group Meeting (EGM 2025), healthcare leaders highlighted results achieved through the use of health IT. They reported the positive impact of automation on clinical workflows, reducing reliance on manual input. The initiative improved clinicians’ workflows and delivered a 550.0% increase in charge capture at Royal Marsden. Such factors highlight the efficiency of these platforms, which are expected to drive market growth.

MARKET RESTRAINTS

High Cost Associated with Medication Management Software to Hamper Market Growth

High cost of such management software implementation hampers the adoption. Most deployments require enterprise licensing plus interfaces to the EHR, pharmacy stock control, dispensing, and identity systems. Such complex medication rules/formularies, validation, training, and change management, adds to the cost. Smaller hospitals and resource-constrained regions often delay projects as the upfront cash outlay competes with staffing, clinical capacity, and other digital priorities. Even when ROI is clear, leaders may phase rollouts by ward/site to control spend, which slows market conversion.

- For instance, in October 2025, Royal Cornwall Hospitals placed the total cost of its eCare EPR project at USD 46.5 million, noting that inpatient electronic prescribing and medicines administration followed shortly after go-live, showing how medication management capability is often part of a very high-cost enterprise transformation program.

MARKET OPPORTUNITIES

Rising Investment in AI-Enabled Medication Management Software to Unlock New Growth Opportunities

Healthcare providers are increasing investment in such software to reduce medication risk while operating with tight staffing and higher patient complexity. As medication data expands across ordering, dispensing, and administration workflows, AI adds value by spotting patterns and exceptions that manual review often misses. This shifts software from documentation to decision support, where analytics can prioritize high-risk events, support faster interventions, and improve consistency across sites. AI integration also strengthens controlled-substance governance by helping detect diversion indicators earlier, thereby protecting patients and reducing compliance exposure. As a result, vendors that embed AI into surveillance, safety analytics, and workflow automation can expand into new budgets tied to quality, safety, and compliance outcomes. This creates a clear growth opportunity for platforms that can prove measurable reductions in risk, time, and operational leakage.

- For instance, in October 2025, BD launched the BD Incada, a connected care platform that unified the company’s device data into one intelligent ecosystem for the first time. Such developments offer medication management software market growth opportunities.

MARKET CHALLENGES

Inconsistent Data Quality to Hamper Market Growth

One of the major challenges in the market is inconsistent data quality. These platforms are reliable only if the underlying inputs they receive from EHRs, pharmacies, and historical medication sources are consistent. When medication histories are incomplete, clinicians are equipped with the wrong baseline list, leading to reconciliation gaps during admission, transfer, and discharge. Duplicate records and mismatched identifiers also inflate data in safety dashboards, making surveillance less actionable and increasing alert fatigue. As a result, buyers often delay deployments or limit scope, slowing market adoption.

Segmentation Analysis

By Type

Reduced Fragmentation Due to Integrated Offerings to Position Them in Leading Position

Based on type, the market is categorized into standalone and integrated.

Among these, the integrated segment accounted for the largest global medication management software market share in 2025. Integrated management software for medication dominates, offering a single platform with medication ordering, verification, administration, and reconciliation. This reduces delays and avoids inconsistencies that can trigger errors. Integration also makes it easier to audit trails across multiple hospitals and care settings, for enterprise standardization. Overall, buyers pay more for integrated solutions as they reduce operational fragmentation and strengthen medication safety controls at scale.

Additionally, highlighting the ease of integrated platforms, various key companies are directing their resources toward new product launches that align with such management software workflows.

- For instance, in December 2024, Omnicell, Inc. launched OmniSphere, a next-generation, cloud native software workflow engine and data platform. The platform is designed to integrate robotics and smart devices to support more secure, data-driven medication management across the continuum of care. Such developments are expected to drive the segment's growth.

The standalone segment is expected to grow at a CAGR of 8.54% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Increasing Utilization of Clinical Decision Support System Solutions to Lead Segmental Growth

Based on the application, the market is segmented into computerized physician order entry (CPOE), clinical decision support system solutions, software modernization and integration, inventory management systems, prescription processing software, medication administration record (MAR) software, and others.

In 2025, clinical decision support system solutions will be dominated based on application. It directly influences prescribing and therapy decisions. When a CDSS layer is embedded into ordering and verification workflows, it helps reduce risks and flag interactions, duplications, dosing issues, and inappropriate therapies. Such a factor improves patient safety and reduces the incidence of adverse drug events, readmissions, and rework. CDSS also strengthens compliance by documenting how the medication decision was made, which is important for audits and quality programs. Underscoring these factors, CDSS tends to command recurring subscription spend and therefore a larger revenue share. Innovative product launches for CDSS further reinforce the segment's dominance.

- For instance, in October 2025, FDB launched pilot integrations of its Model Context Protocol (MCP) server, a new technology designed to support AI and agentic applications in healthcare, such as prescription automation, ambient listening enablement, pre-processing pharmacy order verification, and medication reconciliation, to free up time for clinicians to focus on patient care.

Software modernization and integration is projected to grow at a CAGR of 16.26% during the forecast period for the global market.

By Deployment

Increasing Preference of Healthcare Providers toward On-Premise Deployed Platforms to Drive Segmental Growth

Based on deployment, the market is segmented into on-premises, cloud-based, and hybrid.

Among these, on-premise deployment accounted for the largest share. Large hospitals and closed networks increasingly prefer to keep medication data and clinical data in a controlled environment. On-premise deployments also reduce dependence on internet uptime, reducing medication administration downtime assisting workflows. These factors favor the growth of on-premise segments as safer alternatives for enterprise medication workflows. As a result, buyers increasingly prefer on-premise medication platforms, which reinforce the segment's dominance.

- For instance, in January 2024, Medicalistics launched on premise solution eZmar X for documenting medication administration.

In addition, the hybrid segment is projected to grow at a CAGR of 12.34% during the study period.

By End User

Increasing Demand by Healthcare Payers to Lead Growth in Segment

Based on end user, the market is segmented into healthcare payers, healthcare providers, pharmacies, and others.

Healthcare payers held the dominant share of the market by end user in 2025. Payers need medication decision support and real-time benefit tools to steer prescribing toward cost-effective alternatives and improve adherence. Payers also require standardized medication data and interoperability so that formularies, benefit designs, and medication histories can be applied consistently across networks. This creates sustained demand for payer-facing medication workflow software and transaction platforms, resulting in recurring revenue.

- For instance, in June 2024, Surescripts implemented the National Council for Prescription Drug Programs (NCPDP) SCRIPT Standard Version 2023011, Real-Time Prescription Benefit v13, and Formulary and Benefit v60 standards, following the Centers for Medicare & Medicaid Services (CMS) publication, to improve patient safety and workflow efficiency.

The healthcare providers segment is projected to grow at a CAGR of 12.28% over the study period.

Medication Management Software Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Medication Management Software Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valued at USD 3.17 billion, and maintained its leading position in 2025, with a value of USD 3.53 billion. The market in North America is expected to grow significantly over the forecast period, driven by large-scale discovery and translational programs in the region. The region also has a dense population and an increasing need for specialized providers.

U.S. Medication Management Software Market

Given North America’s substantial contribution and the U.S. dominance in the region, the U.S. market can be estimated at around USD 3.60 billion in 2026, accounting for roughly 39.52% of the global market.

Europe

Europe is projected to grow at 10.39% over the coming years, the second-highest among all regions, and reach a valuation of USD 2.33 billion by 2026. The area is expected to experience robust growth driven by the increasing prevalence of key diseases and a rising ageing population, which is boosting demand.

U.K. Medication Management Software Market

The U.K. market size in 2026 is estimated at around USD 0.36 billion, representing roughly 3.97% of the global market.

Germany Medication Management Software Market

Germany’s market is projected to reach approximately USD 0.60 billion in 2026, equivalent to around 6.64% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 2.05 billion in 2026 and secure the position of the third-largest region in the market. The region's growth is driven by rising healthcare expenditure and rapid technology adoption.

Japan Medication Management Software Market

The Japanese market in 2026 is estimated to be around USD 0.50 billion, accounting for approximately 5.44% of the global market.

China Medication Management Software Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.69 billion, representing approximately 7.55% of global sales.

India Medication Management Software Market

The Indian market in 2026 is estimated at around USD 0.17 billion, accounting for roughly 1.84% of global revenue.

Latin America and the Middle East & Africa

Latin America and the Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.48 billion in 2026. The region is experiencing market growth driven by increased government support. In the Middle East & Africa, the GCC is set to reach USD 0.16 billion in 2026.

South Africa Medication Management Software Market

The South African market is projected to reach approximately USD 0.05 billion by 2026, accounting for roughly 0.54% of the global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on New Product Launches by Key Players to Propel Market Progress

The global market for medication management software is highly consolidated, with companies such as BD, Omnicell, Inc., Baxter International Inc., and Wolters Kluwer N.V. holding a considerable market share. Strategic partnerships, new product launches, technological advancements, and increased investments in the sector drive these companies' market share gains.

- For instance, in November 2025, Wolters Kluwer Health launched the first in a series of expansions of its GenAI clinical decision support solution, UpToDate Expert AI. Comprehensive medication information from UpToDate Lexidrug, the drug reference tool, will be integrated into the AI resource for enhanced medication and therapeutic decision support, such developments are aimed to drive market growth.

Other notable players in the global market include Epic Systems Corporation, Oracle, and Medical Information Technology, Inc. These companies are expected to prioritize technological advancements, strategic collaborations, and new product launches to strengthen their position during the forecast period for the global market.

LIST OF KEY MEDICATION MANAGEMENT SOFTWARE COMPANIES PROFILED

- BD (U.S.)

- Omnicell, Inc. (U.S.)

- Baxter International Inc. (U.S.)

- Wolters Kluwer N.V. (Netherlands)

- Epic Systems Corporation (U.S.)

- Oracle (U.S.)

- Medical Information Technology, Inc. (U.S.)

- NextGen Healthcare, Inc. (U.S.)

- McKesson Corporation. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- October 2025: BD launched the BD Incada Connected Care Platform, an AI-enabled platform that unifies BD device data into one intelligent ecosystem. The platform is now available with the launch of the next-generation BD Pyxis Pro Automated Medication Dispensing Solution, creating enterprise-wide visibility and connectivity that transform data into actionable insights.

- September 2025: PracticeSuite acquired MicroMD to underscore the company’s commitment to accelerating growth, broadening its customer base, and delivering a unified, best-in-class experience for ambulatory care practices of all sizes.

- September 2025: MDI Health, a leader in personalized medication management and polypharmacy optimization, today announced a research collaboration with Stanford Medicine’s Healthcare AI Applied Research Team (HEA₃RT), a cutting-edge team at Stanford advancing responsible, effective, and scalable AI solutions in primary and population health.

- July 2025: HealthArc partnered with PatchRx, a manufacturer of smart medication adherence technology. The development aimed to integrate their solutions to provide a comprehensive, connected offering for patients and providers, thereby improving medication adherence.

- July 2022: BD acquired MedKeeper, a provider of modern, cloud-based pharmacy management applications. MedKeeper complemented the company’s existing presence in the pharmacy and pioneered solutions in compounding, logistics workflows, controlled substance management, and inventory optimization.

REPORT COVERAGE

The global medication management software market analysis includes a comprehensive study of market size & forecast across all market segments covered in the report. It contains details on the market dynamics and trends expected to drive the global market over the forecast period. It provides information on key aspects, including technological advancements and new product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments. The global market research report also provides a detailed competitive landscape, including market share and profiles of major operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 12.45% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, Application, Deployment, End User, and Region |

| By Type |

|

| By Application |

|

| By Deployment |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 8.17 billion in 2025 and is projected to reach USD 23.29 billion by 2034.

In 2025, the market value stood at USD 3.53 billion.

The market is expected to grow at a CAGR of 12.45% over the forecast period.

The integrated segment is expected to lead the market.

The increasing focus on reducing errors in medication management is driving market growth.

BD, Omnicell, Inc., Baxter International Inc., Wolters Kluwer N.V., and Epic Systems Corporation are the major market players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us