Urgent Care Apps Market Size, Share & Industry Analysis, By Type (Pre-Hospital Emergency Care & Triaging Apps, In-Hospital Communication & Collaboration Apps, and Post-Hospital Apps { Medication Management Apps, Rehabilitation Apps, and Care Provider Communication & Collaboration Apps}), By Application (Trauma, Stroke, Cardiac Conditions, Rashes & Allergies, Tract Infections, Musculoskeletal Pain & Injuries, and Others), By Platform (iOS, Android, and Others), By Care Setting (Hospitals and ASCs, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

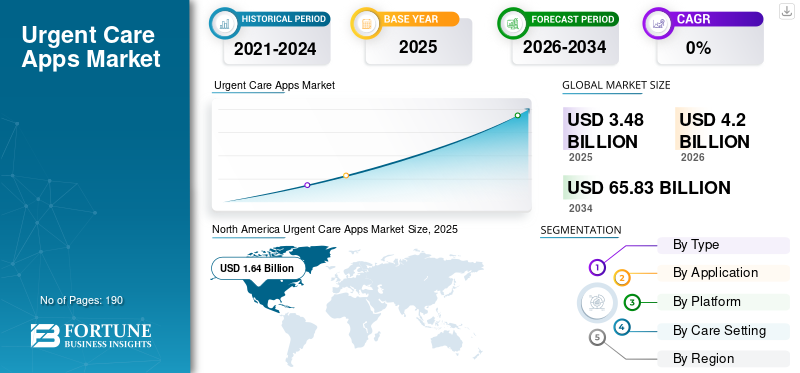

The global urgent care apps market size was valued at USD 3.48 billion in 2025. The market is projected to grow from USD 4.20 billion in 2026 to USD 65.83 billion by 2034, exhibiting a CAGR of 41.04% during the forecast period. North America dominated the global market with a market share of 47.13% in 2025.

The global urgent care apps market is poised for exponential growth in the coming years, driven by the increasing focus on digitalization in healthcare, emergency overcrowding, and the rising popularity and adoption of mobile health apps. The increasing adoption of these healthcare systems has expanded the market's scope. These urgent care apps assist with contacting urgent healthcare providers and scheduling meetings, facilitating smooth business operations.

Several key companies are launching their own urgent care apps to enhance the patient experience and deliver better care.

- For instance, in April 2025, Castlight Health launched its Virtual Urgent Care (VUC) solution to enhance the virtual care experience by integrating the company’s healthcare benefits navigation app. This app provided a unified, high-quality care experience accessible to members whenever and wherever they need it.

Furthermore, many key industry players, such as Teladoc Health, Inc., Allm Inc., and Stryker, operating in the market, are focusing on developing various innovative healthcare solutions to support the growing the global market demand and diversify product offerings.

Download Free sample to learn more about this report.

Urgent Care Apps MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 3.48 billion

- 2026 Market Size: USD 4.20 billion

- 2034 Forecast Market Size: USD 65.83 billion

- CAGR: 41.04% from 2026–2034

- North America dominated the urgent care apps market with a 47.13% share in 2025.

- Post-hospital apps segment led the market with 34.50% share in 2025.

- Android segment dominated due to its large global user base and high accessibility in emerging markets.

North American

North America held USD 1.64 billion in 2025 and USD 1.39 billion in 2024, driven by high telehealth adoption and insurer partnerships.

Europe

Europe is projected to reach USD 0.93 billion in 2026, supported by strong data protection regulations and rapid digital health adoption.

Asia Pacific

Asia Pacific is expected to reach USD 1.09 billion in 2026, driven by rising mobile penetration and telemedicine expansion.

U.S.

Market estimated at USD 1.81 billion in 2026, driven by strong telehealth infrastructure and payer-provider collaboration.

Japan

Market estimated at USD 0.26 billion in 2026, supported by increasing digital healthcare adoption and aging population needs.

Read More

URGENT CARE APPS MARKET TRENDS

Mental Health Triage Embedded in Urgent Care Triage Is a Prominent Trend Observed in Market

A prominent trend observed in the urgent care apps market is the increasing development of applications for mental health triage. With increasing incidences of behavioral health-related indications such as panic attacks, severe distress, and self-harm risk, the need for fast, safe routing is elevated. Embedding mental health screening questions and escalation logic within urgent-care journeys helps platforms and health systems identify crisis indicators early, reduce avoidable load, and improve patient safety and experience. These factors have encouraged key companies to actively take initiatives to effectively formalize mental health triage within the urgent care access channel used for time-sensitive health needs.

- For instance, in June 2025, Ovatient launched its virtual-first care offering, built on Epic and MyChart, in South Carolina to expand its virtual-first primary, urgent, and behavioral health care services in collaboration with the Medical University of South Carolina's health system. The solution provided on-demand urgent care and virtual-first primary care, as well as integrated behavioral health services, with the expectation of delivering care to more than 50,000 MUSC Health patients. Such developments support the growth of the global market.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Emergency Room Overcrowding and Long Wait Times to Increase Demand and Drive Market Growth

The major factor driving the global market is the rising Emergency Room (ER) overcrowding and long wait times. A significant portion of ER visits involves non-life-threatening conditions that could be treated more quickly and at a lower cost elsewhere. These factors can lead to overburden and result in delayed care, patient dissatisfaction, and higher healthcare spending. Urgent care apps address this challenge by offering immediate symptom triage, virtual urgent consultations, real-time clinic availability, and digital check-ins, enabling patients to avoid unnecessary ER visits and receive timely care. As health systems and insurers actively promote these apps to reduce ER congestion and optimize care delivery, adoption and utilization of urgent care apps continue to rise, directly supporting global urgent care apps market growth.

- For instance, in October 2024, the NHS reported that there had been 1.2 million more attendances at Accident and Emergency (A&E) departments. The huge pressure on services saw many patients waiting too long for care, with four-hour performance remaining below the constitutional standard of 95%, at 74.2%. Such high incidences necessitate the need for effective urgent care apps to optimize resource allocation and management.

MARKET RESTRAINTS

High Customer Acquisition Cost to Hamper Market Growth

High Customer Acquisition Costs (CAC) are a major restraint for the market, hindering its growth. The majority of health apps rely heavily on paid digital channels, such as Google search, app store ads, and social media, to acquire first-time users, especially when demand for urgent care is irregular. With increasing competition from other players, and keyword bids and paid media rates rising, the spending on advertisement and marketing increases to differentiate product offerings. This increases the customer acquisition cost, discouraging companies in the long run. This pushes up CAC, delays payback, and compresses margins.

- For instance, in June 2024, Medico Digital published an article analyzing USD 5.7 million invested in direct-to-patient Google Search ad spend across 50+ ad accounts, reporting an average cost per acquisition (CPA) of USD 33.2. These factors highlight that paid search/social can face high CAC and margin pressure and restrict the market growth.

MARKET OPPORTUNITIES

Expanding Urgent Care Apps into Chronic-Adjacent Urgent Needs to Offer Lucrative Market Growth Opportunities

Expanding urgent care apps into chronic-adjacent urgent needs, such as asthma, COPD flare-ups, diabetes-related issues, hypertension spikes, medication side effects, and sudden symptom worsening, offers a lucrative growth opportunity. This development increases the addressable patient base and the frequency of use. Furthermore, unlike acute illnesses, chronic conditions create recurring demands, where patients require prompt guidance, medication adjustments, or rapid clinical decisions to prevent complications. By offering condition-specific pathways, urgent care apps can reduce preventable ER visits and boost monetization through higher visit volumes.

- For instance, in October 2024, VSee Health, Inc. launched a specialized program designed to address obesity and associated health risks by integrating GLP-1 prescription medicines into its existing telehealth service offerings. The initiative builds on its existing infrastructure offering of virtual urgent care, primary care, and wellness services.

MARKET CHALLENGES

Lack of Integration Between Virtual and In-Person Visits to Hinder Pose a Critical Challenge to Market Growth

A lack of integration between virtual and in-person visits is a key market challenge for urgent care apps, as many urgent episodes still require physical exams, diagnostics, or follow-up care. These concerns over integration can lead to repeat visits, delayed diagnosis, inconsistent treatment plans, and poor follow-up, which in turn fuels concerns over care quality and patient safety.

- For instance, in October 2025, the Care Quality Commission reported that the health and social care system remains fragmented and under severe strain as it prepares for a major shift from hospital to community care, resulting in a decline in the quality of care. These factors pose a significant challenge to the market.

Segmentation Analysis

By Type

Adoption of Urgent Care App Solutions in High Volume to Propel Segmental Growth

Based on type, the market is divided into pre-hospital emergency care & triaging apps, in-hospital communication and collaboration apps, and post-hospital apps.

Post-hospital apps segment dominated the global urgent care market in 2025 due to high utilization by healthcare payers and providers. They are often necessary, as most complications occur after discharge, when patients are at home and need help following instructions for medications, wound care, scheduling follow-up appointments, and managing billing among others. These apps also assist to set up reminders, symptom monitoring, and fast escalation, which directly lower readmissions and prevent unnecessary ER returns, making them a priority investment area for providers and payers.

Furthermore, numerous innovative launches for these solutions by key companies support the market growth.

- For instance, in June 2025, Altera Digital Health launched Sunrise CarePath, a mobile patient engagement platform that helps hospitals to close communication gaps and reduce adverse events, readmissions, and financial barriers. Such developments are anticipated to drive the market growth.

The in-hospital communication & collaboration apps segment is expected to grow at a CAGR of 41.30% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

High Incidence Rate of Tract Infections Boosted Tract Infections Segment Growth

Based on application, the market is segmented into trauma, stroke, cardiac conditions, rashes and allergies, tract infections, musculoskeletal pain & injuries, and others.

In 2025, tract infections dominate urgent care apps market. This dominance is attributed to high incidences of tract infections, high-frequency, fast-onset, and reported effectiveness showcased by symptom screening, quick clinician review, e-prescription, and at-home testing through digital health technologies. Also increasing preference of patients toward privacy for these symptoms, result in elevated adoption of these digital/urgent care apps driving high consultation volumes and repeat use.

- For instance, in October 2023, AZOVA launched an UTI Telehealth Bundle that provided at home diagnostic services, demonstrating how these apps are commercializing UTI/tract infection care in urgent use case.

The cardiac conditions segment is projected to grow at a CAGR of 45.19% during the forecast period for the global urgent care apps market.

By Platform

Widespread Usage and Numerous Advantages Boosted Android Segment Growth

Based on the platform, the market is segmented into IOS, Android, and others.

In 2025, Android dominated the global market due to its large global smartphone install base, particularly in price-sensitive and emerging markets. The urgent care app adoption in these price sensitive market is growing rapidly. Android-first distribution provides the large reachable user pool, resulting in higher downloads, bookings, and app-based visit volume.

- For instance, in November 2025, Stat Counter’s global mobile OS tracking shows that Android had the majority share of global mobile operating systems user base between November 2024- November 2025.

The iOS segment is projected to grow at a CAGR of 43.34% during the forecast period for the global urgent care apps market.

By Care Setting

Strategic Initiatives by Hospitals & ASCs Kept them in a Leading Position

Based on care setting, the market is segmented into Hospitals and ASCs, specialty clinics, and others.

Hospitals and ASCs dominate as they have the strongest operational need and budget to deploy apps at scale in these centers, due to high patient throughput, scheduling complexity, and pre- and post-visit instructions, among others. Apps help these facilities improve patient flow, reduce admin load, and maintain continuity beyond the facility, making them the most common and impactful adopters compared with smaller specialty clinics.

- For instance, in September 2024, HST Pathways and SYNERGEN Health announced a partnership to enhance revenue cycle management services for ambulatory surgery centers. Such collaborations and partnerships are needed to drive the growth of the segment.

In addition, the specialty clinics segment is projected to grow at a CAGR of 41.45% during the study period.

Urgent Care Apps Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Urgent Care Apps Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant global urgent care apps market share in 2024, valued at USD 1.39 billion, and maintained its leading position in 2025, with a value of USD 1.64 billion. The market in North America is expected to increase significantly over the projected years. North America represents a leading market for urgent care apps, driven by the high adoption of telehealth and insurer partnerships in the region. Healthcare providers in the U.S. and Canada are investing in expanding their urgent care solutions. These factors are enabling market growth.

U.S Urgent Care Apps Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 1.81 billion in 2026, accounting for roughly 43.0% of the global urgent care apps market.

Europe

Europe is projected to record a growth rate of 37.75% in the coming years, the second-highest among all regions, and reach a valuation of USD 0.93 billion by 2026. The region is estimated to have robust demand, along with support from regulatory bodies for data protection regulations, and rapid adoption by urban healthcare centers.

U.K. Urgent Care Apps Market

The U.K. urgent care apps market in 2026 is estimated to be around USD 0.14 billion, representing roughly 3.4% of the global market in 2026.

Germany Urgent Care Apps Market

Germany’s urgent care apps market is projected to reach approximately USD 0.24 billion in 2026, equivalent to around 5.8% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 1.09 billion in 2026 and secure the position of the third-largest region in the market. The growth is attributed to rising government support for expansion of telemedicine as well as increasing penetration of mobile connectivity in the region.

Japan Urgent Care Apps Market

The Japan urgent care apps market in 2026 is estimated at around USD 0.26 billion, accounting for roughly 6.2% of the global market.

China Urgent Care Apps Market

China’s urgent care apps market is projected to be one of the largest globally, with 2026 revenues estimated at around USD 0.37 billion, representing roughly 8.7% of global urgent care apps sales.

India Urgent Care Apps Market

The Indian urgent care apps market in 2026 is estimated to be around USD 0.09 billion, accounting for roughly 2.1% of the global urgent care apps revenue.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.09 billion in 2026. The region is experiencing an increase in the adoption of urgent care apps in larger private hospitals and health systems and government initiatives promoting digital health. In the Middle East & Africa, the GCC is set to reach a value of USD 0.06billion in 2026.

South Africa Urgent Care Apps Market

The South Africa urgent care apps market is projected to reach approximately USD 0.02 million by 2026, accounting for roughly 0.48% of the global urgent care apps revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Strategic Initiatives by Key Players to Propel Market Progress

The global urgent care apps market has a semi-consolidated market structure, comprising prominent players such as Teladoc Health, Inc., Allm Inc., and Stryker. The significant market share of these companies is due to numerous strategic activities, including collaboration among operating entities to diversify new product launches through various mergers and acquisitions.

- For instance, in November 2025, TytoCare integrated with Teladoc Health. This collaboration integrated the company’s Home Smart Clinic with Teladoc Health’s 24/7 Care and Primary360 primary care programs, using advanced home diagnostic technology to provide clinical insights to virtual care clinicians. Such acquisitions aim to expand the product offering and drive market growth.

Other notable players in the global market include AlayaCare and Hartford HealthCare. These companies are expected to prioritize new product launches and collaborations to increase their global market share during the forecast period.

LIST OF KEY URGENT CARE APPS COMPANIES PROFILED

- Teladoc Health, Inc. (U.S.)

- Allm Inc. (U.S.)

- Stryker (U.S.)

- AlayaCare (U.S.)

- Hartford HealthCare (U.S.)

- (U.S.)

- Medisafe (U.S.)

- Imprivata, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2025: VSee Health, Inc. collaborated with Novant Health Urgent Care to organize a webinar focusing on how healthcare organizations can design and scale high-return virtual urgent-care programs that combine operational efficiency with meaningful patient impact.

- November 2025: TytoCare, integrated with Teladoc Health, a leader in virtual care. This collaboration aimed to integrate the company’s Home Smart Clinic with Teladoc Health’s 24/7 Care and Primary360 primary care programs, using advanced home diagnostic technology to provide clinical insights to virtual care clinicians.

- November 2025: Vital launched Vital Urgent Care, an AI-powered platform that provides patients in urgent care settings with real-time updates, accurate wait times, education, and personalized guidance without requiring downloads or login credentials.

- November 2025: MedVanta launched VantaStat, an urgent care line and mobile app that transformed how patients access orthopedic care. Providing immediate, expert guidance for injuries, joint pain, or fractures without the frustration, delay, or expense of an emergency room visit.

- October 2025: HealthTap partnered with Samsung Health to embed access to virtual primary and urgent care directly into the Samsung Health app. Samsung Health users will be able to book, conduct, and follow up on virtual care consultations within the app experience.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 41.04% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type, Application ,Platform, Care Setting, and Region |

|

By Type |

· Pre-Hospital Emergency Care & Triaging Apps · In-Hospital Communication & Collaboration Apps · Post-Hospital Apps o Medication Management Apps o Rehabilitation Apps o Care Provider Communication & Collaboration Apps |

|

By Application |

· Trauma · Stroke · Cardiac Conditions · Rashes & Allergies · Tract Infections · Musculoskeletal pain & injuries · Others |

|

By Platform |

· iOS · Android · Others |

|

By Care Setting |

· Hospitals and ASCs · Specialty Clinics · Others |

|

By Region |

· North America (By Type, Application, Platform, Care Setting, and Country) o U.S. o Canada · Europe (By Type, Application, Platform, Care Setting, and Country/Sub-region) o Germany o U.K. o France o Spain o Italy o Scandinavia o Rest of Europe · Asia Pacific (By Type, Application, Platform, Care Setting, and Country/Sub-region) o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific · Latin America (By Type, Application, Platform, Care Setting, and Country/Sub-region) o Brazil o Mexico o Rest of Latin America · Middle East & Africa (By Type, Application, Platform, Care Setting, and Country/Sub-region) o GCC o South Africa o Rest of Middle East & Africa |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 3.48 billion in 2025 and is projected to reach USD 65.83 billion by 2034.

In 2025, the market value stood at USD 1.64 billion.

The market is expected to exhibit a CAGR of 41.04% during the forecast period of 2026-2034.

By type, the post-hospital apps segment is expected to lead the market.

The rising emergency room crowding and long waiting times to drive demand and boost market expansion.

Teladoc Health, Inc., Allm Inc., Stryker, and AlayaCare are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us