Microelectronic Medical Implants Market Size, Share & Industry Analysis, By Product Type (Cardiac Rhythm Management Implants, Neurostimulation Implants, Cochlear Implants, Ophthalmic Implants, and Others), By Application (Cardiovascular Disorders, Neurological Disorders, Gastrointestinal Disorders, Urological Disorders, and Others), By End User (Hospitals & ASCs, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

Microelectronic Medical Implants Market Size and Future Outlook

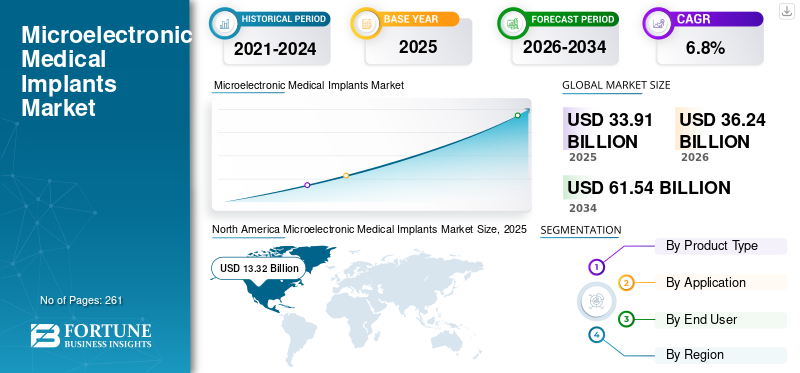

The global microelectronic medical implants market size was valued at USD 33.91 billion in 2025 and is projected to grow from USD 36.24 billion in 2026 to USD 61.54 billion by 2034, exhibiting a CAGR of 6.8% during the forecast period. North America dominated the microelectronic medical implants market with a market share of 39.28% in 2025.

Microelectronic medical implants are surgically inserted, miniature, biocompatible devices used to monitor, diagnose, or treat disorders by directly interacting with physiological systems. The increasing prevalence of chronic disorders, rising preference towards minimally invasive procedures, and the expansion of healthcare and reimbursement infrastructure are resulting in a growing adoption rate of these devices in the market. The increasing aging population is further contributing to the demand for long-term implantable therapeutic devices among patients, thereby boosting the adoption rate of microelectronic medical implants in the market.

- For instance, according to the 2024 data published by the Centers for Disease Control & Prevention (CDC), about 1 in 20 adults aged 20 and older has coronary artery disease.

Additionally, the growing integration of technological advancements in these devices among the major companies, such as Medtronic, Abbott, among others, is further contributing to the demand for these devices in the market.

Download Free sample to learn more about this report.

Microelectronic Medical Implants Market Trends

Technological Advancements in the Medical Products to Fuel the Demand

The technological advancements in sensors, microelectronics, wireless connectivity, and miniaturization technologies are rapidly transforming miniaturized microelectronic medical implants. The advanced implants are increasingly equipped with technologically advanced biosensors, AI-enabled algorithms, digital health platforms, and wireless communication products, enabling real-time monitoring of physiological parameters and allowing tailored therapy management. The development of adaptive neurostimulators, leadless pacemakers, and energy-efficient implantable devices is also enhancing patients' comfort, longevity, and device performance.

Moreover, the advancements, including improved battery life, miniaturized circuitry, and biocompatible materials, are allowing the development of reliable implants with fewer complications, thereby augmenting adoption across various applications.

- In January 2026, Vivani Medical, Inc., a clinical-stage biopharmaceutical company developing miniature implants, announced the presentation of an award-winning poster detailing the technical aspects of its Orion Visual Cortical Prosthesis System, a brain implant that is under development to deliver meaningful visual perception to blind persons by its wholly-owned subsidiary, Cortigent, Inc.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Increasing Prevalence of Chronic Conditions to Boost the Market Growth

The increasing prevalence of chronic conditions such as neurological and urological disorders, chronic pain, and others is driving the demand for miniaturized medical implants, thereby increasing the product demand.

- For instance, according to 2025 data published by the Alzheimer’s Association, it was reported that over 7 million Americans are living with Alzheimer’s in the U.S.

This, along with rising geriatric population and technological advancements in these implants to provide real-time treatment, enhanced patient outcomes, and improved quality of life, is also supporting the growing adoption rate of these devices in the market. Therefore, the factors above, along with the growing emphasis of major companies on research and development to launch novel devices such as pacemakers and defibrillators, are anticipated to boost adoption rates for these products, thereby supporting the global microelectronic medical implants market growth.

Market Restraints

High Capital Cost Associated with these Implants to Hinder the Market Growth

The high cost associated with the manufacturing, development, and surgical implantation of these implants acts as a major restraint on market growth. These devices require extensive research and development, advanced components, a complex development procedure, and stringent clinical trials to meet strict safety and regulatory policies globally.

Furthermore, implantation procedures often involve specialized professionals, healthcare infrastructure, and post-operative monitoring, which significantly increase overall treatment costs among the patient population, thereby limiting the adoption rate and growth of the market globally.

- For instance, according to 2025 data published by Biology Insights, the total cost for a pacemaker implantation procedure typically ranges between USD 20,000 and over USD 100,000 in the U.S.

Market Opportunities

Expansion of Ambulatory Surgical Centers (ASCs) Expected to Create Growth Opportunities

The rapid expansion of ambulatory surgical centers (ASCs) globally is anticipated to create growth opportunities for the market. The advantages associated with ambulatory surgical centers, such as lower costs, shorter recovery times, and enhanced patient convenience as compared to traditional hospital settings, are resulting in a growing patient population opting for these settings globally.

Additionally, the growing preference for minimally invasive surgeries is further enabling healthcare providers to incorporate technologically advanced implantable devices in outpatient settings, thereby favoring the expansion of the market.

- According to 2025 statistics published by Definitive Healthcare, there are about 10,000 active ambulatory surgical centers (ASCs) in the U.S.

Market Challenges

Limited Healthcare Access in Developing Nations to Limit the Market Growth

There is a growing demand for minimally invasive surgeries among the patient population. However, limited adoption of technologically advanced devices, limited healthcare expenditure, strict regulatory approval processes, inadequate reimbursement framework, coupled with concerns related to device safety and long-term reliability, especially in emerging nations, are resulting in limited access to healthcare facilities among the patient population.

Additionally, a limited number of clinical facilities and limited professionals, among others, are some of the crucial factors, resulting in the delayed surgical procedures and implantation of miniaturized implants among the patient population, especially in developing nations, such as China, Brazil, among others.

- For instance, according to 2024 statistics published by Agência Brasil, there are about 2.81 healthcare professionals per thousand people in Brazil.

SEGMENTATION ANALYSIS

By Product Type

Increasing Adoption of Cardiac Rhythm Management Implants Led to the Segmental Dominance

Based on the product type, the market is classified into cardiac rhythm management implants, neurostimulation implants, cochlear implants, ophthalmic implants, and others.

To know how our report can help streamline your business, Speak to Analyst

The cardiac rhythm management implants segment held the largest revenue share in 2025. The growth is due to the increasing incidence of chronic diseases among the patient population, resulting in a rising number of implantations among the patient population globally. This, coupled with the growing emphasis of key companies on launching innovative products, is further anticipated to contribute to the global microelectronic medical implants market share.

- For instance, in October 2025, BIOTRONIK announced the successful first-in-human implantation of a device from its Acticor/Rivacor Sky ICD/CRT-D devices, specifically engineered to support conduction system pacing via left bundle branch area pacing (LBBAP).

The ophthalmic implants segment is expected to grow at a CAGR of 8.7% over the forecast period.

By Application

Increasing Prevalence of Cardiovascular Disorders Led to the Dominance of the Segment

Based on application, the market is segmented into cardiovascular disorders, neurological disorders, gastrointestinal disorders, urological disorders, and others.

The cardiovascular disorders segment dominated the global market in 2025, accounted for 45.6% of the market share. The growth is due to the growing prevalence of cardiovascular diseases, resulting in an increasing number of minimally invasive surgical procedures globally, thereby contributing to the adoption rate of these devices in the market.

- For instance, according to the 2024 statistics published by the Centers for Disease Control & Prevention (CDC), someone has a heart attack every 40 seconds in the U.S.

The segment of neurological disorders is set to flourish with a growth rate of 8.1% across the forecast period.

By End-user

Increasing Number of Hospitals & ASCs Owing to Growing Chronic Disorders Led to the Segmental Dominance

Based on end user, the market is bifurcated into hospitals & ASCs, specialty clinics, and others.

The hospitals & ASCs segment dominated the market in 2025. The increasing prevalence of chronic disorders, the rising number of surgical procedures in hospitals, and the growing number of hospitals, among others, are among the crucial factors driving the segment's growth in the market. Furthermore, the segment is set to hold a 74.8% share in 2026.

- For instance, according to 2025 data published by Statistisches Bundesamt, there are about 1,874 hospitals in Germany.

In addition, specialty clinics’ end users are projected to grow at a 7.5% CAGR during the forecast period.

Microelectronic Medical Implants Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Microelectronic Medical Implants Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market held the dominant share in 2024, valued at USD 12.58 billion, and also held the leading share in 2025 with USD 13.32 billion. The growing prevalence of chronic conditions, strong medical device innovation, advanced healthcare infrastructure, high adoption of implantable medical technologies, and strong presence of medical device manufacturers, among others, are some of the factors supporting the growth of the segment in the market.

- For instance, according to 2024 statistics published by the Centers for Disease Control & Prevention (CDC), it was reported that the prevalence of inflammatory bowel disease is estimated between 2.4 and 3.1 million among patients in the U.S.

U.S. Microelectronic Medical Implants Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market is set to hold around USD 12.80 billion in 2026, accounting for roughly 35.3% of global sales.

Europe

Europe is projected to record a growth rate of 5.8% in the coming years, which is the second highest among all regions, and expected to reach a valuation of USD 10.06 billion by 2026. Advanced healthcare systems support the adoption of implants in the region.

U.K Microelectronic Medical Implants Market

The U.K. market in 2026 is estimated at around USD 1.86 billion, representing roughly 5.1% of global revenues.

Germany Microelectronic Medical Implants Market

Germany’s market is projected to reach approximately USD 2.18 billion in 2026, equivalent to around 6.0% of global sales.

Asia Pacific

Asia Pacific is estimated to reach USD 8.70 billion in 2026 and secure the position of the third-largest region in the market. Improving healthcare access and increasing patient awareness are likely to support the growth of the market. In the region, India and China are both estimated to reach USD 1.15 billion and USD 2.74 billion, respectively, in 2026.

Japan Microelectronic Medical Implants Market

The Japan market in 2026 is estimated at around USD 2.08 billion, accounting for roughly 5.7% of global revenues. Japan has historically reported a relatively high prevalence of chronic conditions, with a large number of surgical procedures.

China Microelectronic Medical Implants Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues to be estimated at USD 2.74 billion, representing roughly 7.6% of global sales.

India Microelectronic Medical Implants Market

The India market size in 2026 is estimated at around USD 1.15 billion, accounting for roughly 3.2% of global revenues.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 1.87 billion in 2026. The growth is driven by the growing demand for advanced medical treatments in the region. The Middle East & Africa are expected to grow as investment in healthcare infrastructure increases. In the Middle East & Africa, the GCC is set to reach a value of USD 0.57 billion in 2026.

South Africa Microelectronic Medical Implants Market

The South Africa market is projected to reach around USD 0.32 billion in 2026, representing roughly 0.9% of global revenues.

Competitive Landscape

Key Industry Players

Increasing Product Approvals to Support Key Industry Players’ Dominance

A significant product portfolio, coupled with a strong emphasis on strategic initiatives globally, is one of the prominent factors supporting the dominance of these companies in the market. Medtronic and Abbott are major companies in the market in 2025. Moreover, the growing focus of key companies on product approvals is likely to support the global microelectronic medical implants market.

- For instance, in January 2024, Medtronic received U.S. FDA approval of its Percept RC Deep Brain Stimulation (DBS) system, which includes the Percept PC neurostimulator, BrainSense technology, and SenSight directional leads.

Other key players, including Boston Scientific Corporation, are also growing in the market, primarily due to their increased focus on acquisitions and collaborations among competitors to strengthen their presence.

List of Key Microelectronic Medical Implants Companies Profiled

- Medtronic (U.S.)

- Abbott (U.S.)

- Boston Scientific Corporation (U.S.)

- Cochlear Ltd. (Australia)

- Biotronik (Germany)

- LivaNova PLC (U.K.)

- Zimmer Biomet (U.S.)

- Sonova (Switzerland)

- NeuroPace, Inc. (U.S.)

- MED-EL (Austria)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Nalu Medical, Inc., developed the Nalu micro-Implantable Pulse Generator (mIPG) system, which consists of a fully-featured, battery-free, miniaturized IPG, which is powered by an externally worn Therapy Disc and controlled through a smartphone-based remote control app for spinal cord stimulation (SCS) and peripheral nerve stimulation (PNS) indications.

- September 2025: Medtronic received U.S. FDA approval for its Altaviva implantable tibial nerve neurostimulator for the treatment of urge urinary incontinence (UUI). This helped the company to increase its brand presence.

- July 2025: Cochlear Ltd., launched the First and Only Smart Cochlear Implant System, such as the Cochlear Nucleus Nexa system, with an aim to strengthen its product offerings.

- February 2025: Medtronic, a global player in healthcare technology, received U.S. Food and Drug Administration (FDA) approval of BrainSense Adaptive deep brain stimulation (aDBS) and BrainSense Electrode Identifier (EI).

- July 2024: Biotronik launched Amvia Sky, the Pacemaker Approved for Left Bundle Branch Area Pacing (LBBAP). This helped the company in strengthening its global presence.

- January 2024: Neuralink announced the first implantation of its brain-computer interface into a human to strengthen its product portfolio.

- October 2020: Sonova received FDA approval for its new Naída CI Marvel and Sky CI Marvel sound processors to strengthen its presence in the U.S.

REPORT COVERAGE

The report provides a detailed global microelectronic medical implants market analysis and focuses on key aspects such as leading companies and market segmentation, including product type, application, and end user. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.8% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, Application, End User, and Region |

| By Product Type |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 33.91 billion in 2025 and is projected to reach USD 61.54 billion by 2034.

In 2025, North Americas market value stood at USD 13.32 billion.

Growing at a CAGR of 6.8%, the market will exhibit steady growth over the forecast period.

By product type, the cardiac rhythm management implants segment is the leading segment in this market.

The introduction of novel microelectronic medical implants is one of the major factors driving the markets growth.

Medtronic and Abbott are the major players in the global market.

North America dominated the market share in 2025.

The growing prevalence of chronic disorders, the increasing number of minimally invasive surgical procedures, among others, are some of the crucial factors anticipated to boost the adoption of these products globally.

- 2021-2034

- 2025

- 2021-2024

- 261

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us