Military Cloud Computing Market Size, Share & Industry Analysis, By Deployment (Public Cloud, Private Cloud, Hybrid Cloud, and Community Cloud), By Service Model (Infrastructure-as-a- Service (IaaS), Platform-as-a-Service (PaaS), and Software-as-a-Service (SaaS)), By Application (Data Storage and Management, Command and Control, Collaboration and Information Sharing, Virtual Training and Simulation, Cybersecurity and Threat Intelligence, and Others), By End-user (Army, Navy, Airforce, and Defense & Intelligence Agencies), and Regional Forecast, 2026-2034

MILITARY CLOUD COMPUTING MARKET SIZE AND FUTURE OUTLOOK

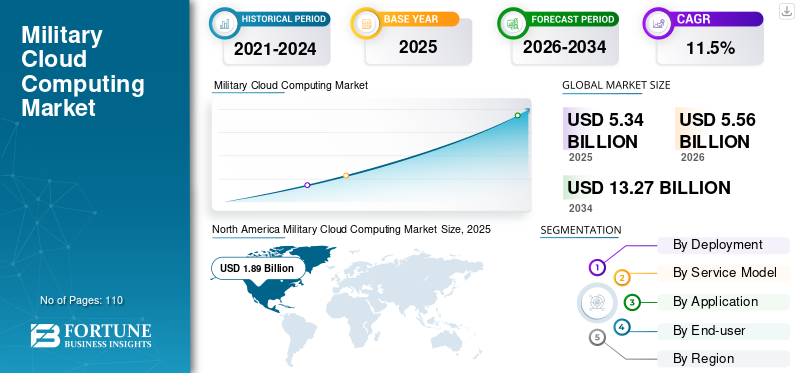

The global military cloud computing market size was valued at USD 5.34 billion in 2025. The market is projected to grow from USD 5.56 billion in 2026 to USD 13.27 billion by 2034, exhibiting a CAGR of 11.5% during the forecast period. North America dominated the military cloud computing market with a market share of 35.39% in 2025.

Military cloud computing platforms are defense-grade digital infrastructures designed to securely store, process, and manage large volumes of military data across centralized, hybrid, and distributed environments. These platforms support mission-critical functions, including command and control, intelligence analysis, mission planning, logistics, and joint operations across multiple domains. Built to meet strict security, sovereignty, and resilience requirements, military cloud environments enable real-time data sharing and decision support even in contested or degraded network conditions.

The increasing shift toward data-centric warfare, multi-domain operations, and AI-driven decision-making is driving demand for secure, scalable, and interoperable military cloud solutions. Defense organizations rely on cloud platforms to integrate data from sensors, ISR assets, and autonomous systems, improving intelligence fusion and situational awareness. Hybrid and sovereign cloud architectures play a critical role by balancing operational flexibility with national control over sensitive defense data.

Key players such as Lockheed Martin, General Dynamics, Microsoft, Google, and BAE Systems are strengthening their positions through technological innovation, strategic partnerships, and investments in AI-enabled cloud capabilities. These efforts aim to deliver defense-specific cloud platforms that meet stringent security, interoperability, and sovereignty requirements while supporting real-time analytics and joint operational needs across military domains.

Download Free sample to learn more about this report.

IMPACT OF GENERATIVE AI

Shifting Demand from Basic Data Hosting Toward AI-Ready Boosts Market Growth

Generative AI is reshaping the military cloud computing market by shifting demand from basic data hosting toward AI-ready, mission-critical cloud infrastructure. Its use in intelligence synthesis, operational scenario generation, and decision-support systems requires high-performance computing, secure data pipelines, and rapid model deployment across centralized and edge environments. This drives investment in specialized military cloud architectures that support trusted AI execution, controlled data access, and real-time integration with command-and-control systems, thereby accelerating both the scale and strategic importance of military cloud adoption.

MILITARY CLOUD COMPUTING MARKET TRENDS

Rising Demand for Sovereign and Nationally Controlled Clouds to Drive Military Cloud Computing Adoption

A significant trend in the military cloud computing market growth is the rising preference for sovereign and nationally controlled cloud environments that ensure full national ownership and control over sensitive defense data. Heightened national security concerns primarily drive this demand, as military data is considered a strategic asset that must be protected from external influence and unauthorized access.

In addition, evolving legal and regulatory frameworks increasingly require defense information to be stored, processed, and managed within national boundaries under domestic jurisdiction. Dependence on foreign-owned infrastructure is also viewed as a strategic risk, particularly in periods of geopolitical tension or conflict. As a result, many defense organizations are investing in domestically hosted or nationally governed cloud platforms that provide greater control, compliance, and operational assurance while still delivering the scalability and flexibility of cloud-based systems.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Complexity of Multi-Domain and Joint Operations Drives Market Growth

Contemporary military operations are increasingly conducted across multiple operational domains, including land, sea, air, cyber, and space, and often involve coordination among different military services and allied nations. This growing operational complexity has significantly increased the demand for interoperable digital systems capable of securely sharing data across organizational, technical, and national boundaries.

- For instance, in July 2025, Danish software company Systematic launched SitaWare BattleCloud, a cloud-based version of its military command-and-control system. Designed for flexibility, mobility, and real-time data access, it draws on lessons from the war in Ukraine to ensure resilience even in unstable conditions.

Traditional, siloed command-and-control and information systems are insufficient to support the scale, speed, and integration required for modern joint operations. Military cloud computing solutions provide a unified digital backbone that enables data fusion, real-time information sharing, and coordinated decision-making across multiple domains and participants. As defense forces place greater emphasis on joint and coalition warfare, the need to manage complexity through secure, scalable, and interoperable cloud-based architectures has become a critical driver for market growth.

MARKET RESTRAINTS

Cyber Threat Concerns to Restrain Market Growth

Security remains one of the most significant restraints for military cloud computing due to the potential risks to national security. Military operations generate highly sensitive data, including real-time battlefield intelligence, satellite imagery, and classified operational plans. Moving such data to cloud platforms, even those that are government-certified or air-gapped, can create vulnerabilities that adversaries may exploit.

- For instance, in March 2023, the U.S. Department of Defense accidentally exposed thousands of sensitive military emails via a misconfigured Microsoft Azure Government cloud server for two weeks. The leak included 3 TB of data from USSOCOM, containing personal, health, and security-clearance information (SF-86 forms), though no classified data.

Cybercriminals actively target defense networks to intercept or manipulate information. Even a minor breach could compromise missions, reveal troop movements, or expose strategic capabilities. These high stakes make defense organizations cautious in adopting cloud solutions, favoring incremental or highly controlled implementation over rapid deployment.

MARKET OPPORTUNITIES

Shift Toward Digital Battlefield Operations to Boost Market Growth

Modern military operations are increasingly centered on digitally enabled battlefields that integrate unmanned systems, networked sensors, real-time surveillance, autonomous platforms, and precision weapons. These systems continuously generate large volumes of structured and unstructured data from multiple operational domains.

Managing and exploiting this data in time-sensitive environments has become a critical operational requirement. Military cloud computing enables real-time data ingestion, fusion, and analysis, allowing commanders to derive actionable intelligence and support faster, more informed decision-making. The market opportunity lies in delivering secure, low-latency cloud platforms that operate across centralized and edge environments, integrate AI and machine learning for advanced analytics, and ensure encrypted, multi-domain access. In this context, cloud solutions move beyond data storage to become core enablers of situational awareness, operational agility, and mission effectiveness.

Segmentation Analysis

By End-user

Army Segment Dominates, Driven by its Ability to Involve Large Troop Deployments

Based on end-user, the market is classified into army, naval, airforce, and defense & intelligence agencies.

Army held the majority share in 2025. In 2026, the segment is anticipated to dominate with a 34.4% as land operations involve large troop deployments, armored vehicles, artillery, and extensive sensor networks that generate massive volumes of data. Real-time command and control, intelligence integration, AI-assisted analytics, and autonomous systems for battlefield operations make cloud computing essential for operational effectiveness. Additionally, armies often receive a larger share of defense modernization budgets, enabling significant investment in scalable, secure, and interoperable cloud infrastructure, thereby reinforcing their leading position relative to the Navy, Air Force, and Defense & Intelligence agencies.

Airforce is expected to witness the highest Compound Annual Growth Rate (CAGR) of 13.4% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

Hybrid Cloud Leads Due to Balanced Security, Flexibility, and Scalability

Based on deployment, the market is divided into public cloud, private cloud, hybrid cloud and community cloud.

Hybrid cloud holds the majority share by deployment in 2024. In 2025, the segment is anticipated to dominate with a 46.0% as it combines the security and control of private clouds with the scalability and flexibility of public clouds. Defense organizations require highly secure environments for sensitive data while also needing the ability to scale resources quickly for intelligence processing, mission simulations, and multi-domain operations. Hybrid architectures allow militaries to maintain critical workloads on private, sovereign clouds while leveraging public cloud resources for non-sensitive applications, AI/ML analytics, and large-scale data processing.

Community cloud is expected to witness the highest Compound Annual Growth Rate (CAGR) of 18.6% during the forecast period.

By Service Model

IaaS Segment Dominates due to its ability to Support Diverse Workloads

Based on service model, the market is categorized into infrastructure-as-a-service (IaaS), platform-as-a-service (PaaS), and software-as-a-service (SaaS).

Infrastructure-as-a-service (IaaS) holds the majority share of the market in 2025. In 2026, the segment is anticipated to dominate with a 49.0% share as defense organizations prioritize flexible, scalable, and secure computing infrastructure to support diverse workloads, including mission-critical applications, AI/ML analytics, and data storage. IaaS provides complete control over virtualized computing resources while enabling militaries to deploy, manage, and scale applications to meet operational needs.

Platform-as-a-service (PaaS) is expected to witness the highest Compound Annual Growth Rate (CAGR) of 14.3% during the forecast period.

By Application

Data Storage and Management Segment Dominated due to its Ability to Generate Massive Volumes of Structured and Unstructured Data from Sensors

Based on application, the market is segmented into data storage and management, command and control, collaboration and information sharing, virtual training and simulation, cybersecurity and threat intelligence, and others.

Data storage and management held the majority share in 2025. In 2026, the segment is anticipated to dominate with a 27.7% as modern defense operations generate massive volumes of structured and unstructured data from sensors, ISR platforms, autonomous systems, and multi-domain operations. Efficient storage, retrieval, and management of this data are critical for real-time analytics, decision support, and mission planning. Military cloud platforms enable secure, scalable, and resilient storage solutions that ensure rapid access to operational data while maintaining strict compliance with defense security and sovereignty requirements. This fundamental role of cloud-based data management underpins nearly all other military applications, making it the largest application segment in the market.

The cybersecurity and threat intelligence segment is expected to witness the highest compound annual growth rate (CAGR) of 16.3% during the forecast period.

By geography, the market is categorized into North America, South America, Europe, the Middle East & Africa, and Asia Pacific.

MILITARY CLOUD COMPUTING MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Military Cloud Computing Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America holds the majority of the military cloud computing market share due to its advanced defense infrastructure, substantial defense budgets, and early adoption of cloud technologies for military operations. The U.S., in particular, is investing heavily in digital transformation initiatives to modernize its armed forces, integrate multi-domain operations, and deploy AI-driven decision-support systems.

The region also benefits from a concentration of leading defense contractors and cloud technology providers, such as Lockheed Martin, Microsoft, AWS, and Raytheon, which actively develop and deploy cloud platforms tailored for mission-critical applications. Additionally, North American militaries emphasize sovereign and secure cloud environments to maintain control over sensitive data, enabling large-scale adoption of hybrid and private cloud solutions.

North American market held the largest market at USD 1.89 billion in 2025.

U.S. Military Cloud Computing Market

Given North America’s strong contribution and the U.S. dominance in the region, the U.S. market can be estimated at around USD 1.71 billion in 2025, accounting for roughly 32.1% of sales.

Europe

Europe is projected to grow at a CAGR of 12.1% over the coming years, reaching a valuation of USD 1.49 billion in 2025. This growth is driven by increased defense modernization programs, increased focus on multi-domain interoperability, and rising investment in AI and autonomous systems across NATO and EU member states. Many European nations are upgrading legacy defense infrastructure while adhering to strict data sovereignty and security regulations, which drives demand for secure, sovereign cloud solutions. Additionally, growing collaboration between national militaries and private technology providers is accelerating the deployment of hybrid and AI-enabled cloud platforms to support intelligence analysis, command and control, and joint operations.

U.K Military Cloud Computing Market

The U.K. market in 2025 reached around USD 0.17 billion, representing roughly 3.2% of global revenues.

Germany Military Cloud Computing Market

Germany’s market reached approximately USD 0.18 billion in 2025, equivalent to around 3.4% of global sales.

Asia Pacific

Asia Pacific is expected to grow at the highest CAGR and reach a valuation of USD 1.25 billion in 2025, driven by a unique combination of rapid defense modernization, regional security pressures, and emerging technological partnerships. Nations such as India, Japan, South Korea, and Australia are simultaneously expanding land, naval, and air capabilities while investing in data-driven battlefield management, autonomous systems, and AI-enabled ISR networks. Unlike North America and Europe, many Asia-Pacific countries are leapfrogging legacy IT systems by adopting cloud-native architectures to accelerate deployments and reduce reliance on fragmented, on-premises networks. Geopolitical tensions in the South China Sea, along the Eastern India border, and in the Indo-Pacific theater are prompting militaries to deploy secure, multi-domain cloud platforms for real-time intelligence sharing and rapid coalition coordination, further driving adoption.

Japan Military Cloud Computing Market

The Japanese market in 2025 stood at around USD 0.13 billion, accounting for roughly 2.4% of global revenues.

China Military Cloud Computing Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues estimated at around USD 0.45 billion, representing roughly 8.4% of global sales.

India Military Cloud Computing Market

The Indian market in 2025 stood at around USD 0.19 billion, accounting for roughly 3.6% of the global market share.

South America and Middle East & Africa

The Middle East and Africa region is expected to grow at the second-highest CAGR in the market during the study period. It is due to rapid military digitalization driven by regional security pressures, modernized defense procurement, and investments in AI-enabled cloud platforms for real-time surveillance and multi-domain coordination. Nations such as the UAE, Saudi Arabia, and Egypt are prioritizing sovereign and hybrid cloud architectures to maintain control over sensitive defense data while supporting intelligence fusion, mission planning, and autonomous operations. Partnerships with global cloud and defense technology providers are accelerating deployment, making this region a key emerging market.

South America is expected to grow at a stable CAGR in the market, driven by gradual defense modernization and selective adoption of cloud-based systems for intelligence, logistics, and mission planning, driven by partnerships with global technology providers and budget-conscious defense planning.

GCC Military Cloud Computing Market

The GCC market reached around USD 0.18 billion in 2025, representing roughly 3.4% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Market Players Implement Strategic Initiatives to Expand Their Technological Capabilities

Market players are expanding their cloud computing portfolios to meet the growing demand for low-latency, secure, and AI-enabled battlefield solutions. They are implementing various strategic initiatives, such as partnerships, joint ventures, and acquisitions, to expand their technological capabilities and global presence.

LIST OF KEY MILITARY CLOUD COMPUTING COMPANIES PROFILED

- Amazon Web Services (U.S.)

- Microsoft Corporation (U.S.)

- Google LLC (U.S.)

- Oracle Corporation (U.S.)

- IBM Corporation (U.S.)

- Cisco Systems, Inc. (U.S.)

- Dell Technologies Inc. (U.S.)

- VMware, Inc. (U.S.)

- Atos SE (France)

- BAE Systems (U.K.)

- General Dynamics Corporation (U.S.)

- Lockheed Corporation (U.S.)

- Leidos Holdings, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: The U.S. Air Force awarded Amazon Web Services a USD 581.3 million contract to continue operating Cloud One, its enterprise military cloud platform, through 2028. The award highlights the Pentagon’s continued shift toward secure, scalable cloud computing to support command-and-control, logistics, weapons systems, and data-driven operations across the Air Force.

- January 2026: Microsoft won a USD 170.4 million contract from the U.S. Air Force to provide cloud computing services for the Cloud One program through 2028. The sole source award reinforces Microsoft Azure’s role in supporting secure military cloud infrastructure and defense digital modernization.

- December 2025: The U.S. Department of Defense awarded Hewlett Packard Enterprise a 10-year, USD 931 million contract to modernize DISA’s most sensitive data centers with a hybrid on-premises cloud platform. Using HPE GreenLake, the DoD aims to deliver public cloud-style capabilities such as unified management, multitenancy, AI, and zero-trust security while keeping classified data fully controlled and isolated.

- November 2025: Google Cloud won a new NATO contract to provide secure, isolated cloud services for military use. The exact value of the deal was not disclosed, but NATO described it as a multimillion-pound contract. The cloud system would support classified data, along with AI and analytics, as part of NATO’s broader move toward secure, sovereign military cloud infrastructure.

- April 2025: Oracle received a task order under the U.S. Department of Defense’s Joint Warfighting Cloud Capability contract to provide the U.S. Army’s Enterprise Cloud Management Agency with secure multicloud compute and storage services. The Oracle Defense Cloud will support multiple security levels, enable Army digital modernization, reduce costs, and provide advanced AI, analytics, and Oracle-specific workloads while keeping sensitive data isolated and secure.

- March 2025: Oracle announced that provide air-gapped, isolated cloud and AI services to Singapore’s military and defense ministry, marking its first defense cloud deal in Southeast Asia. The system will operate offline from the public internet, enabling secure AI-driven video, imagery, and data analysis for classified military networks amid rising cyber threats in the region.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 11.5% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Deployment, Service Model, Application, End-user, and Region |

| By Deployment |

|

| By Service Model |

|

| By Application |

|

| By End-user |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 5.33 billion in 2025 and is projected to reach USD 13.27 billion by 2034.

In 2025, the market value stood at USD 1.89 billion.

The market is expected to exhibit a CAGR of 11.5% during the forecast period (2026-2034).

By end-user, army segment is expected to lead the market.

The increasing complexity of multi-domain and joint operations is the key factor driving market growth.

Lockheed Martin, General Dynamics, Microsoft, Google, and BAE Systems are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 110

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us