Military Multirole Aircraft Market Size, Share, & Industry Analysis, By Aircraft Types (Manned (Crewed) Aircraft, Unmanned Aircraft, and Optionally Piloted Vehicles (OPV)), By Generation (Legacy Platforms, 4th, 4.5th, 5th, & 6th Generation), By Weight Class (Light, Medium, & Heavy Fighters), By Technology (Stealth, Avionics & Sensor Fusion, Electronic Warfare Suites, Radars, & Others), By Propulsion Types (Turbofan, Turboprop/Propeller, and Hybrid-Electric Propulsion), By Procurement Type (New-Build Acquisition, Upgrade/Retrofit Programs, & Others), By Range, and Regional Forecast 2026-2034

KEY MARKET INSIGHTS

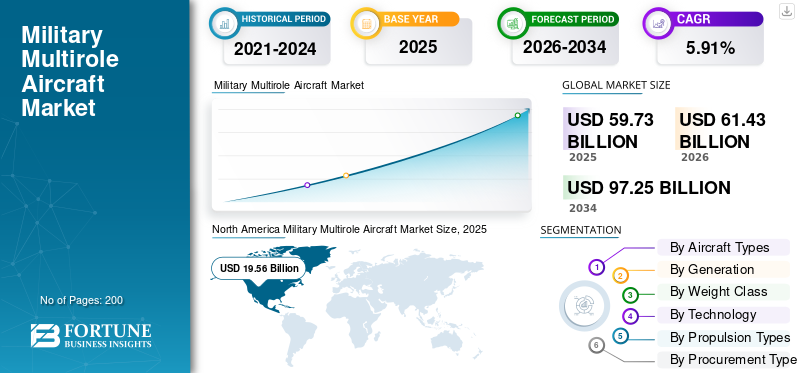

The global military multirole aircraft market size was valued at USD 59.73 billion in 2025. The market is projected to grow from USD 61.43 billion in 2026 to USD 97.25 billion by 2034, exhibiting a CAGR of 5.91% during the forecast period. North America dominated the global market with a market share of 32.74% in 2025.

Military multirole aircraft and multirole fighter aircraft represent a revolutionary type of military airpower development, designed to carry out various mission tasks without requiring specialization in specific military platforms. Military multirole aircraft are designed to perform a range of military tasks, such as air-to-air combat missions, air-to-ground attack missions, air reconnaissance missions, electronic warfare missions, SEAD missions, CAS missions, and air interdiction missions in one military platform.

The market growth is driven by a series of mutually complementary dynamics, the first and foremost of which are the increasing levels of geopolitical tensions, growing defense budgets, regional security risks, and the need for a military overhaul to address emerging threats. The growing global expenditure on the military, especially due to the ongoing Ukrainian crisis, South China Sea disputes, Taiwanese Strait, and Indo-Pacific territorial claims, has placed a special focus on the development of advanced airpower.

The military multirole aircraft industry has moderate to intense fragmentation, with major market leaders such as Lockheed Martin (U.S.), followed by Boeing (U.S.), and BAE Systems (U.K.), and others such as Dassault Aviation (Rafale), Saab AB (Gripen), and Hindustan Aeronautics Limited (India), Korea Aerospace Industries (South Korea), and others.

Download Free sample to learn more about this report.

Military Multirole Aircraft Market Key Takeaways

- 2025 Market Size: USD 59.73 billion

- 2026 Market Size: USD 61.43 billion

- 2034 Forecast Market Size: USD 97.25 billion

- CAGR: 5.91% from 2026–2034

- North America dominated the market with a 32.74% share in 2025.

- Manned (Crewed) Aircraft held the largest market share with 61.70% in 2025.

- Medium-Range (1000km–2500km) segment accounted for the largest market share with 61.70% in 2025.

North America

The market reached USD 19.56 billion in 2025, driven by fleet modernization and strong defense spending.

Asia Pacific

The market reached USD 17.26 billion in 2025, supported by rising defense budgets and military expansion.

Europe

The market reached USD 13.47 billion in 2025, fueled by NATO modernization and aircraft replacement programs.

U.S.

The market reached USD 18.47 billion in 2025, driven by F-35 procurement and advanced air combat programs.

Japan

Rising investments in next-generation fighter aircraft and regional security continue to support market growth.

Read More

Military Multirole Aircraft Market Trends

Stealth Technology and Low Observable Design Evolution Emerges as a Key Market Trend

Fifth- and sixth-generation stealth technologies, with their use of radar-absorbent materials, platform alignment, internal weapons carriage, serpentine air intakes, and thermal signature management, offer distinct advantages in contested airspace environments. The march toward sixth-generation platforms through projects such as the U.S. Next Generation Air Dominance, Japan's Global Combat Air Programme, and a host of Chinese multiple tailless stealth prototypes unveiled in August 2025 will merge stealth with drone teaming, artificial intelligence, directed energy weapons, and advanced electronic warfare capabilities, fundamentally resetting air combat paradigms beyond today's benchmark for fifth-generation aircraft.

Market Dynamics

Market Drivers

Technological Advancement and Combat Effectiveness Optimization Drives the Market Growth

Leaps in stealth technology, AI, sensor fusion, and network-centric warfare solutions have fueled the drive toward multirole aircraft and multi-domain dominance. For instance, in May 2025, Saab marked a significant milestone by achieving flights one through three, incorporating its AI agent Centaur, developed by Helsing, into its Gripen E fighter jets. This indicates that fighter jets designed for production can incorporate AI solutions, as has been demonstrated in lab setups.

Download Free sample to learn more about this report.

Market Restraints

Stringent ITAR Compliance and Technology Transfer Limits Restrict the Market Growth

Export control regulations such as ITAR often have steep compliance burdens, restrict the transfer of technology, make global cooperation complicated, and limit market entry options for defense and aerospace manufacturers. The ITAR, an export control regulation administered by the U.S. Department of State’s Directorate of Defense Trade Controls, governs the transfer of U.S. defense-related articles, services, and technical data listed on the United States Munitions List to persons in the U.S. unless a licensure exception is granted. This regulation carries severe penalties, including fines, export restrictions, and imprisonment, due to the sensitive nature of the materials. This restrains the military multirole aircraft market growth.

Market Opportunities

Autonomous and Unmanned Combat Aerial Vehicle Integration Catalyze the Future Opportunity Growth

The convergence of Artificial Intelligence, Autonomous Systems, and Manned-Unmanned Teaming is revolutionizing combat aviation and force structures. The United States Air Force’s Collaborative Combat Aircraft vision envisions approximately 1,000 autonomous air platforms, indicating that this represents about two unmanned aircraft for each next-generation crewed fighter. Development contracts in the initial tranche have already been awarded to General Atomics and Anduril, and more than USD 8.9 billion is being directed over the budget years 2025 through 2029, with production decisions forecasted in budget year 2026.

Market Challenges

Skilled Workforce Shortages and Weak Talent Pipelines Creates a Market Challenge

Skilled workforce shortages in the aerospace and defense industry are at a fever pitch, driven by demographic shifts, inadequate pipelines of talent, and poor retention strategies that have compromised production capacity and hindered technological innovation. According to a study conducted by the Aerospace Industries Association, 56 percent of companies struggle to find skilled manufacturing workers despite the sector growing nearly 5 percent annually. Factors contributing to this issue include poor workforce planning, reliance on referral-based recruitment that favors "ready-to-go" candidates, and a mismatch between academia and industry in terms of required skills. Additionally, underinvestment in onboarding, career development, and up skilling contributes to high turnover at an early stage and increases recruitment costs.

SEGMENTATION ANALYSIS

By Aircraft Types

Shift to Autonomous, Cost-Effective Air Combat Drives Unmanned Aircraft Segment Growth

Based on aircraft types, the market is divided into manned (crewed) aircraft, unmanned aircraft, and Optionally Piloted Vehicles (OPV).

Unmanned aircraft segment is estimated to be the fastest growing during the forecast period, as defense forces transition from a pilot-centric to a system-centric structure, where unmanned aircraft are utilized to leverage mass, persistence, and presence in high-threat skies cost-effectively. The development is substantiated by three key drivers: breakthroughs in artificial autonomy, a need to mitigate risks to pilots, and political momentum to acquire affordable platforms on a large scale that are far less costly than manned platforms.

The manned (crewed) aircraft sub-segment accounted for the largest market share of 61.70% in 2025 and is estimated to grow at a CAGR of 6.10% during the forecast period.

By Generation

Strategic Interoperability and Alliance Integration Drive the 5th Generation Segmental Growth

Based on generation, the market is divided into Legacy Platforms, 4th Generation, 4.5 Generation, 5th Generation, and 6th Generation.

The 5th generation segment is projected to be the fastest growth in the industry, which is stimulated mainly by the need for Coalition Interoperability between allies in NATO. The major countries are thinking beyond plane interoperability to consider these planes as nodes in the same battle cloud. This directly results in the need for the normalization of 5th generation planes, such as the F-35 to share data seamlessly.

- For instance, in November 2024, Romania codified this shift in strategy through a Letter of Offer and Acceptance (LOA) for the purchase of 32 F-35A Lightning II jets, with an estimated cost of around USD 6.4 billion. Romania will become the 20th member of the global partnership of nations operating F-35 fighter jets, with deliveries expected to begin in 2031. The focus will be on replacing old stocks to ensure compatibility with NATO’s overall defense framework for the eastern flank.

The 4.5 generation segment accounted for the largest market share of 40.13% in 2025 and grow at a CAGR of 6.30% during the forecast period.

By Weight Class

Strategic Balance of Capability and Affordability Propel the Medium Fighters Segment Growth

Based on weight class, the market is divided into light fighters, medium fighters, and heavy fighters.

The medium fighters segment is projected to be the fastest growing with the highest CAGR of 6.50% during the forecast period, and accounted for the largest market share of 50.83% in 2025. The growth is driven by its sweet spot for today’s air forces, providing 80% of the capabilities of the heavy air superiority aircraft at only 50% of the price tag. This category of aircraft has matured from lightweight point-defense interceptors to multi-role aircraft that possess the ability to carry substantial payloads (missiles and precision-guided munitions) over extended ranges.

- For instance, in June 2025, South Korea's Defense Acquisition Program Administration signed a follow-on contract worth USD 1.7 billion. This contract further hastened the induction of 4.5-generation, light-weight, stealth fighter. The market's burning demand for such affordably priced, high-quality replacements for heavy, costly options such as F-15 or Su-57, was successfully fulfilled in the first procurement order placed in 2024 for this aircraft model.

The heavy fighters segment accounted for the second largest market share of 31.63% in 2025 and is expected to grow at a CAGR of 4.62% during the forecast period.

By Technology

AI and Autonomy Integration Segment Dominates Due to Cost-Efficient Collaborative Combat and Autonomous Wingmen Adoption

Based on technology, the market is divided into stealth, avionics & sensor fusion, electronic warfare suites, radars, network-centric data links, AI and autonomy integration, and others.

The AI and autonomy integration segment is projected to grow at the highest CAGR of 8.64% during the forecast period. The segment is expanding rapidly as air forces transition from pilot-centric operations to collaborative combat architectures. This growth is driven by an operational necessity to break the cost curve of traditional air power, where fighter jets are too expensive to risk in large numbers by pairing them with affordable, autonomous wingmen.

- For instance, in August 2025, Shield AI announced the operational deployment of its V-BAT autonomous UAS in Europe under a new contract with Frontex and Global Sat Tech, following a major USD 198 million contract awarded by the U.S.

The stealth sub-segment accounted for the second largest market share of 20.74% in 2025 and is estimated to grow at a CAGR of 4.29% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Propulsion Types

Hybrid-Electric Propulsion Segment Dominates Due to Rising Onboard Power Demands Outpacing Conventional Engine Capabilities

Based on propulsion types, the market is divided into turbofan, turboprop/propeller, and hybrid-electric propulsion.

The hybrid-electric propulsion segment is estimated to be the fastest growing, with the highest CAGR of 9.66% during the forecast period. The growth is driven by the ever-growing power requirements of 6th-generation avionics, laser-based directed energy weapons, and powerful electronic warfare systems. Conventional jet engines are unable to meet both thrust and enormous electrical demand simultaneously without sacrificing performance.

- For instance, in October 2025, a framework agreement worth approximately USD 315 million was signed by Rolls-Royce and the Indian government to develop electric propulsion systems, which will be primarily used in the maritime domain but also have derivative applications for aerial vehicles.

The turbofan sub-segment accounted for the largest market share of 92.09% in 2025 and is anticipated to grow at a CAGR of 4.29%

By Procurement Type

Generational Aircraft Retirements and Evolving Threat Environments Drives New-Build Acquisition Segment Growth

Based on procurement type, the market is divided into new-build acquisition, upgrade/retrofit programs, and MRO & sustainment

The new-build acquisition segment is estimated to be the fastest growing during the forecast period, with the highest CAGR of 6.87% and a share of 40.27% in 2025. This trend arises out of a global phenomenon of generational replacements, in which the air forces are retiring old era aircraft. Anything added to these old-generation aircraft will not be able to fill the gap generated by modern threats; rather, new-build, radars-on, and sensors-on aircraft will be necessary to survive in a 2030+ battlespace. As a result, defense spending will remain overwhelmingly focused on acquiring entirely new aircraft to replace existing ones and augment forces.

- For instance, in September 2025, India's Ministry of Defence signed a historic contract worth USD 7.5 billion with Hindustan Aeronautics Limited (HAL) for the purchase of 97 new Tejas Mk1A jets.

The MRO & sustainment sub-segment is accounted for the second largest global military multirole aircraft market share of 35.61% in 2025 and is estimated to grow with a CAGR of 4.55% during the forecast period.

By Range

Stand-off Warfare Requirements and Extended Capabilities Beyond Advanced Air Defenses Drives Long-Range Segment Growth

Based on range, the market is divided into Short-Range (Tactical) Upto 1000km, Medium-Range 1000km to 2500km, and Long-Range (Strategic) Above 2500 km.

The long-range (strategic) above 2500km segment is estimated to be the fastest growing with the highest CAGR of 6.68% during the forecast period. The growth is spurred by the revolution in combat strategy based on the principle of stand-off dominance. As the enemy expands their defensive cruising altitude with long range SAMs such as the S-500 or HQ-9 missiles, an increased need for combat planes with the range to strike targets well beyond the kill zone regions, and the need for more heavies with fuel capacity for the new hypersonic missiles, and the absence of aerial tankers in those regions drives the market growth.

- For instance, in December 2025, Dassault unveiled the Super Rafale vision of the Rafale F5, confirming the strategic stealth penetration aircraft. The F5 model has been specifically developed for nuclear deterrence and long-range interception and incorporates the ASN4G nuclear hypersonic missile and loyal wingmen drones.

The medium-range 1000km to 2500km accounted for the largest market share of 61.70% in 2025 and is estimated to grow with a CAGR of 6.10% during the forecast period.

Military Multirole Aircraft Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, the Middle East & Africa and Latin America

North America

North America Military Multirole Aircraft Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2025, valued at USD 19.56 billion, and is expected to maintain its leading share in 2026, with USD 19.88 billion. North America, especially U.S. defense budgets exceeding USD 255 billion annually, F-35 procurement, fleet modernization, advanced multi-role capabilities for air superiority and ISR activities catalyze the regional growth. North America sustains dominance through an unmatched procurement scale, as witnessed in the F-35 program.

U.S. Military multirole aircraft Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 18.47 billion in 2025, and estimated growth rate of 4.45% during the forecast period.

Asia Pacific

Asia Pacific is projected to record a growth rate of 7.10% in the coming years, which is the second largest among all regions and reached a valuation of USD 17.26 billion in 2025, increasing to USD 31.09 billion by 2034. Asia Pacific market growth is driven by rapid naval and air force expansions amid South China Sea disputes and rising budgets in China, India, and Japan.

China Military multirole aircraft Market

The China Military multirole aircraft market in 2025 reached a valuation of USD 7.14 billion, representing growth rate of 6.15% during the forecast period.

India Military multirole aircraft Market

The India Military multirole aircraft market in 2025 reached the valuation of USD 3.76 billion, representing growth rate of 9.12% during the forecast period.

South Korea Military multirole aircraft Market

The South Korea Military multirole aircraft market in 2025 recorded the valuation of USD 1.63 billion, representing growth rate of 5.27% during the forecast period.

Europe

Europe is projected to record a growth rate of 6.86% in the coming years, which is the second largest among all regions and reached a valuation of USD 13.47 billion in 2025 increasing to USD 23.77 billion by 2034. Europe’s NATO commitments, fleet replacements, and modernization of fixed wing aircraft (Eurofighter, Rafale), rotorcraft, and modernization amid security threats drive the regional growth.

U.K. Military multirole aircraft Market

The U.K. Military multirole aircraft market in 2025 recorded the valuation of USD 2.11 billion, representing growth rate of 4.62% during the forecast period.

Germany Military multirole aircraft Market

The U.K. Military multirole aircraft market in 2025 recorded the valuation of USD 2.45 billion, representing growth rate of 4.62% during the forecast period.

Eastern Europe Military multirole aircraft Market

The Eastern Europe Military multirole aircraft market in 2025 reached USD 4.36 billion as its valuation, representing growth rate of 9.50% during the forecast period.

Middle East & Africa and Latin America

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Middle East & Africa market recorded the valuation of USD 6.73 billion in 2025.

Saudi Arabia Military multirole aircraft Market

The Saudi Arabia military multirole aircraft market in 2025 reached the valuation of USD 1.67 billion, representing growth rate of 6.30% during the forecast period.

COMPETITIVE LANDSCAPE

Growing Advance Technology Structure and Competitive Rivalry Propel the Market Growth

Key Market Players

The global military multirole aircraft market is characterized by an oligopoly, intense rivalry, and high barriers to entry. This is further exaggerated by geopolitical alliances that distort the market structure. Competition will be driven by price, performance levels, as well as strategic alignment and industrial sovereignty. The three tiers are, namely: The Global Dominant Tier, dominated by stealth platforms in their 5th generation; the Established Sovereign Tier, consisting of highly capable 4.5-generation platforms that offer strategic independence; and the Emerging Indigenous Tier, comprising new entrants in the market who emphasize cost-efficiency and regional autonomy.

The competitive dynamic is increasingly changing from a pure "performance shootout" to a complex negotiation of technology transfer and supply chain localization. Established Western OEMs are increasingly forced to compete on the capability of their airframes and their willingness to share intellectual property and build local manufacturing ecosystems in buyer nations. This trend has diluted the traditional monopoly of the U.S. and European giants, creating openings for new players from South Korea, Turkey, and India to capture market share in the "value" segment of the fighter market.

LIST OF KEY MILITARY MULTIROLE AIRCRAFT COMPANIES PROFILED

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- BAE Systems plc (U.K.)

- Dassault Aviation S.A. (France)

- Saab AB (Sweden)

- Leonardo S.p.A. (Italy)

- Sukhoi Company (PJSC Sukhoi) (Russia)

- United Aircraft Corporation (UAC) (Russia)

- Chengdu Aircraft Industry Group (AVIC) (China)

- Hindustan Aeronautics Limited (HAL) (India)

- Israel Aerospace Industries (IAI) (Israel)

- Korea Aerospace Industries (KAI) (South Korea)

- Mitsubishi Heavy Industries (Japan)

- Turkish Aerospace Industries (TUSAŞ) (Turkey)

- Embraer S.A. (Brazil)

KEY DEVELOPMENT

- December 2025: - The United States Department of War declared the signing of an additional contract with Lockheed Martin to supply logistics support services for the worldwide fleet of multirole combat jets from the F-35 Lightning II series.

- December 2025: - The Ministry of Defence in Spain selected Airbus Defence and Space to lead the creation and execution of the Integrated Training System for the Spanish Air and Space Force.

- December 2025: - The Government of Canada selected domestically produced jets to improve its multi-purpose air transport capabilities, which include medical evacuations, disaster response, humanitarian assistance, and national security missions.

- December 2025: - Egypt received three more Rafale fighter jets from France, designated as EM12, EM13, and EM14. This acquisition bolsters Cairo's continuous efforts to modernize its air force and builds upon its 2021 contract for 30 jets.

- October 2025: - An officer from Bangladesh's air force stated that the interim government of the country granted initial approval for the acquisition of multirole combat aircraft capabilities and attack aircraft, along with new surface-to-air missiles and long-range radar systems.

REPORT COVERAGE

The global military multirole aircraft market growth analysis includes a comprehensive study of the market size and forecast for all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advances, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers, and acquisitions, as well as key Military multirole aircraft industry developments and prevalence by key regions. The global market research report also provides a depth competitive landscape with information on the market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.91% from 2026-2034 |

|

Unit |

USD Billion |

|

Segmentation |

By Aircraft Types · Manned (Crewed) Aircraft · Unmanned Aircraft · Optionally Piloted Vehicles (OPV) By Generation · Legacy Platforms · 4th Generation · 4.5 Generation · 5th Generation · 6th Generation By Weight Class · Light Fighters · Medium Fighters · Heavy Fighters By Technology · Stealth · Avionics & Sensor Fusion · Electronic Warfare Suites · Radars · Network-Centric Data Links · AI and Autonomy Integration · Others By Propulsion Types · Turbofan · Turboprop/Propeller · Hybrid-Electric Propulsion By Procurement Type · New-Build Acquisition · Upgrade/Retrofit Programs · MRO & Sustainment By Range · Short-Range (Tactical) Upto 1000km · Medium-Range 1000km to 2500km · Long-Range (Strategic) Above 2500 km By Geographic North America (By Aircraft Types, By Generation, By Weight Class, By Technology, By Propulsion Types, By Procurement Type, By Range, By Country) · U.S. (By Aircraft Types) · Canada (By Aircraft Types) Europe (By Aircraft Types, By Generation, By Weight Class, By Technology, By Propulsion Types, By Procurement Type, By Range, By Country) · U.K. (By Aircraft Types) · Germany (By Aircraft Types) · France (By Aircraft Types) · Nordic Countries (By Aircraft Types) · Eastern Countries (By Aircraft Types) · Rest of Europe (By Aircraft Types) Asia Pacific (By Aircraft Types, By Generation, By Weight Class, By Technology, By Propulsion Types, By Procurement Type, By Range, By Country) · China (By Aircraft Types) · India (By Aircraft Types) · Japan (By Aircraft Types) · South Korea (By Aircraft Types) · Australia (By Aircraft Types) · Rest of Asia Pacific (By Aircraft Types) Middle East & Africa (By Aircraft Types, By Generation, By Weight Class, By Technology, By Propulsion Types, By Procurement Type, By Range, By Country) · Israel (By Aircraft Types) · Iran (By Aircraft Types) · Saudi Arabia (By Aircraft Types) · Turkey (By Aircraft Types) · South Africa (By Aircraft Types) · Rest of the Middle East & Africa (By Aircraft Types) Latin America (By Aircraft Types, By Generation, By Weight Class, By Technology, By Propulsion Types, By Procurement Type, By Range, By Country) · Brazil (By Aircraft Types) · Argentina (By Aircraft Types) Rest of Latin America (By Aircraft Types) |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 59.73 billion in 2025 and is projected to reach USD 97.25 billion by in 2034.

In 2025, the Europe market value stood at USD 13.47 billion.

The market is expected to exhibit a CAGR of 5.91% during the forecast period of 2026-2034.

The long-range (strategic) above 2500km segment is expected to lead the market.

Technological advancement and combat effectiveness optimization are the key factors driving the market.

Lockheed Martin (U.S.), followed by Boeing (U.S.), and BAE Systems (U.K.), and others like Dassault Aviation (Rafale), Saab AB (Gripen), and Hindustan Aeronautics Limited (India), Korea Aerospace Industries (South Korea), and others.

North America dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us