Military Vehicle Electrification Market, Size, Share and Industry Analysis, By Platform (Ground Combat Vehicles, Tactical Wheeled Vehicles, Logistics & Support Vehicles, Special Mission Vehicles, & UGV/ROV), By Propulsion Type (IC Engine, Drive Configuration, Electric Drive Layout, and Transmission / Gear Solutions), By Systems (Power Generation, Cooling System, Energy Storage, & Others), By Technology (Conventional, Micro/Mild Hybrid, Full Hybrid, PHEV, BEV, FCEV, and Hybrid Fuel-Cell), By Installation Type (New-Build and Retrofit/Upgrade), By Voltage Type, and Regional Forecast 2026-2034

Military Vehicle Electrification Market Size and Future Outlook

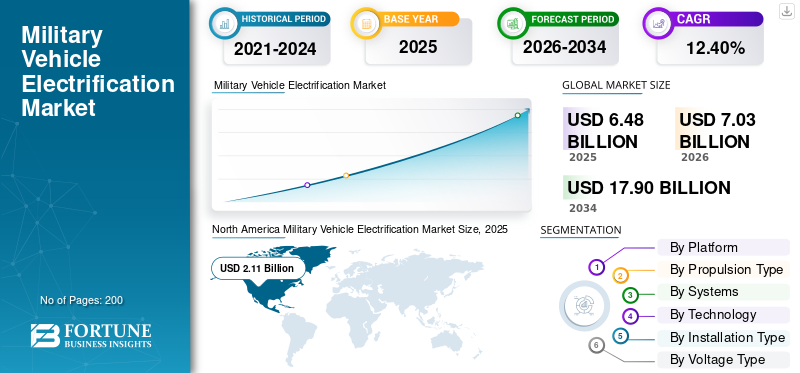

The global military vehicle electrification market size was valued at USD 6.48 billion in 2025. The market is projected to grow from USD 7.03 billion in 2026 to USD 17.90 billion by 2034, exhibiting a CAGR of 12.40% during the forecast period. North America dominated the global military vehicle electrification market with a market share of 32.56% in 2025.

The military vehicle electrification market refers to the fusion of electrified propulsion, hybrids, advanced battery storage, and onboard power sourcing for use in a broad range of military vehicles. This includes battle-ready vehicles such as tanks and infantry fighting vehicles, as well as logistics and support vehicles, light-duty tactical wheeled vehicles, and unmanned armored vehicles.

The growth in the defense sector is quite prominent as the defense forces across the globe are promoting the modernization of defense systems. The governments and defense sectors are investing heavily in upgrading their vehicles with the latest electrification technology.

Major players that are seeking niche electric solutions for various platforms and geographies are BAE Systems, Oshkosh Defense, General Dynamics, Leonardo S.p.A., Krauss-Maffei Wegmann, Textron, QinetiQ Group, Nexter Group, and General Motors Defense.

Download Free sample to learn more about this report.

MILITARY VEHICLE ELECTRIFICATION MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 6.48 Billion

- 2026 Market Size: USD 7.03 Billion

- 2034 Forecast Market Size: USD 17.90 Billion

- CAGR: 12.40% from 2026–2034

- North America dominated the military vehicle electrification market with a 32.56% share in 2025.

- The electric drive layout sub-segment held the largest market share of 32.39% in 2025.

- The energy storage sub-segment accounted for a leading 28.71% market share in 2025.

North America

North America led the global market in 2025, supported by strong defense modernization programs and increasing investments in electrified military platforms.

Europe

Europe is projected to be the fastest-growing regional market through 2034, driven by fleet modernization initiatives and heightened security concerns across the region.

Asia Pacific

Asia Pacific emerged as the third-largest regional market in 2025, benefiting from growing defense spending and expanding adoption of electric unmanned ground vehicles.

U.S.

The market was valued at approximately USD 2.01 billion in 2025, supported by advanced defense electrification programs and sustained military technology investments.

Japan

The market is expected to expand at a CAGR of 14.53% through 2034, driven by defense modernization efforts and increasing focus on energy-efficient military mobility solutions.

Read More

Military Vehicle Electrification Market Trend

Series Hybrid Architecture Operate at Optimal Power Ratings Fuels the Market Trend

Series hybrid architecture is currently the most popular method for the electrification of future military vehicles. In this hybrid architecture, diesel or alternative fuel-powered engines operate at optimal power ratings mainly for the production of electricity, which is used for powering electric motors.

This is because of the engineering trade-offs involved in the choice, and the fact that series hybrids allow for an increase in fuel economy of between 20 and 35 percent over non-hybrid designs, and that they do not have to be tied into charging infrastructure that might be nonexistent in the deployment region in the event of contested or hard-to-reach areas.

Download Free sample to learn more about this report.

Market Dynamics

MARKET DRIVER

Technological Advancement in Energy Storage and Power Systems Drives the Market Growth

Rapid advancements in battery research and power electronics are causing a transformation in how military transportation can be efficiently made electric on a practical scale. The present state of lithium-ion battery energy density and cost trajectories has made tactical véhicule applications feasible. In contrast, new-generation solutions, including solid-state battery technology, could allow for large gains in energy density, charging speed, and operating ranges.

Rheinmetall, a renowned contractor in the military sector, finalized the development of a new electrode technology for hydrogen electrolysis in January 2026 and arranged pilot-scale production to support the fielding of hydrogen fuel cell systems in military applications.

MARKET RESTRAINT

Technical Performance Limitations and Power-to-Weight Ratio Constraints Hamper the Market Growth

There are still several technological challenges that preclude the seamless integration of electric propulsion systems into military platforms, even when one considers the usual power-to-weight ratio, range, and payload requirements. Although energy density for batteries has been improving at a rate of knots, it still remains lower than conventional diesel if weight-for-energy is considered, that is, lithium-ion batteries are certainly not on an equal footing with diesel fuel.

Putting battery packs in alters the entire layout of the vehicle, where the weight will be, how the center of gravity will move, and how the structure needs to be set up. This is why you can’t just bolt batteries in; you do a lot of re-engineering to fit them.

MARKET OPPORTUNITY

Hydrogen Fuel Cell Integration and Multi-Vector Energy Architectures Anticipate the Market Opportunity

Hydrogen fuel cell technology is being seen as a potentially viable route that addresses both the range and the weight challenges posed by current battery electric solutions, while retaining the smooth, quiet, and cooler operating dynamics emitted by electrical architecture.

Ballard Power Systems is a leading developer of fuel cell system R&D and has provided hydrogen proton exchange membrane (PEM) fuel cells for military and aerospace applications. Their past performance could enable them to extend operational life threefold when compared to regular battery life and have reliability levels five times higher than small internal combustion engines with electric systems.

For instance, in November 2025, Rheinmetall formed a strategic partnership with Sunfire to accelerate green hydrogen production for the armed forces with their “Giga PtX" project. The aim is to allow decentralized hydrogen production in remote-operated military facilities and eliminate any need for a hydrogen supply chain.

MARKET CHALLENGES

Charging Infrastructure Development and Operational Logistics Complexity Hinder the Market Growth

A comprehensive electrification solution for military vehicles requires that a robust charge infrastructure be established that is capable of sustaining military forces deployed in remote and challenging environments. Such a task is vastly different from what is needed for developing infrastructure for non-military EVs.

While civilian EVs can make use of distributed charging infrastructure, which reduces reliance on a centralized power grid, military silent operations require a charging solution that is transportable, easily set up, and durable. This technology should be operational in areas with no reliable power grid, and its functionality should not be hampered by adversaries.

SEGMENTATION ANALYSIS

By Platform

Operational Risk Reduction and Personnel Casualty Avoidance Drive the Unmanned Ground Vehicles Segmental Growth

Based on the platform, the market is divided into ground combat vehicles, tactical wheeled vehicles, logistics & support vehicles, special mission vehicles, and Unmanned Ground Vehicles (UGV/ROV)

The unmanned ground vehicles (UGV/ROV) sub-segment is estimated to be the fastest growing with the highest CAGR of 14.60% during the forecast period. The growth is driven by their potential to transfer risk from human personnel to autonomous systems operating in hostile, contaminated, and hazardous environments. With the projected escalation of future warfare, as now evidenced by Russia’s invasion of Ukraine, viewing Russia’s approach to warfare as having made advanced anti-personnel weapons, as well as their utilization in warfare, a new norm, there has been accelerated acquisition and development of unmanned ground vehicle systems by NATO’s allied militaries.

The tactical wheeled vehicles sub-segment accounted for the largest military vehicle electrification market share with a 30.91% and is estimated to have a growth rate of 12.93%.

By Propulsion Type

Superior Power Density and Distributed Motor Technologies Anticipate the Electric Drive Layout Segmental Growth

Based on the propulsion type, the market is divided into IC engine, drive configuration, electric drive layout, and transmission / gear solutions.

The electric drive layout sub-segment is estimated to be the fastest growing with the highest CAGR of 13.21% during the forecast period. In addition, the segment is accounted for as the largest market share of 32.39% in 2025. These are made possible by revolutionary developments in in-wheel hub motor technologies and distributed electric propulsion configurations.

The transmission/gear solutions sub-segment is estimated to be the second-fastest-growing, with a CAGR of 12.86% during the forecast period.

By Systems

Advancements in Battery Technologies Drive Energy Storage Segmental Expansion

Based on the systems, the market is divided into power generation, cooling system, energy storage, traction drive, power conservation, and others.

The energy storage sub-segment is estimated to be the fastest growing with the highest CAGR of 14.18% during the forecast period. In addition, the sub-segment is accounted for the largest market share of 28.71% in the year 2025. The growth is driven by advancements in Solid-State Batteries and Lithium-Sulfur Batteries, which improve the energy density, durability, and ability to withstand extreme environments. Such innovations would make silent watches more viable, as well as reduce the dependency on fuel generators, which is highly important in stealth missions.

The traction drive sub-segment is estimated to be the second fastest growing with a CAGR of 13.01% during the forecast period.

By Technology

Breakthroughs in High-Density Batteries Accelerate Battery Electric (BEV) Adoption

Based on the technology, the market is divided into conventional, micro / mild hybrid, full hybrid, Plug-in Hybrid (PHEV), Battery Electric (BEV), Fuel-cell Electric (FCEV), and hybrid fuel-cell.

The Battery Electric (BEV) is estimated to be the fastest growing with the highest CAGR of 15.51% during the forecast period. The growth is driven by lithium-ion and sulfur batteries with high energy density, and solid-state batteries provide more than 500 Wh/kg with ranges of over 300 km for armored systems. This cuts recharge time to below 30 minutes with megawatt charging that is appropriate for speedy deployment.

The full hybrid sub-segment is accounted for the largest market share of 26.94% in 2025, and is estimated to have a growth rate of 11.41% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Installation Type

Cost-Effective Modernization of Legacy Fleets Accelerates Retrofit Demand

Based on the installation type, the market is divided into new-build and retrofit / upgrade.

The retrofit/upgrade sub-segment is projected to be the fastest growing with the highest CAGR of 13.64% during the forecast period. The growth is driven by cost efficiencies and rapid fleet modernization programs, while New-Build maintains commanding dominance through optimized performance and scalability. This discussion outlines the essential considerations for both forces, described in single-sentence sub-headings and further defined with professional-length paragraphs of approximately 5-6 lines for each point as defined by recent industry trends.

The new-build sub-segment is accounted for the largest global military vehicle electrification market share with 62.40% in 2025.

By Voltage Type

Small, High-Powered Designs for Next-Gen Heavy Platforms Boosts High Voltage (Above 600V) Segment’s Growth

Based on the voltage type, the market is divided into Low Voltage (Less than 50V), Medium Voltage (50-600V), and High Voltage (Above 600V)

The high voltage (above 600V) sub-segment is projected to be the fastest growing with the highest CAGR of 13.32% during the forecast period. The growth is driven by its support for small, high-powered designs needed by next-generation heavy platforms requiring megawatt-class propulsion. These inverters absorb intense heat during battle conditions, resulting in a size reduction of 50% and a 40% decrease in weight, which is suited for air-transportable armor designs. This allows for faster switching rates, which improve silent operation time.

The Medium Voltage (50-600V) has dominated the military vehicle electrification market share with 62.41%

Military Vehicle Electrification Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, the Middle East & Africa, and Latin America

North America

North America Military Vehicle Electrification Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2025, valued at USD 2.11 billion, and also maintained the leading share in 2026, with USD 2.26 billion.

U.S. Military Vehicle Electrification Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 2.01 billion in 2025, and an estimated CAGR of 10.78% during the forecast period.

Europe

Europe is projected to be the fastest-growing region with the highest CAGR of 14.26% during the forecast period of 2026-2034. European militaries face urgent requirements to upgrade aging Cold War-era fleets amid heightened Russian border threats, driving rapid adoption of hybrid-electric systems for enhanced stealth and reduced fuel convoys across all regional platforms.

U.K. Military Vehicle Electrification Market

The U.K. military vehicle electrification market in 2025 is estimated at around USD 0.25 million, and the estimated growth rate of 14.45% during the forecast period.

Germany Military Vehicle Electrification Market

The Germany military vehicle electrification market in 2025 is estimated at around USD 0.31 million, and the estimated growth rate is 16.22% during the forecast period.

Rest of Europe Military Vehicle Electrification Market

The Rest of Europe military vehicle electrification market in 2025 is estimated at around USD 0.25 million, and the estimated growth rate is 8.88% during the forecast period.

Asia Pacific

Asia Pacific is estimated to reach USD 0.96 billion in 2025 and secure the position of the third-largest region in the market. Indo-Pacific pivot and archipelago logistics ignite multi-domain electrification. Regional doctrines emphasize swarm tactics, with electric UGVs comprising procurements for distributed lethality.

China Military Vehicle Electrification Market

The China military vehicle electrification market in 2025 is estimated at around USD 0.73 million, and the estimated growth rate is 10.79% during the forecast period.

India Military Vehicle Electrification Market

The India military vehicle electrification market growth in 2025 is estimated at around USD 0.30 million, and the estimated growth rate is 16.28% during the forecast period.

Japan Military Vehicle Electrification Market

The Japan military vehicle electrification market in 2025 is estimated at around USD 0.20 million, and the estimated growth rate is 14.53% during the forecast period.

Middle East & Africa and Latin America

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.26 billion in 2025. The Middle East & Africa market is set to reach a valuation of USD 0.99 billion in 2025.

Brazil Military Vehicle Electrification Market

The Brazil military vehicle electrification market in 2025 is estimated at around USD 0.16 million, and the estimated growth rate is 9.43% during the forecast period.

Israel Military Vehicle Electrification Market

The Israel military vehicle electrification market in 2025 is estimated at around USD 0.201 million, and the estimated growth rate is 11.46% during the forecast period.

COMPETITIVE LANDSCAPE

Key Industry Players

Growing Modernization Programs of Global Fleet into Conventional to Electric/Hybrid Trend Catalyze the Market Growth

The market for electrification in the military vehicle industry is closely followed by traditional defense sector leaders and niche powertrain technologists who advocate different innovation roads.

R&D spend is accelerating on modular electrification architectures that enable fast platform upgrades and on-the-fly modifications, with a high emphasis on software-defined vehicle control and power management systems.

With advancing defense spending and the advent of electrification, the pace is heating up for several fields, which include fuel efficiency, exportable power production, quiet and stealthy range, low maintenance, and flexible technologies for a variety of vehicles.

LIST OF KEY MILITARY VEHICLE ELECTRIFICATION COMPANY PROFILES

- Oshkosh Corporation (Oshkosh Defense) (U.S.)

- BAE Systems plc (U.K.)

- Rheinmetall AG (Germany)

- General Dynamics Land Systems, Inc. (U.S.)

- KNDS N.V. (Netherlands)

- IVECO Defence Vehicles S.p.A. (Italy)

- Hanwha Aerospace Co., Ltd. (South Korea)

- ST Engineering Land Systems Ltd. (Singapore)

- Otokar Otomotiv ve Savunma Sanayi A.Ş. (Turkiye)

- Hyundai Rotem Company (South Korea)

- Tata Advanced Systems Limited (TASL) (India)

- Mahindra Defence Systems Limited (India)

- Paramount Group (Pty) Ltd (South Africa)

- QinetiQ Group plc (U.K.)

- Allison Transmission, Inc. (U.S.)

KEY DEVELOPMENT

- January 2026: Rheinmetall finalized the development of a highly efficient electrode system for alkaline electrolysis as lead within the E²ngel project. The new electrode technology doubles power density and increases efficiency by over 10% compared to prior electrolysis. Pilot-series production will begin at St. Leon-Rot. With such advancements in hydrogen technology coming to light, other businesses must focus on growing investment in the global military vehicle electrification market.

- November 2025: Rheinmetall announced a collaboration with Sunfire and a group of partners from the high-tech sector for the purpose of advancing the “Giga PtX” military e-fuels project. This effort has the purpose of enabling the production of synthetic fuels for the military within their own supply chains, thus allowing the military to achieve independence from the fossil fuel supplies available worldwide.

- November 2025: BAE Systems Land & Armaments received a contract modification worth USD 390 million to supply additional Bradley A4 infantry combat vehicles. The new systems feature upgraded powertrain items, new electrical architecture, and digitized electronics to enhance situational awareness. The Bradley A4 architecture features an electrification-ready electrical backbone to facilitate future hybrid-electric drive systems.

- July 2025: Leonardo S.p.A. acquired Iveco Defence Vehicles (IDV) from Iveco Group for a consideration of approximately USD 1.96 billion of enterprise value. According to the agreement, Leonardo becomes the prime contractor for the integrated land systems market. This amalgamation of IDV and Leonardo allows the company to work on the development of electric vehicles and power systems and further enhances the development of future generations of battle-ready vehicles based on electrification technologies. This transaction is expected to close in Q1 of 2026.

- April 2025: An order for 150 Dutch Expeditionary Patrol Vehicles (DXPV) Oshkosh JLTV-series vehicles worth approximately USD 306 million has been placed by the Dutch Ministry of Defence for the Royal Netherlands Marine Corps. The order reflects NATO partners' acceptance of Oshkosh's Electrification Architecture and interoperability standards based on its ProPulse hybrid-electric technology.

REPORT COVERAGE

The global military vehicle electrification market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and global military vehicle electrification market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2024 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 12.40% from 2026 to 2034 |

|

Unit |

USD Billion |

|

Segmentation |

By Platform · Ground Combat Vehicles · Tactical Wheeled Vehicles · Logistics & Support Vehicles · Special Mission Vehicles · Unmanned Ground Vehicles (UGV/ROV) By Propulsion Type · IC Engine · Drive Configuration · Electric Drive Layout · Transmission / Gear Solutions By Systems · Power Generation · Cooling System · Energy Storage · Traction Drive · Power Conservation · Others By Technology · Conventional · Micro / Mild Hybrid · Full Hybrid · Plug-in Hybrid (PHEV) · Battery Electric (BEV) · Fuel-cell Electric (FCEV) · Hybrid Fuel-Cell By Installation Type · New-Build · Retrofit / Upgrade By Voltage Type · Low Voltage (Less than 50V) · Medium Voltage (50-600V) · High Voltage (Above 600V) By Region North America (By Platform, By Propulsion Type, By Systems, By Technology, By Installation Type, By Voltage Type, By Country) · U.S. (By Installation Type) · Canada (By Installation Type) Europe (By Platform, By Propulsion Type, By Systems, By Technology, By Installation Type, By Voltage Type, By Country) · U.K. (By Installation Type) · Germany (By Installation Type) · France (By Installation Type) · Nordic Countries (By Installation Type) · Eastern Europe (By Installation Type) · Rest of Europe (By Installation Type) Asia Pacific (By Platform, By Propulsion Type, By Systems, By Technology, By Installation Type, By Voltage Type, By Country) · China (By Installation Type) · India (By Installation Type) · Japan (By Installation Type) · South Korea (By Installation Type) · Australia (By Installation Type) · Rest of Asia Pacific (By Installation Type) Middle East & Africa (By Platform, By Propulsion Type, By Systems, By Technology, By Installation Type, By Voltage Type, By Country) · Israel (By Installation Type) · Gulf Countries (By Installation Type) · Turkey (By Installation Type) · South Africa (By Installation Type) · Rest of Middle East & Africa (By Installation Type) Latin America (By Platform, By Propulsion Type, By Systems, By Technology, By Installation Type, By Voltage Type, By Country) · Brazil (By Installation Type) · Argentina (By Installation Type) · Rest of Latin America (By Installation Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 6.48 billion in 2025 and is projected to reach USD 17.90 billion by 2034.

In 2025, the North American market value stood at USD 2.11 billion.

The market is expected to exhibit a CAGR of 12.40% during the forecast period of 2026-2034.

The High Voltage (Above 600V) segment is expected to hold the highest CAGR over the forecast period.

Technological advancements in energy storage and power systems drive the market growth.

BAE Systems, Oshkosh Defense, General Dynamics, Leonardo S.p.A., Krauss-Maffei Wegmann, Textron, QinetiQ Group, Nexter Group, and General Motors Defense.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us