Military Vetronics Market Size, Share & Industry Analysis, By Product Type (Communication & Navigation Systems, Power System, Display System, C4 Systems, and Others), By Platform (Unmanned Ground Vehicles, Armored Amphibious Vehicles, Light Protected Vehicles, Special Purpose Vehicles, and Others), By Application (OEM and Aftermarket), and Regional Forecast, 2026-2034

Military Vetronics Market Size and Industry Overview

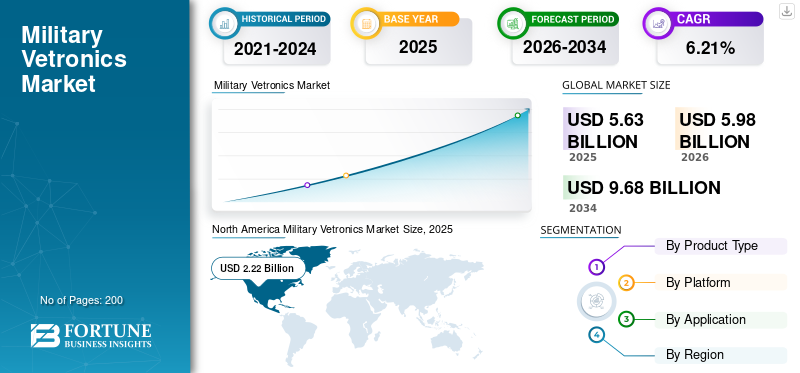

The global military vetronics market size was valued at USD 5.63 billion in 2025. The market is projected to grow from USD 5.98 billion in 2026 to USD 9.68 billion by 2034, exhibiting a CAGR of 6.21% during the forecast period. North America dominated the military vetronics market with a market share of 34.26% in 2025.

Military vetronics consist of several electronic systems installed on a vehicle that control functions such as communication, navigation, and weapons. The system includes components from boards & chips to displays and power electronics. Real-time data collected and analyzed by electronic systems flows over the wireless, which provides soldiers with situational awareness, specifically in battlefield settings. The increasing focus on improving situational awareness in battlefield management and growing instances of network-centric warfare drive market growth. In July 2020, for instance, the U.S. Army Combat Capabilities Development Command (CCDC) C5ISR Center (formerly known as CERDEC) launched the Army’s C4ISR/Electronic Warfare Modular Open Suite of Standards (CMOSS) initiative. It is a modular open system architecture (MOSA) that integrates different capabilities into one box for military vehicle electronics systems.

Download Free sample to learn more about this report.

Global Military Vetronics Market Overview

Market Size:

- 2025 Value: USD 5.63 billion

- 2026 Value: USD 5.98 billion

- 2034 Forecast Value: USD 9.68 billion, with a CAGR of 6.21% (2026–2034)

Market Share:

- Regional Leader: North America held 34.26% market share in 2025, driven by high defense spending and modernization programs in the U.S., along with major players like Lockheed Martin, Raytheon Technologies, and General Dynamics.

- Fastest-Growing Region: Asia Pacific, fueled by rising geopolitical tensions, increased defense budgets, and vehicle procurement programs in countries like India and China.

- Leading Platform Segment: Tanks & Armored Vehicles, due to major acquisition programs and growing cross-border threats.

Industry Trends:

- CAN Bus Integration: Rising adoption of Controller Area Network (CAN) bus systems for high-speed, ruggedized communication across critical systems in military vehicles.

- C4ISR Enhancements: Surge in demand for modular open systems and integration of command, control, communication, computers, intelligence, surveillance, and reconnaissance (C4ISR) capabilities.

- AI & Autonomous Systems: Growing use of artificial intelligence, robotics, and autonomous ground vehicles for combat efficiency and reduced human risk.

Driving Factors:

- Military Modernization Programs: Global initiatives such as France’s SCORPION and the Franco-German MGCS project are enhancing battlefield awareness and networked warfare.

- Increased Defense Budgets: Nations are ramping up spending amid geopolitical instability to procure next-gen combat vehicles with advanced vetronics.

- Combat Vehicle Procurement: Major deals like Australia’s USD 12.5B acquisition of 678 armored vehicles are fueling OEM demand.

Military & Defense Sector Witnessed Unprecedented Challenges amid the COVID-19 Pandemic

The COVID-19 pandemic can affect the global economy in three main domains:

- By directly affecting demand

- By creating market disruptions

- By impacting firms and financial markets

The defense industry in several countries has been impacted by COVID-19. Demand reduction has changed the dynamics of this industry. Due to lockdowns, the defense sector underwent massive disruptions, resulting in a slowdown in electronics production. Various countries’ defense expenditures have contracted amid COVID-19 as resources have been reallocated to the healthcare sector for enhancing infrastructure and facilities. Furthermore, delayed deliveries of combat vehicles may hamper the market scenario. For example, BAE Systems signed a contract worth USD 15 billion with the U.S. Army to deliver 2,936 combat vehicles. Out of these, an initial set of three was expected to be delivered in March 2020, but due to COVID-19, the delivery was delayed by five months.

MILITARY VETRONICS MARKET TRENDS

Download Free sample to learn more about this report.

Increasing Use of Controller Area Network Bus in Military Vehicles to Boost the Market

Controller Area Network (CAN) bus is a communication standard for the embedded systems in different vehicles. The increasing demand for electronics in autonomous vehicles and CAN bus due to higher reliability and flexibility will fuel the global market growth. W.L. Gore & Associates, for instance, provides GORE™ CAN bus cables for defense land systems. Tactical military vehicles have highly attuned sensors for navigation as these vehicles operate in critical environments. Thus, a higher priority is placed on sensors and algorithms to calculate, analyze, and make split-second decisions. CAN bus allows all the complex systems to communicate with high speed, clarity, and accuracy. Furthermore, CAN’s inherent ruggedness enables it to operate in extreme heat and cold environments.

- North America witnessed military vetronics market growth from USD 2.18 Billion in 2018 to USD 2.22 Billion in 2019.

DRIVING FACTORS

Military Modernization Programs by Countries for Network Centric Warfare to Propel Market Growth

The modern battlefield requires dynamic forces that can act with speed and precision. Modern militaries are focusing on the introduction of cutting-edge network technologies to exploit the information advantage. Militaries of different countries are developing their arsenal to enhance situational awareness, streamline decision-making, and increase mission effectiveness by linking sensors, commanders, and shooters in a fully networking environment.

In 2020, for example, the French Army announced plans to invest USD 12 billion in the SCORPION military modernization program. The program includes the acquisition of new armored vehicles and the up-gradation of existing armor assets. Another example is the Franco-German Main Ground Combat System (MGCS), a joint effort to develop main battle tanks that will replace Germany’s Leopard 2 and France’s Leclerc by 2035. Thus, the procurement of new vehicles and modernization of existing armored vehicles are driving the military vetronics market growth.

Growing Defense Expenditures and Procurement of Advanced Combat Vehicles to Aid the Market

The rising incidence of terrorist activities, political unrest across the globe, and geopolitical tensions in the Asian and Middle Eastern countries have led to the procurement of next-generation combat vehicles. Growing military spending for R&D activities and rising defense expenditures, especially in emerging economies, will boost the market. In September 2020, for instance, the Australian Army decided to procure 678 armored vehicles at USD 12.5 billion. The vehicles include modern and high-capacity sensors and communication suites. In September 2020, Rheinmetall Defence Australia signed a contract with the Australian Army to supply 211 Boxer 8×8 combat reconnaissance vehicles (CRVs) and 223 vehicle modules.

RESTRAINING FACTORS

Delayed Deliveries and Reduction of Defense Budgets to Restrict Growth

Reduction in the defense budgets of several countries hampers the growth of this market. Delayed deliveries of combat vehicles due to lack of production capabilities and disruptions in the supply chains are restricting the growth of the market. For example, in 2019, General Dynamics Land Systems-UK (GDLS-UK) was supposed to deliver the first squadron set of vehicles to the UK Ministry of Defence, but there was a delay in the delivery as the Army did not receive the 40 mm turreted Ajax vehicles.

SEGMENTATION ANALYSIS

By Product Type Analysis

To know how our report can help streamline your business, Speak to Analyst

Growing Demand for Real-Time Information to Boost the Communication & Navigation Segment

Based on product type, the market for military vetronics is segmented into communication & navigation systems, display systems, power systems, C4 systems, and others. Among these, the communication & navigation system segment holds the highest share in the market. The increasing demand for advanced communication & navigation systems for real-time information on the battlefield is anticipated to boost segment growth. Modern warfare is technology-centric and effective communication improves military missions' success rate and interoperability, thus driving market growth.

- The Display Systems segment is expected to hold a 15.63% share in 2019.

The command, control, and computer system (C4 System) segment will showcase significant growth during the forecast period. Command and control systems provide combat vehicles flexibility to expand and reconfigure components in the field. These systems reduce risks, costs, and time associated with vehicle disassembly.

The power system segment is anticipated to display moderate growth due to the rising demand for advanced vehicles for different missions.

By Platform Analysis

Increasing Demand for Tanks and Advanced Armored Vehicles to Support Growth

Based on platform, the market is classified into unmanned ground vehicles, tanks & other armored vehicles, lightly protected vehicles, amphibious vehicles, special purpose vehicles, and others. The tanks and other armored vehicles segment held the highest market share in 2019. Increasing procurement of main battle tanks and other armored vehicles by countries for strengthening their military capabilities are driving this segment's growth.

The unmanned ground vehicles segment is expected to show significant growth during 2020-2027. This growth is due to the introduction of robotics, artificial intelligence, and other advanced technologies that enhance operational efficiency, accuracy, and reduce human risks. The light protected vehicle segment is projected to generate USD 1.46 billion in revenue by 2025.

By Application Analysis

Rising Demand for Advanced Combat Vehicles to Drive the OEM Segment

By application, the market is classified into original equipment manufacturers (OEMs) and aftermarket.

The OEM segment held the highest share in the global market in 2019. The OEM segment's growth is supported by the increasing number of orders for advanced armored vehicles from different countries' defense forces. The OEM segment is expected to hold a 89% share in 2025.

The aftermarket segment would show remarkable growth owing to the regular replacement of electronic components and implementation of programs to upgrade existing fleets.

REGIONAL ANALYSIS

North America Military Vetronics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The market has been segmented into four major regions: North America, Europe, Asia Pacific, and the Rest of the World.

North America

North America dominated the military vetronics market share in 2019, attributed to the huge defense spending on procurement of advanced vehicles and investments in the up-gradation of existing vehicles by the US. The presence of key players in North America, including Lockheed Martin Corporation, L3Harris Technologies, Inc., Raytheon Technologies Corporation, and General Dynamics Corporation, will further boost the market.

Asia Pacific

Asia Pacific will witness significant growth during 2020-2027. This growth is attributed to the rising threat of terrorist activities in Asian countries, political conflicts over cross-border issues, and increasing investments from several countries on defense operations across the region. In June 2020, for instance, the Indian Ministry of Defense cleared the procurement of 156 BMP 2 infantry vehicles for the Indian Army. All these vehicles are manufactured at the Ordnance Factory Medak under the Make in India program.

- The military vetronics market in Japan is expected to reach USD 7.31 billion by 2025.

- India is projected to witness a strong CAGR of 4.10% during the forecast period.

Europe

In Europe, the presence of key players, such as BAE Systems, Rheinmetall AG, Leonardo S.p.A, Saab AB, and others, will drive the market across the region. Increasing defense expenditures and higher spending on combat vehicles' procurement is anticipated to boost market growth. The Europe is anticipated to grow at a CAGR of 3.71% during the forecast period.

Rest of the World

The Rest of the World is set to register a remarkable growth trajectory during the forecast period. This growth is owing to the increasing expenditure on defense and strengthening of military forces by several Middle Eastern countries such as Saudi Arabia, Turkey, and Israel.

KEY INDUSTRY PLAYERS

Introduction of Advanced Technologies with Augmented C4ISR Capabilities to Fuel Competition

Military vetronics manufacturers are majorly focusing on introducing advanced technologies such as robotics, artificial intelligence, and big data analytics for performance improvement. OEMs are aiming to reduce hardware size, weight, power, and cost (SWaP-C) using these advanced technologies. Furthermore, the up-gradation programs to enhance command, control, communication, computers (C4), intelligence, surveillance, and reconnaissance (ISR) capabilities of the existing fleets of combat vehicles are also driving market growth. In September 2020, for instance, Tectonica signed a contract worth USD 25 million with the Australian Army for the supply of situational awareness systems for the Boxer vehicles built by Rheinmetall AG.

LIST OF KEY COMPANIES PROFILED:

- BAE Systems (The U.K)

- General Dynamics Corporation (The U.S.)

- L3Harris Technologies, Inc. (The U.S.)

- Leonardo S.p.A (Italy)

- Lockheed Martin Corporation (The U.S.)

- Raytheon Technologies Corporation (The U.S.)

- Rheinmetall AG (Germany)

- Saab AB (Sweden)

- Thales Group (France)

- Oshkosh Corporation (The U.S.)

- Curtiss Wright Corporation (The U.S.)

KEY INDUSTRY DEVELOPMENTS:

- In July 2021, The U.S. army signed a contract worth USD 72.5 million with BAE systems to provide artillery armored combat vehicles with digital vetronics. This will upgrade M109A7 armored combat vehicle with digital vetronics and modern power system.

- In June 2021, For a Swedish armoured combat vehicle, BAE Systems has chosen Elbit for vetronics sensors and active protection. The CV90 is a Swedish tracked combat vehicle that was developed in the mid-1980s and entered service in Sweden in the mid-1990s.

- In Feb 2021, The Army Contracting Command at Detroit Arsenal in Warren, Mich., revealed earlier this month that Oshkosh had been awarded a USD 942.9 million contract to develop and service the Stryker Medium-Caliber Weapon system. The 30-millimeter cannon on this version of the eight-wheel Stryker combat vehicle will be used to destroy lightly armoured vehicles and bunkers.

REPORT COVERAGE

The military vetronics market research report provides an in-depth technical analysis of the market and majorly focuses on key aspects such as leading market players, COVID-19 effect on the market, leading technological advancements, trends, and research methodology of the product. Besides this, the report offers insights into the current market trends and highlights key industry developments & trends. In addition to the aforesaid factors, the report provides multiple factors that will contribute towards the growth of the market during the forecast period.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Product Type

|

|

By Platform

|

|

|

By Application

|

|

|

By Geography

|

Frequently Asked Questions

According to Fortune Business Insights, the global military vetronics market size was USD 5.63 billion in 2025 and is projected to reach USD 9.68 billion by 2034, growing at a CAGR of 6.21% during the forecast period 2026–2034.

Military vetronics refers to the integrated electronic systems used in military vehicles for communication, navigation, surveillance, command and control (C4), and weapons systems, enhancing battlefield awareness and operational efficiency.

Growing at a CAGR of 6.21%, the market will exhibit decent growth in the forecast period (2026-2034).

Key growth drivers include increased military modernization programs, rising demand for network-centric warfare systems, C4ISR upgrades, and growing use of AI and data analytics in defense vehicle platforms.

The tanks and armored vehicles segment holds the largest share due to the increasing global procurement of main battle tanks and infantry fighting vehicles with advanced electronic warfare systems.

Emerging trends include the adoption of modular open systems architectures (MOSA), the use of CAN bus communication, miniaturization of components (SWaP-C), and integration of augmented C4ISR technologies.

Major companies include BAE Systems, General Dynamics, Lockheed Martin, Raytheon Technologies, Rheinmetall AG, L3Harris Technologies, Saab AB, Thales Group, and Leonardo S.p.A., all of which invest in R&D and system upgrades.

North America holds the largest market share, driven by high U.S. defense spending, rapid adoption of cutting-edge vetronics systems, and a strong presence of major defense contractors.

Asia-Pacific is expected to witness significant growth due to increasing defense budgets in countries like India, China, and Australia, regional conflicts, and ongoing investments in indigenous armored vehicle programs.

Major challenges include budget constraints in some countries, delays in procurement and deliveries, and supply chain disruptions, particularly affecting the delivery of electronic components and vehicle systems.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us