Milk Packaging Market Size, Share & Industry Analysis, By Material (Plastic, Paper & Paperboard, Glass, and Metal), By Packaging Type (Pouches, Cartons, Bottles & Cans, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

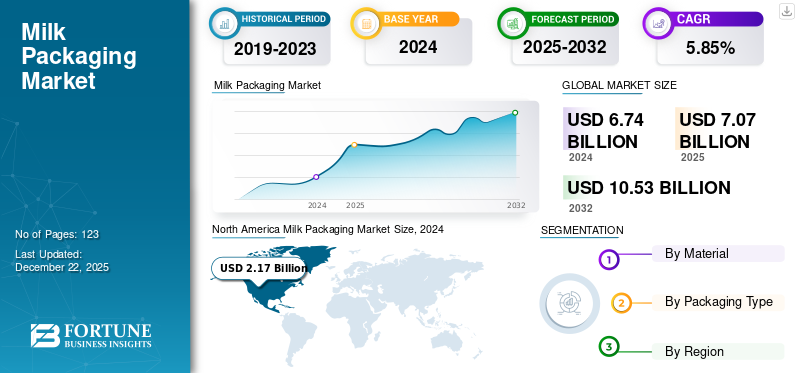

The global milk packaging market size was valued at USD 7.07 billion in 2025. The market is projected to grow from USD 7.44 billion in 2026 to USD 11.91 billion by 2034, exhibiting a CAGR of 6.05% during the forecast period. North America dominated the milk packaging market with a market share of 32.19% in 2024.

Milk packaging refers to the materials and techniques employed to hold and deliver milk while maintaining its freshness, quality, safety, and convenience for consumers. It includes several kinds of containers, such as bottles, cartons, pouches, glass bottles, and cans. The demand for packaged liquid products, especially dairy products, is propelled by the rapid urbanization in developing nations, contributing to market growth. Furthermore, increasing consumer spending and higher disposable incomes are driving the expansion of the global liquid packaging cartons sector.

- The International Dairy Federation states that the dairy industry is crucial for feeding the global population, generating 881 million tons of milk in 2019, a figure that continues to grow annually. Over 80% of people globally, which amounts to around 6 billion individuals, frequently consume liquid milk or various dairy items.

Tetra Pak International S.A. and Nippon Paper Industries Co. Ltd. are the leading manufacturers, accounting for the largest global market share.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Augmenting Product Demand from Online Food Delivery Sector Drives Market Growth

The global online food delivery sector is expanding rapidly. The increasing consumption of milk products among the millennial population is fueling the need for effective packaging such as cartons, bottles. This industry is witnessing a transition toward eco-friendly packaging due to stricter regulations on plastic packaging being enacted by governments globally. The growth of the plant-based and dairy beverage markets, which include milk, remains a significant driver for the demand for milk packages. There is a rising interest in home-delivered milk using reusable packaging. In the U.K., companies such as Milk & More are broadening their services to cater to this demand, showcasing a consumer trend toward sustainability and convenience.

- In 2024, a survey from Statista of Canadian consumers regarding online food delivery orders by brand revealed that 54% of participants had used Uber Eats in the last year for food orders. DoorDash claimed the second spot, with 49% of those surveyed utilizing the food delivery service. These findings come from a representative online survey conducted in 2024 involving 776 consumers across Canada.

MARKET RESTRAINTS

Fluctuations in Raw Material Prices & Upfront Product Costs Hamper Market Growth

In spite of positive market conditions, various limitations impede growth. The initial investment needed for manufacturing milk packaging can be higher than that of traditional packaging materials, which could deter smaller businesses from entering the market. Furthermore, fluctuations in the prices of raw materials can impact profit margins, as seen in the rising costs of paperboard and coatings used in production. The increasing consumer trend toward plant-based milk alternatives, such as almond, oat, and soy milk, diminishes the need for conventional milk packages. The perishability of milk requires effective cold chain logistics, and advancements in packaging alone might not completely solve the issue of shelf-life extension, which in turn limits the milk packaging market growth.

MARKET OPPORTUNITIES

Increasing Need for Eco-Friendly Packaging and Smart Cartons to Provide Lucrative Opportunities

The global market for milk packaging is experiencing significant growth, driven by a rising demand for packaged liquid products and an increasing focus on sustainable packaging options. There is a growing emphasis from both consumers and regulatory bodies on environmentally friendly packaging, leading to an uptick in the use of milk packaging solutions made from renewable materials such as paperboard with thin layers of plastic and aluminum. Innovations in smart carton technology, which include features such as freshness indicators and RFID tags, are attracting consumer interest and contributing to notable market expansion.

MILK PACKAGING MARKET TRENDS

Implementation of Ergonomic Designs for Modern Lifestyles Emerge as a Key Trend

Efficient as well as user-friendly designs are at the forefront of modern milk packaging. Such innovations make household tasks smoother while keeping milk storage functional for limited spaces. The ergonomic design of milk packaging is centered on developing solutions that are intuitive, comfortable, and simple for users to engage with, considering aspects such as accessibility, grip, and dimensions. It aims to enhance the packaging for human interaction, simplifying the process of opening, handling, and utilizing the contained product. The market is seeing a rise in the popularity of innovative milk pouches equipped with resealable caps and convenient easy-pour spouts. These features cater to the demands of busy households by preventing spills and facilitating quick, hassle-free milk handling, and emerging as a key trend for the market growth.

Download Free sample to learn more about this report.

Segmentation Analysis

By Material

Paper & Paperboard Material Led Market Due to Its Eco-friendly Characteristics

Based on material, the market is divided into plastic, paper & paperboard, glass, and metal.

The paper & paperboard segment accounted for the largest milk packaging market share in 2024. Paper reduces reliance on alternative packaging materials and holds eco-friendly characteristics. Aseptic ultra-high temperature cartons can preserve milk for extended periods without the need for refrigeration, making them suitable for long-term storage and transport. The paperboard's surface allows for high-quality printing, enabling brands to showcase product details and marketing messages effectively. This material represents a more sustainable choice for packaging a variety of liquids and beverages. The growing awareness of environmental impact is fueling expansion in this sector.

Plastic is the second-leading material segment globally. Using plastic for milk packages offers various benefits. It provides a lighter, sturdier, and potentially more economical packaging solution compared to traditional materials such as glass or metal. Furthermore, plastic serves as an effective barrier against moisture and damage, ensuring that the product arrives at its destination in perfect condition.

By Packaging Type

Growing Utilization of Milk Pouches Owing to Their Convenience & Sustainability Boosted Segment Growth

Based on the packaging type, the market is segmented into pouches, cartons, bottles & cans, and others. Pouches dominated the market in 2024 as they utilize less material than bottles or cartons, resulting in lower production and transportation costs. Reduced manufacturing expenses allow for more affordable pricing for both producers and buyers. Milk pouches are lightweight, which decreases shipping costs and simplifies handling. They occupy less space in storage and refrigerators compared to solid containers. Numerous pouches use less plastic than hard bottles, making them more environmentally friendly and increasing their demand from the milk industry. Some can be recycled or are made from biodegradable substances, attracting consumers who prioritize sustainability.

On the other hand, cartons are the second-dominating packaging type segment and are expected to witness steady growth over the forecast period. Milk cartons provide numerous advantages, such as being environmentally friendly, user-friendly, and safeguarding the freshness and nutrients of milk. Typically constructed from renewable materials, they are recyclable and have a lower carbon footprint than many other packaging alternatives. Furthermore, they are simple to store, pour, and reseal, which helps maintain milk's freshness for an extended shelf life.

Milk Packaging Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

North America

North America Milk Packaging Market Size, 2024 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America is dominating the market. In North America, the U.S. stands out as a significant market for milk packaging. This is due to the increasing demand for flexible packaging options among consumers in the nation. The growing fluid milk consumption in several parts of the region also drives the market growth.

- The U.S. Department of Agriculture states that the U.S. contributes to 15% of the global milk production. Total milk production in the U.S. for 2024/2025 was 102.66 million metric tons.

Europe

Europe is a significant market, and it is expected to thrive, driven by an increasing demand for milk products. Government initiatives aimed at encouraging sustainable packaging options are facilitating market growth. Shifts in consumer habits, a significant demand for PET containers, and heightened concerns about product quality are likely to enhance the demand for milk packages.

Asia Pacific

Asia Pacific is the second-largest region and will experience massive growth. The liquid packaging cartons in this region are preferred for milk products. Countries such as India are the major milk producers in the world, which in turn boosts demand for sustainable and cost-effective packaging solutions. It further drives the market growth.

- According to the Food and Agriculture Organization, over the past thirty years, global milk production has risen by over 77%, increasing from 524 million tons in 1992 to 930 million tons in 2022. India ranks as the leading milk producer in the world, contributing 22% of the total global output, followed closely by the U.S., Pakistan, China, and Brazil.

Rest of the World

The market in the rest of the world region is expected to witness considerable growth in the near future. The need for milk packaging has grown in recent years as a response to ongoing changes in the packaging industry. As a result, the rising demand for advanced milk packaging materials and the increasing use of new, environmentally friendly options have driven the global demand for milk packaging.

COMPETITIVE LANDSCAPE

Key Industry Players

Continuous Development and Introduction of New Products by Key Companies Resulted in Their Dominating Market Positions

The global milk packaging market analysis is concentrated with companies such as Tetra Pak International S.A., Nippon Paper Industries Co., Ltd., Elopak AS, Nampak, SIG, and Parksons Packaging, accounting for a significant market share.

Tetra Pak is a global leader in solutions for food processing and packaging, committed to ensuring that food is safe and available to all. Their dedication stems from the conviction that everyone deserves access to safe and nutritious food. They accomplish this through cutting-edge processing and packaging technologies, which help maintain food quality and prolong shelf life.

Elopak AS is a prominent global provider of carton packaging and filling machinery, especially for liquid food items. Their emphasis is on sustainable options, utilizing renewable, recyclable, and responsibly sourced materials to develop innovative packaging solutions as an alternative to plastic. Established in 1957, Elopak is currently a Net Zero company with a workforce of over 2,600 employees, functioning in more than 40 nations and distributing over 15 billion cartons each year.

Additionally, SIG and Nampak are among the other prominent players in the market. Focus on significant investments in the research & development of innovative products has supported the companies’ share in the market.

- In April 2025, SIG collaborated with Plastic Bank, Carta Misr, and TileGreen to create Egypt's first comprehensive recycling system for used aseptic beverage cartons. This initiative aims to transform the Egyptian recycling landscape and convert waste into valuable materials. Carta Misr, a regional paper mill, extracts paper fibers from the aluminum and polymer components of the cartons to produce high-quality recycled paper products. In addition, TileGreen, an Egyptian startup, transforms the PolyAl mixture into sturdy interlock bricks.

LIST OF KEY MILK PACKAGING COMPANIES PROFILED

- Tetra Pak International S.A. (Switzerland)

- Nippon Paper Industries Co. Ltd. (Japan)

- Elopak AS (Norway)

- Nampak (South Africa)

- SIG (Switzerland)

- Parksons Packaging (India)

- Liquibox (U.S.)

- Amcor (Switzerland)

- Mondi (U.K.)

- Refresco (Netherlands)

- Adam Pack (Greece)

- Pactiv Evergreen (U.S.)

- Smurfit Kappa (Ireland)

- Stanpac Inc. (Canada)

- Tilak Polypack Private Limited (India)

KEY INDUSTRY DEVELOPMENTS

- July 2024: Tetra Pak and Mengniu Group unveiled a limited-edition Milk Deluxe Pure Milk range, featuring 30 unique designs based on masterpieces by Van Gogh and Monet. The products are packaged in Tetra Prisma Aseptic 250 Edge cartons with DreamCap 26 closures, and this special edition range has been launched through a partnership with Meet You Museum. Consumers in Greater China can now find these cartons both online and in physical stores.

- April 2024: Nampak Liquid Cartons, in collaboration with Woodlands Dairy, introduced a tethered cap carton in South Africa. This innovation was created to address the reduction of plastic waste, and the new design aims to keep the cap attached to the carton during its recycling process after consumer use.

- January 2024: Coop and Emmi declared the launch of sustainable PET bottles for dairy products. Effective immediately, certain milk and cream products under Coop's private labels are now offered in more environmentally friendly PET bottles, in addition to a range of Emmi brand products, including Emmi Energy Milk.

- August 2022: Delamere Dairy reintroduced its primary fresh goat's milk range in a novel SIG Combidome packaging design. The specialty milk producer from Cheshire stated that this format – a fairly recent idea for U.K. shops – merges the convenience and ease of pouring found in bottles, alongside the eco-friendly benefits of the Brick cartons that were used before.

- March 2019: Granarolo S.p.A., a prominent Italian-owned agro-industrial company, introduced a distinctive product to the market starting in March: the first bottle of milk in Italy created with 20% recycled plastic, reflecting a strengthened dedication to environmental sustainability.

REPORT COVERAGE

The global milk packaging industry analysis provides market size & forecast by all the segments included in the report. It contains details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on the utilization of milk packaging in key regions/countries, company profiles, key industry developments, new product launches, and details on partnerships, mergers & acquisitions in key countries. The report covers a detailed, highly competitive landscape with information on the market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Estimated Year |

2026 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.05% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Material

|

|

By Packaging Type

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 7.44 billion in 2026 and is projected to reach USD 11.91 billion by 2034.

In 2024, the market value in North America stood at USD 2.17 billion.

The market is expected to grow at a CAGR of 6.05% during the forecast period of 2026-2034.

The paper and paperboard segment led the market by material.

The key factor driving the market is the augmenting demand from the online food delivery sector drives market growth.

Tetra Pak International S.A., Nippon Paper Industries Co. Ltd., Elopak AS, Nampak, SIG, and Parksons Packaging are the top players in the market.

North America dominated the milk packaging market with a market share of 32.19% in 2024.

Increased demand from the milk industry is one of the factors that is expected to favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 123

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us