Missile Canister Market Size, Share & Industry Analysis, By Launch Mechanism (Cold Launch Canister and Hot Launch Canister), By Structure (Single-Cell Canister and Multi-Pack Canister), By Missile Class (Surface-to-Air Missiles, Surface-to-Surface Missiles, Anti-Ship Missiles, and Others), By Launch Platform (Land Based and Sea Based), By Standard (Mk 41 VLS Canister, Mk 57 Peripheral VLS, Mk 56 Guided Missile VLS, SYLVER VLS, TEL-mounted Canister, and Others), By Material (Metallic, Composite, and Hybrid), By End User (Navy, Army, and Strategic Forces), and Regional Forecast, 2026-2034

Missile Canister Market Size and Future Outlook

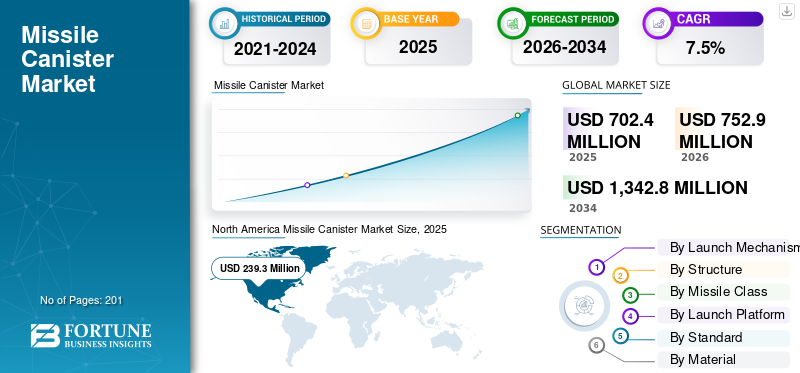

The global missile canister market size was valued at USD 702.4 million in 2025. The market is projected to grow from USD 752.9 million in 2026 to USD 1,342.8 million by 2034, exhibiting a CAGR of 7.5% during the forecast period. North America dominated the missile canister market with a market share of 34.07% in 2025.

The global market is experiencing robust growth, driven by an increasing demand for modular launch vehicles systems and rising geopolitical tensions necessitating rapid deployment capabilities. The proliferation of hypersonic and precision-guided munitions across defense forces and naval operations is another factor propelling industry expansion.

- For instance, in November 2025, the U.S. Navy awarded BAE Systems a contract worth over USD 850 million for next-generation vertical launch system (VLS) canisters, upgrading Mk 41 and Mk 57 platforms with enhanced sealing, thermal protection, and compatibility for hypersonic missiles such as the Conventional Prompt Strike.

Prominent players such as Lockheed Martin, BAE Systems, Raytheon Technologies, Kongsberg Defence & Aerospace, and MBDA are focused on innovations such as lightweight composite materials for reduced weight, increased payload capacity, and corrosion-resistant designs for extended naval service life.

Download Free sample to learn more about this report.

Missile Canister Market Key Takeaways

- 2025 Market Size: USD 702.4 million

- 2026 Market Size: USD 752.9 million

- 2034 Forecast Market Size: USD 1,342.8 million

- CAGR: 7.5% from 2026–2034

- North America dominated the market with a 34.07% share in 2025.

- The Hot Launch Canister segment accounted for the largest market share in 2025.

- The Surface-to-Air Missiles (SAM) segment held the dominant market share in 2025.

Asia Pacific

Asia Pacific recorded USD 212.9 million in 2025, driven by rising defense modernization and regional security investments.

North America

North America reached USD 239.3 million in 2025 and is projected to grow to USD 253.7 million in 2026.

Europe

Europe is projected to grow at a CAGR of 7.8% during the forecast period.

U.S.

U.S. market reached USD 232.2 million in 2025.

Japan

Japan market reached USD 16.9 million in 2025.

Read More

Impact of Russia Ukraine War

The Russia Ukraine war has affected the demand dynamics of the market by accelerating missile consumption rates and exposing the fragility of interceptor stockpiles. It has created sustained demand for air defense systems capable of countering cruise missiles, ballistic missiles, and unmanned aerial threats. Systems such as NASAMS rely on sealed, canisterized interceptor launchers, indicating that each deployment requires both launcher units and continuous replenishment of missile canisters.

- For instance, in May 2023, the U.S. State Department approved a USD 285 million sale of the National Advanced Surface-to-Air Missile System (NASAMS) to Ukraine to counter Russian aerial threats. The package includes one AN/MPQ-64F1 Sentinel Radar, a Fire Distribution Center, and canister launchers, enhancing Ukraine's defense of people and critical infrastructure.

The conflict has also driven governments to prioritize surge manufacturing capacity, long-term framework contracts, and domestic industrial resilience for sealed launch containers and composite missile tubes.

MISSILE CANISTER MARKET TRENDS

Shift toward Modular Canister Designs and Composite Structure is a Prominent Trend

The shift toward modular canister designs and hypersonic compatibility is accelerating in missile canister systems for defense, naval, and ground-based operations. This is driven by the rising demand for rapid reload capabilities, enhanced survivability in high-threat environments, interchangeable munitions support, and seamless integration with next-generation launchers. Moreover, key players are focusing on the development of composite architectures for boosting launch reliability during extreme maneuvers, mitigating corrosion in maritime settings, and enabling high-speed missile ejections without structural failure.

- For instance, in September 2025, Lockheed Martin tested its JAGM Quad Launcher (JQL), successfully firing a Joint Air-to-Ground Missile (JAGM) from a 45-degree angled canister, hitting a stationary ground target and gathering flight data. The JQL features four modular composite canisters for rapid individual reloads, a pivot for angled/vertical launches enabling 360-degree targeting of air, ground, and maritime threats.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increase in Geopolitical Tension and Expansion of Missile Production to Drive Market Growth

A primary driver for the missile canister market growth is escalating geopolitical tensions including hypersonic arms races, naval standoffs, and border conflicts requiring immediate strike capabilities. Geopolitical tensions significantly accelerate the investment in advanced missile canister development as nations prioritize rapid deployment and survivability of missile systems during surged threats.

Defense contractors are increasingly facing increased demand which is leading to the expansion of facilities and adoption of automation for rapid production of cruise missiles and ballistic missiles.

For instance, in November 2025, Raytheon (RTX) signed five landmark framework agreements with the U.S. Department of War to ramp up production of key missiles, including Tomahawk Land Attack/Maritime Strike variants, AMRAAM, SM-3 IB/IIA interceptors, and SM-6. These factors are contributing to a rise in innovation in canister designs and increase focus on modularity and advanced loading mechanisms, driving the global market growth.

MARKET RESTRAINTS

Supply Chain Restraints to Limit Market Expansion

Supply chain bottlenecks are likely to restrain the market by limiting access to specialized composites and propellants essential for durable, high-pressure designs. Single-source dependencies on materials such as carbon fiber and ammonium perchlorate create high lead times. Geopolitical sanctions increase shortages, with rare earth processing dominated by adversarial suppliers inflating costs. Export controls delay alternative vendor qualification, stalling production despite major contracts.

MARKET OPPORTUNITIES

Expansion of Air and Missile Defense Stockpile Replenishment Programs to Present Growth Opportunities

The sustained use of interceptor missiles in active conflict zones has created a structural gap between missile consumption and production capacity. Governments are now prioritizing long-term stockpile replenishment contracts to rebuild the depleted inventories of canisterized air defense systems. This presents a significant opportunity for the manufacturers of sealed launch canisters, composite missile tubes, and vertical launch modules. Multi-year procurement frameworks, particularly across NATO, the Middle East, and parts of Asia, are shifting the market from cyclical orders to steady recurring demand. In addition, allied nations are investing in domestic production resilience, opening pathways for joint ventures and localized canister manufacturing, which is expected to present significant opportunities for market growth.

MARKET CHALLENGES

Skilled Workforce Shortages Acts a Challenge for the Market

Skilled workforce shortages critically challenge missile canister production by hindering the precision manufacturing of stealth and modular designs. The demand for composites and CNC experts exceeds supply, with widespread defense vacancies reported. Aging workers and aerospace competition extend training periods per specialist. This slows automated processes such as filament winding for hypersonic canisters, creating challenges for market growth.

Segmentation Analysis

By Launch Mechanism

Geopolitical Tensions and VLS Demand for Rapid Naval Sector to Propel Segmental Growth

Based on launch mechanism, the market is divided into cold launch canister and hot launch canister.

The hot launch canister segment is anticipated to account for the largest missile canister market share. The segment experiences strong growth due to an increasing demand for vertical launch systems (VLS) in naval and ground platforms during geopolitical tensions. Navy forces prioritize hot launch canisters to achieve rapid reaction times critical for defending the narrow, high-threat.

- For instance, in February 2026, Iran’s IRGC Navy demonstrated its Sayyad-3G air defense missile during the "Smart Control of the Strait of Hormuz" with a hot launch, where ignited propellant blasts the missile directly from its canister on the Shahid Sayyad Shirazi corvette's forward vertical launch system (VLS), enabling rapid 360-degree firing without ship maneuvering.

Therefore, these type of canisters enable gas-propelled ejection of missiles directly from internal compartments, maximizing platform space efficiency and payload capacity compared to cold launch alternatives, which drives the growth of the segment.

The cold launch canister segment is anticipated to rise at a steady CAGR of 6.7% over the forecast period.

By Structure

High-Density Configurations Maximizing Firepower Efficiency to Propel Segmental Growth

By structure, the market is segmented into single-cell canister and multi-pack canister.

The multi-pack canisters segment holds the largest market share through their high-density configuration, accommodating multiple missiles within a single robust housing. This design maximizes launch platform efficiency, enabling concentrated firepower from surface combatants, submarines, and ground batteries. Moreover, countries in Europe are focusing on strengthening defense capabilities and upgrade its air defenses.

- For instance, in June 2024, Norway's government signed a USD 500 million contract with Kongsberg Defence & Aerospace for advanced NASAMS systems, including multi-missile canister launchers and Fire Distribution Centers to replace units donated to Ukraine.

In addition, the factors such as naval expansions and army modernization also drive the growth of the segment.

The single-cell canister segment is projected to grow at a steady CAGR of 6.3% over the forecast period.

By Missile Class

Rising Drone and Hypersonic Threats to Push Surface-to-Air Missiles (SAM) Segment Growth

Based on missile class, the market is segmented into Surface-to-Air Missiles (SAM), Surface-to-Surface Missiles (SSM), Anti-Ship Missiles (AShM), and others.

The Surface-to-Air Missiles (SAM) segment accounts for the largest market share due to rising aerial threats from drones, hypersonic weapons, and contested airspace in regions such as Eastern Europe and the Indo-Pacific. These canisters provide protective encapsulation and rapid vertical launch integration for systems such as Patriot PAC-3 and S-400, enabling layered defense from mobile ground platforms and naval vessels.

The anti-ship missiles (AShM) segment is expected to grow at the fastest CAGR of 9.3% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Launch Platform

Significant Role in Mobile Ground Launchers to Support Land Based Segment Growth

Based on launch platform, the market is segmented into land based and sea based.

The land based segment held the largest share in the market in 2025. The segment grows significantly due to their pivotal role in mobile ground launchers addressing territorial defense needs amid such as conflicts and hybrid warfare. These platforms, including truck-mounted TELs for systems such as HIMARS and Iskander, demand ruggedized canisters. Moreover, there is an increase in the demand for canisters resilient to off-road mobility, extreme weather, and rapid dispersal tactics essential for survivability, which drives segment growth.

- For instance, in January 2026, Denmark's MoD signed a USD 117 million deal with Kongsberg for the NSM Coastal Defence System, featuring truck-mobile, land-based canister launchers loaded with >300km-range, long range anti-ship missiles to guard Danish Straits.

The sea-based segment is projected to emerge as the fastest-growing segment at a CAGR of 10.0% over the forecast period.

By Standard

Interoperability in Fleet Modernization for Versatile Missile Loading to Support Mk 41 VLS Canister Segment Growth

On basis of standard, the market is segmented into Mk 41 VLS Canister, Mk 57 Peripheral VLS (PVLS), Mk 56 Guided Missile VLS (GMVLS), SYLVER VLS, TEL-mounted Canister, and others.

The Mk 41 VLS Canister segment is expected to acquire major share in the market as it is a widely adopted standard for vertical launch systems across the U.S. Navy and allied surface combatants. Their quad-pack and strike-length configurations enable versatile loading of SM-6, Tomahawk, and ESSM missiles, maximizing firepower from destroyers and cruisers in carrier strike groups. Proven interoperability and hot-launch reliability drives its utilization in fleet modernization programs, which accelerates the segment growth.

- For instance, in November 2025, BAE Systems secured a USD 22 million U.S. Navy contract to manufacture Mk 41 Vertical Launch System canisters for surface ships, with options potentially reaching USD 317 million following a prior USD 738 million award. These shipboard canisters store, ship, and launch critical missiles such as Tomahawk, Standard variants, and Evolved SeaSparrow from Mk 41/Mk 57 systems, sustaining naval deterrence worldwide.

The TEL-mounted canister segment is projected to emerge as the fastest-growing segment, expanding at a CAGR of 8.4% over the forecast period.

By Material

High Strength-to-Weight Ratio and Corrosion Resistance for Extended Deployments to Support Composite Segment Growth

By material, the market is segmented into metallic, composite, and hybrid.

The composite segment is expected to acquire major share in the market owing to their high strength-to-weight ratio and corrosion resistance critical for extended deployments. These advanced designs, using carbon fiber and Kevlar reinforcements, reduce launcher weight by significant margins while withstanding extreme pressures. The thermal stability of composite material minimizes deformation during rapid salvos, enhancing reliability in naval VLS and mobile missile defense systems.

The hybrid segment is projected to grow at a steady CAGR of 7.2% over the forecast period.

By End User

Defense Modernization and Mobile Precision Strike Needs to Support Army Segment Growth

By end user, the market is segmented into navy, army, and strategic forces.

The army segment dominated the market by end user in 2025 driven by the need for mobile, advanced, precision strike capabilities in land domain. Land forces prioritize strong canisters for truck-mounted and wheeled launchers such as HIMARS, ATACMS, and MLRS, enabling shoot-and-scoot tactics against time-critical targets in hybrid warfare scenarios. In addition, the emphasis on rapid deployment from forward operating bases is expected to propel the growth of the segment.

The navy segment is projected to grow at a steady CAGR of 7.0% over the forecast period.

Missile Canister Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America dominated the missile canister market in 2025 with a valuation of USD 239.3 million. The market is anticipated to reach USD 253.7 million in 2026, driven by surging U.S. DoD investments in naval VLS modernization and Army precision strike expansions during Indo-Pacific and European tensions. Moreover, the surge in requirements for resilient, hot-launch compatible designs in Mk 41/57 systems and HIMARS platforms fuel the demand for composite multi-packs, supporting Tomahawk, SM-6, and ATACMS deployments.

North America Missile Canister Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

U.S. Missile Canister Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be approximated at a value of around USD 232.2 million in 2025. High defense allocations, fleet modernizations, and long range precision fire development initiatives for countering threats are factors contributing to the market growth in U.S.

- For instance, in February 2026, the U.S. Army revealed pictures of Dark Eagle LRHW, hypersonic missile showing the ground-based hypersonic glide vehicle nearing operational deployment as a counter to Russian/Chinese advances. Each mobile Transporter Erector Launcher (TEL) on M870 trailer carries two missile canisters.

Moreover, the presence of major manufacturers such as Lockheed Martin and RTX which prioritize rapid production scaling and stealth enhancements through specialized contracts is driving market growth in the country during the forecast period.

Europe

The Europe market is projected to record a growth rate of 7.8% during 2026 to 2034. The market sustains strong growth propelled by NATO replenishment programs and national defense budget increase following Ukraine conflict depletions. Moreover, surge in Russian aerial threats drive the procurement of VLS canisters for FREMM frigates, Type 31 corvettes, and ground-based systems such as NSM and Aster 30, emphasizing hot-launch modularity for air defense and strike missions. Collaborative frameworks such as OCCAR streamline production scaling, while EU industrial policies prioritize supply chain sovereignty to counter sanctions-induced shortages, driving expansion of the market in Europe.

U.K. Missile Canister Market

In 2025, the U.K. reached a value of around USD 32.5 million, representing roughly 4.6% of global revenues.

Germany Missile Canister Market

The Germany market reached a valuation of approximately USD 35.8 million in 2025, equivalent to around 3.4% of global sales.

Asia Pacific

The Asia Pacific market reached USD 212.9 million in 2025 and secured the position of the second-largest region in the market. The market in Asia Pacific is growing due to territorial tensions in the South China Sea, Taiwan Strait, and Indo-Pacific flashpoints. Naval expansions by Japan, South Korea, India, and Australia drive the demand for Mk 41-compatible VLS canisters on Aegis destroyers and indigenous platforms such as Japan's Maya-class and Australia's Hunter-class frigates. Land-based armies prioritize ruggedized HIMARS-style canisters for mobile strike brigades, exemplified by India's Pinaka and BrahMos mobile regiments.

Japan Missile Canister Market

The Japan market is estimated to reach around USD 16.9 million in 2025, accounting for roughly 3.5% of global revenues.

China Missile Canister Market

The China market is projected to be one of the largest worldwide. The 2025 revenues in the market reached around USD 108.9 million, representing roughly 15.5% of global sales.

India Missile Canister Market

The India market reached a value of around USD 30.7 million in 2025, accounting for roughly 4.4% of global revenues.

Latin America and the Middle East & Africa

The Latin America market registers modest yet steady growth, driven by regional security concerns and modernization of aging defense inventories. Brazil and Chile lead the procurement of naval VLS canisters which contributes to market expansion in the Latin America region. The Middle East & Africa market accelerates through Gulf state procurements and asymmetric conflict demands. Players such as Israel Aerospace Industries dominates with modular composite designs for David's Sling and Arrow interceptors in the region.

Saudi Arabia Missile Canister Market

The Saudi Arabia market reached a value of around USD 5.5 million in 2025, representing roughly 1.5% of global revenues.

COMPETITIVE LANDSCAPE

Focus on Modular Hot-Launch Canisters and Resilient VLS Platforms by Key Players to Propel Market Progress

The global missile canister market remains consolidated, led by major players such as Lockheed Martin, Northrop Grumman, Raytheon Technologies (RTX), Boeing, MBDA, and Kongsberg Defence & Aerospace, which command significant shares through innovations in composite multi-pack designs and advanced launch systems. These firms advance market growth with strategic contracts from U.S. Missile Defense Agency, European defense ministries, and Indo-Pacific allies, emphasizing development of stealth-coated VLS modules, hypersonic-compatible canisters, and modular single-cell configurations for distributed lethality.

- For instance, in October 2025, Lockheed Martin successfully tested its JAGM Quad Launch Canister (JQL) system at Yuma Proving Ground, validating vertical launch capabilities for counter-UAS missions and demonstrating reloadable deep-magazine solutions for naval and ground platforms .

Other prominent players such as BAE Systems, Thales, Israel Aerospace Industries (IAI), and L3Harris Technologies focus on ruggedized land-mobile canisters, automated reload mechanisms for HIMARS platforms, and composite materials for high-temperature hot launches.

LIST OF KEY MISSILE CANISTER COMPANIES PROFILED

- Lockheed Martin Corporation (U.S.)

- Raytheon Technologies (RTX) (U.S.)

- BAE Systems (U.K.)

- Northrop Grumman (U.S.)

- General Dynamics Ordnance & Tactical Systems (U.S.)

- MDBA (France)

- China Aerospace Science and Industry Corporation (CASIC) (China)

- Israel Aerospace Industries (IAI) (Israel)

- Kongsberg Defence & Aerospace (Norway)

- Rafael Advanced Defense Systems (Israel)

KEY INDUSTRY DEVELOPMENTS

- November 2025: The U.S. Navy awarded BAE Systems a USD 22 million contract to produce missile canisters for the MK 41 Vertical Launch System (VLS) and MK 29 Guided Missile Launching System on surface ships, with potential expansion to USD 317 million if options are exercised.

- October 2025: Lockheed Martin successfully tested its JAGM Quad Launcher (JQL) at Yuma Proving Ground launching a government-furnished Joint Air-Ground Missile (JAGM) at a 45-degree elevation from a newly developed canister system.

- January 2025: The Israel Ministry of Defence and IAI finalized a multi-billion-shekel contract to expand production of Arrow-3 interceptors, indirectly supporting ongoing canister production and integration for the Arrow Weapon System.

- October 2024: Stark Aerospace Inc. was awarded a USD 61.45 million contract by the U.S. Naval Sea Systems Command to produce Mk 41 VLS canisters in support of FY24–29 canister production requirements.

- July 2024: BAE Systems secured a USD 738 million contract to produce Mk 41 VLS canisters covering production needs through FY28 for the U.S. Navy.

REPORT COVERAGE

The globalmissile canister market analysis provides an in-depth study of market size & forecast by all the market segmentation included in the report. It includes details on the market dynamics, market trends, and regional analysis expected to drive the market over the forecast period. The market report includes Porter’s five forces analysis which illustrates the potency of buyers and suppliers in the market. The market forecast offers information on the technological advancements, new product launches, key trends, major industry developments, and details on partnerships, mergers, and acquisitions. The market analysis also encompasses detailed competitive landscape with information on the market share and profiles of key major players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.5% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Launch Mechanism, By Structure, By Missile Class, By Launch Platform, By Standard, By Material, By End User, and Region |

| By Launch Mechanism |

|

| By Structure |

|

| By Missile Class |

|

| By Launch Platform |

|

| By Standard |

|

| By Material |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 702.4 million in 2025 and is projected to reach USD 1,342.8 million by 2034.

In 2025, the market value stood at USD 239.3 million.

The market is expected to exhibit a CAGR of 7.5% during the forecast period of 2025-2034.

By missile class, the Surface-to-Air Missiles (SAM) segment is expected to lead the market.

The increase in geopolitical tension and expansion of missile production are key factors driving market expansion.

BAE Systems (U.S.), Lockheed Martin (U.S.), Raytheon Technologies (U.S.), and General Dynamics Ordnance & Tactical Systems (U.S.), among others are some of the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 201

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us