Surface-to-Air Missiles Market Size, Share, Industry & Russia-Ukraine War Analysis, By Range (Very Short-Range, Short-Range, Tactical Medium-Range, Strategic Medium-Range, and Others), By Component (Airframe & Materials, Sensors & Seeker Heads, Navigation & Control System, Propulsion Systems, and Others), By EW Resistance (Class 1, Class 2, Class 3, and Others), By Guidance System (Infrared Homing (IIR), Laser/Optical Guidance, Command Guidance, and Others), By Launch Mode (Man-Portable Air Defense Systems, Vehicle-Launched, Mobile Missile Systems, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

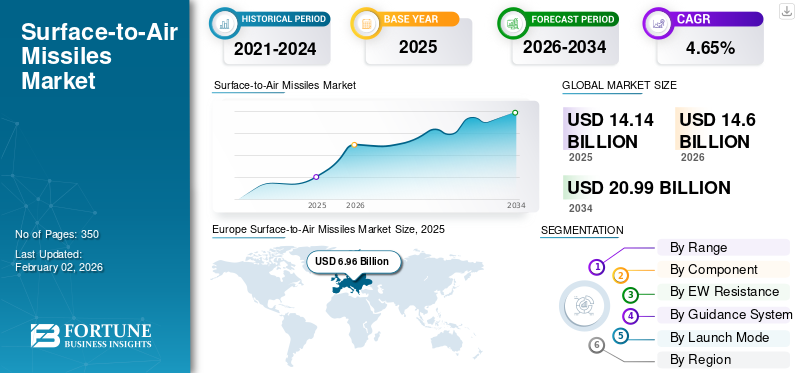

The global Surface-to-Air Missiles market size was valued at USD 14.14 billion in 2025. It is projected to grow from USD 14.60 billion in 2026 to USD 20.99 billion by 2034, exhibiting a CAGR of 4.65% during the forecast period. Europe dominated the Surface-to-Air Missiles market with a market share of 49.26% in 2025.

Surface-to-air missiles are guided weapons launched to destroy aerial targets such as helicopters, drones, missiles, and enemy aircraft. These can be stationary or mobile and are available for a range intended to protect vast areas and strategic assets. These missiles heavily rely on guidance technologies such as optical tracking, infrared, radars, and others, to detect and interpret threats in real time. SAMs are critical components for an integrated defense system, deployed by military forces globally that offer layered protection and enhance national safety capabilities against attacks and intrusions. Some advanced systems, such as the Russian S-4000 and U.S. Patriot, can engage multiple targets at the same time.

The global surface-to-air missiles market is expected to experience high growth due to growing geopolitical tensions, increasing defense budgets, and the growth of aerial threats including stealth aircraft, drones, and hypersonic weapons. Additionally, surge in defense expenditure, growing geopolitical tension, and increasing advances in aerial threats are expected to bolster market growth. As countries advance toward modernization of air defense technology to protect national security, a surge in asymmetric warfare escalates the need for advanced warfare to counter these threats. Technological advancements such as real-time tracking, radar tech, command and control, and advanced GPS are expected to lead to a rise in demand for the product in the forthcoming years. Raytheon Technologies Corporation, Lockheed Martin Corporation, and Northrop Grumman Corporation are some of the major players in the market, driving growth through heavy investments in research and development of complex advanced air combat and missile defense systems.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Increasing Threat from Unmanned Aerial Vehicles (UAVs) and Cruise Missiles to Fuel Demand for Surface-To-Air Missiles

Increasing threat from Unmanned Aerial Vehicles (UAVs) and cruise missiles has compelled countries to expand and upgrade their air defense systems. Advanced warfare involves a primary use of drones for surveillance, precision strikes, and others, making them an effective and low-cost alternative. Even in the ongoing Russia-Ukraine conflict, both the countries have been heavily relying on Unmanned Aerial Vehicles (UAVs) such as Iran-based Shaheed and Turkey-based Bayraktar TB2. Similarly, Israel uses the Iron Dome and David sling system to identify and intercept threats such as rockets and UAVs fired from Gaza. Countries including India have promptly responded to this by acquiring advanced systems such as Russia-based S-4000, which has evidently helped them counter attacks from Pakistan.

The accessibility and cost-effectiveness of UAVs to rogue nations and terrorist groups have led to a rise in demand for effective modern warfare and countermeasures to neutralize attacks and threats. Therefore, an evolution of aerial warfare is a primary catalyst driving demand for SAM advances globally.

Market Restraints

High Procurement, Operation, and Maintenance Costs to Limit Market Growth

High procurement, maintenance, and operation costs are major factors limiting the growth of the surface-to-air missiles market. The advanced technology and complex manufacturing processes involved in generating advanced SAM systems add to the high upfront costs. These ongoing costs can be substantial over the lifespan of the system, adding to the overall financial load. This includes the costs of raw materials, R&D, and dedicated manufacturing facilities. Surface-to-air systems require continuous maintenance, upgrades, and trained personnel to operate. This high costs can restrain low economies needing them to allocate larger defense budgets. Developing nations, despite recognizing the strategic importance of SAM systems, may struggle to afford them, thereby limiting the market expansion.

Additionally, the development of countermeasures by potential enemies further increases the cost of air defense systems. These systems need to be continuously adapted and upgraded to counter various evolving threats and remain effective, leading to higher research and development expenses. These costs act as a major barrier to entry, particularly for underdeveloped or developing nations with limited defense budgets, impeding the widespread adoption and deployment of advanced air defense systems.

Market Opportunities

Rising Geopolitical Tensions and Regional conflicts Needs Fuel Market Growth Opportunities

Geopolitical tensions and territorial security requirements are driving the global demand for cutting-edge defense systems, particularly missiles, as nations seek to bolster deterrence in the middle of increasing conflicts. Growing defense budgets, such as China's 7.2% increase in 2025 (according to industry experts) to protect national security, showcases a larger drift of military modernization due to regional uncertainties.

Global defense budgets are growing, with countries raising investments in military modernization and to bolster their air defense capabilities. This development is partially fueled by the ongoing wars, geopolitical volatility, and regional conflicts, prompting nations to bolster their defense capabilities. Rising geopolitical tensions and the proliferation of advanced weapons systems are creating a need for countries to acquire and deploy effective air defense systems, which is expected to contribute to the high market growth in the forthcoming years.

Surface-to-Air Missiles Market Trends

Multi-Platform Integration and Advancements in Hyperspectral Technologies to Amplify Product Demand

The development of surface-to-air missiles (SAMs) is currently marked by a trend toward advanced, longer-range systems and a growing emphasis on creating multi-layered air defense networks. Additionally, a significant shift toward domestic production and procurement within many countries, particularly in regions such as India, driven by a desire for greater self-reliance in defense capabilities is an emerging market trend. Development of SAMs with extended ranges to counter threats including faster aircraft, ballistic missiles, and drones is a major focus. Systems such as Project Kusha in India aim to provide long-range interception capabilities against high-speed threats. To address diverse threats at different altitudes and ranges, countries are developing integrated air defense systems by incorporating multiple layers of protection, including short, medium, and long-range SAMs, as well as radar systems and electronic warfare capabilities.

Download Free sample to learn more about this report.

Impact of Russia-Ukraine War

Ongoing War Conditions and Geopolitical Tensions Significantly Influenced Market, Driving Demand for Advanced Warfare Technologies

The global surface-to-air missiles market is experiencing significant growth, primarily fueled by ongoing conflicts and rising geopolitical tensions worldwide. This growth is further driven by advancements in missile technology, including extended ranges, enhanced accuracy, and integration with advanced sensors and AI. Increased defense spending and modernization efforts by various nations are also key factors contributing to the market's expansion.

Conflicts such as the ongoing war between Russia and Ukraine have significantly increased demand for SAM systems, as nations prioritize bolstering their air defense capabilities. Many countries are modernizing their air defense systems, replacing older platforms with advanced, long-range, and hypersonic-capable SAMs. Nations are allocating larger portions of their defense budgets to missile systems, including SAMs, to protect national interests and deter potential challengers. Ongoing territorial disputes and regional conflicts are driving demand for SAMs in various parts of the world, particularly in Asia Pacific. Innovations in propulsion, guidance, and warhead design are leading to the introduction of missiles with increased ranges, enabling them to engage targets at greater distances. Integration of advanced sensors, AI, and network-centric capabilities enhances situational awareness and enables faster, more accurate targeting. The development of hypersonic weapons is driving the need for advanced SAM systems capable of intercepting these threats.

SEGMENTATION ANALYSIS

By Range

Short-range Surface-to-Air Missiles Dominated the Market, Propelled by Technological Advancements

By range, the market is divided into Very Short-Range (V-SHORAD) (Below 5 km), Short-Range (SR-SAMs) (5 - 15 km), Tactical Medium-Range (15 - 40 km), Strategic Medium-Range (40 - 70 km), Long-Range (LR-SAMs) (70 - 200 km), and Very Long-Range (Above 200 km).

The Short Range SAM segment accounted for a dominating market share and is expected to grow at the fastest CAGR in the forthcoming years. The growth of short-range surface-to-air missiles (SHORAD) is driven by the growing need for effective defense against a variety of aerial threats, particularly in close proximity to ground forces or critical infrastructure. This includes protection against low-flying aircraft, helicopters, drones, and cruise missiles, which are increasingly prevalent in modern warfare. SHORAD systems are crucial for safe-guarding ground troops and critical assets from air attacks during maneuver warfare, and are also vital for defending airbases and other strategic locations.

The long-range SAM segment is expected to grow at a significant CAGR over the forecast period. Growth in long-range surface-to-air missile (SAM) systems is due to the increasing sophistication and range of airborne threats, including aircraft, cruise missiles, and ballistic missiles. These threats necessitate longer-range defensive capabilities to protect critical assets and infrastructure. Modern air warfare is characterized by advanced aircraft, stealth technology, and a proliferation of cruise and ballistic missiles, demanding longer-range interception capabilities. Long-range SAMs are crucial for defending against a wide range of aerial threats, including aircraft, cruise missiles, and even ballistic missiles, protecting both strategic and tactical assets.

To know how our report can help streamline your business, Speak to Analyst

By Component

Preference for Lightweight Components Led to the Dominance Of Airframe & Materials Segment

By component, the market is divided into airframe & materials, sensors & seeker heads, navigation & control systems, propulsion systems, guidance systems, and warheads.

The airframe & materials segment accounted for a dominating market share in 2024. The segment is witnessing tremendous growth due to the increasing demand for lightweight, high-strength, and heat-resistant materials that improve missile performance. Advanced SAM missiles are expected to operate at high speeds such as Mach 2 and above, under high environmental stress. Traditional airframes are readily being replaced with advanced alloys, composite materials, and high-temperature ceramics. These materials enhance maneuverability, payload capacity, and range while reducing the missile’s radar cross-section. For instance, Russian S-400, U.S. Patriot PAC-3, and many other new-age missiles are heavily pushing R&D in airframe design and optimization of aerodynamics.

The sensors & seeker heads segment is expected to grow at the highest CAGR over the forecast period. The growing need for precision strikes and enhanced electronic warfare (EW) resistance in modern SAM missile systems is driving the segment growth. As air threats evolve in drones, aircraft, and hypersonic missiles, countermeasures require multi-mode seekers combining radar, IIR, and optical sensors to ensure target interception, tracking, and acquisition. This, in turn, has led to high investments in advanced infrastructure to support and aid in operations of air defense systems. Technologies such as active electronically scanned array (AESA) radars, semi-active laser homing, imaging infrared seekers, among others, are being highly used in next-gen missiles such as Barak-8, Akash-NG, Aster, and others.

By EW Resistance

Increase in Demand For Affordable Electronic Warfare Resistance To Drive Class 4 Segment Growth

By EW Resistance, the market is divided into Class 1, Class 2, Class 3, Class 4, and Class 5.

The class 4 segment dominated the market in 2024 and is expected to grow at a significant CAGR in the forthcoming years. Increasing sophistication of airborne electronic attack capabilities and the urgent need to counter advanced jamming techniques contributes to the segment’s dominance. Class 4 electronic warfare resistance provides signal encryption, adaptive frequency hopping, anti-deception algorithms, and advanced filtering features. These are essential to create a defensive infrastructure against modern countermeasures used by fifth-generation UAS and fighter jets. These systems are also cost-effective and easy to integrate with traditional platforms. A rise in regional conflict, stealth aircraft, and swarm threats, fuels defense budgets for EW-resistance modernization of missiles. Class 4 EW-resistance works as a complete balance between affordability and performance, making it the most practical upgrade for countries modernizing their air defense systems without reinvesting in full potential, therefore leading to segment growth.

The Class 5 segment is expected to grow at the highest CAGR in the forecast period. This is due to an increase in threat from spoofing, multi-spectral jamming, decoy, and GPS denial countermeasures deployed by technologically advanced systems. Class 5 acts as a top-tier electronic warfare defense system, which also offers AI support for threat analysis, adaptive waveform generation, real-time ECM adaptation, and multi-sensor fusion, thereby making it vital for high-threat environment operations. Countries such as the U.S. and Israel are heavily investing in class 5 capable systems such as S-500 and Barak-8ER. Additionally, rising focus on network-centric defense framework requires surface-to-air missiles that can continue target tracking along with surviving EW attacks. As threats evolve and traditional air defense systems become increasingly vulnerable, defense forces around the world are shifting toward class 5 EW resistance, thereby leading to segment growth.

By Guidance System

Increased Demand for Precision Targeting Led To Infrared Homing (IIR) Segment’s Dominance

By Guidance System, the market is divided into Infrared Homing (IIR), Laser/Optical Guidance, Command Guidance, Active Radar Homing (Active RF) / AESA, SALH + GPS/INS, (Semi-Active Laser Homing + GPS/ Inertial Navigation System), and Dual Mode (Radar + IIR).

The infrared homing segment dominated the global market in 2024 and is expected to grow at a significant CAGR in the forecast period. Infrared homing (IIR) is capable of passive targeting, resistant to radar jamming, and provides increased precision targeting close-range low-altitude targets, thereby being a primary choice for major air defense systems by defense forces worldwide. IR homing seekers track thermal signatures of enemy missiles, UAVs, or aircraft, enabling “fire and forget” operation to reduce workload and improve survivability. The new-gen IIRs offer lock-on-after-launch (LOAL) wherein targets can be acquired from multiple directions, long after missile deployment. Modern IIRs are also equipped with Focal Plane Arrays (FPA) with high-resolution thermal imaging to differentiate between real targets and decoys.

The SALH + GPS/INS (Semi-Active Laser Homing + GPS/ Inertial Navigation System) segment is estimated to grow at the highest CAGR over the forecast period. The guidance system’s utility in mid and long-range missiles, multiple targets engagement, and high ECM resilience operation gives them an advantage and preference over other guidance systems, thereby leading to the segment growth. SALH- leads to terminal accuracy, even in the least of radar signatures or in cluttered terrain. GPS- a satellite-based positioning system and IMUs, guide the missile with precision even on extended ranges. These technologies together provide an utmost precision strike with the least amount of human intervention, therefore leading to a substantial segment’s growth in the forthcoming years.

By Launch Mode

Cost Effectiveness, Deployability, and Ease in Operations Led To Vehicle-Launched Accounting for Leading Share

The market is segmented into Man-Portable Air Defense Systems (MANPADS), Vehicle-Launched, and Vertical Launch Systems.

The vehicle-launched segment accounted for a dominating market share in 2024 and is expected to grow at a significant CAGR in the forthcoming years. Defense forces around the world widely use vehicle-launched platforms as it offers an extended range, mobility, and integration with advanced command and radar systems, making them ideal for tactical and strategic air defense. These systems are usually mounted on tracked or wheeled vehicles and equipped with long-range missile systems. VL-SAMs are often equipped with electro-optical targeting, data-link enabled guidance, and a highly configured network radar system, enabling real-time tracking; Therefore, these are highly preferred by defense agencies around the world.

The man-portable air defense system is expected to grow at the highest CAGR in the forthcoming years. Ongoing regional conflicts Eastern Europe, Asia Pacific, and the Middle East have established the necessity of MANPADS to protect critical infrastructure, civilian populations, and military resources from aerial threats. Additionally, the growth in demand for Unmanned Aerial Vehicles (UAVs) for reconnaissance and surveillance has also increased the demand for MANPADS as a means of countering these potential threats. Continuous innovation in areas such as guidance systems, propulsion, and materials has made MANPADS more effective and user-friendly, further fueling their adoption.

Surface-to-Air Missiles Market Regional Outlook

By region, the market is studied into North America, Europe, Asia Pacific, and the rest of the world.

North America

Europe Surface-to-Air Missiles Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, North America held 37.08% of the global market share, reaching a valuation of USD 5.24 billion, and is projected to grow to USD 5.39 billion in 2026. North America, mainly the U.S. market is rising rapidly due to an increase in defense modernization and geopolitical strains around the globe. Innovations in missile guidance systems, radar technology, and propulsion are making SAMs more effective and versatile, leading to its increased adoption. The U.S. has invested in systems such as the National Advanced Surface-to-Air Missile System (NASAMS) and the PAC-3 missile system to improve detection and engagement range. The U.S. Army is also expanding its Patriot missile battalions to address operational demands, thereby leading to an overall regional growth. The U.S. market is projected to reach USD 3.29 billion by 2026.

Europe

The market in Europe reached USD 6.96 billion in 2025, representing 49.26% of total market revenue, and is projected to reach USD 7.2 billion in 2026. due to heightened geopolitical tensions and the need for robust air defense systems to counter evolving threats. Increased defense spending, particularly on advanced missile systems, and modernization efforts to replace outdated systems are also significant factors contributing to the regional market growth. Collaborative efforts such as ESSI (European Sky Shield Initiative) aim to standardize and procure air defense systems across Europe, fostering interoperability and potentially reducing costs through shared development and procurement. The UK market is projected to reach USD 2.74 billion by 2026, while the Germany market is projected to reach USD 1.45 billion by 2026.

Asia Pacific

Asia Pacific contributed approximately USD 1.21 billion to the global market in 2025, accounting for 8.57% share, and is expected to reach USD 1.27 billion in 2026. The Asia Pacific region is expected to witness the highest CAGR in the market during the forecast period. Ongoing conflicts and tensions, particularly in areas including the South China Sea, the India-Pakistan border, and the Korean peninsula, have heightened the need for stronger air defense capabilities. The development and deployment of indigenous hypersonic missiles by some countries, such as India, have further driven the need for advanced air defense systems capable of countering this emerging threat. The Japan market is projected to reach USD 0.26 billion by 2026, the China market is projected to reach USD 0.38 billion by 2026, and the India market is projected to reach USD 0.18 billion by 2026.

Rest of the World

The rest of the world is expected to experience significant growth during the forecast period. The increased deployment and development of surface-to-air missile (SAM) systems in the Middle East are largely driven by regional security concerns, including the proliferation of ballistic missiles, drone attacks, and ongoing conflicts. The growth of surface-to-air missiles (SAMs) in Latin America is primarily driven by the modernization of armed forces and the need to enhance air defense capabilities against emerging threats, including drug trafficking and other activities.

Competitive Landscape

Key Market Players

Leading Players Are Focusing on Integrating Advanced Technologies for Precision Strikes

The market is vastly competitive, including key players such as Raytheon Technologies Corporation, Lockheed Martin Corporation, Thales Group, BAE Systems plc, and Northrop Grumman Corporation. These businesses are highly focused on accuracy, supersonic/hypersonic capabilities, stealth, guidance, and extended range.

AI-based targeting and vertical launch capabilities strengthen competition in the market. Defense export policies, strategic alliances, and indigenous development are key factors enabling competitive edge for the market.

LIST OF KEY SURFACE-TO-AIR MISSILES COMPANIES PROFILED

- Raytheon Technologies Corporation (U.S.)

- Lockheed Martin Corporation (U.S.)

- MBDA (France)

- Northrop Grumman Corporation (U.S.)

- BrahMos Aerospace (India)

- Thales Group (France)

- BAE Systems (U.S.)

- Rafael Advanced Defense Systems (Israel)

- China Aerospace Science and Technology Corporation (CASC) (China)

- Kongsberg Defence Aerospace (Norway)

- Bharat Dynamics Limited (India)

- Rosoboron export (Russia)

KEY INDUSTRY DEVELOPMENTS

- June 2025- DRDO, India, won a contract from the Indian Ministry of Defense to produce indigenously made quick reaction surface-to-air missile (QR-SAM) systems for the Army.

- February 2025- The French defence procurement agency (DGA) unveiled an order for 530 Appui SCORPION armored vehicles for the French Army that support a Surface-to-air missiles system. The contract marks a major step in military modernization, with deliveries scheduled between late 2025 and 2031.

- January 2025- The defense ministry of India unveiled a contract worth USD 345.2 million with Bharat Dynamics Limited to supply Medium-Range Surface-to-Air Missiles (MR-SAM) for the Indian Navy.

- November 2024- Kongsberg Defence & Aerospace, a pioneer defence OEM, unveiled a contract with the Netherlands government to supply NASAMS, a type of advanced surface-to-air missile, and NOMADS air defence systems. The contract is worth USD 1.18 million.

- September 2024- The U.S. Navy awarded a contract to Raytheon Technologies worth USD 1.1 billion to produce AIM-9X Block II missiles. This contract is expected to increase production to 2,500 missiles per year.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on important aspects, such as key players, products, applications, and platforms, depending on various countries. Moreover, it offers deep insights into the market trends, competitive landscape, market competition, pricing of surface-to-air missiles, and market status, and highlights key industry developments. In addition, it encompasses several direct and indirect factors that have contributed to the global surface-to-air missiles market growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.65% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation

|

By Range

|

|

By Component

|

|

|

By EW Resistance

|

|

|

By Guidance System

|

|

|

By Launch Mode

|

|

|

By Region

|

Frequently Asked Questions

According to the Fortune Business Insights study, the global market was valued at USD 14.14 billion in 2025 and is anticipated to be USD 20.99 billion by 2034.

The market is likely to grow at a CAGR of 4.65% during the forecast period.

The top players in the industry are Lockheed Martin Corporation, Raytheon Technologies Corporation, and Northrop Grumman Corporation.

Europe dominated the global market.

Increasing Threat from Unmanned Aerial Vehicles (UAVs) and Cruise Missiles to Fuel Demand for Surface-To-Air Missiles.

Multi-Platform Integration and Advancements in Hyperspectral Technologies to Amplify Product Demand.

- 2021-2034

- 2025

- 2021-2024

- 350

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us