Mobile Gaming Market Size, Share & Industry Analysis, By Game Type (Shooter, Action, Sports, Role Playing, and Others), By Platform (Android, iOS, and Others), By Business Model (In-app Purchase, Advertising, and Paid Purchases), By End-user (Male and Female), and Regional Forecast, 2026-2034

(Offer valid till 30th Jun 2026)

KEY MARKET INSIGHTS

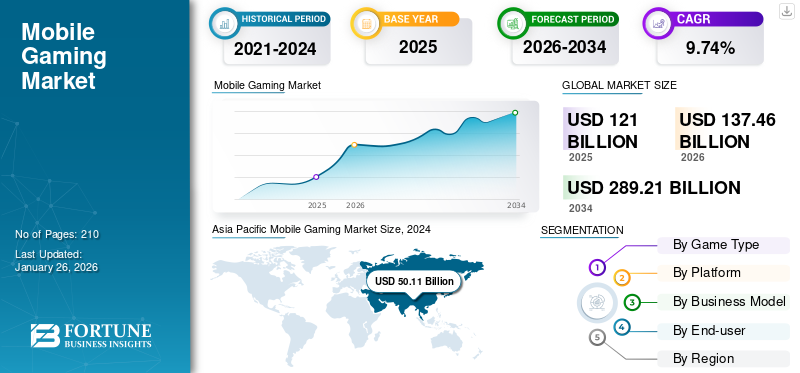

- The mobile gaming market size is projected to grow from USD 137.46 billion in 2026 to about USD 289.21 billion by 2034, reflecting a compound annual growth rate (CAGR) of around 9.74% during the forecast period.

- Adoption of mobile gaming is expected to accelerate with increasing smartphone penetration, improving internet connectivity, and rising consumer preference for digital entertainment experiences.

- Although the industry continues to evolve, mobile gaming has become a major component of the global gaming ecosystem, supported by expanding in-app monetization models and growing engagement across diverse game genres.

- Asia Pacific currently leads the global mobile gaming market, accounting for 47.04% of market share in 2024, supported by a large player base, strong smartphone adoption, and the presence of major gaming publishers across countries such as China, Japan, and South Korea.

The global mobile gaming market size was valued at USD 121 billion in 2025, and it is projected to grow from USD 137.46 billion in 2026 to USD 289.21 billion by 2034, exhibiting a CAGR of 9.74% during the forecast period. Asia Pacific dominated the mobile gaming market with a market share of 47.04% in 2024.

The rise of e-sports has transformed mobile gaming into a competitive sport, attracting both players and spectators on a global scale. Large-scale tournaments and leagues have emerged as major drivers of the market growth. Several companies, such as Electronic Arts, Nintendo Co., Ltd., NetEase, Inc., and Gameloft SE, are investing heavily in high-quality e-sports by organizing and sponsoring tournaments while also incorporating augmented reality (AR) and virtual reality (VR) into mobile games. These innovations are further boosting the industry's visibility and broadening its appeal.

Furthermore, high-speed internet access, particularly with the rollout of 5G networks, provides a seamless gaming experience. This enhances overall gameplay quality, making smartphone gaming more attractive to consumers and leading to an increase in average revenue per user within the market.

For instance, according to data from 5G Americas, an industry trade organization, as of the first quarter of 2024, global 5G connections have reached approximately 2 billion, with an increase of 185 million new connections. Projections indicate that this number will rise to 7.7 billion by 2028.

The global mobile gaming market continues to represent one of the most resilient segments within the digital entertainment economy. Sustained smartphone penetration, improvements in mobile processors, and expanding internet accessibility are supporting long-term market expansion. The industry has evolved from a casual gaming ecosystem into a sophisticated platform encompassing competitive gaming, social interaction, digital commerce, and immersive experiences.

Mobile gaming market growth is increasingly influenced by advancements in cloud gaming infrastructure, artificial intelligence-driven personalization, and the integration of live service models. Publishers are focusing on recurring monetization strategies through subscriptions, advertising, battle passes, and in-app purchases. These approaches are improving lifetime customer value while reducing reliance on premium game sales.

Asia-Pacific maintains a dominant position in the mobile gaming market share due to its extensive user base and mature digital ecosystems. North America and Europe continue to generate strong revenue contributions through premium spending behavior and advanced monetization models. Emerging economies are creating additional opportunities through rising smartphone adoption and expanding digital payment capabilities.

The competitive landscape is characterized by strong participation from global publishers, platform providers, and independent developers. Strategic investments in intellectual property, user acquisition technologies, and cross-platform experiences are reshaping industry dynamics. Artificial intelligence, augmented reality, and cloud-enabled delivery are expected to influence future competitive positioning.

Download Free sample to learn more about this report.

Mobile Gaming Market KEY TAKEAWAYS

- 2025 Market Size: USD 121.00 Billion

- 2026 Market Size: USD 137.46 Billion

- 2034 Forecast Market Size: USD 289.21 Billion

- CAGR: 9.74% from 2026–2034

- Asia Pacific dominated the mobile gaming market with a 47.04% share in 2024.

- The shooter segment captured the maximum share of the market.

- The Android segment is expected to dominate the market during the forecast period.

Asia Pacific

Asia Pacific held a 47.44% share in 2024, driven by smartphone adoption and gaming demand.

Europe

Europe is growing due to esports popularity, fan engagement, and AR/VR adoption in gaming.

North America

North America is driven by major game developers, esports investments, and cloud gaming adoption.

U.S.

Leading developers, cloud gaming, AR/VR integration, and platform innovation drive market growth.

Japan

Consumer loyalty, in-app purchases, and a mature gaming ecosystem drive market growth.

Read More

Mobile Gaming Industry Trends

Increasing User Penetration in the Gaming World to Boost Market Growth

The percentage of the population actively involved in the gaming world plays a vital role in shaping the market trend of mobile gaming. As user penetration increases, the number of individuals playing games on mobile phones also rises, which boosts the overall market growth of mobile-based gaming. Besides, the expanding user base creates a larger market for developers and publishers, leading to higher revenues for the market.

The mobile gaming market is undergoing rapid transformation driven by technological innovation and evolving consumer expectations. Live service models have emerged as a defining trend, enabling publishers to deliver continuous content updates and maintain long-term engagement. Seasonal events, battle passes, and community-driven features are becoming central to monetization strategies.

Cross-platform gaming is gaining momentum across the industry. Consumers increasingly expect seamless experiences across smartphones, tablets, consoles, and personal computers. Publishers are investing in unified ecosystems that support synchronized progression and social connectivity.

Artificial intelligence is reshaping game development and player engagement. AI-enabled systems are improving matchmaking, personalization, and content recommendations. These capabilities are helping developers optimize retention and enhance user experiences.

Cloud gaming technologies are expanding accessibility by reducing hardware limitations. Improvements in connectivity infrastructure are enabling high-quality streaming experiences and creating opportunities for broader audience participation. Subscription-based gaming ecosystems are also attracting increasing consumer interest.

Mobile Gaming Market Drivers

Growing Smartphone Usage and Rollout of 5G Networks to Support Market Growth

The increasing availability and affordability of smartphones have broadened the audience for mobile gaming. As more people own smartphones, the potential market for mobile games expands, particularly in emerging regions. Modern smartphones offer advanced processors, high-resolution displays, and dedicated GPUs, enabling developers to create more immersive mobile gaming experiences.

Besides, the rollout of 5G networks and advancements in cloud gaming technology improve connectivity, allowing for smoother online multiplayer gameplay and support for more complex game mechanics. These technological improvements are attracting a wide range of users, from casual players to hardcore gamers. For instance, currently, more than half of the global population, approximately 4.3 billion people, possess smartphones, as reported in the GSMA's 2023 State of Mobile Internet Connectivity Report.

The mobile gaming industry is benefiting from structural shifts in digital entertainment consumption. Rising smartphone penetration and expanding internet connectivity continue to increase the addressable player base across developed and emerging economies. Improvements in device performance are enabling publishers to deliver graphics-intensive experiences that were previously limited to consoles and personal computers.

The proliferation of fifth-generation wireless networks is improving download speeds and reducing latency. These developments are supporting multiplayer gaming, cloud-based experiences, and real-time interactions. Enhanced accessibility is increasing user engagement and encouraging higher spending across multiple game genres.

Monetization innovation represents another important growth catalyst. In-app purchases, advertising, and subscription models are enabling developers to diversify revenue streams while improving customer lifetime value. Live service strategies are further strengthening player retention and recurring engagement.

The emergence of competitive gaming ecosystems is expanding audience participation. Esports tournaments, influencer marketing, and social media integration are increasing user acquisition and extending game lifecycles. Publishers are increasingly investing in community-driven experiences to maintain long-term engagement.

Market Restraints

Increasing Data Privacy Concerns to Limit Market Growth

The enforcement of new regulations, such as the Digital Market Act and privacy laws, requires mobile game developers to invest more in compliance efforts, which can be costly and time-consuming. Therefore, the need to balance privacy with monetization can lead to the adoption of less effective revenue models, potentially reducing overall market revenue. Besides, gamers are increasingly concerned about data privacy, with many willing to delete apps or stop supporting companies involved in data breaches. This may lead to reduced user retention, negative publicity, and reduced average revenue per user (ARPU), impacting market growth.

Despite favorable fundamentals, several factors continue to constrain industry expansion. Intensifying competition among publishers has significantly increased customer acquisition costs. User retention remains challenging as consumers have access to a large and fragmented content ecosystem. Developers are required to continuously invest in updates and marketing initiatives to sustain engagement levels.

Regulatory scrutiny is increasing across several markets. Governments are implementing stricter policies related to privacy, digital advertising, monetization practices, and youth protection. Restrictions on playtime and content approvals can affect revenue generation and delay market entry.

Platform dependency represents another challenge. Publishers remain heavily reliant on dominant application marketplaces for distribution and payment processing. Changes in platform policies, commission structures, or visibility algorithms may influence profitability and competitive positioning.

Market Opportunities

Emerging Technologies and Innovations to Offer Market Opportunity

The integration of Augmented Reality (AR) and Virtual Reality (VR) technologies into mobile games offers immersive gaming experiences, attracting a wide range of gamers. This enhances user engagement and retention, driving mobile gaming market growth. Additionally, AI creates personalized gaming experiences by adapting difficulty levels and content based on player behavior, enhancing user satisfaction, and encouraging longer play sessions.

Besides, AR and VR unlock innovative gameplay formats that combine the physical and digital worlds, creating unique and captivating experiences for users. For instance, in October 2023, Nextech3D.ai launched AR-based games within its newly developed AR-powered mobile app, designed for trade show organizers. This innovative app integrates AR technology to enhance attendee engagement and provide unique sponsorship opportunities.

Emerging economies represent significant opportunities for long-term industry expansion. Rising smartphone affordability and improving internet infrastructure are increasing access to digital entertainment across Asia, Latin America, Africa, and the Middle East. Expanding digital payment ecosystems are supporting monetization efficiency in these regions.

Cloud gaming presents an important avenue for future growth. Reduced dependence on high-end hardware allows publishers to reach broader audiences while lowering barriers to entry. Improvements in network infrastructure are expected to accelerate adoption over the coming years.

Artificial intelligence offers opportunities across content creation, personalization, and operational efficiency. AI-assisted development tools can reduce production timelines while enhancing scalability. Advanced analytics also enable publishers to optimize monetization and improve user engagement.

Advertising innovation represents another attractive opportunity. Programmatic technologies and rewarded advertising formats are creating more effective monetization strategies without compromising user experience. Hybrid revenue models are gaining wider acceptance among publishers.

By Game Type Analysis

Strong Community Engagement Encouraged Shooter Segment Expansion

Based on game type, the market is divided into shooter, action, sports, role-playing, and others.

Shooter

The shooter segment captured the maximum share of the market. Shooter games, specifically those featuring multiplayer modes, foster strong community engagement and competitive spirit. This encourages player retention and attracts new users through social interactions and eSports events, which boosts segment growth.

Action

Action games maintain broad appeal due to their accessibility and immersive gameplay mechanics. Developers are introducing increasingly sophisticated visual environments and story-driven experiences. The segment attracts both casual and experienced users across multiple age groups. High engagement levels contribute to sustained monetization opportunities.

Frequent content updates support user retention and lifetime value. Artificial intelligence-enabled personalization is improving player experiences. Social features and cooperative modes are becoming more common. These trends are reinforcing long-term mobile gaming market growth.

Sports

Sports games benefit from strong consumer affinity toward established leagues and franchises. Real-time competitions and multiplayer formats are increasing player engagement. Publishers continue to expand licensing partnerships to enhance authenticity and attract loyal audiences. Seasonal updates also encourage recurring spending.

Fantasy sports integration and esports tournaments are creating additional revenue opportunities. Advertising partnerships remain particularly effective within this segment. Mobile gaming market trends indicate rising demand for social and competitive experiences. Sports titles are expected to maintain stable growth prospects.

Role Playing

Role-playing games account for a significant share of industry revenues. Rich narratives and character development systems encourage extended engagement periods. Players frequently invest in customization features and premium content. These characteristics support attractive monetization dynamics.

Advances in graphics technologies are enhancing immersion levels. Cloud gaming capabilities are expanding accessibility across devices. Publishers are increasingly integrating social interaction features to improve retention. This segment remains a major contributor to the mobile gaming market size.

Others

Puzzle, strategy, simulation, and casual games collectively represent an important component of the industry. Their accessibility attracts a broad demographic base. Lower hardware requirements support adoption in emerging economies. Advertising-based monetization models remain highly effective.

Many casual titles achieve rapid scalability through viral user acquisition. Short gameplay sessions align with changing consumer lifestyles. Developers continue to experiment with hybrid gameplay models. These factors contribute to sustained segment expansion.

The other segment is expected to grow at the fastest CAGR in the near term. This category includes puzzle games, card games, and popular titles such as Candy Crush Saga. These games are categorized under casual gaming, which is easy to pick up and play, making them accessible to a wide audience, including casual gamers.

By Platform Analysis

Android Segment to Dominate Owing to Its User-Friendly Nature and Affordability

On the basis of the platform, the market is segmented into Android, iOS, and others.

Android

The Android segment is likely to lead the market during the estimated period. Android devices are generally more affordable than iOS devices, making them accessible to a wider demographic. This affordability contributes to a larger potential market for Android games. Moreover, Android offers a developer-friendly environment with tools, such as Android Studio, making it easier for developers to create and distribute games.

Android maintains the largest mobile gaming market share due to its extensive global user base. Affordable smartphone availability supports adoption across developing economies. The ecosystem provides broad access to diverse content categories. These advantages strengthen revenue opportunities for publishers.

Regional manufacturers continue to improve device capabilities. Expanding internet connectivity supports multiplayer and cloud gaming experiences. Flexible pricing structures enhance accessibility. Android is expected to remain the dominant platform during the forecast period.

iOS

The iOS segment is anticipated to grow at the fastest CAGR in the upcoming years. iOS users spend more on in-app purchases compared to Android users, making iOS a lucrative platform for developers seeking high revenue per user. This higher spending power attracts developers to create premium content for iOS. Additionally, iOS tends to attract a demographic with higher disposable income, further contributing to its revenue growth.

The iOS ecosystem generates strong monetization performance despite a comparatively smaller installed base. Premium user demographics contribute to higher spending levels. Developers often prioritize iOS optimization for flagship releases. Strong security standards also enhance consumer confidence.

Subscription services and in-app purchases perform particularly well on this platform. High-performance processors support advanced gaming experiences. Brand loyalty contributes to stable user engagement. These characteristics support attractive revenue generation opportunities.

By Business Model Analysis

In-app Purchase Segment Leads Due to Developer Preference

By business model, the market is separated into in-app purchase, advertising, and paid purchases.

In-App Purchase

The in-app purchase segment holds the largest share of the market. In-app purchases generate a continuous revenue stream through consumables, subscriptions, and non-consumable items. This model is more attractive than one-time paid purchases, making it a preferred monetization strategy for developers and contributing to segment growth.

In-app purchases represent the leading monetization framework across the mobile gaming market. Publishers increasingly rely on recurring transactions rather than one-time purchases. Cosmetic items, premium currencies, and expansion content are major revenue drivers. These mechanisms enhance customer lifetime value.

Behavioral analytics are improving pricing strategies and user targeting. Personalized offers increase conversion rates and retention levels. Live operations support sustained engagement. The segment is expected to retain a dominant position.

Advertising

Advertising-based monetization has become increasingly sophisticated. Rewarded video formats and native advertisements improve user experiences while generating revenue. Casual and hyper-casual titles particularly benefit from this approach. Programmatic technologies are enhancing campaign efficiency.

Brands are recognizing gaming environments as valuable engagement channels. Data analytics support improved audience targeting. Hybrid monetization models are becoming common. These trends continue to influence mobile gaming market trends.

Paid Purchases

Paid purchases remain relevant in selected premium categories. Story-driven experiences and franchise titles often rely on upfront pricing structures. Consumers seeking ad-free experiences continue to support this model. Revenue visibility remains relatively stable.

Although smaller than alternative models, premium purchases retain strategic importance. Publishers use paid releases to strengthen intellectual property value. Cross-platform distribution expands addressable audiences. These factors support continued market participation.

The paid purchase segment is predicted to grow at the fastest CAGR in the coming years. Paid games, often found on platforms such as the Google Play Store, offer a more sophisticated and premium experience, attracting users who are willing to pay for high-quality content. This segment attracts players seeking immersive experiences without the distractions of ads or aggressive monetization strategies, augmenting the segment’s growth.

By End-user Analysis

Male Segment Dominated Due to the Competitive Nature of Male Participants

In terms of end-users, the market is bifurcated into male and female.

Male

The male segment held a dominant share of the market. Video games, including mobile games, meet several psychological needs of the male population, such as achievement, creativity, exploration, and socialization. These needs are often fulfilled through competitive gameplay, creative expression, and social interactions within games, fueling segment growth.

Male players account for a significant portion of spending across competitive and action-oriented genres. Shooter, sports, and role-playing games demonstrate particularly strong engagement among this demographic. Esports ecosystems and multiplayer experiences support long-term retention. Publishers continue to tailor content to these preferences.

Monetization levels remain relatively high within this segment. Community engagement influences purchasing behavior. Social features strengthen loyalty. These dynamics support sustained revenue generation.

Female

The female segment is expected to grow at the fastest rate in the near future. Women are becoming increasingly active in the mobile gaming space, with many playing games more than five times a week. This high level of engagement reflects a shift in the gaming demographic and contributes to the expanding influence of female gamers, driving growth and diversity in the market.

Female participation has expanded significantly across the mobile gaming market. Puzzle, simulation, and casual genres demonstrate strong adoption levels. Improved accessibility and diverse content offerings are broadening audience participation. This shift is reshaping industry priorities.

Developers are increasingly focusing on inclusive game design. Social interaction and personalization features enhance engagement. Advertising monetization performs effectively among casual users. Female gamers are expected to contribute meaningfully to future mobile gaming market growth.

Regional Analysis of the Mobile Gaming Industry

By region, the market is divided into Asia Pacific, North America, Europe, South America, and the Middle East & Africa.

Asia-Pacific Mobile Gaming Market Analysis:

Asia Pacific Mobile Gaming Market Size, 2024 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2024, the Asia Pacific secured a major share of 47.44% of the global mobile gaming market. The region has a vast and young demographic with a high affinity for digital entertainment. This demographic, combined with rapid smartphone adoption, creates a massive potential audience for mobile games.

Besides, mobile devices are increasingly becoming affordable in Asian countries, making mobile gaming accessible to a broader audience within the region. For instance, according to the Observer Research Foundation, published data, in August 2023, India boasts the world's largest youth population, with approximately 808 million people, or 66% of its total population, under the age of 35.

Asia-Pacific accounts for the largest mobile gaming market share globally. Large user populations and improving smartphone affordability support adoption. Expanding digital payment ecosystems enhances monetization efficiency. Competitive gaming and social engagement drive player retention. Investments in network infrastructure and cloud gaming capabilities continue to reinforce long-term growth opportunities.

Japan Mobile Gaming Market:

Japan represents a technologically advanced and highly monetized market. Consumers demonstrate strong loyalty toward established intellectual properties and role-playing games. Premium content and in-app purchases contribute significantly to revenues. Publishers focus on long-term engagement strategies. Continued innovation and high spending levels support the country's strategic importance within the industry.

China Mobile Gaming Market:

China remains one of the world's largest mobile gaming ecosystems. Extensive smartphone penetration and large player communities support strong demand. Domestic publishers maintain significant competitive advantages. Esports activities and live service models continue to expand. Government policies and content regulations influence market dynamics and strategic investment decisions across the sector.

Download Free sample to learn more about this report.

Europe Mobile Gaming Market Analysis:

The growing popularity of esports in Europe contributes to the games market growth. Events such as Games.com Cologne attract large audiences, and the esports fan base is expanding rapidly. Additionally, the adoption of emerging technologies such as AR and VR in mobile games offers immersive experiences, attracting both casual and committed players. For instance, in March 2025, OG Esports announced its expansion into Western Europe with the establishment of a new esports team. This team will participate in tournaments for the popular mobile game Honor of Kings, marking OG Esports' entry into the mobile esports arena.

Europe maintains a strong position within the global mobile gaming market. Diverse player demographics and widespread smartphone usage support stable demand. Subscription services and digital advertising continue to expand. Regulatory frameworks encourage transparency and consumer protection. Publishers are increasingly focusing on localized content and community-driven engagement strategies across major European economies.

Germany Mobile Gaming Market:

Germany represents one of Europe's most important gaming economies. Strong digital infrastructure and high smartphone penetration support user engagement. Consumers demonstrate increasing interest in multiplayer and strategy titles. Subscription-based services are gaining momentum. Investments in cloud technologies and esports ecosystems are expected to support future market growth and strengthen competitive dynamics.

United Kingdom Mobile Gaming Market:

The United Kingdom remains a major contributor to European revenues. High digital adoption and strong consumer spending support market expansion. Publishers emphasize live operations and user retention strategies. Advertising-based monetization models continue to evolve. Growing interest in esports and creator ecosystems is contributing to increased engagement across multiple game categories.

North America Mobile Gaming Market Analysis:

The region is home to prominent game developers such as Electronic Arts, Activision Blizzard, and Zynga, which contribute to its strong gaming ecosystem. The region has a vibrant esports scene, with significant investments in competitive gaming platforms and events, further boosting the market. Major companies in the region have been developing advanced and innovative technologies to launch new products in the market.

North America represents a mature and highly monetized mobile gaming market. Strong smartphone penetration and widespread digital payment adoption support spending growth. Publishers benefit from advanced advertising ecosystems and strong engagement across multiplayer titles. Cloud gaming investments and expanding esports participation continue to strengthen market prospects. Premium content and subscription models are gaining wider acceptance among users.

United States Mobile Gaming Market:

The U.S. is also home to major game developers and publishers, supporting innovation and the creation of high-quality mobile games. Besides, the adoption of cloud gaming services and AR and VR technologies enhances the gaming experience, attracting more users and driving market growth. For instance, in July 2021, Mobile Premier League (MPL), an Indian online gaming platform, launched its app in the U.S. market, making it available for download on both Android and Apple app stores. This marked a significant expansion for MPL, enabling it to capture a share of the large mobile gaming market in the U.S.

The United States remains the largest contributor to regional revenues. High consumer spending and advanced network infrastructure support sustained growth. Major publishers continue to prioritize live service strategies and cross-platform experiences. Influencer ecosystems and esports activities enhance player engagement. Continuous innovation in monetization models supports long-term market expansion and competitive intensity.

South America and the Middle East & Africa Mobile Gaming Market Analysis

The expanding developer ecosystem in cities such as Buenos Aires fosters innovation and the creation of regionally relevant games, attracting both domestic and international investment. Countries such as Brazil and Argentina are investing in digital infrastructure, which supports the growth of the phone-based gaming market by improving connectivity and access to high-quality games.

Furthermore, improvements in internet connectivity, particularly with the rollout of 4G and 5G networks in the Middle East & Africa, are enhancing the smartphone gaming experience by supporting smoother online gameplay. The affordability and availability of smartphones in the Middle East & Africa have also increased significantly, contributing to the region’s growing mobile gaming market share.

The Middle East and Africa are experiencing steady growth in mobile gaming adoption. Expanding smartphone ownership and improving connectivity are supporting market development. Younger demographics and rising digital consumption create favorable conditions. Publishers are increasingly targeting localized content and advertising opportunities to strengthen regional presence and long-term engagement.

Latin America Mobile Gaming Market Analysis

Latin America is emerging as a high-growth region for mobile gaming. Improving internet accessibility and affordable smartphones are increasing user participation. Advertising-based monetization remains highly attractive. Young demographics support long-term demand expansion. Investments in digital payment systems and esports ecosystems are expected to create additional opportunities for publishers.

Competitive Landscape

Key Market Players

Increasing Diversification of Game Genres and Monetization by Key Players to Boost Market Revenue

The mobile gaming market is highly saturated, with several types of games competing for attention. By offering a diverse range of genres, companies can attract different segments of the market, reducing reliance on a single genre and mitigating the risk of market saturation.

Additionally, diversifying genres allows developers to innovate and adapt to changing consumer preferences. As new genres emerge or existing ones evolve, companies that diversify can capitalize on these trends, staying ahead of competitors. Additionally, companies that successfully diversify their monetization strategies can differentiate themselves from competitors, offering more flexible and attractive options to players.

For instance, in May 2024, LinkedIn expanded its platform by introducing gaming to enhance user engagement and foster a more enjoyable experience. The company has launched three puzzle games, Pinpoint, Queens, and Crossclimb, which can be played on mobile phones. These games aim to spark conversations and friendly competition among professionals worldwide.

The mobile gaming industry is characterized by intense competition among established publishers, platform operators, and emerging studios. Leading participants are focusing on portfolio diversification, live service capabilities, and data-driven user acquisition strategies to strengthen competitive positioning. Continuous investment in intellectual property and community engagement remains central to long-term success.

Major global vendors include Tencent Holdings, Activision Blizzard, Electronic Arts, NetEase, Take-Two Interactive, Roblox Corporation, Zynga, Supercell, Playrix, and Garena. These companies maintain extensive portfolios across multiple genres and monetization models. Strong distribution capabilities and large active user bases provide significant competitive advantages. Strategic acquisitions continue to reshape market concentration.

Partnerships with cloud infrastructure providers, telecommunications companies, and digital advertising platforms are becoming increasingly important. Publishers are using artificial intelligence and analytics to improve retention and optimize monetization. Cross-platform experiences and creator ecosystems are expanding user engagement opportunities. These initiatives are strengthening customer lifetime value.

Emerging developers are pursuing differentiated content strategies to compete with larger participants. Indie studios increasingly rely on niche genres and innovative gameplay mechanics. Hybrid monetization models and social interaction features are gaining broader acceptance. User-generated content ecosystems are creating additional opportunities for audience growth.

List of Key Mobile Gaming Top Companies Profiled:

- Electronic Arts (U.S.)

- Nintendo Co., Ltd. (Japan)

- NetEase, Inc. (China)

- Gameloft SE (France)

- Tencent (China)

- Microsoft Corporation (U.S.)

- Niantic, Inc. (U.S.)

- Supercell Oy (Finland)

- Zynga Inc. (U.S.)

- Epic Games (U.S.)

Recent Developments in the Gaming Industry:

- March 2025: Scopely announced the acquisition of Niantic’s games business for approximately USD 3.5 billion. The transaction was undertaken to strengthen Scopely’s position in live-service mobile gaming and expand its portfolio with franchises including Pokémon GO. The acquisition enhanced capabilities in location-based gaming, augmented reality, and player community management.

- March 2025: Ubisoft established a new subsidiary focused on the Assassin’s Creed, Far Cry, and Tom Clancy’s Rainbow Six franchises, supported by a EUR 1.16 billion investment from Tencent. The initiative was designed to accelerate franchise expansion and reinforce long-term live-service strategies. Technologies involved include cloud-connected gaming ecosystems and online multiplayer infrastructure.

- June 2025: Nintendo launched the Nintendo Switch 2, introducing enhanced graphics and improved performance capabilities. The launch was intended to strengthen Nintendo’s gaming ecosystem and support the next generation of digital entertainment experiences. The platform incorporates advanced processing technologies and expanded multiplayer functionality.

- September 2025: Electronic Arts agreed to a USD 55 billion take-private transaction led by Silver Lake, the Public Investment Fund, and Affinity Partners. The deal was aimed at accelerating long-term strategic investments and expanding entertainment capabilities beyond public market constraints. The transaction supports scalable game development and live-operations infrastructure.

- January 2026: Tencent Holdings increased investments in artificial intelligence across its gaming operations to improve player engagement and optimize content delivery. The strategy was intended to strengthen competitive positioning and enhance digital ecosystem capabilities. Technologies involved include artificial intelligence-driven personalization and platform optimization systems

REPORT COVERAGE

The mobile gaming market research report provides a comprehensive analysis, focusing on key elements such as major companies, regional and market segmentation, competitive dynamics, game type, platform, business model, and end-user. Additionally, it offers insights into market dynamics and highlights significant developments within the industry. Beyond these aspects, it also examines various factors that have contributed to market growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 9.74% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Game Type

By Platform

By Business Model

By End-user

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 137.46 billion in 2026 and is anticipated to record a valuation of USD 289.21 billion by 2034.

Fortune Business Insights says that the global market value stood at USD 121 billion in 2025.

The global market will exhibit a CAGR of 9.74% during the forecast period of 2026-2034.

By game type, the shooter segment dominated the market.

Growing smartphone usage and rollout of 5G networks are key factors driving the global market.

Electronic Arts, Nintendo Co., Ltd., NetEase, Inc., Gameloft SE, and Tencent are some of the leading players globally.

Asia Pacific dominated the global market in 2024.

- 2021-2034

- 2025

- 2021-2024

- 210

-

(Offer valid till 30th Jun 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us