Mono Material Packaging Market Size, Share & Industry Analysis, By Material (Plastics, Paper & Paperboard, Metal, Glass, and Others), By Product Type (Bags & Pouches, Bottles & Jars, Trays & Containers, and Others), By End-use Industry (Food & Beverages, Personal Care & Cosmetics, Healthcare, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

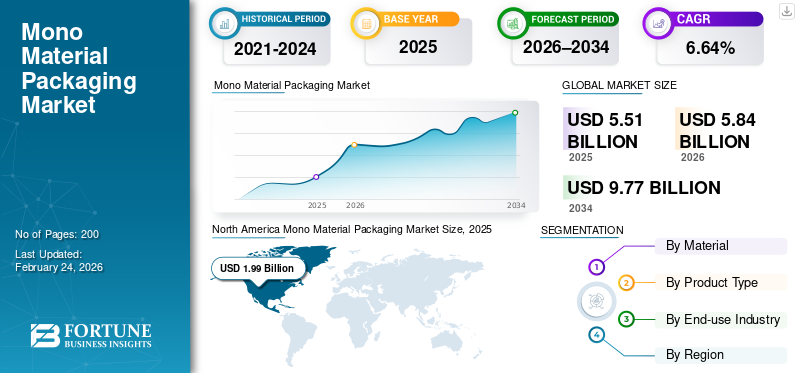

Mono Material Packaging Market Size and Future Outlook

The global mono material packaging market size was valued at USD 5.51 billion in 2025. The market is projected to grow from USD 5.84 billion in 2026 to USD 9.77 billion by 2034, exhibiting a CAGR of 6.64% during the forecast period. North America dominated the mono material packaging market with a market share of 36.12% in 2025.

The global mono-material packaging market comprises packaging solutions crafted from a single material, such as PE, PP, PET, paper, or aluminum, designed to enhance recyclability, streamline waste sorting, and advance circular economy objectives across the food, beverage, pharmaceutical, and consumer goods sectors. The increasing sustainability regulations and brand pledges toward recyclable packaging are propelling the uptake of mono-material solutions, as they reduce material complexity, enhance recycling efficiency, and help companies achieve circular economy and extended producer responsibility goals.

Furthermore, many key industry players, such as Amcor, Mondi, and Sealed Air, operating in the market, are focusing on developing innovative products and conducting R&D, thereby contributing to the market share.

Download Free sample to learn more about this report.

MONO MATERIAL PACKAGING MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 5.51 Billion

- 2026 Market Size: USD 5.84 Billion

- 2034 Forecast Market Size: USD 9.77 Billion

- CAGR: 6.64% from 2026–2034

- North America dominated the mono material packaging market with a 36.12% share in 2025.

- The paper & paperboard segment is projected to grow at a CAGR of 6.82% during the forecast period.

- The bottles & jars segment is expected to expand at a CAGR of 6.55% over the forecast period.

North America

North America reached USD 1.99 billion in 2025, driven by strong sustainability commitments, retailer pressure for recyclable packaging, and investments in recycling infrastructure.

Europe

Europe attained a market value of USD 0.94 billion in 2025 and is projected to grow at a CAGR of 6.28%, driven by stringent environmental regulations and circular economy initiatives.

Asia Pacific

Asia Pacific was valued at USD 1.56 billion in 2025 and remained the second-largest regional market, supported by urbanization, packaged food consumption, and manufacturing expansion.

U.S.

The market was valued at USD 1.61 billion in 2025, supported by corporate sustainability goals, packaging recyclability targets, and state-level recycling regulations.

Japan

The market reached USD 0.26 billion in 2025, benefiting from a strong recycling culture, advanced waste management systems, and growing demand for sustainable packaging solutions.

Read More

MONO MATERIAL PACKAGING MARKET TRENDS

Shift Toward Recyclability-First Packaging Design is a Prominent Trend Observed in the Market

A significant trend influencing the global mono material packaging market is the increasing focus on recyclability-first design across consumer goods and industrial packaging. Brand owners are reengineering flexible and rigid packaging formats to remove multi-layer laminates that pose chemical recycling challenges. Mono-material alternatives made from PE, PP, PET, and paper are progressively supplanting intricate composites while still providing satisfactory barrier properties, sealability, and shelf-life performance. Innovations in material science, including improved coatings and downgauged films, are facilitating this transition without a substantial rise in material consumption. This trend is further supported by retailer sustainability scorecards and consumer demand for packaging that is evidently recyclable and easy to dispose of properly.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Stringent Environmental Regulations and Policy Pressure Are Driving Market Growth

Stringent environmental regulations serve as a key catalyst propelling the expansion of the global mono-material packaging market. Governments in Europe, North America, and certain regions of Asia are implementing Extended Producer Responsibility (EPR) mandates, recycling requirements, and objectives to reduce packaging waste. These regulations impose penalties on non-recyclable, multi-material packaging and promote the adoption of materials that can be efficiently collected, sorted, and recycled.

Mono-material packaging is well-suited to these regulatory requirements, allowing manufacturers and brand owners to maintain compliance while mitigating long-term environmental risks. As regulatory oversight becomes more rigorous, mono-material formats are increasingly regarded as a lower-risk, more sustainable packaging option, gaining traction, and further cushioning the global mono material packaging market growth.

MARKET RESTRAINTS

Performance Limitations Versus Multi-Material Structures Hinders Market Growth

A significant limitation for the global mono material packaging market is the performance disparity compared to traditional multi-material or laminated packaging. Mono-material options often struggle to achieve the oxygen, moisture, light, and aroma barrier characteristics that complex structures provide, especially for sensitive products in the food, pharmaceutical, and chemical sectors. To achieve similar performance levels, it may be necessary to use thicker materials or implement additional processing, which can increase costs and material consumption. These constraints can hinder the adoption of mono material solutions in applications that require extended shelf life or stringent protection standards. Consequently, some end users remain hesitant to completely shift away from established multi-layer packaging systems.

MARKET OPPORTUNITIES

Growing Adoption in Flexible Packaging Applications Offers Potential Growth Opportunities

The growing use of mono-material solutions in flexible packaging offers a considerable opportunity for market expansion. Flexible packaging types, including pouches, sachets, and films, are prevalent across the food, personal care, and household product sectors, making them a primary focus for enhancing recyclability. Mono-material flexible packaging enables brands to achieve lightweighting while meeting recyclability objectives. Advancements in recyclable, high-barrier mono material films and mono-material zipper and closure systems are broadening the scope of applications. As the global collection and recycling infrastructure for flexible plastics continues to improve, mono-material flexible packaging is anticipated to experience accelerated adoption in high-volume consumer product categories.

MARKET CHALLENGES

Recycling Infrastructure and Material Sorting Limitations Pose a Critical Challenge to Market Growth

A significant obstacle confronting the global mono material packaging industry is the inconsistent availability of recycling infrastructure and effective material sorting systems. Although mono-material packaging is inherently more recyclable, its practical recyclability depends on local collection, sorting, and processing capabilities. In numerous emerging markets, insufficient waste management systems hinder the recovery and reuse of mono-material packaging. Even in advanced regions, issues such as contamination, inconsistent labeling, and consumer disposal habits can diminish recycling technology rates. Addressing this challenge requires collaborative efforts among packaging manufacturers, municipalities, recyclers, and brand owners to ensure packaging design aligns with actual recycling capabilities.

Segmentation Analysis

By Material

Versatility, Processability, and Recycling Compatibility Drive the Dominance of Plastics Segment

Based on material, the market is divided into plastics, paper & paperboard, metal, glass, and others.

The plastics segment is expected to account for the largest mono material packaging market share. This growth is driven by its unparalleled versatility, cost-effectiveness, and compatibility with current packaging and recycling systems. These materials facilitate high-speed processing, downgauging, and advanced barrier improvements without sacrificing recyclability. Furthermore, mono material plastics are well-suited to monomaterial design specifications, enabling easier waste sorting and higher recycling rates than multi-material structures. Their extensive availability and well-established supply chains further solidify their dominance in several applications.

The paper & paperboard segment is expected to grow at a CAGR of 6.82% over the forecast period.

By Product Type

Lightweighting, Design Flexibility, and Sustainability Goals Drive the Dominance of Bags & Pouches Segment

Based on product type, the market is segmented into bags & pouches, bottles & jars, trays & containers, and others.

In 2025, the bags & pouches segment dominated the global market. This growth is driven by their lightweight characteristics, design versatility, and strong alignment with sustainability goals. Compared with rigid formats, they use considerably less material, reducing overall packaging weight, transportation costs, and carbon emissions. Their versatility across various applications, including food, personal care, household items, and pet food, further encourages widespread use. Moreover, high consumer acceptance, convenient features such as resealability, and their suitability for high-volume packaging make bags & pouches the preferred choice.

The bottles & jars segment is projected to grow at a CAGR of 6.55% over the forecast period.

By End-use Industry

To know how our report can help streamline your business, Speak to Analyst

High Consumption Volumes, Shelf-Life Needs, and Sustainability Pressure Drive Food & Beverages Dominance

Based on the end-use Industry, the market is segmented into food & beverages, personal care & cosmetics, healthcare, and others.

The food & beverages segment is expected to hold a dominant market share over the forecast period. The growth of this segment is driven by substantial packaging consumption and rising sustainability demands. F&B items require safe, hygienic, and protective packaging for storage, transport, and extended shelf life, making packaging a vital element in terms of cost and performance. Moreover, global food brands are under significant regulatory scrutiny and face consumer pressure for recyclable packaging, hastening the transition away from complex multi-layer structures. The swift expansion of packaged foods, beverages, and convenience items further solidifies the segment's leading position.

The personal care & cosmetics segment is projected to grow at a CAGR of 6.55% over the forecast period.

Mono Material Packaging Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Mono Material Packaging Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valued at USD 1.88 billion, and maintained its leading position in 2025, with a value of USD 1.99 billion. The growth observed in North America is driven by robust sustainability commitments from brands and by retailers' pressure to implement recyclable packaging formats. Companies in the food, beverage, and personal care packaging sectors are reengineering their packages to fulfill recyclability objectives, while investments in plastic recycling infrastructure and innovations in mono-material flexible packaging facilitate wider market acceptance.

U.S. Mono Material Packaging Market

Based on North America’s substantial contribution and the U.S. dominance within the region, the U.S. market was valued at USD 1.61 billion in 2025, accounting for roughly 29.29% of global sales. The U.S. market is influenced by commitments to corporate sustainability and by state-level regulations on packaging and recycling.

Prominent food and beverage companies are allocating resources toward mono-material flexible packaging to achieve recyclability goals, bolstered by technological advancements and increased funding in advanced recycling and material recovery facilities.

Europe

Europe is projected to grow at 6.28% over the coming years, the third-highest among regions, and reached a valuation of USD 0.94 billion by 2025. The mono material packaging market in Europe is primarily influenced by strict environmental regulations and policies that promote a circular economy. Directives on packaging waste from the EU, along with extended producer responsibility initiatives and recyclability objectives, are compelling manufacturers to transition from multi-material laminates to mono-material structures compatible with established collection and recycling systems.

U.K Mono Material Packaging Market

The U.K. market in 2025 was estimated at USD 0.15 billion, representing approximately 2.67% of global revenues.

Germany Mono Material Packaging Market

Germany’s market reached approximately USD 0.22 billion in 2025, equivalent to around 3.96% of global sales.

Asia Pacific

Asia Pacific was estimated at USD 1.56 billion in 2025 and secured the position of the second-largest region in the market. In the region, the Indian and Chinese markets reached the valuations of USD 0.38 billion and USD 0.49 billion, respectively, in 2025. In the Asia Pacific region, rapid urbanization, increased consumption of packaged foods, and the expansion of manufacturing facilities are driving demand for mono material packaging. Although sustainability regulations differ from one market to another. Multinational companies are working to standardize recyclable packaging across regions. Key factors contributing to growth in the region include cost efficiency, lightweight flexible packaging, and a growing awareness of environmental issues.

Japan Mono Material Packaging Market

The Japanese market in 2025 was valued at USD 0.26 billion, accounting for roughly 4.77% of global revenues. A robust recycling culture and a focus on efficient packaging design propel Japan's mono material packaging sector. Manufacturers prioritize material minimization, precise engineering, and compatibility with advanced waste-sorting systems. The adoption of mono-material packaging is further accelerated by brand reputation, regulatory compliance, and consumer demand for environmentally sustainable packaging.

China Mono Material Packaging Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues estimated at around USD 0.49 billion, representing roughly 8.83% of global sales.

India Mono Material Packaging Market

The Indian market in 2025 was valued at USD 0.38 billion, accounting for roughly 6.82% of global markets.

Latin America and the Middle East & Africa

The Latin America and the Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market reached a valuation of USD 0.61 billion in 2025. The progressive development of regulations and the growing adoption of eco-friendly packaging by multinational consumer goods firms drive the market in Latin America. Lightweight mono-material packaging helps lower logistics costs in extensive distribution networks, while new recycling initiatives and brand commitments foster consistent, albeit uneven, regional adoption.

In the Middle East & Africa, South Africa reached a valuation of USD 0.16 billion in 2025. In the Middle East and Africa, demand is driven by food security concerns, rising packaged food consumption, and the expansion of retail infrastructure. The adoption of sustainability practices is progressing more slowly. Yet it is on the rise, supported by government initiatives to reduce waste and by private-sector programs.

Saudi Arabia Mono Material Packaging Market

The Saudi Arabian market was valued at USD 0.11 billion by 2025, accounting for roughly 1.98% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Expanding Product Launch and Acquisitions by Key Players to Propel Market Progress

The global market has a semi-consolidated structure, with prominent players including Amcor, Mondi, and Sealed Air. The significant market shares of these packaging companies are due to numerous strategic initiatives, including collaborations among operating entities to advance research.

- For instance, in June 2025, Amcor unveiled its custom three-compartment tray designed for French manufacturer Cofigeo’s selection of single-serve ready meals. This tray is reported to adhere to Design for Recycling standards. It features a lightweight mono-material Polypropylene (PP) construction, suitable for collection and reprocessing within France’s recycling system.

Other notable players in the global market include Sonoco Products Company, Graphic Packaging International, and Constantia Flexibles. These companies are expected to prioritize new product launches, strategic partnerships, and collaborations to increase their global market shares during the forecast period.

LIST OF KEY MONO MATERIAL PACKAGING COMPANIES PROFILED

- Amcor (Switzerland)

- Mondi (U.K.)

- Sealed Air (U.S.)

- Sonoco Products Company (U.S.)

- Graphic Packaging International (U.S.)

- Constantia Flexibles (Austria)

- ProAmpac (U.S.)

- Smurfit Kappa (Ireland)

- Toppan Inc. (Japan)

- Polysack Flexible Packaging Ltd. (Israel)

- Dai Nippon Printing Co. (Japan)

- APC Packaging (U.S.)

- Huhtamaki (Finland)

- Profol GmbH (Germany)

- HCP Packaging (China)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Sealed Air launched Cryovac VPP MonoPro, a novel vertical form-fill-seal packaging solution tailored for pumpable and liquid food items. This advancement focuses on products such as soups, sauces, purees, proteins, and syrups, facilitating a transition from traditional multi-layer films to a single-material design. The film features a minimal amount of polyamide, available at 0% or 10% content, and is offered in both transparent and colored versions.

- October 2025: Amcor declared that the straightforward, clean, and sanitary refill procedure for its Exclusive stick has rendered it the perfect selection for the French natural hair specialist Cut by Fred’s Detox Stick Shampoo. This mono-material design ensures that the packages can be recycled, provided suitable collection and recycling facilities are available, once they reach the end of their lifecycle.

- May 2025: Constantia Flexibles, a prominent figure in the flexible packaging industry, effectively introduced EcoVerHighPlus, a groundbreaking mono PP laminate that is currently revolutionizing coffee packaging. This soft bag packaging, developed in close collaboration with Delica AG, which is part of the Migros Industrie AG group, a renowned Swiss manufacturer of high-quality chocolate, snacks, cooking products, and coffee, merges enhanced sustainability with superior performance.

- April 2025: Amcor introduced monomaterial pouches in Europe for bulk foodservice. The company states that this packaging reduces carbon emissions by up to 79% and uses 84% less water. These statistics are derived from an evaluation certified by the Carbon Trust. The pouches are engineered to enhance efficiency in storage and transportation, occupying less space than metal cans before being filled.

- July 2024: Mondi introduced the newest member of its well-regarded collection of sustainable pre-made plastic bags - FlexiBag Reinforced: a series of innovative packaging solutions based on mono-PE that are recyclable and possess enhanced mechanical properties. By supporting a circular economy, the FlexiBag Reinforced range is recyclable in areas where collection facilities and recycling systems for PE films are available.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.64% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Material, Product Type, End-use Industry, and Region |

| By Material |

|

| By Product Type |

|

| By End-use Industry |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 5.51 billion in 2025 and is projected to reach USD 9.77 billion by 2034.

In 2025, North Americas market value stood at USD 1.99 billion in the mono material packaging industry.

The market is expected to grow at a CAGR of 6.64% over the forecast period of 2026-2034.

By material, the plastic segment is expected to lead the market.

Stringent environmental regulations and policy pressure are the key factors driving the market.

Amcor, Mondi, and Sealed Air are the major players in the global market.

North America dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us