Nanophotonics Market Size, Share & Industry Analysis, By Product Type (LEDs, OLEDs, Near Field Optics (NFO), Photovoltaic Cells, Optical Amplifiers, Optical Switches, and Others (Holographic Data Storage Systems, etc.)), By Material (Plasmonics, Photonic Crystals, Nanotubes, Nanoribbons, Quantum Dots, and Others (Graphene, etc.)), By Application (Telecommunication, Consumer Electronics, Energy & Power, Healthcare, Aerospace & Defense, Lighting & Digital Signage, and Others (Security, etc.)), and Regional Forecast, 2026-2034

NANOPHOTONICS MARKET SIZE AND FUTURE OUTLOOK

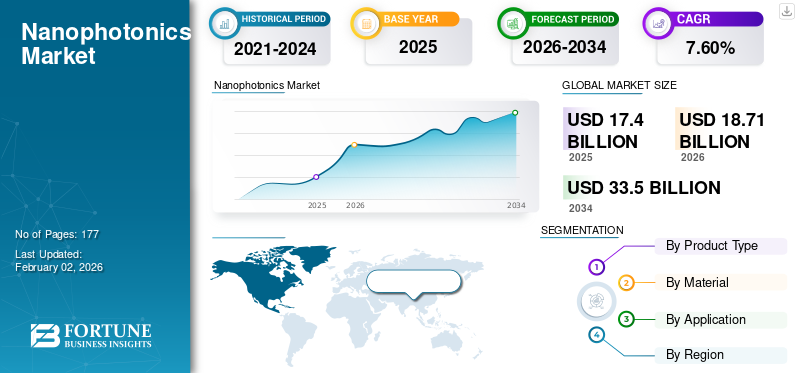

The global nanophotonics market size was valued at USD 17.40 billion in 2025 and is projected to grow from USD 18.71 billion in 2026 to USD 33.50 billion by 2034, exhibiting a CAGR of 7.60% during the forecast period. Asia Pacific dominated the nanophotonics market with a market share of 39.70% in 2025.

Emerging as a new and rapidly developing field, nanophotonics is a combination of nanotechnology and photonics enable to control the light on the Nanometer scale, making it critically important for a multitude of applications, including solar energy, medical imaging, displays, optical communication, and high-performance computing.

The market driving factors include the demand for faster Internet access, growing adoption of energy-efficient LED and OLED technologies for energy efficiency, advances in solar energy collection, and the increasing use of nanophotonic resources in quantum calculation and biosensor applications.

A few prominent players operating in the market are Cree, Inc., Samsung Electronics Co., Ltd., OSRAM Opto Semiconductors GmbH, Lumentum Holdings, Inc., Intel Corporation, and others.

Download Free sample to learn more about this report.

NANOPHOTONICS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 17.40 billion

- 2026 Market Size: USD 18.71 billion

- 2034 Forecast Market Size: USD 33.50 billion

- CAGR: 7.60% from 2026–2034

- Asia Pacific dominated the nanophotonics market with a 39.70% share in 2025.

- The photovoltaic cells segment is projected to account for 27.53% of the global market in 2026.

- The consumer electronics segment is expected to hold 28.90% of the global market share in 2026.

Asia Pacific

Asia Pacific generated USD 6.91 billion in revenue in 2025 and is projected to reach USD 7.48 billion in 2026.

North America

North America reached USD 5.15 billion in 2025 and is expected to grow to USD 5.55 billion in 2026.

Europe

Europe accounted for USD 3.72 billion in 2025 and is projected to reach USD 3.97 billion in 2026.

U.S.

The market is projected to reach USD 3.27 billion by 2026.

Japan

The market is expected to reach USD 1.80 billion by 2026.

Read More

MARKET DYNAMICS

Market Drivers

Rapid Growth of Data and AI is Boosting the Need for High-Speed, Energy-Efficient Connections which is Driving the Market Development

The rapid growth of data and AI is boosting the need for high-speed, energy-efficient connections, which is driving the global nanophotonics market growth. Driven by the exponential growth of data and the emergence of artificial intelligence (AI), the Nanophotonics industry is experiencing growth. Speed, power usage, and heat generation are physical limits for traditional electronic components, which transmit data utilizing electrical signals. Nanophotonics presents a disruptive approach whereby light (photons) rather than electrons is used to convey and analyze data, therefore ushering in a new age of fast, energy-efficient data transmission.

One of the main bottlenecks and a significant energy consumer is the interconnects. By offering ultra-fast, low-latency, and very energy-efficient optical interconnections, nanophotonics solves this problem. NVIDIA, which revealed at its GTC conference in March 2025 that it is directly connecting silicon photonics with its fresh wave of Spectrum and Quantum switch integrated circuits. Compared to conventional pluggable optical transceivers, the company's co-packaged silicon photonics (CPO) switch systems offer up to 3.5 times less power consumption and faster latency.

Market Restraints

Difficulties in Producing Nanophotonic Devices at Large Scale and Low Cost Hampers the Market Growth

The difficulties in producing nanophotonic devices at large scale and low cost act as significant restriction factors for the nanophotonics market. Although it has enormous potential, the nanophotonic market is severely restricted due to the high complexity and high manufacturing cost of nanophotonic devices at scale. Although technology offers innovative discoveries, the transition from a laboratory model to an element produced in mass, economically feasible, presents a significant obstacle. This restriction stems from the fact that nanofabrication is a very complicated process that demands many resources. Manufacturing requires highly trained personnel, expensive cleanroom facilities, electro-beam lithography and atomic layer deposition technologies.

Market Opportunities

Strong Growth Potential in AI Datacenters, Edge Computing, and Renewable Energy Applications Offers Lucrative Growth Opportunities

Driven by the constraints of conventional electronics, especially in areas needing high speed, energy efficiency, and small size, the industry has great possibilities. Exponential data growth, technological advancements, and the development of artificial intelligence are fueling a pressing need for a new generation of hardware that can manage tremendous data flows with minimal power consumption.

This opportunity is now turning into real progress. Big corporations in the AI data center sector are using nanophotonics to get around interconnect bottlenecks. Leading in AI hardware, NVIDIA, for instance, announced in March 2025 its straight silicon photonics integration with its next-generation switches.

Compared to conventional optical interconnects, the company's co-packaged optics (CPO) switch systems guarantee up to 3.5 times reduced power usage and latency. Likewise, in the sectors of data centers and edge computing, the emphasis on energy efficiency is spurring invention. Using a phase-change material and a graphene heater, a team at the University of Washington created a new, energy-efficient optical switch in May 2025.

NANOPHOTONICS MARKET TRENDS

Increasing Use of Silicon Photonics to Create Smaller and Faster Optical Systems Has Emerged as a Prominent Market Trend

A key trend in the market is a greater approach to silicon photonics to develop smaller and faster optical systems. The approach to silicon photonics represents a critical trend in the nanophotonic materials that will help enable the development of smaller, faster, and more integrated optical systems. The use of Silicon to create photonic components offers a scalable and profitable solution for integrating electrical and optical capabilities into a single chip. The manufacturing methods of metal-oxide semiconductors (CMOS) offer general capacities related to extension manufacturing options.

Support for this trend continues stronger than ever among industry leaders and academic institutions. At the end of September 2025, a European consortium launched the STARLight project to develop a high-volume 300mm Silicon Photonics production line. Including large corporations such as STMicroelectronics, this initiative expects to establish Europe as a leader in SiPho technology for artificial intelligence groups and data centers.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Product Type

LEDs Segment Dominated Due to Widespread Use in Consumer Electronics and Lighting

Based on the product type, the market is segmented into LEDs, OLEDs, Near Field Optics (NFO), photovoltaic cells, optical amplifiers, optical switches, and others (Holographic Data Storage Systems, etc.).

In 2024, the LEDs segment held the largest share of the nanophotonics market share, with a revenue of USD 4.50 billion. This can be explained as nanophotonics are increasingly utilized in high-brightness LEDs for electronic display panels, smart lighting, and automotive use, along with demand for higher brightness, energy efficiency, and miniaturization.

The photovoltaic cells product type segment is projected to dominate the nanophotonics market, accounting for 27.53% of the global market share in 2026. This swift growth is driven by the global trend of renewable energy andincreased research activity aimed at harnessing nanophotonic structures to enhance light absorption and solar cell efficiency, thereby creating growth avenue for higher energy output at a reduced cost per watt.

By Material

Plasmonics Segment Dominated Due to its Unique Properties for High-Speed and Sensing Applications

The market is divided into plasmonics, photonic crystals, nanotubes, nanoribbons, quantum dots, others (Graphene, etc.).

The plasmonics material segment is expected to lead the market, contributing 38.63% globally in 2026. This is attributed to the special capability of plasmonics in manipulating light at the nanoscale level, which enables high-speed optical interconnects, ultra-sensitive biosensors, and creation of intricate light-cutting systems.

By Application

Consumer Electronics Holds the Largest Market Share Due to Its Wide-Scale Adoption

Based on application, the market is segmented into telecommunication, consumer electronics, energy & power, healthcare, aerospace & defense, lighting & digital signage, and others (security, etc.).

The consumer electronics application segment will remain the largest end-use category, and is projected to reach for 28.90% of the global market share in 2026. Its supremacy is credited due to the wide adoption of nanophotonics in smartphones, tablets, and TV displays, where nanophotonics are utilized for bright images with richer colors and also to save power.

The healthcare segment is expected to grow with the highest CAGR of 10.26%. This growth is made possible by the use of cutting-edge medical imaging and hypersensitive biosensors to detect early disease, as well as the development of nanophotonic strategies within drug delivery targeting systems.

To know how our report can help streamline your business, Speak to Analyst

NANOPHOTONICS MARKET REGIONAL OUTLOOK

Geographically the market is segmented into North America, Europe, Asia Pacific, South America and Middle East & Africa.

North America

North America is a key player in nanophotonics, with a strong R&D culture and the presence of well-established tech companies. The North America market accounted for USD 5.15 billion in 2025, representing 29.60% of the global industry, and is expected to reach USD 5.55 billion in 2026. This development is largely due to massive investments in building high-performance computing through AI data centers and new technologies for defense. In the U.S., this progress is largely driven by the presence of existing infrastructure, substantial government venture capital funding, and the highest levels of academic/private research in silicon photonics and quantum computing. The U.S. market is projected to reach USD 3.27 billion by 2026.

Europe

Europe recorded a market size of USD 3.72 billion in 2025, capturing 21.40% of the global market share, and is projected to reach USD 3.97 billion in 2026. This is largely due to an emphasis on sustainability and a strong financial supply for R&D, funded through government programs like Horizon Europe. The UK market is pro jected to reachUSD 0.96 billion by 2026 and the Germany market is projected to reach USD 0.83 billion by 2026. Supporting this information is the strength of the automotive industry in Europe, which is working on advanced LiDAR systems utilizing nanophotonics, as well as the telecom industry.

Asia Pacific

In 2025, Asia Pacific represented USD 6.91 billion, accounting for 39.70% of the worldwide market, and is projected to grow to USD 7.48 billion in 2026. The growth in this market is attributed to the rapid industrial development taking place here, huge electronics manufacturing, and the vigorous government support for technology development. The Japan market is projected to reach USD 1.80 billion by 2026, the China market is estimated to reach USD 2.12 billion by 2026, and the India market is projected to reach USD 1.43 billion by 2026.

Asia Pacific Nanophotonics Market Size, 2025

To get more information on the regional analysis of this market, Download Free sample

Another driver of the Asia Pacific market is the presence of major industrial developments underway, which are bolstering the region's leadership. By 2025, a fair number of initiatives and investments will support the regional market growth. An example includes China, where its government has invested billions into moving more domestic industry into semiconductor manufacturing, coupled with a focus on nanophotonics in data centers and AI accelerators for next-generation equipment.

South America and Middle East & Africa

The markets of South America and those of the Middle East & Africa are expected to grow slowly on account of rapid urbanization, infrastructure expansion, and economic diversification. Middle East & Africa contributed 5.90% to the global market in 2025, with a valuation of USD 1.02 billion, and is projected to reach USD 1.08 billion in 2026. Within the Middle East & Africa, the GCC countries are expected to witness revenue capture worth USD 0.34 billion in 2025, with investments flowing in from smart city projects and high-tech industries.

Latin America

The Latin America market was valued at USD 0.6 billion in 2025, capturing 3.50% of global revenue, and is estimated to reach USD 0.63 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Growing Focus of Key Players on Innovation and New Launches Leads to their Dominating Market Positions

The global nanophotonics market is highly fragmented, with several major players in the market are actively competing across different regions. Leading companies include Cree, Inc., Samsung Electronics Co., Ltd., OSRAM Opto Semiconductors GmbH, Lumentum Holdings, Inc., Intel Corporation, Lumileds Holding B.V., Nichia Corporation, and Sharp Corporation. These companies focus on a range of strategic initiatives, including product innovation, mergers and acquisitions, advancements in nanophotonic technologies, and investments in research and development to strengthen their market position and remain competitive in the evolving global landscape.

LIST OF KEY NANOPHOTONICS COMPANIES PROFILED:

- Cree, Inc. (U.S.)

- Samsung Electronics Co., Ltd. (South Korea)

- OSRAM Opto Semiconductors GmbH (Germany)

- Lumentum Holdings, Inc. (U.S.)

- Intel Corporation (U.S.)

- Lumileds Holding B.V. (U.S.)

- Nichia Corporation (Japan)

- Sharp Corporation (Japan)

- Novaled GmbH (Germany)

- Nanosys, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- September 2025 - Researchers at the University of St Andrews revealed a new optolectronic device that combines OLEDs with holographic metasurfaces to produce an innovative pixel.

- September 2025 - IBM Research has advanced the development of microwave photonic systems in a single chip that can be configured for various signal processing applications. This programmable solution is for use in wireless communications and microwave detection, and is part of the "Exploratory Photonics" project.

- September 2025 - A new consortium has been launched, led by a European initiative, to develop a high-volume manufacturing line for 300 mm silicon photonics. The project, which has major companies such as STMicroelectronics among its partners, is considered a strategic move to put Europe at the forefront of SiPho technology for data centres and AI groups.

- September 2025- The scientists of a leading university in the United States achieved an important advancement in the manipulation of light waves in two-dimensional materials, which allows light to be compressed in volumes hundreds of times smaller than its wavelength.

- July 2025- Nanophotonic computing startup, Arago, recently announced $26MM raised in a seed round. The company will use the funding to accelerate its R&D and scale its team, developing an all-photonic AI-supercomputing network. The significant initial round shows both strong confidence from investors in nanophotonics as a key compositional technology for AI moving forward.

REPORT COVERAGE

The global report provides a detailed analysis of the market and focuses on key aspects such as prominent companies, deployment modes, types, and end users of the product. Besides this, it offers insights into the nanophotonics market trends and highlights key industry developments and market share analysis for key companies. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE |

DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Growth Rate | CAGR of 7.60% from 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, Material, Application, and Region |

| By Product Type |

|

| By Material |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size is projected to grow from USD 18.71 billion in 2026 to USD 33.50 billion by 2034, exhibiting a CAGR of 7.60% during the forecast period.

The market is expected to exhibit steady growth at a CAGR of 7.60% during the forecast period.

Rapid Growth of Data and AI is Boosting the Need for High-Speed, Energy-Efficient Connections drives the market growth.

Cree, Inc., Samsung Electronics Co., Ltd., OSRAM Opto Semiconductors GmbH, Lumentum Holdings, Inc., Intel Corporation, Lumileds Holding B.V., Nichia Corporation, and Sharp Corporation are some of the top players in the market.

The Asia Pacific region held the largest market share.

Asia Pacific was valued at USD 6.91 billion in 2025.

- 2021-2034

- 2025

- 2021-2024

- 177

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us