Silicon Photonics Market Size, Share & Industry Analysis, By Component (Photodetectors, Optical Waveguides, Wavelength-Division Multiplexing (WDM) Filters, Laser, and Optical Modulators), By Product (Transceivers, Active Optical Cables, Optical Multiplexers, Optical Attenuators, and Others), By Application (Data Center and High Performance Computing, Consumer Electronics, Healthcare & Life Sciences, Aerospace, Defense and Security, Automotive, and Others), and Regional Forecast, 2026–2034

Silicon Photonics Market Size

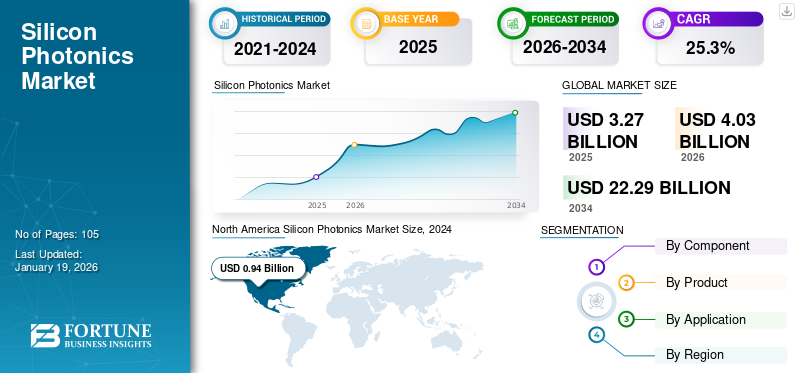

The global silicon photonics market size was valued at USD 3.27 billion in 2025. The market is projected to grow from USD 4.03 billion in 2026 to USD 22.29 billion by 2034, exhibiting a CAGR of 23.83% during the forecast period. North America dominated the global silicon photonics market with a market share of 34.56% in 2025.

The market encompasses silicon-based photonic components, integrated photonic devices, and system-level products utilized across various applications, including data communication, computing, defense, medical and life sciences, automotive, and industrial sectors. The market also includes development, manufacturing, and commercialization of photonic components and integration of systems into silicon substrates, enabling the transmission, modulation, detection, and processing of optical communication using semiconductor fabrication techniques.

The technology leverages CMOS-compatible manufacturing processes to integrate optical and electronic functions on a single chip, offering advantages such as high bandwidth, reduced power consumption, compact form factors, and scalability. These solutions are increasingly adopted to address data transmission limitations in traditional electronic interconnects.

The scope of this market focuses exclusively on silicon photonics technology, including silicon-on-insulator (SOI) platforms and related integration approaches. It excludes purely discrete optical components and non-silicon-based photonic technologies unless they are directly integrated within silicon photonic systems.

The market is driven by the increasing demand for high speed broadband, growing adoption of co-packaged optics and next-generation transceivers, and rising need for scalable bandwidth to support cloud computing and 5G infrastructure. Intel Corporation, Cisco Systems (Acacia), GlobalFoundries Inc., Marvell Technology, Coherent Corp., IBM Corporation, and Jabil Inc. are among the top companies operating in the market.

Download Free sample to learn more about this report.

SILICON PHOTONICS MARKET TRENDS

Integration of Silicon Photonics in Automotive LiDAR Systems for Fully Autonomous Vehicles

Silicon photonics is emerging as a critical enabler for next-generation automotive LiDAR systems, offering compact, high-resolution, and energy efficient sensing solutions that are essential for autonomous vehicles and Advanced Driver-Assistance Systems (ADAS).

By leveraging CMOS-compatible fabrication, it enables the development of miniaturized, cost-effective LiDAR modules with improved reliability and robustness under automotive operating conditions. For instance,

- In March 2024, Stellantis Ventures invested in SteerLight, a startup developing compact, cost-effective LiDAR systems using silicon photonics for advanced driver assistance systems (ADAS). The on-chip Frequency Modulated Continuous Wave (FMCW) LiDAR provides high-resolution 3D sensing, accurate depth and velocity data, eliminates moving parts, and offers lower production costs.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Computational Demands from AI and ML to Fuel Market Growth

The rapid acceleration of Artificial Intelligence (AI), Machine Learning (ML), and High-Performance Computing (HPC) has emerged as a fundamental driver for the market. Modern AI models, particularly large-scale deep learning architectures, require the movement of massive volumes of data between processors, memory, and storage across distributed computing environments. As model sizes and dataset complexity increases, traditional electrical interconnects are reaching practical limits in terms of bandwidth density, latency, and power consumption, creating a structural bottleneck in compute scaling.

The technology directly addresses these limitations by enabling high-bandwidth, low-latency optical interconnects that significantly reduce energy consumption per transmitted bit. For instance,

- In December 2025, NTT partnered with Toshiba and Broadcom, advancing silicon photonics to address power and bandwidth challenges in data centers and telecommunications. Their photonic-electronic convergence (PEC) devices integrate optical and electronic components on a single chip, enabling board-to-board optical interconnects with a capacity of 51.2 terabits per second (Tb/s) while drastically reducing power consumption and latency.

MARKET RESTRAINTS

High Costs and Capital Requirements to Hinder the Market Growth

One of the most significant restraints on the growth of the market is the high cost associated with both production and market entry. Manufacturing silicon photonics devices requires specialized fabrication facilities, precision equipment, and advanced materials, all of which demand substantial capital investment.

Unlike traditional semiconductor devices, these components often involve the complex integration of optical and electronic circuits, hybrid material systems, and precise alignment techniques, further increasing production costs. These elevated expenses make the technology relatively expensive compared to conventional optical and electronic interconnect solutions, hindering the silicon photonics market growth.

MARKET OPPORTUNITIES

Telecommunications & 5G/6G Networks to Create Growth Prospects for the Market

The global rollout of 5G and the early development of 6G networks are driving unprecedented demand for high-speed, energy-efficient optical interconnects. Silicon photonics presents a significant market opportunity, as it can deliver high-bandwidth, low-latency optical links while leveraging CMOS-compatible manufacturing to reduce costs and scale production. For instance,

- In June 2025, Vodafone partnered with the University of Málaga to develop silicon photonic chips that use light for precise signal steering in 5G-advanced and future 6G networks. The technology, known as optical beamforming, aims to enhance data rates, minimize interference, and reduce latency.

This opens avenues for companies to develop telecom-specific optical transceivers, switches, and co-packaged optics designed for next-generation network infrastructure.

Strategic partnerships with carriers and network equipment OEMs offer a fast-track adoption, while solutions that meet telecom performance standards will position businesses to capture a share of the multi-billion-dollar optical components market, driven by 5G/6G expansion.

SEGMENTATION ANALYSIS

By Component

Optical Waveguides Dominate Owing to Their Essential Role In Silicon Photonics PICs

Based on the component, the market is divided into photodetectors, optical waveguides, Wavelength-Division Multiplexing (WDM) filters, lasers, and optical modulators.

Optical waveguides hold the largest share and are expected to grow at the highest CAGR because they are the fundamental light-routing backbone of silicon photonics PICs and are increasingly adopted as hyperscalers and telecom players scale high-density optical interconnect architectures.with a share of 30.16% in 2026

WDM filters hold the second-largest share because they are essential for enabling multi-wavelength transmission over a single fiber, making them critical components in high-capacity datacom and telecom optical networks.

To know how our report can help streamline your business, Speak to Analyst

By Product

High Data Center Interconnect Usage Is Boosting the Leadership of Active Optical Cables

Based on product, the market is segmented into transceivers, active optical cables, optical multiplexers, optical attenuators, and others.

Active optical cables hold the largest share because they provide a cost-effective, plug-and-play solution for short-reach high-speed connectivity in data centers, supporting the growing deployment of AI and high-bandwidth interconnects.with a share of 30.96% in 2026

Optical multiplexers are expected to grow at the highest CAGR due to the accelerating demand for higher fiber utilization and bandwidth scaling, which is driving the rapid adoption of multiplexing solutions in next-generation networks and data center interconnects.

By Application

Defense and Security Takes the Leading Position Due to Mission-Critical Photonics Adoption

Based on application, the market is segmented into data centers and high-performance computing, consumer electronics, healthcare & life sciences, aerospace, defense and security, automotive, and others.

Defense and security holds the highest share as the technology enables high-performance, compact, and resilient optical systems used in mission-critical applications such as secure communications, sensing, and surveillance.with a share of 25.26% in 2026

Data centers and high-performance computing are expected to record the highest CAGR, driven by AI-driven workloads that are fueling exponential demand for high-speed optical interconnects. It also offers superior bandwidth density and energy efficiency compared to electrical links.

SILICON PHOTONICS MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Silicon Photonics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America contributed approximately USD 1.13 billion to the global market in 2025, accounting for 34.56% share, and is expected to reach USD 1.39 billion in 2026. The region has the strongest concentration of hyperscale data centers, leading developers, and early adoption of high-speed optical interconnects across AI and cloud infrastructure.

U.S Silicon Photonics Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market has been analytically approximated to be around USD 0.83 billion in 2026, accounting for roughly 20.5% of global sales.

Asia Pacific

The Asia Pacific region captured 21.31% of the global market in 2025, generating USD 0.7 billion in revenue, and is projected to reach USD 0.87 billion in 2026. In the region, India and China both were estimated to reach USD 0.15 billion and USD 0.20 billion, respectively, in 2025. The rapid expansion of data center capacity, the acceleration of 5G and fiber network rollouts, and increased investments in semiconductor and photonics manufacturing are driving faster adoption.

Japan Silicon Photonics Market

The Japan market in 2026 is estimated to be around USD 0.19 billion, accounting for approximately 4.9% of global revenues.

China Silicon Photonics Market

China’s market is projected to be one of the largest markets globally, with revenues estimated to be approximately USD 0.25 billion in 2026, accounting for roughly 6.0% of global sales.

India Silicon Photonics Market

The India market in 2026 is estimated to be around USD 0.19 billion, accounting for approximately 4.6% of global revenues.

Europe

In 2025, the Europe market stood at USD 0.87 billion, representing 26.60% of global demand, and is projected to grow to USD 1.06 billion in 2026, driven by steady demand from telecom modernization, strong R&D ecosystem, and growing deployment of photonics-enabled networking solutions across the industrial and defense sectors.

U.K Silicon Photonics Market

The U.K. market in 2026 was estimated to be around USD 0.24 billion, representing approximately 5.8% of global revenues.

Germany Silicon Photonics Market

Germany's market size has been projected to reach approximately USD 0.19 billion by 2026, equivalent to around 4.6% of the global market.

South America and the Middle East & Africa

In 2025, Middle East & Africa generated USD 0.41 billion, contributing 12.50% to global market revenue, and is projected to grow to USD 0.51 billion in 2026. The South America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The South America market is set to reach a valuation of USD 0.16 billion in 2025. The Middle East & Africa is set to reach the value of USD 0.41 billion in 2025. Adoption in both regions is progressing gradually, supported by incremental data center and telecom upgrades, while investment intensity and the depth of the local photonics ecosystem remain comparatively moderate.

GCC Silicon Photonics Market

The GCC market has been projected to reach approximately USD 0.16 million by 2025, accounting for roughly 4.9% of global market revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Launch New Solutions to Strengthen Their Market Positioning

Players in the silicon photonics industry are launching new solutions to enhance their market positioning by leveraging technological advancements, such as machine learning, and addressing diverse consumer needs, thereby staying ahead of competitors. They prioritize product portfolio enhancement and strategic collaborations, as well as acquisitions and partnerships to strengthen their offerings. Such strategic launches enable the technology companies to maintain and expand their market share in a rapidly evolving landscape.

LIST OF KEY SILICON PHOTONICS COMPANIES PROFILED

- Intel Corporation (U.S.)

- Cisco Systems, Inc. (U.S.)

- GlobalFoundries Inc. (U.S.)

- Lumentum Operations LLC (U.S.)

- Marvell Technology, Inc. (U.S.)

- Coherent Corp. (U.S.)

- Broadcom, Inc. (U.S.)

- Synopsys, Inc. (U.S.)

- IBM Corporation (U.S.)

- Jabil Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- In December 2025, GlobalFoundries (GF) partnered with Finnish VC firm Cloudberry to strengthen Europe’s semiconductor and photonics startup ecosystem. GF will invest in Cloudberry’s new fund and provide technology expertise, resources, and design support to help startups scale from concept to industrial production.

- In December 2025, Marvell Technology announced its acquisition of Celestial AI for approximately USD 3.25 billion, with the intention of integrating Celestial AI’s Photonic Fabric technology into next-generation AI and cloud data centers. The platform enables high-bandwidth, low-latency, and energy-efficient optical interconnects for multi-rack AI systems, replacing traditional copper

- In September 2025, Coherent Corp. unveiled 400 mW continuous-wave lasers for silicon photonics and co-packaged optics applications. The 1311 nm lasers offer stable high power, low noise, and narrow linewidths, addressing key challenges in optical interconnects. Engineering samples are available now, with volume production expected in Q3 2026.

- In September 2025, Synopsys partnered with TSMC to advance AI and multi-die chip designs using TSMC’s cutting-edge processes and packaging technologies. They provide certified EDA flows, 3DIC Compiler tools, and AI-optimized photonic design for improved performance, power efficiency, and thermal management.

- In April 2025, Jabil launched a 1.6T pluggable optical transceiver utilizing Intel Silicon Photonics, which supports either dual 800G Ethernet connections or a single 1.6T connection, catering to high-speed data centers and AI workloads. The transceiver is energy-efficient, doubles rack bandwidth without infrastructure changes, and maintains high reliability.

- In March 2025, MaxLinear and Jabil started production of silicon photonics-based 800G pluggable optical modules, designed for AI/ML and high-speed data center applications. The modules use Intel’s silicon photonics platform and MaxLinear’s 5nm 800G PAM4 DSP, offering high reliability, efficiency, and scalability.

- In March 2025, GlobalFoundries certified four Ansys Lumerical photonic design tools, FDTD, MODE, CHARGE, and HEAT, for its GF Fotonix silicon photonics platform. This enables engineers to design high-performance passive and active photonic components, simulate electrical and thermal effects, reduce costs, and accelerate the development of photonic integrated circuits for AI, autonomous vehicles, hyperscale data centers, and IoT applications.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 23.83% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Component, Product, Application, and Region |

|

By Component |

· Photodetectors · Optical Waveguides · Wavelength-Division Multiplexing (WDM) Filters · Laser · Optical Modulators |

|

By Product |

· Transceivers · Active Optical Cables · Optical Multiplexers · Optical Attenuators · Others |

|

By Application |

· Data Centers and High Performance Computing · Consumer Electronics · Healthcare & Life Sciences · Aerospace · Defense and Security · Automotive · Others (Agriculture, etc.) |

|

By Region |

· North America (By Component, Product, Application, and Country/Sub-region) o U.S. o Canada o Mexico · Europe (By Component, Product, Application, and Country/Sub-region) o U.K. o Germany o France o Italy o Spain o Russia o Benelux o Nordics o Rest of Europe · Asia Pacific (By Component, Product, Application, and Country/Sub-region) o China o India o Japan o South Korea o ASEAN o Oceania o Rest of Asia Pacific · South America (By Component, Product, Application, and Country/Sub-region) o Brazil o Argentina o Rest of South America · Middle East & Africa (By Component, Product, Application, and Country/Sub-region) o Turkey o Israel o GCC o North Africa o South Africa o Rest of Middle East & Africa |

Frequently Asked Questions

The global silicon photonics market size is projected to grow from $4.03 billion in 2026 to $22.29 billion by 2034, at a CAGR of 23.83% during the forecast period

In 2025, the market value stood at USD 1.13 billion.

The market is expected to exhibit a CAGR of 23.83% during the forecast period.

By application, the defense and security is expected to lead the market.

Rising computational demands from AI and ML will fuel the market growth.

Intel Corporation, Cisco Systems, Inc., GlobalFoundries Inc., and Lumentum Operations LLC (U.S.) are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 105

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us