Naval Directed Energy Systems Market Size, Share & Industry Analysis, By Technology (High-Energy Laser (HEL) Systems, High-Power Microwave (HPM) Systems, and Others), By Platform (Destroyers, Frigates, Aircraft Carriers, Amphibious Warfare Ships, and Others), By Application (Air and Missile Defense, Counter-Unmanned Aerial Systems, Anti-Swarm Defense, Anti-Surface Defense, and Others), By Range (Less than 50 kW, 50–150 kW, 150–300 kW, and Above 300 kW), By End User (Navy, Coast Guard, Naval Special Operations Forces, and Defense Research, and Others), and Regional Forecast, 2026-2034

Naval Directed Energy Systems Market Size and Future Outlook

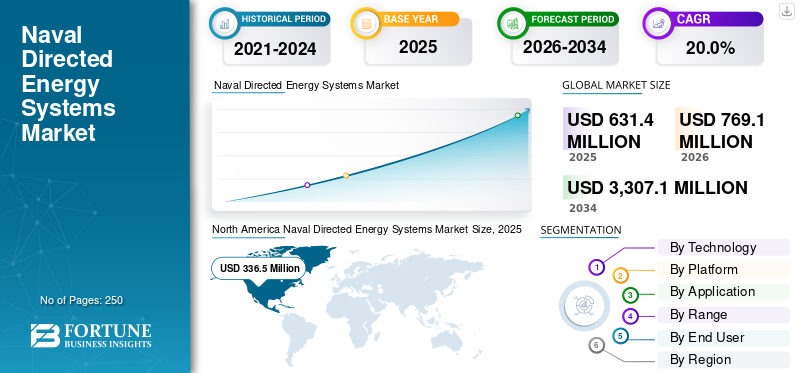

The global naval directed energy systems market size was valued at USD 631.4 million in 2025. The market is projected to grow from USD 769.1 million in 2026 to USD 3,307.1 million by 2034, exhibiting a CAGR of 20.0% during the forecast period. North America dominated the naval directed energy systems market with a market share of 53.29% in 2025.

Naval directed energy systems represent a critical component of aerospace and defense technologies, delivering high-energy laser weapon systems, microwave weapons, and particle-beam technologies for precision threat neutralization, non-kinetic fleet defense, and power-efficient countermeasures in maritime operations. The global market within the aerospace and defense sector is surging, fueled by escalating geopolitical tensions, evolving anti-access/area-denial (A2/AD) threats, and next-generation naval platforms demanding scalable, magazine-independent weapon systems on next-generation naval platforms.

Leading industrial players such as Lockheed Martin, Raytheon Technologies (RTX), BAE Systems, and Northrop Grumman are advancing innovations such as solid-state laser weapon systems (SSLWS), high-power microwave (HPM) effectors for drone swarm defense, and integrated directed energy architectures for shipboard and submarine applications. These innovations are intended to support persistent maritime superiority, counter-hypersonic threats, and resilient naval force projection in contested operational environments.

Download Free sample to learn more about this report.

NAVAL DIRECTED ENERGY SYSTEMS MARKET TRENDS

AI and AI-Powered Targeting in Laser Systems is Emerging as a Defining Market Trend

Artificial intelligence (AI) and AI‑powered targeting are emerging as a significant trend in the industry. Integration of AI in laser and microwave weapon systems is helping optimize the way ship‑borne defense platforms detect, prioritize, and engage threats. AI‑driven algorithms enhance target acquisition by fusing data from multiple sensors, enabling rapid identification between hostile and non‑hostile platforms in complex maritime and electromagnetic environments.

- For instance, in April 2026, AeroVironment (AV) announced a demonstration of its palletized LOCUST Laser Weapon System (LWS) neutralizing drone threats at sea in collaboration with the U.S. Navy and Army RCCTO. It features advanced AI capabilities across the "kill chain," including detection, identification, and hard-kill engagement, enabling rapid and reliable defense against drones.

These systems leverage machine learning for real‑time tracking, predicting target trajectories, and optimizing engagement windows, which is critical for countering fast‑maneuvering missiles, drones, and small‑boat swarms. Furthermore, the integration of AI supports autonomous or semi‑autonomous operation modes, which are expected to remain a significant trend in the market during the forecast period.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Defense Budgets and Geopolitical Tensions are Propelling Market Growth

Rising defense budgets and escalating geopolitical tensions are acting as a primary driver for the market, accelerating the development, procurement, and deployment of ship‑borne laser and microwave weapon systems. Increased regional rivalries and asymmetric threats such as drones, cruise missiles, and small‑boat swarm attacks are pushing naval forces to modernize their fleet‑level defense systems beyond traditional kinetic armaments.

- For instance, in April 2026, the Australian Government awarded contracts worth USD 21.3 million to AIM Defence for portable high-energy laser systems and USD 10.4 million to SYPAQ Systems for Corvo Strike interceptor drone projects under ASCA's Mission Syracuse initiative.

These contracts aim to strengthen sovereign counter-drone systems, influenced by operational lessons from the Ukraine/Middle East conflicts and supported by the 2026 National Defence Strategy and Integrated Investment Program. As defense expenditures increase globally, a growing portion of investment is being directed toward next‑generation technologies, including directed energy weapons, which offer lower cost‑per‑shot and deeper operational magazines compared to missiles and gun‑based systems. This funding is accelerating R&D, technology maturation, and integration efforts for naval directed energy systems across multiple platforms.

MARKET RESTRAINTS

High Development and Deployment Costs to Limit Market Expansion

High development and deployment costs, along with the evolving technological maturity of naval directed energy systems, remain significant market restraints. Underlying technologies such as high‑power lasers, advanced beam‑control systems, and associated power and cooling infrastructure require substantial upfront investment in research, engineering, and testing to achieve militarily relevant performance levels. In addition, naval integration further compounds expenses due to stringent requirements for shock resistance, electromagnetic compatibility, and platform‑specific modifications. These factors increase design, qualification, and integration costs, thereby hampering the naval directed energy systems market growth.

MARKET OPPORTUNITIES

Integration of the Product in Counter-Drone/UAS Operations Presents Several Growth Opportunities for the Market

The integration of naval directed energy systems into counter‑drone/UAS operations by the Department of Defense presents a major growth opportunity for the market, as unmanned aerial threats become central to modern maritime security. The rising use of small, low‑cost drones has driven navies to seek scalable, cost-effective defense systems that can handle large‑volume, swarm‑like attacks without depleting expensive missile magazines.

Directed energy weapons, particularly high‑energy lasers and high‑power microwaves, offer these capabilities by enabling rapid engagement of multiple targets at a fraction of the cost‑per‑shot of kinetic interceptors. This opportunity is being validated through operational demonstrations, such as the U.S. Navy trials of AeroVironment’s containerized Locust X2 P‑HEL aboard the USS George H. W. Bush (CVN‑77) in October 2025, during which the system downed all 17 UAS targets in live‑fire tests. Adapted from the U.S. Army’s Rapid Capabilities and Critical Technologies Office (RCCTO), the system underwent about 10 major navaliization upgrades to support maritime deployment requirements. Furthermore, counter‑UAS architectures increasingly emphasize layered, sensor‑fused approaches, where naval directed energy systems are integrated with radars, RF detectors, electronic warfare suites, and electro‑optical/infrared tracking systems.

MARKET CHALLENGES

Absence of Robust Standardization and Well‑Defined Frameworks Is a Key Market Challenge

One significant market challenge for the naval directed energy systems sector lies in the absence of robust standardization and well‑defined doctrinal frameworks governing how these systems should be integrated into existing platform‑level combat architectures and operational concepts. Naval fleets typically comprise diverse, heterogeneous platforms equipped with legacy sensor suites, command‑and‑control ecosystems, and established rules of engagement. This complexity makes it difficult to establish uniform technical interfaces, performance benchmarks, and employment doctrines for directed energy weapons across different vessel classes and mission profiles.

Segmentation Analysis

By Technology

Layered Ship Defense Requirements Supported High-Energy Laser (HEL) Systems Segment Expansion

Based on technology, the market is divided into high-energy laser (HEL) systems, high-power microwave (HPM) systems, electromagnetic railgun systems, and particle beam/advanced directed energy concepts.

The high-energy laser (HEL) systems segment is leading the market. It is projected to witness strong growth as naval forces prioritize layered defensive architectures capable of engaging drones, fast attack threats, and selected airborne targets at the speed of light. HEL systems are gaining traction as they combine precision engagement with low cost per shot, while also reducing dependence on finite missile inventories f. Their integration potential is improving as programs such as the U.S. Navy’s HELIOS move from development into shipboard integration, reinforcing confidence in operational viability.

- For instance, in January 2024, the U.K. Ministry of Defence announced that DragonFire had achieved the U.K.’s first high-power firing of a laser weapon against aerial targets, while also demonstrating the ability to track moving air and sea targets with very high accuracy at range.

The high-power microwave (HPM) systems segment is anticipated to rise with a CAGR of 21.6% over the forecast period.

By Platform

Naval Modernization Programs Support Destroyers Segment Growth

By platform, the market is segmented into destroyers, frigates, aircraft carriers, amphibious warfare ships, unmanned surface vessels (USVs), and others.

The destroyers segment dominates the market as it remains the most capable and power-rich surface combatants in frontline naval service. These vessels are already central to air defense, fleet escort, maritime security, and missile defense missions, making them ideal platforms for the early integration of directed energy systems. Several publicly disclosed naval programs have also concentrated on destroyer-class platforms, including the Optical Dazzling Interdictor (ODIN) system and HELIOS laser weapon system integration on Arleigh Burke-class destroyers. These ongoing modernization efforts are significantly contributing to segment growth.

The Unmanned Surface Vessels (USVs) segment is projected to grow at a CAGR of 23.0% over the forecast period.

By Application

Counter-Unmanned Aerial Systems Segment to Lead due to Rising Naval Threats From Drones and Loitering Systems

By application, the market is segmented into air and missile defense, counter-unmanned aerial systems, anti-swarm defense, anti-surface defense, electronic warfare, and intelligence, surveillance, and reconnaissance support.

The counter-unmanned aerial systems segment is projected to hold the largest naval directed energy systems market share owing to an increase in demand for advanced shipborne defense solutions against low-cost drones, loitering systems, and saturation-style aerial threats. Naval and defense programs continue to emphasize drone neutralization as a primary mission set for shipboard laser and related directed energy capabilities. This segment is also benefiting from the growing need for rapid re-engagement, precise target discrimination, and improved resilience against repeated attacks in congested maritime operating environments.

- For instance, in September 2024, Rheinmetall and MBDA Deutschland signed a cooperation agreement to bring a joint maritime laser weapon product within five to six years. This initiative builds on the Sachsen frigate demonstrator program, which reportedly completed more than 100 test shots.

The electronic warfare segment is projected to grow at a CAGR of 17.5% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Range

50–150 kW Segment to Lead due to Growing Demand for Counter-UAS Operations

Based on range, the market is segmented into Less than 50 kW, 50–150 kW, 150–300 kW, and above 300 kW.

The 50–150 kW segment is expected to hold the largest share in the market due to the increasing deployment of systems within this power range for counter-UAS operations, short-range air defense, and point-protection missions. This band is also supported by several prominent defense programs, including the U.S. Navy’s 60+ kW-class HELIOS and Rafael’s 100 kW Naval Iron Beam solution for maritime defense applications. As naval operators favor scalable solutions with credible near-term adoption pathways, the 50–150 kW category is expected to witness robust commercial and programmatic momentum.

The 150–300 kW segment is expected to grow at a CAGR of 19.4% over the forecast period.

By End User

Navy Segment to Lead due to Rising Fleet Protection Priorities

On the basis of end user, the market is segmented into navy, coast guard, naval special operations forces, and defense research and test organizations.

Navy segment is expected to remain a primary dominant segment in the market as navies are the primary operators of surface combatants, fleet escorts, and maritime defense networks where directed energy systems are most actively being evaluated and deployed. Naval forces are under increasing pressure to protect ships, crews, sensors, and mission systems from drones, missiles, and other asymmetric threats without over-relying on expensive kinetic interceptors.

- For instance, in August 2022, Lockheed Martin announced delivery of the U.S. Navy’s 60+ kW-class HELIOS system, describing it as the first tactical laser weapon system to be integrated into existing ships and intended to support counter-UAS, ISR, and related ship-defense missions.

The coast guard segment is projected to grow at a CAGR of 18.2% over the forecast period.

Naval Directed Energy Systems Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, and the Rest of the World.

North America

North America Naval Directed Energy Systems Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the market in 2025 with a valuation of USD 336.5 million and is projected to reach USD 406.5 million by 2026. The region experiences significant growth due to its large naval procurement base, early transition of programs from demonstration to shipboard integration, and sustained investment in both high-energy laser and high-power microwave technologies. Growth is being supported by the U.S. Navy’s increasing focus on layered ship defense, counter-UAS capability, protection against fast inshore threats, and the broader requirement to reduce the cost burden of using kinetic interceptors against lower-cost aerial and surface threats. Moreover, U.S. Navy and defense program developments continue to showcase that naval HEL and HPM systems remain high-priority technologies for defensive maritime applications, supporting regional market growth during the forecast period.

- For instance, in February 2025, U.S. Navy test reporting released through DOT&E showed that USS Preble (DDG-88) used its HELIOS system against an unmanned aerial vehicle target. This highlighted continued progress in operational shipboard laser testing beyond laboratory and pier-side demonstrations.

U.S. Naval Directed Energy Systems Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market stood at around USD 319.7 million in 2025. The country is expected to witness strong growth in the market due to its dominant naval procurement position, large installed base of surface combatants, and sustained investment in shipboard laser and high-power microwave technologies. Growth is being supported by the U.S. Navy’s requirement to strengthen layered fleet defense against unmanned aerial systems, cruise missiles, and other asymmetric threats while improving magazine depth and reducing the cost burden associated with kinetic interceptors.

Europe

Europe is projected to record the fastest growth rate of 22.4% from 2026 to 2034. The region is expected to witness steady growth in the market owing to rising maritime-security pressures, stronger emphasis on naval air and drone defense, and visible movement from trial activity toward deployable capability. The growth is further supported by the need for European naval forces to strengthen close-in defense against uncrewed platforms, saturation attacks, and other asymmetric threats while reducing reliance on high-cost conventional interceptors. The U.K.’s DragonFire program, Germany’s successful laser trials at sea aboard frigate Sachsen, and France’s HELMA-P testing aboard the Forbin are significantly contributing to the European directed energy weapons market growth.

- For instance, in April 2024, the U.K. Ministry of Defence stated that DragonFire is expected to be installed on Royal Navy warships beginning in 2027, accelerating one of Europe’s most visible naval laser deployment pathways.

U.K. Naval Directed Energy Systems Market

The U.K.’s market in 2025 stood at around USD 53.4 million, representing roughly 8.5% of global revenues.

Germany Naval Directed Energy Systems Market

Germany’s market reached approximately USD 39.0 million in 2025, equivalent to around 6.2% of global sales.

Asia Pacific

Asia Pacific is projected to be the fastest-growing region in the market due to accelerating maritime modernization, rising demand for counter-drone and point-defense capability, and increasing investment in indigenous high-power energy technologies. Growth is further supported by the region’s expanding naval threat environment, the need to protect high-value surface combatants and maritime infrastructure, and a broader push to improve cost-effective response options against UAVs, rockets, and other emerging threats.

- For instance, in April 2025, the Indian Navy successfully tested a 30 kW truck‑mounted Directed Energy Weapon (DEW) at the Kurnool Test Range, validating its ability to neutralise drones and small aerial targets. The system, part of DRDO’s laser‑weapon program, demonstrated speed‑of‑light engagement and low‑cost intercepts against aerial threats.

Japan Naval Directed Energy Systems Market

The Japanese market in 2025 stood at around USD 15.6 million, accounting for roughly 2.5% of global revenues.

China Naval Directed Energy Systems Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues standing at around USD 28.8 million, representing roughly 4.6% of global sales.

India Naval Directed Energy Systems Market

The Indian market in 2025 stood at around USD 24.6 million, accounting for roughly 3.9% of global revenues.

Rest of the World

The Rest of the World is expected to witness moderate but sustained growth in the market due to the gradual strengthening of maritime security capabilities across Latin America and Africa. Demand is being supported by the need to improve cyber resilience across naval shore infrastructure, port environments, maritime communications, and defense support systems as countries expand digital connectivity within their security architectures.

Latin America Naval Directed Energy Systems Market

The Latin America market stood at around USD 19.1 million, accounting for roughly 1.4% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Industry Players Focus on Delivering Modular Directed Energy Architectures to Gain Competitive Edge

The global naval directed energy systems market is characterized by extensive collaboration among naval forces, defense ministries, system integrators, major defense contractors, and directed energy‑technology specialists involved in the development of high‑energy laser and microwave effectors, integrated beam‑control systems, shipboard power and thermal‑management upgrades, and resilient command‑and‑control architectures for maritime platforms. Market leadership is increasingly being shaped by players capable of delivering scalable, modular directed energy architectures, open‑architecture integration with existing C4ISR and combat‑management systems, fleet‑wide hardening against advanced threats, and seamless technology insertion across destroyers, frigates, corvettes, unmanned surface vessels, and future‑focused naval platforms.

LIST OF KEY NAVAL DIRECTED ENERGY SYSTEMS COMPANIES PROFILED

- Lockheed Martin Corporation (U.S.)

- RTX Corporation / Raytheon (U.S.)

- Northrop Grumman Corporation (U.S.)

- BAE Systems plc (U.K.)

- MBDA (France)

- Leonardo S.p.A. (Italy)

- QinetiQ Group plc (U.K.)

- Rheinmetall AG (Germany)

- Thales Group (France)

- Rafael Advanced Defense Systems Ltd. (Israel)

KEY INDUSTRY DEVELOPMENTS

- April 2026: AeroVironment announced that its palletized LOCUST Laser Weapon System had been successfully demonstrated aboard USS George H.W. Bush (CVN-77) during an October 2025 live-fire event conducted with the U.S. Navy and the U.S. Army RCCTO. During the demonstration, the system reportedly detected, tracked, engaged, and neutralized multiple unmanned aerial vehicles.

- November 2025: MBDA stated that it had been awarded a USD 427.9 million (GBP 316 million) contract to deliver new DRAGONFIRE laser weapon systems to the Royal Navy from 2027, marking a major milestone for operational naval laser deployment in Europe.

- November 2025: The Royal Navy announced successful DRAGONFIRE trials in which the system detected, tracked, engaged, and destroyed high-speed drones beyond the horizon. The trials were described as a U.K. first and a significant step toward shipboard deployment.

- September 2025: The Israel Ministry of Defense and Rafael Advanced Defense Systems Ltd. announced the completion of development for the Iron Beam high-power laser system following final testing.

- June 2025: Coherent Aerospace & Defense received a USD 29.98 million U.S. Navy contract under the SONGBOW project to develop pulsed fiber lasers and a 400 kW directed-energy subsystem by integrating a 50 kW laser with a beam-control assembly, supporting future naval directed-energy scaling.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 20.0% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Technology, By Platform, By Application, By Range, By End User, and Region |

| By Technology |

|

| By Platform |

|

| By Application |

|

| By Range |

|

| By End User |

|

| By Geography |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 631.4 million in 2025 and is projected to reach USD 3,307.1 million by 2034.

In 2025, the market value stood at USD 336.5 million.

The market is expected to exhibit a CAGR of 20.0% during the forecast period.

By application, the counter-unmanned aerial systems segment is expected to lead the market.

Rising defense budgets and geopolitical tensions are the key factors driving the market.

Lockheed Martin Corporation, RTX Corporation/Raytheon, Northrop Grumman Corporation, and BAE Systems plc are some of the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us