Naval Vessels Acoustic Quieting Technologies Market Size, Share & Industry Analysis, By Technology (Machinery Noise & Vibration Isolation Technologies, Propulsion Quieting Technologies, and Others), By Vessel (Submarines, Frigates, Destroyers, Corvettes, and others), By Application (Acoustic Signature Reduction, Anti-Submarine Warfare Survivability, Mine Warfare, and Others), By Technology Integration (New-Build Integration and Retrofit/Modernization), By End User (Navy/Naval Forces, Coast Guard/Maritime Security Agencies, Defense Shipyards, and Others), and Regional Forecast, 2026-2034

Naval Vessels Acoustic Quieting Technologies Market Size and Future Outlook

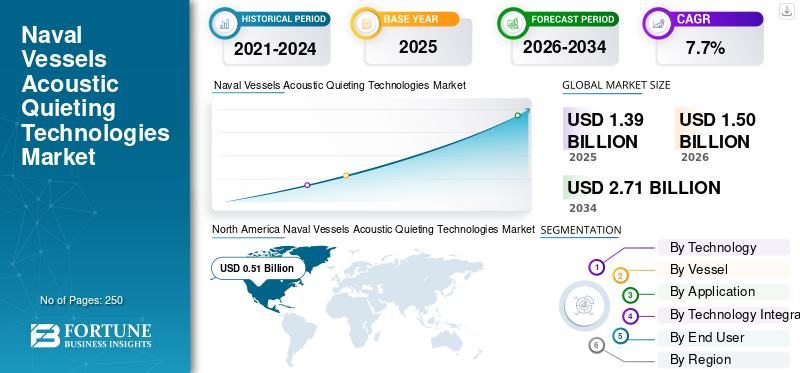

The global naval vessels acoustic quieting technologies market size was valued at USD 1.39 billion in 2025. The market is projected to grow from USD 1.50 billion in 2026 to USD 2.71 billion by 2034, exhibiting a CAGR of 7.7% during the forecast period. North America dominated the naval vessels acoustic quieting technologies market with a market share of 36.69% in 2025.

Naval acoustic quieting technology forms a critical component of modern underwater warfare, utilizing advanced materials, vibration isolation, and structural design to minimize the acoustic signature of naval platforms. The global market is expanding steadily, driven by the increasing sophistication of anti-submarine warfare (ASW) sensors, the rising use of autonomous underwater vehicles (AUVs), and the strategic necessity for stealth capabilities in contested maritime environments.

Leading industrial players such as Hutchinson Aerospace & Industry, Trelleborg Anti-Vibration Solutions, and Rubber Design B.V. are advancing innovations focused on enhancing operational stealth. Key technological developments include the implementation of specialized anechoic coatings, high-performance vibration-damping systems, active noise-cancellation architectures, and advanced propulsion designs that mitigate cavitation and mechanical ship noise.

Download Free sample to learn more about this report.

NAVAL VESSELS ACOUSTIC QUIETING TECHNOLOGIES MARKET TRENDS

Development of Advanced and Sophisticated Materials for Soundproofing is Emerging as a Key Market Trend

A significant trend shaping the naval vessels' acoustic quieting technologies market is the growing focus on frequency-specific acoustic stealth solutions and advanced soundproofing materials. There is increased focus on the design of next-generation materials to attenuate specific acoustic signatures generated by high-output propulsion systems and sensitive onboard electronic suites.

- For instance, in April 2026, India developed a new hull-coating technology that reduces acoustic signatures by ~6 dB insertion loss and echo reduction, significantly boosting submarine stealth and detectability evasion. The innovation is designed for both conventional and nuclear submarines, enhancing survivability in dense sensor maritime environments without disclosed deployment timelines.

This trend is becoming increasingly critical as contemporary naval platforms operate in contested littoral environments where acoustic signature management directly dictates operational survivability. Manufacturers are integrating these targeted materials directly into structural bulkheads, machinery foundations, and hull-mounted tiles to disrupt harmonic noise propagation at the source. In addition, innovative acoustic quieting technologies, particularly those involving advanced propulsion and hydrodynamic optimization, significantly reduce vessel drag, thereby directly lowering greenhouse gas emissions during maritime operations.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Defense Budgets and Submarine Fleet Modernization Programs are Propelling Market Growth

The rising use of advanced anti-submarine warfare (ASW) capabilities is driving a massive surge in defense spending, effectively transforming acoustic stealth into the primary metric of naval parity. As nations accelerate the modernization of submarine fleets, demand for cutting-edge acoustic quieting technologies has become an essential requirement for next-generation platform development.

- For instance, Russia's Ministry of Defense launched a modernization program in 2022 to equip nuclear submarines with advanced heavy rubber plates designed to suppress vessel noise and sonar signals, thereby enhancing underwater stealth performance.

This growing investment priority is driven by the strategic need to counter evolving A2/AD threats, where even marginal improvements in acoustic signature reduction provide decisive operational advantages. Modern acoustic quieting solutions, such as electric propulsion and optimized hull geometries, improve overall energy efficiency by minimizing the sound levels and ship noise levels. Governments are consistently allocating significant portions of their naval budgets toward the procurement of stealth-integrated vessels, creating sustained demand for high-performance acoustic materials and systems. In addition, compliance with evolving International Maritime Organization (IMO) noise reduction guidelines is increasingly driving the adoption of commercial-grade silencing technologies that bridge the gap between naval stealth and civilian maritime standards.

MARKET RESTRAINTS

High Development Cost and Technical Complexities to Limit Market Expansion

The market faces significant constraints driven by the high technical complexity and capital-intensive nature of maritime defense systems. High development costs for proprietary stealth materials, which require extensive R&D and specialized, high-cost manufacturing facilities, exceed the budgetary flexibility of even major naval programs. Furthermore, the integration of these sophisticated soundproofing technologies into existing vessel architectures poses a severe logistical challenge. Supply chain vulnerabilities regarding rare-earth elements or specialized polymers used in next-generation anechoic coating lead to delivery delays and hamper the market naval vessels acoustic quieting technologies market growth.

MARKET OPPORTUNITIES

Ongoing Digital Transformation of Maritime Operations Presents Growth Opportunities for the Market

The ongoing digital transformation across naval commercial operations presents a significant opportunity for the naval vessels acoustic quieting technologies market. Modern naval platforms are increasingly shifting toward modular, software-defined countermeasures. Unlike traditional, static acoustic treatments, modern digital naval architectures allow the integration of modular systems that can be updated throughout a vessel's lifecycle to counter emerging threat signatures. This approach leverages high-speed onboard data processing to create adaptive acoustic profiles, allowing platforms to dynamically adjust their underwater radiated noise based on real-time mission requirements and environmental conditions. By utilizing open-system architectures, shipbuilders can now incorporate scalable and upgradeable acoustic dampening components that are easily swappable, significantly reducing the downtime associated with conventional mid-life upgrades.

MARKET CHALLENGES

Lack of Highly Skilled Labor and Customized Shipyard Infrastructure Hinders Market Expansion

The naval vessels acoustic quieting technologies market is significantly constrained by the inherent rigidity of defense procurement cycles, which frequently conflict with the rapid pace of technological innovation. These lengthy acquisition processes often span several years, creating a critical misalignment between initial design specifications and the evolving threat landscape faced by modern fleets. Furthermore, the specialized installation of advanced acoustic materials and decoupling suites needs highly skilled labor and customized shipyard infrastructure. Such complex integration requirements require extensive vessel dry-docking, leading to prolonged operational downtime that can compromise fleet readiness schedules.

Segmentation Analysis

By Technology

Growing Emphasis On Reducing Propeller Cavitation Boosts Propulsion Quieting Technologies Segment Growth

Based on technology, the market is divided into machinery noise & vibration isolation technologies, propulsion quieting technologies, hull & hydrodynamic noise reduction technologies, acoustic materials, coatings & treatments, and others.

The machinery noise & vibration isolation technologies include resilient mounts, shock mounts, raft-mounted machinery systems, flexible couplings, vibration isolators, and others. The propulsion quieting technologies comprise low-cavitation propellers, pump-jet propulsors, shaft-line quieting systems, quiet bearings, waterjet noise reduction systems, and others. Moreover, acoustic materials, coatings & treatments are further subdivided into anechoic tiles, elastomeric acoustic coatings, damping sheets/damping layers, acoustic insulation materials, and composite acoustic treatments.

The propulsion quieting technologies segment is leading the market and is expected to witness strong growth as navies place greater emphasis on reducing propeller cavitation, shaft-line vibration, and propulsion-radiated acoustic signatures. Demand is being driven by submarine modernization, ASW frigate procurement, and the need for vessels to operate with lower detectability in contested undersea environments. Low-cavitation propellers, pump-jet propulsors, quiet bearings, and shaft-line quieting systems are becoming increasingly important as passive sonar networks and acoustic surveillance capabilities improve.

For instance, in April 2024, Damen Naval selected Kongsberg Maritime Sweden to supply controllable pitch propellers and shaft lines for four Netherlands-Belgium ASW frigates. The vessels are being designed with hybrid diesel-electric propulsion systems to ensure extremely quiet operations.

The machinery noise & vibration isolation technologies segment is anticipated to rise with a steady growth rate of a CAGR of 8.1% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Vessel

Submarines Segment Leads due to Rising Investment in Quieter Propulsion Technologies

By vessel, the market is segmented into submarines, frigates, destroyers, corvettes, offshore patrol vessels, amphibious ships, and mine countermeasure vessels.

The submarines segment dominates the market, as destroyers remain among the most stealth-oriented and power-rich surface combatants in frontline naval service. These vessels are already central to air defense, fleet escort, maritime security, and missile defense missions, making them a key platform for the early integration of acoustic quieting technologies s. Submarines drive demand for acoustic quieting technologies as stealth is central to survivability, especially against modern sonar, ASW aircraft, and sensor networks. Navies are investing in quieter propulsion, vibration isolation, and signature reduction to improve mission endurance and reduce detectability in contested waters.

Rising submarine modernization programs and new-build fleets are therefore expanding the need for advanced quieting materials, coatings, and systems.

- For instance, in October 2025, Saab received a new order from Sweden’s FMV to complete the final production phase for two Blekinge-class A26 submarines. The order also included additional materials and services tied to Saab’s cutting-edge signature management and low-detectability submarine design.

The frigates segment is projected to grow with a steady annual growth rate of 7.9% over the forecast period.

By Application

Increasing Importance of Passive Sonar to Support Acoustic Signature Reduction Segment Growth

By application, the market is segmented into acoustic signature reduction, anti-submarine, warfare survivability, mine warfare/low-signature operations, special operations/covert maritime missions, and sonar self-noise reduction).

The acoustic signature reduction segment is projected to hold the largest naval vessels acoustic quieting technologies market share as naval forces prioritize reduced detectability across submarines, ASW frigates, MCM vessels, and selected unmanned maritime platforms. Demand is driven by the increasing importance of passive sonar, seabed sensors, sonobuoys, and undersea surveillance systems in modern naval operations. Acoustic signature reduction focus is increasing through rapid adoption of propulsion quieting, vibration isolation, structural damping, acoustic materials, hydrodynamic noise reduction, and onboard monitoring.

- For instance, in November 2025, Poland selected Saab’s A26 submarine design for its Orka program, with the platform promoted for very low acoustic and magnetic signatures and Saab’s Baltic Sea stealth experience.

The anti-submarine warfare survivability segment is projected to grow at a CAGR of 9.3% over the forecast period.

By Technology Integration

New-Build Integration Segment to Dominate as It Allows Navies to Optimize Machinery Layout

By technology integration, the market is segmented into new-build integration and retrofit/ modernization.

The new-build integration segment is expected to dominate the market, as effective acoustic quieting is most successful when it is engineered into the vessel from the outset, allowing propulsion, machinery isolation, and hull design to work together. New-build programs allow navies and shipyards to optimize machinery layout, raft mounting, propulsion design, hull form, damping materials, acoustic coatings, and signature modelling from the beginning of the platform lifecycle.

The retrofit/modernization segment is projected to grow at a CAGR of 6.5% over the forecast period.

By End User

Rising Defense Spending Boosts Navy/Naval Forces Segment Growth

On basis of end user, the market is segmented into navy/naval forces, coast guard/maritime security agencies, defense shipyards, and naval design & engineering organizations.

The navy/naval forces segment holds the largest share as modern fleets increasingly rely on acoustic quieting to improve stealth, survivability, and mission effectiveness in anti-submarine warfare environments. Navies are also upgrading older vessels and investing in new platforms that require lower radiated noise levels to reduce detectability by advanced sonar systems. Moreover, rising defense spending and the need for operational advantage in contested maritime zones are pushing the adoption of quieting technologies across ships and submarines in the naval sector, which drives segment growth.

The naval design & engineering organizations segment is projected to grow at a CAGR of 10.5% over the forecast period.

Naval Vessels Acoustic Quieting Technologies Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Naval Vessels Acoustic Quieting Technologies Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the market in 2025, reaching USD 0.51 billion. The market is expected to reach USD 0.55 billion by 2026. The region experiences strong growth due to the large U.S. naval procurement base, continued investment in nuclear submarines, advanced surface combatants, unmanned undersea systems, and acoustic-signature management infrastructure. Growth is supported by the U.S. Navy’s requirement to maintain undersea superiority, reduce sound pressure level and vessel detectability, improve sonar self-noise performance, and enhance survivability against increasingly capable passive sonar and anti-submarine warfare networks. Moreover, the U.S. shipbuilding base continues to support Virginia-class and Columbia-class submarine activity, where propulsion quieting, vibration isolation, acoustic coatings, and structural noise-control solutions remain critical parts of platform performance.

- For instance, in April 2025, General Dynamics Electric Boat announced USD 12.40 billion in contract modifications for the construction of two FY2024 Virginia-class submarines, with options that could raise the cumulative value to USD 17.20 billion. This supports continued demand for submarine-linked acoustic quieting, propulsion quieting, vibration isolation, and signature-management technologies in North America.

U.S. Naval Vessels Acoustic Quieting Technologies Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market stood at around USD 0.49 billion in 2025. The U.S. is expected to witness steady growth due to its robust submarine industrial base, large installed fleet of destroyers and submarines, and continued investments in ship modernization, maintenance, and lifecycle readiness. NAVSEA’s 2025 enterprise strategy also emphasizes ship, submarine, and system modernization and sustainment, supporting the long-term demand for acoustic signature-related engineering and integration activities.

Europe

Europe is projected to record the fastest growth rate of 8.0% during 2026 to 2034. Europe is expected to witness strong growth due to the region’s concentration of submarine builders, ASW frigate programs, mine countermeasure vessel modernization, and rising demand for acoustic signature reduction across NATO and European naval forces. Growth is further supported by the U.K., France, Germany, Italy, Sweden, Norway, Spain, Turkey, and Russia, which collectively maintain significant submarine, surface combatant, and naval engineering ecosystems. The region’s growth is also being driven by increasing emphasis on advanced acoustic materials, low-noise propulsors, hydrodynamic quieting, and lifecycle signature-management technologies.

- For instance, in November 2025, the European Defence Agency (EDA) initiated a USD 5.62 million, four-year SPHYDA research program to reduce underwater noise from autonomous underwater vehicles (AUVs), enhancing naval stealth and marine life protection. The program, led by Italy in collaboration with Germany, the Netherlands, Spain, and Norway, plus nine partners, focuses on developing numerical models and conducting tests to analyze hull-rudder-propeller noise generation.

U.K. Naval Vessels Acoustic Quieting Technologies Market

The U.K.’s market in 2025 stood at around USD 0.11 billion, representing roughly 7.8% of global revenues.

Germany Naval Vessels Acoustic Quieting Technologies Market

Germany’s market reached approximately USD 0.07 billion in 2025, equivalent to around 5.4% of global sales.

Asia Pacific

Asia Pacific is projected to be the fastest-growing region in the market and is expected to record the fastest growth due to expanding submarine fleets, rising ASW requirements, Indo-Pacific maritime competition, and strong naval construction activity across China, India, Japan, South Korea, and Australia. Growth is further supported by new-build submarine programs, destroyer and frigate procurement, underwater surveillance requirements, and the increasing need for low-noise propulsion, machinery isolation, anechoic treatments, and acoustic modelling.

- For instance, in March 2025, Australia released its AUKUS Submarine Industry Strategy, outlining the development of a sovereign industrial base to build, operate, and sustain future conventionally armed nuclear-powered submarines while sustaining and upgrading the Collins-class fleet.

Japan Naval Vessels Acoustic Quieting Technologies Market

The Japanese market in 2025 stood at around USD 0.05 billion, accounting for roughly 3.7% of global revenues.

China Naval Vessels Acoustic Quieting Technologies Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues standing at around USD 0.16 billion, representing roughly 11.7% of sales.

India Naval Vessels Acoustic Quieting Technologies Market

The Indian market in 2025 stood at around USD 0.07 billion, accounting for roughly 4.9% of global revenues.

Latin America and Middle East & Africa

The Latin America region is u, mainly driven by Brazil’s submarine program, selective naval modernization initiatives, and limited demand from countries such as Chile, Colombia, Argentina, and Mexico. Growth is supported by submarine construction activities, conventional submarine sustainment programs, surface-vessel refit operations, and gradual adoption of acoustic coatings, vibration isolation, and low-noise propulsion components. Moreover, the Middle East & Africa region is expected to witness moderate growth due to naval modernization in Saudi Arabia, the UAE, Egypt, Israel, Algeria, and South Africa. Demand is primarily linked to corvettes, frigates, OPVs, patrol vessels, and selected submarine fleets. Regional growth is supported by increasing requirements for machinery vibration control, acoustic materials, propulsion noise reduction, and improved survivability of surface combatants.

Saudi Arabia Naval Vessels Acoustic Quieting Technologies Market

The Saudi Arabia market in 2025 stood at around USD 0.02 billion, accounting for roughly 1.5% of global revenues.

COMPETITIVE LANDSCAPE

Key Players Emphasis on Delivering Intelligent Acoustic-Monitoring Architectures to Gain Competitive Edge

The global naval acoustic quieting technologies market is defined by collaboration among navies, defense ministries, system integrators, major shipbuilders, and materials-science specialists delivering advanced anechoic coatings, vibration-damping suites, precision propulsion-quieting modules, and intelligent acoustic-monitoring architectures for diverse maritime platforms. Market leadership is increasingly being shaped by players capable of supporting modular and scalable acoustic-signature management, seamless integration with existing C4ISR and combat-management systems, fleet-wide hardening against high-sensitivity passive sensors, and agile technology insertion across submarines, surface combatants, unmanned underwater vehicles, and next-generation stealth naval platforms.

LIST OF KEY NAVAL VESSELS ACOUSTIC QUIETING TECHNOLOGIES COMPANIES PROFILED

- Hutchinson Aerospace & Industry (France)

- Trelleborg Anti-Vibration Solutions (Sweden)

- Rubber Design B.V. (Netherlands)

- Socitec Group (France)

- Christie & Grey (U.K.)

- ITT Enidine (U.S.)

- Getzner Werkstoffe (Austria)

- Kongsberg Maritime (Norway)

- BAE Systems (U.K.)

- Wärtsilä Corporation (Finland)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Ultra Maritime received a U.S. Navy development contract for the next-generation Acoustic Device Countermeasure MK6, highlighting improved acoustic output and compatibility for undersea threat-response missions.

- February 2026: ITT’s Enidine announced that it would showcase shock and vibration isolation solutions for naval ships, submarines, and critical maritime applications at WEST 2026, directly supporting shipboard noise/vibration control and acoustic-stealth-related isolation requirements.

- January 2026: Kongsberg Maritime received a contract to supply its ultra-quiet rim-drive thrusters for a new advanced acoustic research vessel being built by GRSE for India’s Naval Physical and Oceanographic Laboratory under DRDO. The package includes two RD-AZ2600 azimuth thrusters, two RD-TT1600 tunnel thrusters, and the MCON control system, chosen specifically to meet very stringent underwater radiated noise limits needed for sensitive acoustic research.

- January 2025: The U.S. Navy issued SBIR 25.1 topic N251-043 for the development of toroidal propellers for torpedo and unmanned underwater vehicle applications, specifically highlighting reduced noise and reduced acoustic signatures compared with conventional propeller geometries.

- January 2025: The U.S. Navy issued SBIR 25.1 topic N251-027 for an acoustically transparent underwater-curing adhesive designed to repair conformal sonar-related structures on submarine platforms without degrading acoustic transmissibility.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.7% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Technology, By Vessel, By Application, By Technology Integration, By End User, and Region |

| By Technology |

|

| By Vessel |

|

| By Application |

|

| By Technology Integration |

|

| By End User |

|

| By Geography |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1.39 billion in 2025 and is projected to reach USD 2.71 billion by 2034.

In 2025, the market value stood at USD 0.51 billion.

The market is expected to exhibit a CAGR of 7.7% during the forecast period.

By technology, the propulsion quieting technologies segment leads the market.

Rising defense budgets and submarine fleet modernization programs are the key factors driving market growth.

Hutchinson Aerospace & Industry / Hutchinson Stop-Choc, Trelleborg Anti-Vibration Solutions, Rubber Design B.V., Socitec Group, and Christie & Grey are some of the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us