Non-Dairy Cheese Market Size, Share & Industry Analysis By Source (Soy, Almond, Cashew, and Others), By Product Type (Mozzarella, Cheddar, Parmesan, and Others), By End-Use (Household and Foodservice), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

KEY MARKET INSIGHTS

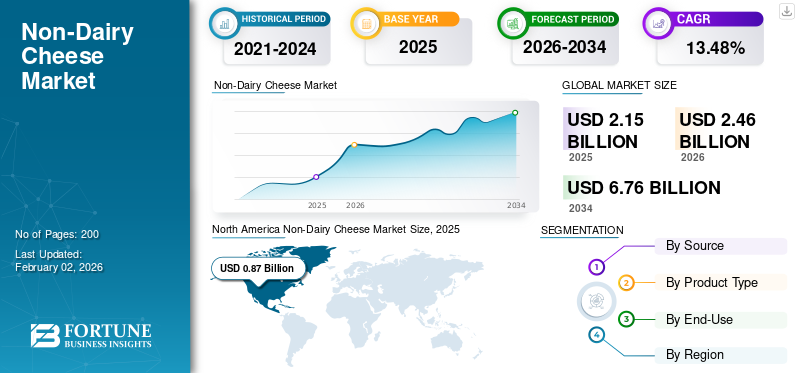

The global non-dairy cheese market size was valued at USD 2.15 billion in 2025 and is projected to grow from USD 2.46 billion in 2026 to USD 6.76 million by 2034, exhibiting a CAGR of 13.48% during the forecast period. North America dominated the non-dairy cheese market with a market share of 40.42% in 2025.

Non-dairy cheese, also known as cheese substitute, vegan cheese, cruelty-free cheese, and plant-based cheese, is depicting huge popularity among individuals. The product is gaining traction as more people are opting for environmentally sustainable cheese, cruelty-free, and imitating the qualities of the original food items. The market is expected to show promising growth with more brands coming up with a variety of non-dairy cheese slices and shreds. Some of the leading players operating in the market are Flora Food Group B.V., Miyoko’s Creamery, Daiya Foods, Bel Brands USA, and KiteHill.

Download Free sample to learn more about this report.

Global Non-Dairy Cheese Industry Key Takeaways

Market Size & Forecast:

- 2025 Market Size: USD 2.15 billion

- 2026 Market Size: USD 2.46 billion

- 2034 Forecast Market Size: USD 6.76 billion

- CAGR: 13.48% from 2026–2034

Market Share:

- North America dominated the non-dairy cheese market with a value of USD 0.87 billion in 2025, supported by the rising adoption of plant-based diets, health awareness, and growing vegan and vegetarian population. Manufacturers in the region are improving taste, texture, and meltability of vegan cheese to attract a wider consumer base.

- By product type, Mozzarella held the largest share in 2024 due to its widespread application in pizzas, pasta, salads, and foodservice menus across global markets.

Key Country Highlights:

- United States: Rising veganism, lactose intolerance awareness, and innovation from major brands such as Oatly and Daiya Foods are fueling growth.

- China: High demand for dairy alternatives supported by lifestyle changes, growing purchasing power, and consumer preference for protein-rich plant-based foods.

- Germany: Leading European market for plant-based cheese, driven by sustainability concerns, mainstream adoption, and retail expansion.

- Brazil: Increasing vegetarian population and strong growth in the plant-based food sector are boosting demand for non-dairy cheese.

- United Arab Emirates: Growing foodservice adoption and introduction of global vegan brands like Violife are accelerating market expansion

MARKET DYNAMICS

MARKET DRIVERS

Rising Incidence of Lactose Intolerance and Ethical Concerns to Drive Market Growth

A significant proportion of the population across the globe is lactose intolerant. Individuals who are lactose intolerant can hardly indulge in milk or milk-based delicacies. According to the National Institutes of Health (NIH), around 68% of the world's population has lactose malabsorption. This factor has been significantly fueling the demand for vegan cheese. Moreover, many hotels, restaurants, and cafés have begun offering vegan cheese on their menu to appeal to those consumers who prefer a vegan diet and those who are lactose intolerant. Furthermore, ethical concerns regarding animal welfare significantly drive the consumer demand for dairy alternatives such as vegan cheese due to widespread issues involving animal treatment in the conventional dairy industry.

MARKET RESTRAINTS

High Price and Lack of Consumer Awareness to Hinder Market Growth

Price is one of the significant factors affecting the growth of the non-dairy cheese industry. Typically, these products are more expensive than their dairy equivalents, which may put off price-sensitive consumers. The high cost is usually due to the involved complicated manufacturing processes and the use of high-end ingredients, including nuts, legumes, and others. Moreover, availability and awareness are other factors limiting the global non-dairy cheese market growth. Consumers might not be familiar with plant-based cheeses in certain areas or they might not be easily available on the shelves of local outlets, hindering market penetration. For instance, in regions such as Southeast Asia or sub-Saharan Africa, awareness and penetration of vegan cheese are likely to be very low. These areas often have limited exposure to Western food trends and may lack the infrastructure or consumer demand for plant-based alternatives such as vegan cheese.

MARKET OPPORTUNITIES

Growing Adoption of Vegan Culinary Innovation in the HoReCa Sector to Offer Opportunities for the Market

The increasing popularity of veganism and vegetarianism among the millennial generation influences the hotel, restaurant, and café industries. This movement has also boosted the global market for plant-based cheese alternatives, leading food industry players to innovate and produce new products and increase spending on research and development. Additionally, improvements in technology have enhanced the taste and texture of non-dairy cheeses, making them more appealing substitutes. The environmental impact of dairy farming and animal welfare concerns also play a significant role in driving the demand for non-dairy cheese.

NON-DAIRY CHEESE MARKET TRENDS

Evolving Consumer Preferences to Fuel Industry Growth

The vegan cheese market is experiencing dynamic changes, spurred by evolving consumer preferences and an increasing need for plant-based products. One of the plant-based food trends is the remarkable expansion of product variety, with producers launching a vast variety of flavors, textures, and formats, including aged and artisanal cheeses. For instance, in January 2025, RIND, a Brooklyn-based brand, launched ALPINE SVVISS, a new cashew-based artisan vegan cheese. The new product is a cholesterol-free, certified Kosher Pareve, and gluten-free non-dairy cheese.

Download Free sample to learn more about this report.

Segmentation Analysis

By Source

Mild Flavor Attributes and High Protein Source to Boost Soy Segment Expansion

Based on source, the market is divided into soy, almond, cashew, and others.

The soy segment dominates the global market. Soy-based cheese is a dairy cheese substitute that serves those with a demand for dairy-free and vegan sources. It is made from soy, a versatile legume with a high content of protein and mild flavor. Soy-based vegan cheese contains high levels of plant-based proteins and presents a healthy alternative to individuals embracing the vegan or vegetarian diet.

The cashew segment will significantly expand, driven by its naturally creamy consistency, mild sweet flavor, and versatility in simulating the range of cheese varieties. This makes it perfect for replicating the flavor and consistency of authentic cheeses such as ricotta, cream cheese, and even cheddar cheese.

By Product Type

Dominance of Plant-based Mozzarella Owing to Widespread Application and Popularity

Based on product type, the market is subdivided into Mozzarella, Cheddar, Parmesan, and others.

The Mozarella segment dominates the global market, due to its widespread use in a broad array of recipes across the household and food services industry in all major economies. Mozzarella is available in various forms, i.e., cube, slice, shreds, and blocks, which find application in recipes such as pasta, lasagne, risotto, pizzas, and salads, in all possible forms.

The plant-based Cheddar cheese is expected to grow significantly over the forecast period, owing to its hard, creamier taste and a longer shelf life. This cheese is widely used in fast food, savory snacks, bakery products, and others. Moreover, the price of cheddar cheese is comparatively lower compared to mozzarella cheese; thereby, fueling its adoption in developing countries, including India and China.

By End-Use Type

Convenience and Availability Influence the Dominance of the Household Segment

Based on end-use, the market is bifurcated into household and foodservice.

The household segment dominates the global non-dairy cheese market share. This is driven by rising household income in all economies, willingness to spend on healthier and premium products for diet, and rising awareness of animal cruelty. Additionally, vegan cheese variants are readily available in convenience stores and supermarkets, which makes purchase options convenient for residential needs. Ready-to-use vegan cheese products provide convenience to home cooks, enabling them to add vegan cheese to numerous dishes, ranging from pizzas and sandwiches to snacks and dips.

The foodservice segment is poised to grow at the highest CAGR over the forecast period. Restaurants and other foodservice businesses are adding vegan cheese to their menus, creating new and different items that will be attractive to a wider customer base. For instance, in May 2024, Daiya Foods, a Canada-based dairy-alternative food company, launched Dairy-Free Cheese Shreds tailored specifically for foodservice operators. Foodservice businesses are recognizing the need to cater to consumers with dietary restrictions, including lactose intolerance and dairy allergies.

Non-Dairy Cheese Market Regional Outlook

By geography, the market is categorised into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Non-Dairy Cheese Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market was valued at USD 0.87 billion in 2025, capturing 40.42% of global revenue, and is estimated to reach USD 0.99 billion in 2026. The increasing demand for plant-based diets and plant-based meat alternatives in the region aids market expansion. Health is a major driver for consumers opting for dairy alternatives. This includes people with dietary restrictions such as lactose intolerance, as well as those who are seeking lower amounts of saturated fat and cholesterol.

Drastic changes in climate and the rising animal welfare concerns among consumers in the region are driving them toward veganism and vegetarianism. According to Canada’s Dietary Guidelines, published in 2019, there is a focus on consuming plant-based foods amongst Canadians. Moreover, the clean eating trend is driving significant change in the clean-label cheese alternatives industry. Manufacturers are actively working to improve the taste, texture, and meltability of vegan cheese, making it more appealing to a wider audience. For instance, in June 2023, Oatly Group AB, one of the largest oatmilk companies, launched a delectable plant-based cream cheese, in the U.S. The new range boasts a rich and creamy texture and is available in Plain and Chive & Onion flavors.

Asia Pacific

The market in Asia Pacific reached USD 0.72 billion in 2025, representing 33.35% of total market revenue, and is projected to reach USD 0.82 billion in 2026. The Asia plant-based cheese market has witnessed tremendous growth in recent years, fueled by various drivers such as the growing trend for vegetarian food, urbanization, health and nutrition awareness, innovation in products, and the clean label trend. China is among the key countries in the region, which is a major consumer of plant-based dairy alternatives, attributable to its popularity amongst consumers as a source of protein. The changing lifestyles of consumers have influenced them to shift toward dairy-free food and beverages. Meanwhile, the increasing purchasing power of individuals has increased due to the overall economic development of the country and has supported the demand for high-quality dairy alternatives, such as cheese. In addition, the outbreak of the COVID-19 pandemic in 2020 raised concerns amongst Chinese individuals about the safety of animal-based proteins, which led to increasing inclination toward plant-based substitutes and positively aided in driving the non-dairy cheese industry.

Europe

In 2025, Europe held 23.62% of the global market, reaching a valuation of USD 0.51 billion, and is projected to grow to USD 0.58 billion in 2026. The trend for global plant-based diets has sparked a transformation in the food sector, with major food manufacturers and retailers embracing the change. In Europe, supermarket sales of vegan cheese have grown steadily in recent years, supported by the development of new products entering the market. These next-generation plant-based dairy alternatives are increasingly competitive with animal-based products in terms of taste, price, and convenience, making them more accessible to a wider range of consumers. The growth of the dairy alternatives industry in the region reflects a deep shift in consumer preference toward health and sustainability, which offers opportunities for innovation and market growth. According to the Good Food Institute, the sales of dairy alternatives grew by 49% between 2020 and 2022 in Europe. Germany is said to dominate plant-based cheese sales in Europe. The increasing consumption of plant-based cheeses is driven by mainstream consumers who are taking on new perspectives about sustainability and animal welfare and seeking to lower the level of meat and dairy in their diets, further boosting the market growth.

South America

Non-dairy cheese is becoming increasingly popular in South America, particularly in Brazil and Argentina. Brazil is the market leader in the South America non-dairy cheese market, driven by factors such as a large population, growing health consciousness, and diverse consumer preferences. The country has been witnessing a rise in the number of individuals becoming vegetarians, which drives the dairy-free cheese demand. According to the Good Food Institute, Brazil's plant-based foods sector reached USD 170 million in 2022, depicting a 42% rise compared to 2021. Additionally, Brazilian consumers are shifting toward a more balanced diet, expanding the new innovative food items market, including non-dairy cheese.

Latin America

Latin America maintained a strong presence in the global market, reaching USD 0.05 billion in 2025, accounting for 2.51% share, and is expected to reach USD 0.06 billion in 2026.

Middle East & Africa

In 2025, the Middle East & Africa market stood at USD 0 billion, representing 0.10% of global demand, and is projected to grow to USD 0 billion in 2026. The region's growing food and beverage industry, along with the consumers' focus toward vegan and sustainable food consumption, is influencing the demand for plant-based flexitarian food products, particularly in the UAE, Saudi Arabia, and other African countries. In addition, consumers are replacing dairy in various Middle Eastern and African cuisines with plant-based options so as to enhance their flavor and texture. Many restaurants, hotels, and other eateries have begun to offer delectable, full-fledged plant-based menus. This culinary trend is poised to change eating habits in the Middle East countries and present the food service sector with enormous development potential. In July 2021, Upfield, a Dutch-based consumer goods firm, introduced its award-winning, 100% vegan and allergen-free cheese brand Violife in the UAE to address this rising demand.

COMPETITIVE LANDSCAPE

Key Industry Players

Foray into Business by Emerging Players to Expand Business

The flourishing global non-dairy cheese industry is influencing producers to expand their business operations. Leading players such as Flora Food Group B.V., Miyoko’s Creamery, Daiya Foods, Bel Brands USA, and KiteHill are investing in R&D, new product launches, and other operations to attain a high market share. Moreover, new players have also been foraying into the industry, achieving a more competitive advantage while concentrating on serving new consumers. For instance, in August 2022, Saputo Inc. made strategic investments in the U.K. and forayed into vegan cheese in the market by launching the Vitalite brand. The global non-dairy cheese market holds tremendous growth opportunities in the forthcoming years, owing to the increasing consumers' shift toward substitutes for processed dairy products, paired with the flourishing popularity of plant-based foods.

LIST OF KEY NON-DAIRY CHEESE COMPANIES PROFILED

- Flora Food Group B.V. (Netherlands)

- Miyoko’s Creamery (U.S.)

- The Paleo Running Momma (U.S.)

- KiteHill (U.S.)

- Daiya Foods (Canada)

- Bel Brands USA (U.S.)

- Epic Cheese (New Zealand)

- Nuts For Cheese (U.K.)

- Bute Island Foods Ltd. (U.K.)

- La Fauxmagerie (U.K.)

KEY INDUSTRY DEVELOPMENTS

- January 2025: Julienne Bruno, a plant-based dairy products company, launched a new non-dairy product, named vegan mozzarella pearls.

- August 2023: Agrocorp International, a global agri-commodity firm, launched Singapore’s first plant-based, nut-free cheese range, under brand name HerbYvore Just Like Cheese. The new range would be sold under its consumer brand, HerbYvore.

- March 2023: PlantWise, a plant-based dairy alternative company, launched a new vegan cheese product. The new product is available in 3 different flavors – classic cheese, garlic, and pepper.

- January 2023: The Laughing Cow, a brand owned by Le Groupe Bel, launched its plant-based spreadable cheese product nationwide. The new product is made using almond milk to create a creamy texture.

- November 2022: CJ CheilJedang, a South Korean international food company, invested in New Culture, a California-based food-technology company that makes dairy-identical vegan cheese. The investment underscores the overwhelming demand for animal-free ingredients across the industry.

REPORT COVERAGE

The global market report provides the market size and forecast on the basis of various segments. It includes details on the market dynamics and global market trends expected to drive the market over the forecast period. It offers information about the key regions/countries, key industry developments, new product launches, and details on partnerships, mergers, and acquisitions. The global market analysis also covers a detailed competitive landscape with information on the market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 13.48% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Source

|

|

By Product Type

|

|

|

By End-Use

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.15 billion in 2025 and is projected to reach USD 6.76 million by 2034.

The market is expected to exhibit a CAGR of 13.48% during the forecast period of 2026-2034.

The household segment is the leading segment in the market by end-use.

The rising incidences of lactose intolerance is a key factor driving market growth.

Flora Food Group B.V., Miyokos Creamery, Daiya Foods, Bel Brands USA, and KiteHill are the top players in the market.

North America dominates the market.

The evolving consumer preferences is a key trend anticipated to influence the global market expansion.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us