Osteoarthritis Therapeutics Market Size, Share & Industry Analysis, By Product Type (NSAIDs, Non-NSAID Analgesics, Corticosteroids, Viscosupplementation, and Others), By Joint Type (Knee, Hip, Foot & Ankle, Hand & Wrist, and Others), By Route of Administration (Oral, Parenteral, and Topical), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies and Drug Stores, and Online Pharmacies), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

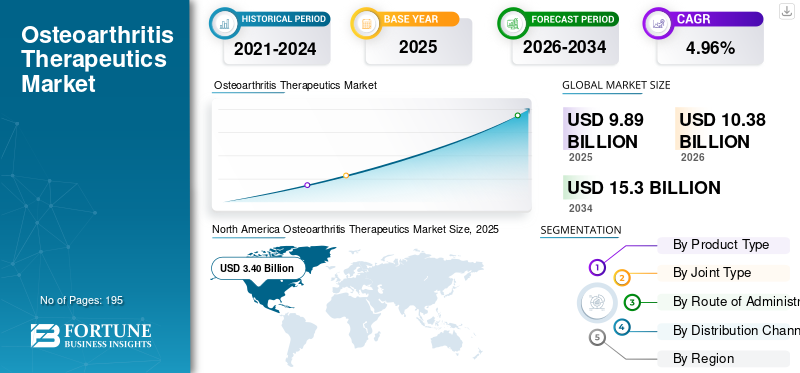

The global osteoarthritis therapeutics market size was valued at USD 9.89 billion in 2025. The market is projected to grow from USD 10.38 billion in 2026 to USD 15.30 billion by 2034, exhibiting a CAGR of 4.96% during the forecast period. North America dominated the global osteoarthritis therapeutics market with a market share of 34.37% in 2025.

The global market is expanding at a considerably robust rate, driven by the rising prevalence of osteoarthritis, aging population, and development of more premium therapies. Osteoarthritis (OA) impacts a considerable number of patients worldwide and the patient volume is projected to increase significantly. The surging awareness of osteoarthritis and a deepening focus on the development of therapies that control the symptoms for a longer duration and the presence of disease-modifying OA drugs (DMOADs) in key players’ drug development pipelines is expected to drive the market growth. Furthermore, the surging prevalence of associated comorbidities such as obesity and efforts for the development of innovative therapies by major companies also augment the market growth prospects.

- For instance, in June 2025, Kolon TissueGene, Inc. (KTG), a clinical-stage biopharmaceutical company demonstrated the considerable progress of its pipeline drug therapy of TG-C, a first-in-class disease-modifying osteoarthritis drug (DMOAD). The therapy has been developed to provide a long acting anti-inflammatory and regenerative impact on the patient and is designed to modulate the patient’s immune responses.

Moreover, several pharmaceutical giants such as Haleon Group of Companies, Sanofi, Pfizer, Inc., and others, are present and operating in the market. These players are focused on the development of innovative therapies, addressing the unmet needs of patients, and emphasizing the expansion of their existing osteoarthritis products.

Download Free sample to learn more about this report.

Osteoarthritis Therapeutics Market Key Takeaways

- 2025 Market Size: USD 9.89 billion

- 2026 Market Size: USD 10.38 billion

- 2034 Forecast Market Size: USD 15.30 billion

- CAGR: 4.96% from 2026-2034

- North America dominated the market with a 34.37% share in 2025.

- Corticosteroids segment is projected to grow at a 5.21% CAGR.

- Foot & ankle segment is expected to grow at a 5.67% CAGR.

North America

North America accounted for USD 3.40 billion in 2025, maintaining the leading regional position in osteoarthritis therapeutics.

Asia Pacific

Asia Pacific reached USD 3.65 billion in 2025, making it the second-largest regional market globally.

Europe

Europe is projected to reach USD 2.37 billion in 2026, supported by steady demand and rising treatment adoption.

U.S.

Estimated at around USD 3.07 billion in 2026, driven by high disease prevalence and advanced healthcare infrastructure.

Japan

Valued at USD 1.09 billion in 2025, supported by aging population and increasing osteoarthritis cases.

Read More

OSTEOARTHRITITS THERAPEUTICS MARKET TRENDS

Increased Transition from Short Acting Injections to Longer Duration Injectables

One of the key trends witnessed in the global market is the advent and growing demand for longer duration injectables in terms of osteoarthritis treatment. Longer duration injectables have several benefits for patients such as the elimination of multiple visits to the physicians for administering multiple courses of injections, better convenience and treatment adherence, and a stronger willingness to try injectables before surgery, leading in improved treatment adoption rates. Furthermore, several players are engaging in this category of the market by developing products such as single hyaluronic acid (HA) injections, extended-release corticosteroids, and injectable hydrogels, among others.

- For instance, in July 2023, the U.S. FDA awarded the designation of Regenerative Medicine Advanced Therapy (RMAT) to GNSC-001. This potential recombinant adeno-associated viral vector gene therapy is being developed by Genascence. Its treatment mechanism includes the blocking of interleukin 1 (IL-1) and is indicated for the knee osteoarthritis disease type.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Aging Population Coupled with Surge in Obesity Rates to Drive Market Growth

One of the most critical drivers for the growth of the global market is the rise in the aging population almost across all the regions in the world, coupled with the increasing rates of obesity. Improvements in various healthcare indicators across the globe has led to the creation of demographics that lives longer, leading to an increase in the prevalence rates of osteoarthritis. Furthermore, the global surge in the rates of obesity has also contributed to an increase in the number of people suffering from osteoarthritis. This has been observed as one of the most common side effects of obesity is that the higher body weight increases the compressive and shear forces across the weight-bearing joints (especially knees), accelerating cartilage breakdown and pain.

- For instance, in December 2025, Eli Lilly and Company announced the positive topline results from the Phase 3 TRIUMPH-4 clinical trial that evaluated the efficacy and safety of the two highest investigational retatrutide doses, a first-in-class GIP, GLP-1 and glucagon triple hormone receptor agonist in adult patients suffering from knee osteoarthritis and obesity or overweight and without diabetes, as an adjunct to physical activity and healthy diet.

MARKET RESTRAINTS

Side Effects Associated with Key Therapies and Reimbursement Concerns May Impact Market Growth

One of the key factors hindering the greater adoption of these therapies includes the concerns related to the potentially adverse impact of the usage of these therapies for a longer duration. Some of the common side effects associated with these therapies include gastrointestinal/renal and cardiovascular risks. Moreover, there have been several concerns in terms of adequate reimbursement or insurance coverage for major therapies such as viscosupplementation therapies. These factors are likely to collectively hinder the growth of the market.

- For example, in September 2025, Blue Cross and Blue Shield of Texas announced that the benefit coverage of viscosupplementation therapies for the treatment of osteoarthritis will be discontinued with effect from 1st January, 2026. Such developments further restrict the market growth as they limit the number of patients adopting these therapies.

MARKET OPPORTUNITIES

Development of Innovative, Premium Therapies for Long Lasting Treatment of Osteoarthritis to Provide Lucrative Growth Opportunities

The most important opportunities for the global osteoarthritis therapeutics market growth lies in the development of cutting edge therapies that significantly improves the patient treatment outcomes by guaranteeing benefits such as long lasting treatment effects. Major established and emerging companies are focusing on the development of therapies such as single injection therapies, disease-modifying OA therapies (DMOADs), and regenerative medicine, among others. There are several advantages in terms of development of these therapies as it ensures that these companies can command premium prices owing to ability to demonstrate lasting improvement in osteoarthritis patients.

- For instance, in April 2025, Contura International Ltd., presented 10-Year Data on the safety profile and 5-Year Data on the long term efficacy of its product Arthrosamid. Arthrosamid is an example of a long acting injectable, often providing relief up to 12 months.

MARKET CHALLENGES

Clinical Trial Failures and Issues Present a Critical Challenge to Market Growth

Some of the significant challenges associated with the market is the fact that proving an osteoarthritis drug actually treats or modifies the disease is extremely hard to demonstrate. This is as the progression of osteoarthritis is slow and heterogeneous and often therapies that have a positive impact on cartilage biology may not create a favorable impact on the regulators and payers as it often cannot lead to a fast and clean signal in terms of actual treatment improvement. Further, it has been noted that several clinical trials centered on osteoarthritis have high placebo response rates, especially at the endpoint of pain management. Such challenges may create an obstacle to a more positive market growth rate.

- For instance, in April 2025, Novartis AG announced the termination of a Phase 2 clinical trial that was evaluating an investigational ADAMTS-5 inhibitor for patients with osteoarthritis knee pain after an initial assessment concluded that the investigational drug had an inadequate impact on pain relief.

Segmentation Analysis

By Product Type

Robust Demand for Viscosupplementation Therapies to Propel Segmental Growth

Based on product type, the market is segmented into NSAIDs, non-NSAID analgesics, corticosteroids, viscosupplementation, and others.

In terms of product type, the viscosupplementation segment is anticipated to account for the largest osteoarthritis therapeutics market share. The high segmental share is primarily attributed to the strong utilization rate of viscosupplementation therapies in the osteoarthritis patients. In addition, clinicians and patients continue to look for local intra-articular options, keeping viscosupplementation relevant even when guidelines vary. Furthermore, practical guidance and responder targeting are improving, which supports appropriate use and durability of the product type.

- For instance, 2025 EUROVISCO good-practice recommendations and 2025 evidence discussions about HA’s association with delayed arthroplasty strengthen the clinical positioning narrative.

The corticosteroids segment is anticipated to rise with a CAGR of 5.21% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Joint Type

High Treatment Pathway for Knee Osteoarthritis to Boost Knee Segmental Dominance

Based on joint type, the market is segmented into knee, hip, foot & ankle, hand & wrist, and others.

In 2025, the knee segment dominated the global market. This dominance of the segment was due to the fact that the knee is a primary weight-bearing joint. Hence, everyday loading creates high cumulative mechanical stress resulting in higher incidence and earlier symptom onset than many other joints. Additionally, clinically, knee OA has the largest treatable pathway before surgery in turn driving higher utilization across drug and injection classes.

- For instance, according to the Global Burden of Disease (GBD) study, around 374.7 million prevalent knee OA cases were diagnosed globally in 2021.

The foot & ankle segment is projected to grow at a CAGR of 5.67% over the forecast period.

By Route of Administration

Parenteral Segment to Lead the Market Due to Rising Deployment with Persistent Pain

Based on the route of administration, the market is segmented into oral, parenteral, and topical.

The parenteral segment is anticipated to dominate the market over the forecast period. This is as many patients progress from OTC/Rx oral/topical options to clinic-administered injections when pain persists. Additionally, technological advancements such as single-injection/long-acting intra-articular products further boost the segment growth.

- For instance, in October 2025, Doron Therapeutics announced the first patients dosed in a Phase 3 trial of MOTYS (PTP-001), a single intra-articular knee injection for OA.

The topical segment is projected to grow at a CAGR of 4.89% over the forecast period.

By Distribution Channel

High Consumer Preference for Retail Pharmacies and Drug Stores Kept Them in a Leading Position

By distribution channel, the market is fragmented into retail pharmacies and drug stores, hospital pharmacies, and online pharmacies.

The retail pharmacies and drug stores segment dominated the global osteoarthritis therapeutics market share in 2025. This high market share was driven by repeat purchases through these settings, ease of product distribution, and the easy availability of product through these networks. Furthermore, the segment is set to hold 57.9% share in 2026.

- For instance, Walmart and Amazon pharmacy are some of the retail pharmacies operating in the U.S. market.

The online pharmacies segment is projected to grow at a CAGR of 6.19% during the study period.

Osteoarthritis Therapeutics Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Osteoarthritis Therapeutics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valuing at USD 3.25 billion, and also maintained the leading share in 2025, with USD 3.40 billion. The market in North America is projected to expand considerably during the forecast period owing to the significant prevalence of osteoarthritis in the region coupled with the presence of major players developing innovative therapies. These factors, in conjunction with an advanced healthcare infrastructure and active environment for research and development initiatives, followed by clinical trials, are estimated to contribute to the market growth in the region.

U.S. Osteoarthritis Therapeutics Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market value can be analytically approximated at around USD 3.07 billion in 2026, accounting for roughly 29.6% of the global sales.

Europe

The Europe market is on track to record a growth rate of 4.31% over the analysis period, which is the third highest among all regions, and reach a valuation of USD 2.37 billion by 2026. Some of the factors contributing to the region’s strong market share include the presence of robust treatment guidelines, adequate reimbursement coverage, and increasing scale up of digital health initiatives for osteoarthritis patients including telehealth measures.

U.K. Osteoarthritis Therapeutics Market

In 2025, the U.K. market reached around USD 0.33 billion, representing roughly 3.2% of global revenues.

Germany Osteoarthritis Therapeutics Market

The Germany market reached approximately USD 0.41 billion in 2025, equivalent to around 3.9% of global sales.

Asia Pacific

Asia Pacific market touched a value of USD 3.65 billion in 2025 and secured the position of the second-largest region in the market.

Japan Osteoarthritis Therapeutics Market

The Japan market, in 2025, is estimated at around USD 1.09 billion, accounting for roughly 10.5% of global osteoarthritis therapeutics revenues. Japan has a considerable share in the global market owing to the country’s significant volume of aging persons and the adoption of advanced therapies such as regenerative medicine.

China Osteoarthritis Therapeutics Market

The China market is projected to be one of the largest worldwide. In 2025, the country’s market revenue reached around USD 1.00 billion, representing roughly 9.6% of global sales.

India Osteoarthritis Therapeutics Market

In 2025, the India market touched a value of around USD 0.37 billion, accounting for roughly 3.6% of global revenues.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The Latin America market reached a valuation of USD 0.44 billion in 2025. Large patient population, rising investment trends, and an increasingly competitive private sector are poised to drive the market growth in these regions. In the Middle East & Africa, the GCC touched a value of USD 0.13 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Players Place Emphasis on Development of Innovative Therapies and Expansion of Existing Product Portfolio to Enhance Market Share

The global osteoarthritis therapeutics market comprises a semi-consolidated competitive market structure, constituting prominent players such as Bayer, Kenvue, Reckitt, and Sanofi. The considerable market revenue share accounted by these companies is due to numerous strategic activities, including collaborations among operating entities to advance research activities through various ongoing clinical trials.

- For instance, in April 2025, Sun Pharmaceutical Industries and Moebius Medical announced dual peer-reviewed publications on MM-II’s Phase 2b knee osteoarthritis results and stated that new data would be presented at the OARSI 2025 World Conference.

Other notable players in the global market include Anika Therapeutics, Ferring, Zimmer Biomet and others. These companies are expected to prioritize new product launches and collaborations to increase their global market share during the forecast period.

LIST OF KEY OSTEOARTHRITITS THERAPEUTICS COMPANIES PROFILED

- Haleon Group of Companies (U.K.)

- Sanofi (France)

- Pfizer, Inc. (U.S.)

- Bayer AG (U.S.)

- Kenvue (U.S.)

- Reckitt (U.K.)

- Ferring (Switzerland)

- Bioventus (U.S.)

- Anika Therapeutics, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Pacira joined the PROBE Consortium (IHI-funded public–private initiative) aimed at improving OA research endpoints, real-world data integration, and trial design

- November 2025: UnicoCell announced the completion of patient enrollment in a Phase III trial of ELIXCYTE (allogeneic adipose-derived MSC investigational therapy) for knee OA.

- July 2025: Pacira announced a strategic collaboration with Johnson & Johnson MedTech to significantly expand promotional efforts for ZILRETTA.

- May 2025: Pacira announced that it would present 3-year data following a single intra-articular injection of PCRX-201 for moderate-to-severe knee OA.

- April 2025: Pacira announced the first patient dosed in a Phase 2 study of PCRX-201, a locally administered gene-therapy approach designed to increase intra-articular IL-1Ra production for knee OA.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2019-2024 |

|

Growth Rate |

CAGR of 4.96% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type, Joint Type, Route of Administration, Distribution Channel, and Region |

|

By Product Type |

· NSAIDs · Non-NSAID Analgesics · Corticosteroids · Viscosupplementation · Others |

|

By Joint Type |

· Knee · Hip · Foot & Ankle · Hand & Wrist · Others |

|

By Route of Administration |

· Oral · Parenteral · Topical |

|

By Distribution Channel |

· Hospital Pharmacies · Retail Pharmacies and Drug Stores · Online Pharmacies |

|

By Region |

· North America (By Product Type, Joint Type, Route of Administration, Distribution Channel, and Country) o U.S. o Canada · Europe (By Product Type, Joint Type, Route of Administration, Distribution Channel, and Country/Sub-Region) o Germany o U.K. o France o Spain o Italy o Scandinavia o Rest of Europe · Asia Pacific (By Product Type, Joint Type, Route of Administration, Distribution Channel, and Country/Sub-Region) o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific · Latin America (By Product Type, Joint Type, Route of Administration, Distribution Channel, and Country/Sub-Region) o Brazil o Mexico o Rest of Latin America · Middle East & Africa (By Product Type, Joint Type, Route of Administration, Distribution Channel, and Country/Sub-Region) o GCC o South Africa o Rest of Middle East & Africa |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 9.89 billion in 2025 and is projected to reach USD 15.30 billion by 2034.

In 2025, the North America market value stood at USD 3.40 billion.

The market is expected to exhibit a CAGR of 4.96% during the forecast period of 2026-2034.

By product type, the viscosupplementation segment is expected to lead the market.

The increasing prevalence of osteoarthritis and development of advanced therapies are key factors driving market expansion.

Bayer AG, Kenvue, and Reckitt are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 195

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us