Packaging Printing Market Size, Share & Industry Analysis, By Printing Process (Flexography Printing, Offset Printing, Digital Printing, Lithography Printing, Gravure Printing, and Others), By Packaging Type (Boxes & Cartons, Labels & Tags, Bags & Pouches, and Others), By End-use Industry (Food & Beverages, Personal Care & Cosmetics, Pharmaceuticals, Consumer Goods, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

KEY MARKET INSIGHTS

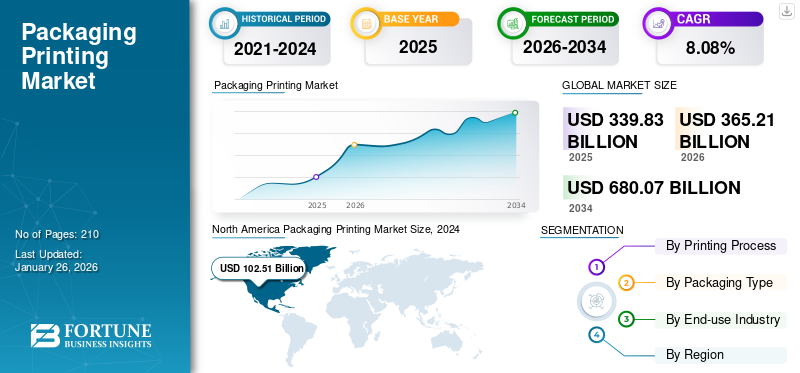

The global packaging printing market size was valued at USD 339.83 billion in 2025 and is projected to be worth USD 365.21 billion in 2026 and record a valuation of USD 680.07 billion by 2034, exhibiting a CAGR of 8.08% during the forecast period. North America dominated the packaging printing market with a market share of 32.57% in 2025. Moreover, the packaging printing market in the U.S. is expected to witness strong expansion, reaching USD 161.88 billion by 2032. The increasing focus on branding, product differentiation, and sustainable printing technologies is fueling market demand.

Packaging printing refers to the packaging of a product printed according to the requirement of the brand and the enclosed product. The print is designed by various printing processes that communicate and attract value to customers in a market or on an e-commerce platform. The growing demand for printed cartons and labels will drive the global packaging printing market share. The increasing demand for advanced printing processes for product packaging is boosting the global printing packaging market growth.

The advent of the COVID-19 pandemic disrupted the supply chain of several industries worldwide. However, there was a surge in growth of the shipping & logistics, e-commerce, and food & beverage industries. It thus, led to increased sales of food, beverages, pharmaceuticals, and consumer goods products, enhancing market growth.

Download Free sample to learn more about this report.

Packaging Printing Market Key Takeaways

- 2025 Market Size: USD 339.83 billion

- 2026 Market Size: USD 365.21 billion

- 2034 Forecast Market Size: USD 680.07 billion

- CAGR: 8.08% from 2026-2034

- North America dominated the packaging printing market with a 32.57% share in 2025.

- The Flexography Printing segment accounted for a 32.50% share in 2026.

- The Boxes & Cartons segment accounted for a 44.33% share in 2026.

North America

North America accounted for USD 110.69 billion in 2025 and is projected to reach USD 119.60 billion in 2026.

Asia Pacific

Asia Pacific represented USD 88.98 billion in 2025 and is projected to grow to USD 97.05 billion in 2026.

Europe

Europe recorded USD 66.32 billion in 2025 and is expected to reach USD 70.96 billion in 2026.

U.S.

Strong demand for sustainable and e-commerce packaging is supporting market growth.

Japan

Advanced printing technologies and premium packaging demand are driving market expansion.

Read More

Packaging Printing Market Trends

Increase in Demand for Digital and 3D Printing Technique Emerges as a Market Trend

There is an upsurge in demand for digital and 3D printing processes worldwide. Digital printing technology offers high-quality print for corrugated boxes, labels, folding cartons, flexible packaging, and many other products. The printing process also provides versatility, fast turnaround times, variable data printing for customized and engaging packaging design, and is cost-effective for small runs. It also minimizes waste and emissions, aligning with the brand’s sustainability goals through efficient and small-batch production. In addition, there is a growing demand for 3D printing techniques in the food industry. 3D-printed food packaging boosts the enhanced creativity for package design & brand individuality and also allows for further technological innovation. Several packaging companies utilize 3D printing to produce prototypes, allowing customers to understand how their product will appear on the shelf when the packaging is produced & filled. The rising demand for digital and 3D printing techniques thus emerges as a key market trend and boosts market growth. North America witnessed a packaging printing market growth from USD 95.16 billion in 2023 to USD 102.51 billion in 2024.

Download Free sample to learn more about this report.

Packaging Printing Market Growth Factors

Potential Benefits Offered by Flexographic Printing Drives Market Growth

Due to its significant benefits, there is an astonishing demand for flexographic printing for product packaging. The printing consistently offers high-print quality across a vast range of substrates without the requirement of special coatings, as it decreases the overall cost per unit. It is also the cheapest option for large run orders, owing to the speed of its machines, and it can match the desired colors. Flexographic printing mainly uses flexible packaging solutions such as standup pouches, bags, labels, and other packaging products, such as corrugated boxes and cartons.

Additionally, the process can print millions of impressions and cater to a wide range of cylinder repeat lengths to fulfill the customer's specifications. It is also more cost-effective than other techniques and provides faster production, due to its high-speed process and flexographic inks. Such noteworthy benefits of flexographic printing boost demand in various end-use industries and drive market growth.

Remarkable Growth in the Food & Beverage Industry Propels Market Growth

The packaging printing industry has experienced significant growth in recent years. The exponential growth of the food & beverage sector is analyzed as a key contributor to its rapid development. Printing on food packaging develops a distinctive & memorable brand identity, allowing the brand to stand out from its customers and boost its customer base and loyalty. The initial first impression of the customers through printed packages has also boosted brand recognition, trust, and lucrative growth opportunities.

There has also been a rise in demand for on-the-go, frozen, chilled, and snack food products globally. This demand is contributing to the growth of the food & beverage industry and further leading to a massive rise in the need for attractive and customizable printing options. Henceforth, the growing food & beverage sector is analyzed as a prime contributor to enhancing the demand and driving the global packaging printing market growth.

RESTRAINING FACTORS

High Upfront Costs Associated with Printing Processes & Stringent Regulations Restrain Market Growth

Despite the astonishing demand for printed packaging solutions, some factors limit the market growth. The establishment of printing facilities requires high capital investment. The majorly utilized printing processes, such as flexography, rotogravure, offset, lithography, and others, require a large amount of capital investment in setup and equipment and other raw materials such as paper, printing inks, and energy supply. The high capital investment limits the short businesses from opting for printing facilities, further hampering the market growth. In addition, various regulations ensure that the printing processes are carried out with a low environmental impact. The regulations are also critical to ensure that the chemicals used in printing do not negatively impact and eliminate carbon footprint. Henceforth, the high upfront costs and the stringent regulations hamper market growth for packaging printing.

Packaging Printing Market Segmentation Analysis

By Printing Process Analysis

Significant Benefits Offered by Flexography Printing Boosts Segmental Growth

Based on the printing process, the market is segmented into flexography printing, offset printing, digital printing, lithography printing, gravure printing, and others.

The Flexography Printing segment led the market accounting for 32.50% market share in 2026. Flexography printing is the dominating printing process segment, accounting for the largest market share. Flexography printing offers productivity, cost-effectiveness, sustainability, and higher-consistent quality to various packaging solutions, such as labels and tags, flexible packaging, carton board, corrugated board, plastic bags, shrink-wrap, and many others. The flexography printing process is more cost-effective than other competing methods, leading to faster production, owing to its high-speed process and flexographic inks. Moreover, the process is very versatile, thus increasing its usage on a wide range of substrates, such as plastic, paper, and even metallic films.

Digital printing is the second-dominating printing process. Digital printing offers more precise and vibrant colors, excellent quality, consistency, and faster production times, further boosting its utilization in the packaging industry. The food and beverages segment is expected to hold a 51.74% share in 2024.

By Packaging Type Analysis

High Demand for Printed Boxes & Cartons Among Several End-use Industries Drives Segmental Growth

Based on packaging type, the market is segmented into boxes & cartons, labels & tags, bags & pouches, and others.

The Boxes & cartons segment led the market accounting for 44.33% market share in 2026. The segment’s growth is attributed to increased brand protection and awareness, cost-effectiveness, customer experience, and elevated design flexibility. Printing on boxes & cartons expands brand awareness and protection without spending additional money, thus boosting its demand from multiple end-use industries. Moreover, printed cartons & boxes have enabled the brands to communicate better and connect with customers, thus boosting segmental growth.

Labels and tags are the second-dominating packaging type segment. Labels allow the brand owners to demonstrate their brand and communicate their distinct brand identity, further aiding segmental growth.

By End-use Industry Analysis

To know how our report can help streamline your business, Speak to Analyst

Rising Demand for Printed Packaging Among Food & Beverage Sectors Aids Segment’s Growth

Based on the end-use industry, the market is segmented into food & beverages, personal care & cosmetics, pharmaceuticals, consumer goods, and others.

Food & beverages are the dominating end-use industry segment. The printed boxes & cartons offer several advantages to the food & beverages industry. The cost-effectiveness, quicker turnaround times, and high-quality features of the printed cartons boost its utilization in food packaging solutions. Moreover, printing on boxes, cartons, or labels is an important way to notify the consumer regarding all the necessary information about the product and its usage. Henceforth, the rising demand for printed packaging among the food & beverage industries will boost the segment’s growth.

Consumer goods is the second-dominating end-use industry segment. The rising demand for attractive and consumer-friendly packaging solutions will drive the segment’s growth. The Food and Beverages segment is expected to hold a 52.36% share in 2026.

REGIONAL INSIGHTS

The market for packaging printing is analyzed across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America Packaging Printing Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

The North America market accounted for USD 110.69 billion in 2025, representing 32.57% of the global industry, and is expected to reach USD 119.6 billion in 2026. The presence of major packaging and printing manufacturers is a key factor enhancing the market growth in the region. In addition, the massive demand for bags & pouches, labels, and corrugated boxes amongst the region’s well-established food, beverage, and consumer goods sectors also drives the market growth.

Asia Pacific

In 2025, Asia Pacific represented USD 88.98 billion, accounting for 26.18% of the worldwide market, and is projected to grow to USD 97.05 billion in 2026. Asia Pacific is the second-dominating region and is analyzed to foresee significant development in the upcoming years. The rise in the demand from pharmaceutical and consumer goods sectors in the region for printed packaging solutions to provide accurate product information, such as nutritional information, ingredients, and instructions for use, cushions the market growth.

Europe

Europe recorded a market size of USD 66.32 billion in 2025, capturing 19.52% of the global market share, and is projected to reach USD 70.96 billion in 2026. The growth can be attributed to the region's ongoing sustainability and eco-friendly packaging trend, which boosts the demand for direct printing on packaging materials/substrates, such as corrugated boxes & cartons.

Latin America

The Latin America market was valued at USD 43.22 billion in 2025, capturing 12.72% of global revenue, and is estimated to reach USD 45.52 billion in 2026. The Latin American market for packaging printing will witness steady growth due to the growing demand for printed packaging solutions in the food and pharmaceutical industries in the region.

Middle East & Africa

Middle East & Africa contributed 9.01% to the global market in 2025, with a valuation of USD 30.62 billion, and is projected to reach USD 32.08 billion in 2026. The Middle East & African market is projected to experience moderate growth owing to the rising utilization of printing packages, such as labels, corrugated cartons, and pouches, in the region's consumer goods and personal care sectors.

KEY INDUSTRY PLAYERS

Key Market Participants to Witness Significant Growth Opportunities with New Product Launches

The global packaging printing market is highly fragmented and competitive. A few significant players are dominating the market by offering innovative packaging solutions in the packaging industry. These major market players constantly focus on expanding their customer base across regions by innovating their existing product range. The market report also highlights the key developments by the manufacturers.

Major players in the industry include Amcor Plc, Stora Enso Oyj, CCL Industries Inc., Constantia Flexibles, Smurfit Kappa, Huhtamaki Oyj, and others. Numerous other companies operating in the market are focused on market scenarios and delivering advanced packaging solutions.

List of Top Packaging Printing Companies:

- Amcor Plc (Switzerland)

- Stora Enso Oyj (Finland)

- CCL Industries Inc. (Canada)

- Constantia Flexibles (Austria)

- Smurfit Kappa (Ireland)

- Huhtamaki Oyj (Finland)

- WestRock (U.S.)

- Mondi (U.K.)

- International Paper Company (U.S.)

- Sonoco Products Company (U.S.)

- Sealed Air (U.S.)

- Tetra Pak (Switzerland)

- DS Smith (U.K.)

- Rengo Co., Ltd. (Japan)

- American Packaging Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- September 2023 – A leading global paper-based carton packaging manufacturer, Tetra Pak, and owner of North America’s biggest carton water brand, Flow Beverage, collaborated with Live Nation Canada. Tetra Pak launched new carton designs, which highlight Tetra Pak Custom Printing. It is the "first & only" ink jet-based & premium carton package printing solution to provide brands with innovative, customizable, and cost-effective systems.

- April 2023 – SIG announced the launch of SIG Digital Printing, specifically for its aseptic carton packs manufactured in Europe. The printing solution provides full-color digital printing without requiring cylinders and printing forms for additional agility and flexibility, intending to fulfill the growing customer demands. The investment also complements the company’s existing rotogravure printing.

- March 2022 – Mondi, a leading global company in packaging and paper, divulged an advanced printing line in its Gronau, Germany plant. The advanced equipment will facilitate the hygiene industry’s augmenting demand for advanced printing options for laminates and films and provide excellent flexibility in feminine care film choices and pouch wrapping designs.

- April 2021 – Amcor declared the launch of a strategic investment in ePac Flexible Packaging, a global leader in the high-quality and short-run length digital printing company for flexible packaging. The investment will range between USD 10 - USD 15 million and comprise a minority ownership interest in ePac Holdings LLC.

- March 2021 – Sealed Air introduced a portfolio of solutions for design services, digital printing, and connected packaging, Prismiq, that focuses on the food supply chain. The digital printing services provide easy updates and multiple designs per run to print a personalized message on the packaged products.

REPORT COVERAGE

The market research report provides detailed market analysis and focuses on key aspects, such as top key players, competitive landscape, product/service types, market segments, Porter’s five forces analysis, and leading segments of the product. Besides, it offers insights into the market trends and highlights key industry developments. In addition to the abovementioned factors, it encompasses several factors that have contributed to the market intelligence & growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.08% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Printing Process

|

|

By Packaging Type

|

|

|

By End-use Industry

|

|

|

By Region

|

Frequently Asked Questions

The Fortune Business Insights study shows that the global market size was valued at USD 339.83 billion in 2025.

The market is projected to record a CAGR of 8.08% during the forecast period.

The market size of North America was valued at USD 110.69 billion in 2025.

Based on end-use industry, the food & beverage industry is the dominating segment with the largest market share.

The global market value is expected to record a valuation of USD 680.07 billion by 2034.

The key market drivers are the potential benefits of flexographic printing and the remarkable growth in the food & beverage industry.

The top players in the market are Amcor Plc, Stora Enso Oyj, CCL Industries Inc., Constantia Flexibles, Smurfit Kappa, Huhtamaki Oyj, and others.

- 2021-2034

- 2025

- 2021-2024

- 210

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us