PEM Electrolyzer Materials Market Size, Share & Industry Analysis, By Material Type (Bipolar Plate, Catalysts, Porous Transport Layers, Membranes, and Others), By End Use (Ammonia Production, Refining, Chemical Production, Steel Production, Mobility, Power Generation & Energy Storage, and Others), and Regional Forecast, 2026-2034

PEM Electrolyzer Market Overview

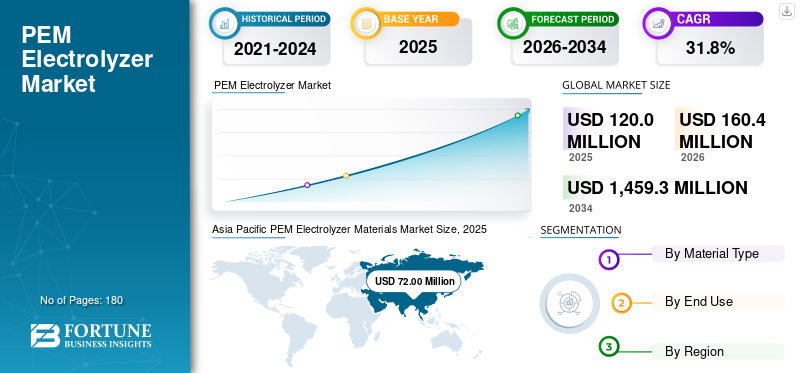

The PEM electrolyzer materials market size was valued at USD 120.0 million in 2025. The market is projected to grow from USD 160.4 million in 2026 to USD 1,459.3 million by 2034, exhibiting a CAGR of 31.8% during the forecast period. Asia Pacific dominated the PEM electrolyzer materials market with a market share of 60% in 2025.

PEM electrolyzer materials are highly specialized inputs used in the manufacturing of proton exchange membrane water electrolyzer systems, where each material plays a critical role in enabling electrochemical hydrogen production under demanding operating conditions. These materials include proton exchange membranes, iridium and platinum-based catalysts, porous transport layers, bipolar plates, gas diffusion layers, sealing materials, and other balance-of-stack components. These together determine electrolyzer efficiency, durability, current density, and system cost.

The rising global focus on green hydrogen production, industrial decarbonization, renewable power integration, and energy security is driving the market growth. Green hydrogen generation projects linked to ammonia, refining, methanol, steel, grid balancing, and long-duration energy storage increasingly require PEM electrolyzers due to their fast response times, compact system designs, and suitability for coupling with intermittent renewable electricity. As a result, market growth is increasingly supported by the shift toward higher-performance, lower-cost materials solutions rather than electrolyzer capacity expansion alone.

The global market is shaped by a relatively concentrated group of specialized material suppliers with strong capabilities in catalyst development, membrane chemistry, advanced coatings, titanium processing, and precision component engineering. Key players include Chemours, W. L. Gore & Associates, Johnson Matthey, Heraeus Precious Metals, Umicore, Bekaert, and Toray Industries. Continuous investments in enhancing electrolyzer technologies, such as developing low-iridium catalyst technologies, titanium porous transport-layer optimization, corrosion-resistant coatings, precious-metal recovery, and other membrane technological advancements to strengthen competitive positioning in the evolving electrolyzer materials ecosystem.

Download Free sample to learn more about this report.

PEM ELECTROLYZER MATERIALS MARKET TRENDS

Low-Iridium Catalyst Development and Material Efficiency Improvements is a Key Market Trend

The market is increasingly shifting toward the development of low-iridium catalysts and broader material-efficiency improvements. Since PEM electrolyzers rely on iridium-based catalyst systems for strong performance in acidic environments, the limited availability and high cost of iridium have pushed manufacturers to lower catalyst loading while maintaining electrochemical efficiency and durability. Similarly, ongoing improvements in membrane chemistry, catalyst-coated components, porous transport layers, and coating technologies are helping optimize material utilization across the stack. As PEM electrolyzer projects move toward larger commercial deployment, these material advancements are becoming more important for improving supply security and project economics. Additionally, as commercial-scale green hydrogen deployment increasingly requires lower stack costs, higher electrochemical efficiency, and stronger long-term project economics, these developments are accelerating the adoption of PEM electrolyzer materials that enable lower precious-metal intensity, better performance, and improved durability.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Green Hydrogen Project Pipeline and Electrolyzer Installations Drives Market Growth

The rising pipeline of green hydrogen projects and increasing electrolyzer installations are driving demand for PEM electrolyzer materials by expanding the need for specialized stack components across both pilot-scale and commercial-scale deployments. Government incentives are pushing market players to accelerate the investments in green hydrogen to support decarbonization across industries such as refining, ammonia, methanol, steelmaking, mobility, and the energy sector. PEM electrolyzers are gaining strong traction in these projects due to their compact footprint, higher operational flexibility, and faster response to variable renewable electricity compared with some alternative technologies. As installed PEM electrolyzer capacity increases, demand is rising for proton exchange membranes, iridium- and platinum-based catalysts, titanium porous transport layers, bipolar plates, and advanced sealing materials. Therefore, the growing number of announced, funded, and commissioned hydrogen production projects, along with in-line capacity expansion plans for PEM electrolyzers, is set to drive the PEM electrolyzer materials market growth during the forecast period.

- IEA analysis indicates that announced electrolyzer capacity could reach nearly 520 GW by 2030, underscoring the substantial long-term expansion potential for critical PEM electrolyzer materials, such as membranes, catalysts, and porous transport layers.

MARKET RESTRAINTS

Limited Availability and High Cost of Critical Raw Materials Constrains Market Expansion

Limited availability and high cost of critical raw materials are constraining the growth of the market, particularly as large-scale hydrogen deployment increases pressure on specialized supply chains. PEM electrolyzer stacks depend on scarce and high-value inputs such as iridium, platinum, and titanium, all of which play essential roles in catalyst systems and corrosion-resistant structural components. Among these, iridium remains one of the most significant bottlenecks due to its extremely limited global production base and high price volatility. This creates a major challenge for scaling PEM electrolyzer manufacturing economically, especially when developers aim to lower hydrogen production costs for wider industrial processes. In addition, concentrated sourcing, long qualification cycles, and limited availability of processed, high-purity materials can further increase procurement risk, delay projects, and limit the pace of global electrolyzer capacity expansion.

MARKET OPPORTUNITIES

Advancements in Catalyst Loading Reduction and Material Innovation Creates New Growth Opportunities

Advancements in catalyst loading reduction and broader material innovation are creating strong growth opportunities in the market by improving cost competitiveness and enabling wider commercialization of the technology. Reducing the amount of iridium and platinum required per stack is becoming a major area of innovation, as it directly lowers material cost and reduces exposure to critical mineral constraints. Similarly, ongoing developments in membrane chemistry, catalyst-coated membranes, corrosion-resistant coatings, porous transport layers, and alternative support materials are opening new pathways to improve efficiency and durability while reducing total system cost. These innovations are significant as PEM electrolyzers move from demonstration-scale projects to multi-megawatt and gigawatt-scale deployment. Therefore, companies that can commercialize advanced materials solutions with lower precious metal intensity and better long-term performance are likely to gain significant market opportunities.

Segmentation Analysis

By Material Type

Bipolar Plates Dominate the Market Owing to Their Critical Role in Stack Architecture, Conductivity, and Flow Management

Based on material type, the market is segmented into bipolar plates, catalysts, porous transport layers, membranes, and others.

Bipolar plates account for the largest PEM electrolyzer materials market share due to their essential role in stack assembly, current conduction, gas-water flow distribution, and mechanical support. These components are indispensable for ensuring electrical connectivity between cells while also helping manage thermal balance and operational stability across the electrolyzer stack. Their material intensity and high value contribution per system further strengthen segment dominance. Therefore, their structural and electrochemical importance continues to secure this segment's leading market position.

Catalysts are among the most strategically crucial segments in the market as they directly influence hydrogen evolution efficiency, reaction kinetics and overall stack performance. The segment is strongly supported by platinum- and iridium-based catalyst systems, which remain essential for acidic PEM operating conditions. Although catalyst loading reduction is a major industry priority, commercial deployment growth continues to sustain material demand. Therefore, the catalysts segment is projected to expand at a CAGR of 32.3% from 2026 to 2034, supported by accelerating electrolyzer installations and continued material innovation.

Membranes remain a foundational component in PEM electrolyzers, enabling proton conductivity while separating product gases and maintaining safe cell operation. Their performance directly affects system efficiency, durability, and operating reliability, making membrane quality a key differentiator in stack design. Demand is rising as manufacturers pursue higher conductivity, better chemical stability, and longer operational life in both pilot-scale and commercial-scale installations. Therefore, the membranes segment is anticipated to register a CAGR of 31.7% from 2026 to 2034, driven by growing demand for high-performance electrolyzer systems.

By End Use

Ammonia Production Leads Market as Green Hydrogen Integration Accelerates in Chemical Feedstock Applications

Based on end use, the market is segmented into ammonia production, refining, chemical production, steel production, mobility, power generation & energy storage, and others.

To know how our report can help streamline your business, Speak to Analyst

Ammonia production accounted for the market share in 2025, driven by rising integration of green hydrogen into fertilizer and chemical value chains. Ammonia remains one of the most established large-volume hydrogen consumption sectors globally, making it a key early demand center for low-carbon hydrogen production. As decarbonization pressures intensify, producers are increasingly evaluating electrolytic hydrogen as a substitute for fossil fuel-derived hydrogen in ammonia synthesis. Furthermore, the industrial scale of ammonia production creates strong long-term potential for large electrolyzer installations, helping this segment maintain its leading position in the market.

Refining remains a significant application area for PEM electrolyzer materials as oil refiners explore low-carbon hydrogen pathways to reduce emissions from conventional hydrogen use. Hydrogen is widely used in refining processes such as hydrocracking and desulfurization, making the sector an important candidate for clean energy substitution. PEM electrolyzers are gaining attention in this space for their operational flexibility and suitability for integrating renewable electricity, particularly for refiners pursuing gradual decarbonization strategies. Therefore, the refining segment is expected to grow at a CAGR of 29.3% from 2026 to 2034.

Steel production is expected to emerge as the fastest-growing segments as the industry increasingly explores green hydrogen for direct-reduced iron and other low-carbon metallurgical routes. PEM electrolyzers can support this transition by supplying renewable hydrogen, especially in projects where flexible power use and high-purity output are beneficial. Although the segment is still at a relatively early stage compared with refining or ammonia, long-term demand potential is substantial as pilot and commercial demonstration activities expand. Therefore, the steel production segment is forecast to grow at a CAGR of 36.2% from 2026 to 2034.

Power generation and energy storage are gaining relevance as hydrogen increasingly becomes part of long-duration storage, renewable balancing, sector-coupling strategies, and fuel cell-based power applications. PEM electrolyzers are suitable for grid-linked hydrogen production and for supplying green hydrogen to stationary and distributed fuel cell systems. Although this segment remains relatively small in the current market, its strategic importance is increasing as power systems integrate hydrogen-to-power generation. Therefore, the segment is projected to expand at a CAGR of 35.1% from 2026 to 2034, reflecting strong future potential.

PEM Electrolyzer Materials Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific PEM Electrolyzer Materials Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominated the market in 2025, reaching USD 72.0 million, and is projected to remain the leading regional market over the forecast period, expanding at a CAGR of 31.2% over the forecast period. The region accounts for the largest share of market due to its strong concentration of electrolyzer manufacturing activity, rapid green hydrogen project development, and increasing policy support for domestic hydrogen ecosystems across major Asian economies. Moreover, the region’s growing role in the assembly of electrolyzer systems and in localizing the supply chain continues to reinforce its dominant position in the market.

China PEM Electrolyzer Materials Market

China is expected to account for USD 48.6 million in 2026, representing around 30.3% of global market sales, supported by aggressive green hydrogen capacity additions, expanding domestic electrolyzer manufacturing, and strong policy backing for clean hydrogen infrastructure. The country’s leading position is further reinforced by its broader push to localize key hydrogen technologies and scale up deployment across industrial decarbonization applications.

To know how our report can help streamline your business, Speak to Analyst

India PEM Electrolyzer Materials Market

India will reach USD 17.9 million in 2026, contributing close to 11.0% of the global market. The country’s growth is being supported by rising investment interest under the National Green Hydrogen Mission, increasing participation in electrolyzer manufacturing, and the gradual development of hydrogen-linked projects across fertilizers, refining, and renewable-powered industrial applications. As commercialization accelerates, demand for specialized PEM materials is expected to expand further.

North America

North America reached USD 13.2 million in 2025 and is projected to expand at a CAGR of 33.1% during the forecast period. Regional growth is being driven by expanding clean hydrogen hub initiatives, increasing government support, and rising project activity tied to industrial decarbonization and low-carbon fuels. The market is also supported by efforts to establish domestic supply chains for electrolyzer systems and critical stack materials, particularly in the U.S., where hydrogen deployment is gaining stronger strategic importance.

U.S. PEM Electrolyzer Materials Market

The U.S. market will be valued at USD 16.0 million in 2026, accounting for roughly 10.0% of global revenues. Federal funding initiatives are supporting demand, announcing hydrogen hub projects, and increasing investment in domestic electrolyzer deployment. The country is also witnessing rising interest in renewable hydrogen for transportation, refining, and energy storage applications, which is positively influencing demand for PEM electrolyzer materials.

Europe

Europe reached USD 28.8 million in 2025, growing at a CAGR of 32.0% over the forecast period. The region represents a policy-led, technology-intensive market, supported by strong decarbonization commitments, hydrogen strategy frameworks, and an increasing industrial focus on low-carbon feedstock. Demand for PEM electrolyzer materials is closely tied to applications in refining, chemicals, steel, and power system balancing. In addition, Europe’s emphasis on hydrogen infrastructure, local production, and supply chain resilience is creating favorable conditions for long-term market expansion.

Germany PEM Electrolyzer Materials Market

Germany is probable to reach USD 13.1 million by 2026, representing nearly 8.2% of global demand. The country remains one of Europe’s most important markets, supported by its industrial decarbonization agenda, strong project pipeline, and active participation in electrolyzer deployment initiatives. Demand for PEM electrolyzer materials is also being bolstered by Germany’s focus on integrating renewable energy for industrial transformation.

U.K. PEM Electrolyzer Materials Market

The U.K. market will reach USD 8.4 million in 2026, accounting for around 5.3% of the global market. The country’s evolving hydrogen economy is shaping growth, rising policy support for low-carbon hydrogen production, and increasing interest in renewable-linked electrolyzer deployment. The U.K. is also strengthening its position in hydrogen-based industrial clusters, helping create medium-term demand for advanced PEM stack materials.

Rest of World

The Rest of the World region reached USD 6.0 million in 2025 and is projected to register the fastest regional growth at a CAGR of 33.9% through 2034. This segment covers emerging hydrogen markets across the Middle East, Latin America, and other developing regions, where interest in green hydrogen is rising as part of the energy transition and export-oriented clean-fuel strategies. Although the current market size remains comparatively small, improved policy support, abundant renewable energy resources, and the gradual commercialization of hydrogen projects are expected to drive stronger future demand for PEM electrolyzer materials.

COMPETITIVE LANDSCAPE

Key Industry Players

Material Innovation, Supply Chain Expansion, and Strategic Partnerships Are Reshaping Competitive Positioning

The global market is moderately consolidated, with competition led by a focused group of specialized material suppliers that focus on precious-metal catalyst development, porous transport layer engineering, titanium processing, advanced coatings, and precision stack-material manufacturing. Key companies such as Chemours, W. L. Gore & Associates, Johnson Matthey, Heraeus Precious Metals, Umicore, Bekaert, ATI, and Toray Industries continue to maintain strong market positions through various organic and inorganic strategies. For instance, Chemours has expanded its focus on Nafion-related membrane capacity and durable high-performance membrane development. Similarly, Bekaert has strengthened its market position through both its Hydrogen Innovation Hub and its partnership with Toshiba for iridium-saving MEA technology. Therefore, the competitive landscape is increasingly being shaped by a cumulative mix of low-iridium innovation, membrane advancement, recycling integration, strategic partnerships, and manufacturing expansion.

LIST OF KEY PEM ELECTROLYZER MATERIALS COMPANIES PROFILED

- 3M (U.S.)

- Bekaert (Belgium)

- Chemours (U.S.)

- Ensinger Plastics (Germany)

- FUMATECH BWT GmbH (Germany)

- Johnson Matthey (U.K.)

- Heraeus Precious Metals (Germany)

- Toray Industries (Japan)

- Umicore (Belgium)

- L. Gore & Associates (U.S.)

- Hovogen (China)

KEY INDUSTRY DEVELOPMENTS

- April 2025: Bekaert opened its Hydrogen Innovation Hub in Belgium, a dedicated facility focused on accelerating innovation in electrolyzer technologies and porous transport layer (PTL) development. The hub is intended to support faster product validation, strengthen customer collaboration, and advance market-ready PTL and cell-material innovations for both PEM and AEM electrolyzer platforms.

- February 2024: Bekaert and Toshiba Energy Systems & Solutions signed a global partnership and manufacturing technology license agreement for membrane electrode assembly (MEA) technology for PEM electrolyzers. The collaboration combines Bekaert’s PTL expertise with Toshiba’s iridium-saving MEA technology, designed to enable a 90% reduction in iridium use, supporting a more stable material supply.

- September 2024: Ravindra Heraeus acquired Arora Matthey’s catalyst and recycling site in Vizag, India, expanding Heraeus’ footprint in precious metal catalyst production and recycling. The acquisition is intended to strengthen regional access to catalyst and recycling capabilities and improve support for customers requiring high-quality precious metal solutions.

- June 2024: Heraeus acquired 100% of McCol Metals in Canada, a company specializing in recovering and recycling iridium from spent mixed metal oxide electrodes. The acquisition is intended to strengthen Heraeus’s precious metals recycling capabilities and support the circular supply of iridium.

- February 2024: Chemours and its partners were selected for USD 0.06 billion in U.S. Department of Energy grants, with Chemours leading a project on durable, high-performance membranes for PEM water electrolysis. The program is intended to develop a low-resistance Nafion membrane with high stack durability and improved manufacturability at scale.

REPORT COVERAGE

The global PEM electrolyzer materials market analysis provides an in-depth study of market size & forecast across all market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 31.8% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Material Type, End Use, and Region |

| By Material Type |

|

| By End Use |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 120.0 million in 2025 and is projected to reach USD 1,459.3 million by 2034.

In 2025, the Asia Pacific market value stood at USD 72.0 million.

Recording a CAGR of 31.8%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The ammonia production end use segment led in 2025.

The rising green hydrogen project pipeline and electrolyzer installations are expected to drive market growth.

Chemours, W. L. Gore & Associates, Johnson Matthey, Heraeus Precious Metals, Umicore, Bekaert, and Toray Industries are some of the prominent players in the market.

Asia Pacific held the highest market share in 2025.

Low-Iridium catalyst development and material efficiency improvements are expected to favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us