Peptide Mapping Market Size, Share & Industry Analysis, By Product (Consumables, Instruments, Software, and Services & Workflow Solutions), By Application (Biologics Characterization, QC & Release Testing, Stability Testing, and Others), By Technology (LC-MS/MS Peptide Mapping, LC-MS Peptide Mapping, LC-UV / HPLC-UV Peptide Mapping, and Others), By Type of Peptide (Monoclonal Antibody-derived Peptides, and Others), By End User (Pharmaceutical & Biotechnology Companies, CROs/CDMOs & Analytical Testing Labs, Academic & Research Institutes, and Others), and Regional Forecast, 2026-2034

Peptide Mapping Market Size and Future Outlook

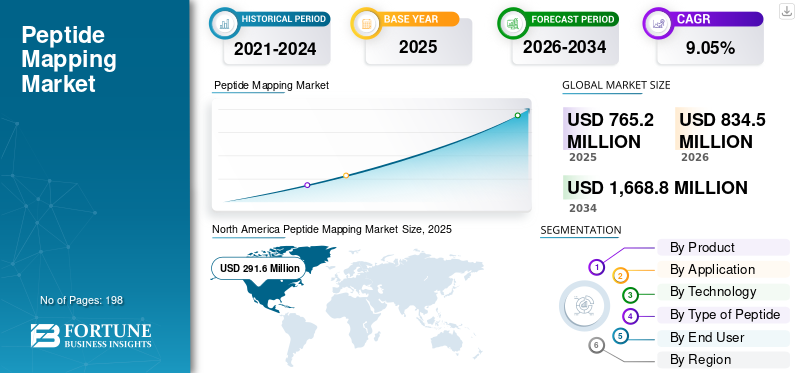

The global peptide mapping market size was valued at USD 765.2 million in 2025. The market is projected to grow from USD 834.5 million in 2026 to USD 1,668.8 million by 2034, exhibiting a CAGR of 9.05% during the forecast period. North America dominated the peptide mapping market with a market share of 38.11% in 2025.

Peptide mapping is widely used in biologics characterization, QC & release testing, biosimilar comparability, stability testing, process development, and peptide drug analysis. The market is gaining importance as pharmaceutical and biotechnology companies are increasing their focus on complex biologics, monoclonal antibodies, recombinant proteins, biosimilars, and antibody-drug conjugates, where detailed peptide-level analysis is required to confirm identity, sequence coverage, post-translational modifications, degradation, and product consistency.

Key players operating in the global market include Thermo Fisher Scientific Inc., Danaher Corporation, and Agilent Technologies, Inc. These companies are focusing on high-resolution mass spectrometry systems, UHPLC/HPLC platforms, peptide mapping columns, digestion enzymes, sample preparation kits, biopharma informatics software, and outsourced analytical testing services to strengthen their market presence.

Download Free sample to learn more about this report.

Peptide Mapping Market Key Takeways

- 2025 Market Size: USD 765.2 million

- 2026 Market Size: USD 834.5 million

- 2034 Forecast Market Size: USD 1,668.8 million

- CAGR: 9.05% from 2026–2034

- North America dominated the peptide mapping market with a 38.11% share in 2025.

- The monoclonal antibody-derived peptides segment is set to hold a 36.6% share in 2026.

- The pharmaceutical & biotechnology companies segment is set to hold a 55.1% share in 2026.

North America

North America maintained its leading position in 2025, with the market valued at USD 291.6 million.

Europe

Europe is projected to expand at a CAGR of 8.36% during the forecast period, supported by a strong biosimilar development ecosystem and established biopharma manufacturing base.

Asia Pacific

Asia Pacific market size is expected to reach USD 221.8 million by 2026, driven by increasing biologics research and manufacturing activities.

U.S.

U.S. The market is projected to reach approximately USD 295.1 million by 2026, leading the North American region.

Japan

Japan The market is estimated to reach around USD 50.5 million by 2026.

Read More

PEPTIDE MAPPING MARKET TRENDS

Integration of AI and Automation in Peptide Analysis Workflows is a Major Trend Observed in the Market

The incorporation of AI and automation into peptide analysis workflows is becoming a significant trend in the global market, as laboratories aim to decrease manual review time, enhance reproducibility, and handle the increasing volume of LC-MS/MS data produced by biologics and biosimilar programs. Peptide mapping consists of several labor-intensive stages, such as sample digestion, chromatographic separation, MS data acquisition, identification of peptides, analysis of PTMs, review of sequence coverage, and reporting results. Consequently, organizations are progressively embracing automated sample preparation systems, AI/ML-driven data analysis, and workflow-oriented software to minimize analyst reliance and enhance uniformity in development and QC environments. This trend holds significant importance for monoclonal antibodies, ADCs, recombinant proteins, and biosimilars, as even minor sequence variations, oxidation, deamidation, glycation, or clipping events need to be identified with high assurance. Automation assists CROs/CDMOs and analytical testing laboratories in boosting throughput as additional biologics progress through development and necessitate repeated peptide mapping for characterization, comparability, stability, and release testing. In general, AI and automation are transforming peptide mapping from a predominantly expert-led analytical procedure into a quicker, more uniform, and scalable process. These factors are supporting the overall global peptide mapping market growth.

- For instance, in October 2024, Genedata announced Genedata Expressionist 18.5, which introduced automated characterization workflows for novel therapeutics and specifically highlighted faster high-throughput peptide mapping data review for biotherapeutics using mass spectrometry.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growth in Proteomics and Protein Characterization Research to Boost Market Growth

The expansion of proteomics and protein characterization studies significantly contributes to the global market, as peptide mapping serves as a fundamental analytical technique to analyze protein sequence, structure, modifications, and product quality. With the growth of biologics, biosimilars, antibody-drug conjugates (ADCs), recombinant proteins, and peptide-focused drug pipelines in pharmaceutical and biotechnology firms, there is a necessity for dependable peptide-level information to validate sequence coverage, identify post-translational modifications, and assess essential quality attributes. This is amplifying the application of LC-MS/MS, LC-MS, and HPLC-based peptide mapping throughout discovery, process development, comparability, stability, and QC workflows. The growth of proteomics research is generating a need for improved mass spectrometry resolution, enhanced digestion enzymes, advanced columns, and specialized software for data analysis. Furthermore, CROs/CDMOs and analytical testing laboratories are enhancing their protein characterization abilities to assist outsourced biologics development and regulatory filings. The rising significance of proteomics and thorough protein characterization is directly boosting the demand for precise, reproducible, and high-throughput peptide mapping processes.

- For instance, in 2025, Waters published an application note on advanced monoclonal antibody peptide mapping using multi-reflecting TOF-MS technology, highlighting peptide mapping as a primary approach for characterization and monitoring of biotherapeutics, particularly monoclonal antibodies, to confirm protein identity, sequence, modifications, and product-related impurities.

MARKET RESTRAINTS

High Cost of Advanced Analytical Instrumentation to Limit Market Growth

The expensive nature of advanced analytical instruments serves as a limitation for the global market since peptide mapping typically necessitates high-resolution LC-MS/MS systems, UHPLC/HPLC platforms, automated sample preparation equipment, validated software, and proficient technical support. These systems require significant initial capital outlay, along with ongoing expenses for maintenance agreements, columns, solvents, enzymes, calibration standards, software licenses, and skilled analysts. Consequently, smaller biotechnology firms, research institutions, and local analytical testing laboratories might postpone implementation or rely on external peptide mapping services rather than developing them internally. The limitations are more pronounced in emerging markets, where budget constraints and restricted access to advanced mass spectrometry facilities hinder the routine implementation of peptide mapping in the development of biologics and biosimilars. The elevated cost of instruments impacts scalability, since labs require numerous systems to facilitate high-throughput QC, stability, and comparability research. In general, although sophisticated LC-MS/MS systems enhance peptide-level analysis, their expense restricts broader usage among cost-sensitive consumers.

- For instance, in June 2025, Thermo Fisher Scientific launched the Orbitrap Astral Zoom MS and Orbitrap Excedion Pro MS at ASMS 2025, highlighting next-generation high-resolution mass spectrometry for proteomics, biopharma applications, protein data, and post-translational modification analysis. Such advanced platforms strengthen peptide mapping capabilities, but they also reflect the high-end instrumentation requirements that can increase capital burden for smaller laboratories and outsourced testing providers.

MARKET OPPORTUNITIES

Expansion of Advanced Bioanalytical and Proteomics Applications to Offer Lucrative Growth Opportunities

Expansion of advanced bioanalytical and proteomics applications is creating a strong opportunity for the global market as peptide-level analysis is moving beyond from basic protein identity confirmation to broader use across biologics development, biosimilar comparability, ADC characterization, stability studies, impurity profiling, and process monitoring. As pharmaceutical pipelines shift toward complex proteins, peptides, and next-generation biologics, companies need deeper analytical data to understand sequence coverage, post-translational modifications, degradation pathways, and product-related variants. This is increasing the demand for high-resolution LC-MS/MS systems, biocompatible HPLC/UHPLC platforms, peptide mapping columns, digestion reagents, and automated informatics tools. Advanced bioanalytical applications also support DMPK, immunogenicity risk assessment, and large-molecule quantification, which creates additional use cases for peptide mapping workflows. CROs, CDMOs, and analytical testing labs can benefit from this opportunity by offering specialized peptide mapping services to pharma and biotech clients that lack in-house advanced mass spectrometry capabilities. Overall, the expansion of proteomics and bioanalytical applications is widening the commercial scope of the market from research use to routine development, QC, and regulatory support.

- For instance, in April 2025, Waters Corporation announced the expansion of its Alliance iS Bio HPLC product line with integrated photodiode array detection for biopharma development and QC laboratories. This system supports enhanced spectral analysis, including impurity detection, peak purity analysis, multi-wavelength detection, and method validation, which strengthens advanced bioanalytical workflows relevant to peptide mapping and protein.

MARKET CHALLENGES

Requirement for Highly Skilled Professionals Pose a Prominent Challenge to Market Growth

Requirement for highly skilled professionals is a major challenge for the global market as peptide mapping requires strong expertise in enzymatic digestion, LC/HPLC method development, high-resolution mass spectrometry, peptide sequencing, PTM interpretation, data processing, and regulatory documentation. Even with advanced instruments and software, inaccurate sample preparation, incomplete digestion, poor chromatographic resolution, or incorrect MS data interpretation can affect sequence coverage and lead to unreliable characterization results. This creates a dependency on trained analytical scientists, bioinformaticians, and QC specialists who understand both protein chemistry and regulated biopharma testing requirements. Small biotech firms, academic labs, and regional testing facilities may face delays because they often lack presence of enough experienced LC-MS and biopharma characterization professionals. The challenge also increases outsourcing dependency, as companies may prefer CROs/CDMOs or specialist analytical labs rather than building full peptide mapping capabilities themselves internally. Overall, limited availability of skilled professionals can slow adoption, reduce testing throughput, and create variability in peptide mapping workflows. For instance, in August 2025, a Springer-published review on biopharmaceutical analysis identified the need for skilled professionals to implement advanced analytical techniques as one of the key limitations, along with the complexity of biopharmaceuticals and high instrumentation costs.

Segmentation Analysis

By Product

Instruments Segment Took The Lead Owing To Its Critical Role In Reproducible And Reliable Peptide-Level Analysis

In terms of product, the market is divided into software, services & workflow solutions, consumables, instruments, and reagents & enzymes.

The instruments segment led the global peptide mapping market share in 2025 as instruments are essential for peptide separation, mass detection, sequence confirmation, PTM identification, impurity profiling, and comparability analysis in biologics and biosimilar development. Moreover, instruments carry higher unit value, which gives makes them larger revenue contributors even when purchase frequency is lower. Also, pharmaceutical and biotechnology companies also prefer advanced instruments because they support multiple applications. This makes instruments the most commercially significant product segment, supported by their critical role in reliable and reproducible peptide-level analysis.

- For instance, in 2025, Waters published an application note demonstrating advanced monoclonal antibody peptide mapping using the ACQUITY Premier UPLC System coupled with the Xevo MRT Mass Spectrometer, highlighting high sensitivity, high mass resolution, sub-ppm mass accuracy, and confident identification of product variants and impurities.

The software, services & workflow solutions segment is anticipated to rise with a CAGR of 10.89% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

High Use of Biologics Characterization in Complex Biologics Development Has Bolstered theSegment’s Leadership

Based on application, the market is classified into biologics characterization, QC & release testing, biosimilar comparability, stability testing, process development, peptide drug analysis, and others.

The biologics characterization segment accounted for the dominant market share in 2025 as peptide mapping is one of the most significant methods used to confirm the primary structure, sequence coverage, post-translational modifications, impurities, and product variants of therapeutic proteins. This segment also benefits from the growing number of biologics and biosimilars in development, where companies must prove product identity, consistency, and quality before clinical and commercial use. Furthermore, the segment is set to hold 29.7% share in 2026.

- For instance, in September 2025, Danaher Life Sciences published a SCIEX-focused application article on ADC characterization, highlighting the use of EAD peptide mapping and icIEF-UV/MS for multilevel characterization of antibody-drug conjugates and for supporting the development of high-quality biologic drug products.

The biosimilar comparability segment is anticipated to rise with a CAGR of 10.74% over the forecast period.

By Technology

Superior Fragmenatation-Based Sequence Confirmation and Peptide Mass Information has Helped LC-MS/MS Peptide Mapping to be the Superior Technology

On the basis of technology, the market is divided into LC-MS/MS peptide mapping, LC-MS peptide mapping, LC-UV / HPLC-UV peptide mapping, and others.

In 2025, LC-MS/MS peptide mapping segment led the market as this technology provides both peptide mass information and fragmentation-based sequence confirmation, making it more powerful than LC-UV or single-stage LC-MS methods. In addition, LC-MS/MS is also preferred in regulated biopharma workflows as it supports deeper characterization and better evidence for product identity, comparability, and quality attributes. Furthermore, the segment is set to hold 47.5% share in 2026.

- For instance, in October 2025, a review published in the International Journal of Molecular Sciences highlighted that peptide mapping has evolved from LC-UV approaches toward high-resolution mass spectrometry, and MS/MS fragmentation is required for residue-level amino acid sequence confirmation in therapeutic proteins and recombinant vaccine antigens.

The LC-MS peptide mapping segment is anticipated to rise with a CAGR of 8.42% over the forecast period.

By Type of Peptide

Monoclonal Antibodies for Developing Classes Of Biologic Drugs Aided Monoclonal Antibody-derived Peptides to Gain a Leading Position

Based on type of peptide, the market is categorized into monoclonal antibody-derived peptides, recombinant protein-derived peptides, synthetic therapeutic peptides, biosimilar product-derived peptides, ADC-derived peptides, and others.

In 2025, the monoclonal antibody-derived peptides segment dominated the global market as monoclonal antibodies remain one of the largest and most actively developed classes of biologic drugs across oncology, autoimmune diseases, inflammatory disorders, and rare diseases. Since mAbs are large and structurally complex proteins, manufacturers need peptide-level analysis during discovery, process development, comparability, stability testing, and regulatory submissions. The segment also benefits from the growing use of biosimilar mAbs, where peptide mapping is essential to compare the biosimilar with the reference product. Furthermore, the segment is set to hold 36.6% share in 2026.

- For instance, in October 2025, a study published in mAbs discussed the development and qualification of an LC-MS peptide mapping multi-attribute method for protein biopharmaceuticals such as monoclonal antibodies, highlighting its role in detecting purity and impurity attributes for release and stability testing.

The ADC-derived peptides segment is anticipated to rise with a CAGR of 12.21% over the forecast period.

By End User

Strong In-house Biologics Development and Commercial Need Has Upholded the Dominance for Pharmaceutical & Biotechnology Companies’ Dominance

Based on end user, the market is segmented into pharmaceutical & biotechnology companies, CROs/CDMOs & analytical testing labs, academic & research institutes, and others.

The pharmaceutical & biotechnology companies segment dominated the market share in 2025. These companies are the primary developers and manufacturers of biologics, biosimilars, recombinant proteins, ADCs, and peptide-based therapeutics. Large biopharma companies usually invest directly in LC-MS/MS systems, HPLC/UHPLC platforms, digestion reagents, columns, and informatics tools because peptide mapping is repeatedly required throughout a product’s lifecycle. Moreover, pharma and biotech companies have stronger commercial need, larger testing volumes, and higher regulatory responsibility for product quality, thereby supporting the segment growth. Furthermore, the segment is set to hold 55.1% share in 2026.

- For instance, in November 2025, the MAM Consortium listed a presentation by Novartis titled “Development, Qualification, and Application of a Highly Efficient and Robust New Peak Detection Workflow for the LC-MS Peptide Mapping Multi-Attribute Method,” showing how major pharmaceutical companies are actively applying peptide mapping workflows for biopharmaceutical product characterization and quality monitoring. Source: MAM Consortium.

In addition, CROs/CDMOs & analytical testing labs are projected to witness 10.50% growth rate during the forecast period.

Peptide Mapping Market Regional Outlook

Based on region, the global market is divided into Asia Pacific, Latin America, Europe, North America, and the Middle East & Africa.

North America

North America Peptide Mapping Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

The North America market was vauled at USD 271.8 million in 2024 and dominated the global market. In 2025, the region maintained its leading position, with USD 291.6 million. The region is expected to remain a leading region due to the strong presence of pharmaceutical and biotechnology companies, advanced biologics R&D, and high adoption of LC-MS/MS and UHPLC-based analytical workflows.

U.S. Peptide Mapping Market

The U.S. market led the North American region and is projected to be approximately USD 295.1 million in 2026, representing about 35.4% of the global market.

Europe

Europe market is growing at a CAGR of 8.36% during the forecast period. Europe’s market growth is supported by strong biosimilar development ecosystem, established biopharma manufacturing base, and rising focus on biologics quality control. Growth is also driven by increasing investment in biologics, recombinant proteins, ADCs, and advanced protein characterization workflows across both innovator and biosimilar companies.

U.K. Peptide Mapping Market

The U.K. market in 2026 is estimated at around USD 44.3 million, representing roughly 5.3% of global revenues.

Germany Peptide Mapping Market

Germany market size is projected to reach approximately USD 55.1 million in 2026, equivalent to around 6.6% of global sales.

Asia Pacific

The Asia Pacific market size is expected to reach a valuation of USD 221.8 million by 2026. Asia Pacific is expected to show strong growth due to rapid expansion of biologics manufacturing, biosimilar development, and contract research and manufacturing activities. Rising government support for biotechnology, lower manufacturing costs, and growing local biologics pipelines are further supporting market expansion.

Japan Peptide Mapping Market

The Japan market in 2026 is estimated at around USD 50.5 million, accounting for roughly 6.0% of global revenues.

China Peptide Mapping Market

China’s market is projected to reach revenues of around USD 67.5 million in 2026, representing roughly 8.1% of global sales.

India Peptide Mapping Market

The India market in 2026 is estimated at around USD 30.7 million, accounting for roughly 3.7% of global revenues.

Latin America and Middle East & Africa

The growth in the Middle East & Africa and Latin America regions is anticipated to be moderate in the coming years. Key factors such as increasing investment in healthcare infrastructure, biotechnology research, and local pharmaceutical manufacturing are expected to boost the market growth in these regions. The Latin America market in 2026 is estimated at around USD 32.2 million.

In the Middle East Africa region, the GCC market is projected to reach approximately USD 10.0 million by 2026, representing about 1.2% of worldwide revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Instrument, Application-Specific Workflow, and Testing Specialists are Leading Through Integrated Peptide Mapping Solutions

The competitive landscape of the global market is moderately consolidated, with Thermo Fisher Scientific Inc., Agilent Technologies Inc., Danaher Corporation, and others holding the strongest position in the market. Their strategies are focused on improving sequence coverage, PTM identification, impurity profiling, workflow automation, and regulatory-ready data reporting for biologics, biosimilars, ADCs, recombinant proteins, and peptide therapeutics.

- For instance, January 2025, Agilent Technologies announced that it would feature new automated laboratory workflow solutions at SLAS2025, aimed at improving lab productivity, efficiency, and reproducibility across research, drug discovery, development, and manufacturing workflows.

Other significant participants include Merck KGaA, Promega Corporation, New England Biolabs, among others. These firms are strengthening their presence through product launches, application-specific peptide mapping workflows, biopharma software upgrades, and outsourced characterization services.

LIST OF KEY PEPTIDE MAPPING COMPANIES PROFILED

- Thermo Fisher Scientific Inc. (U.S.)

- Agilent Technologies Inc. (U.S.)

- Waters Corporation (U.S.)

- Danaher Corporation (U.S.)

- Shimadzu Corporation (Japan)

- Bruker (U.S.)

- Merck KGaA (Germany)

- Promega Corporation (U.S.)

- New England Biolabs (U.S.)

- Charles River Laboratories (U.S.)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Bruker announced new machine-learning additions to ProteoScape software for immunopeptidomics, PTM analysis, de novo peptide identification, and proteoform characterization. This supports advanced peptide-level analysis and strengthens software-driven protein characterization workflows.

- June 2025: Isogenica announced a collaboration with Charles River to accelerate next-generation peptide and VHH discovery, combining Isogenica’s synthetic peptide/VHH libraries with Charles River’s drug discovery and development expertise.

- September 2024: Eurofins expanded its U.S. BioPharma Product Testing offering through the acquisition of Infinity Laboratories, adding 8 laboratories and strengthening its analytical testing network for pharmaceutical and biotechnology clients.

- July 2024: SGS announced the expansion of biologics testing capabilities at its Lincolnshire Center of Excellence, adding instrumentation, expertise, and capacity to support product characterization of novel biologics and biosimilars.

- June 2024: SCIEX launched ZT Scan DIA at ASMS 2024, a next-generation data-independent acquisition method for LC-MS/MS that improves depth, precision, sensitivity, and selectivity in protein and peptide analysis workflows.

REPORT COVERAGE

The global peptide mapping market analysis includes a thorough evaluation of the market size and forecasts for every segment highlighted in the report. It offers insights into the market dynamics and trends expected to drive the market throughout the forecast period. The global market report provides understanding of essential factors, including technological progress, product innovations, the regulatory environment, and the launch of new products. Additionally, it details partnerships, mergers & acquisitions, as well as key developments in the industry within the market. The global market forecast report also provides an in-depth competitive landscape, including information on market share and profiles of key active players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.05% from 2026 to 2034 |

| Unit | Value (USD Million) |

| Segmentation | By Product, Application, Technology, Type of Peptide, End User, and Region |

| By Product |

|

| By Application |

|

| By Technology |

|

| By Type of Peptide |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 765.2 million in 2025 and is projected to reach USD 1,668.8 million by 2034.

In 2025, the market value for North America stood at USD 291.6 million.

The market is expected to exhibit a CAGR of 9.05% during the forecast period.

By product, the instruments segment is expected to lead the market.

Increasing biologics and biosimilar approvals globally and growth in proteomics and protein characterization research are primarily driving market expansion.

Thermo Fisher Scientific Inc., Agilent Technologies Inc., and Danaher Corporation are some of the prominent players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 198

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us