Personal Watercraft Market Size, Share & Industry Analysis, By Product Type (Rec-Lite, Recreation, Stand-Up, Performance, and Luxury / Touring), By Distribution Channel (Direct and Indirect Channel), By Propulsion (ICE and Electric), By End User (Individual User, Rental Operator, and Military/ Law Enforcements), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

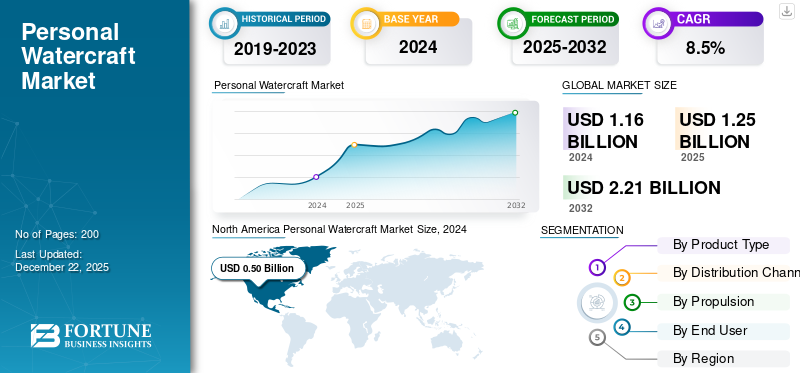

The global personal watercraft market size was valued at USD 1.25 billion in 2025 and is projected to grow from USD 1.35 billion in 2026 to USD 2.59 billion by 2034, exhibiting a CAGR of 8.51% during the forecast period. North America dominated the personal watercraft market with a market share of 42.36% in 2025.

Personal Watercraft (PWC) is a small, motorized water vehicle designed for individual or small-group use, where the rider sits, kneels, or stands on the craft rather than inside it, unlike traditional boats.

The PWC demand is witnessing strong growth, primarily driven by the rising popularity of recreational and adventure activities. Consumers are increasingly seeking engaging water-based leisure options such as jet skiing, wakeboarding, and coastal exploration, which has positioned personal watercraft as a preferred choice for both individual use and rental services. The expansion of coastal tourism, growing participation in water sports, and the rising trend of adventure tourism, especially among younger demographics, are further fueling this demand. In addition, the development of marinas, water sports infrastructure, and rental fleets has made PWCs more accessible to a wider audience, complementing the shift toward recreational lifestyles and higher discretionary spending. As a result, the recreational segment continues to be the primary driver behind the global growth of the personal watercraft industry.

Download Free sample to learn more about this report.

For Instance:

According to the Bureau of Economic Analysis, the U.S. outdoor recreation economy accounted for 1.9% of current-dollar gross domestic product (GDP) for the nation in 2021. This is up from 1.7% in 2020 but still below the 2.2% before the COVID–19.

In 2020 and 2021, the market experienced a notable downturn due to the impact of the COVID-19 pandemic. Global lockdowns, restrictions on tourism, and the closure of recreational facilities significantly reduced consumer participation in water-based leisure activities. However, the market began to recover gradually as restrictions eased, outdoor activities gained popularity, and consumer preference shifted toward individual recreational experiences.

Download Free sample to learn more about this report.

Personal Watercraft Market Trends

Electric PWC is Expected to Have a Strong Hold in Market

The e-PWC market is emerging as one of the fastest-growing segments within the marine leisure industry, driven by rising environmental concerns, stricter emission regulations, and consumer demand for sustainable recreation. Unlike traditional gasoline-powered models, e-PWCs offer quieter, zero-emission rides, making them increasingly attractive for rental fleets, eco-tourism, and recreational users in lakes, coastal resorts, and urban waterfronts. Advances in lithium-ion battery technology and fast-charging solutions are extending ride times and reducing range anxiety, while major brands such as Sea-Doo and Yamaha, along with innovators such as Taiga Motors, are investing heavily in electric models.

This shift is further supported by government incentives and the growing global emphasis on green mobility. Although higher upfront costs and limited charging infrastructure remain challenges, the strong appeal of cleaner, smarter, and more efficient personal watercrafts is positioning the electric segment as a key growth driver in the overall PWC market, with adoption expected to accelerate rapidly over the next decade.

MARKET DRIVERS

Technological Advancements in PWCs to Boost Market Growth

Technological advancements in product designs are playing a crucial role in shaping the personal watercraft market growth and enhancing user experience. Modern PWCs are being equipped with advanced digital features such as GPS navigation, Bluetooth connectivity, touch-screen displays, and smartphone integration, which improve convenience and safety for riders. Manufacturers are also incorporating intelligent braking and reverse systems, improved hull designs for stability, and advanced ride-control modes that cater to both beginners and experienced users.

For instance, in 2023, California-based e-boat startup Boundary Layer Technologies (BLT) officially launched its Valo Hyperfoil, an all-electric hydrofoiling jet ski. The company revealed that pre-orders for the craft have already exceeded expectations, with demand is projected to reach three times the planned production volume for the inaugural 2023 run.

BLT only began developing the Valo Hyperfoil in late 2022, following a strategic pivot from its original mission of applying hydrofoiling technology to container ships. The company’s rapid shift toward personal watercraft has now positioned it at the forefront of the growing electric PWC market.

In parallel, the industry is witnessing a shift toward eco-friendly innovations, with the development of electric and hybrid personal watercrafts that reduce emissions and noise while delivering high performance. Lightweight materials such as carbon fiber and improved hydrodynamic designs are further enhancing speed, efficiency, and maneuverability. These technological upgrades not only make personal watercrafts more appealing to consumers but also align them with evolving environmental regulations and sustainability trends, positioning the segment for stronger adoption in both developed and emerging markets.

MARKET RESTRAINTS

Seasonal Demand and Increasing Accidental Cases are Restraining Market Growth

Seasonal demand and limited utility act as significant restraints for the PWC market. Unlike automobiles or motorcycles that can be used year-round, personal watercrafts are highly dependent on favorable weather conditions and are mostly restricted to summer seasons or warm coastal regions. In colder climates, their usage is limited to just a few months, which reduces the overall value proposition for potential buyers. This seasonal nature of demand also impacts rental operators and manufacturers, as sales and revenues fluctuate significantly during off-peak months.

PWCs are often operated at high speeds in recreational settings, where lack of experience, inadequate training, or negligence can lead to collisions and mishaps. According to reports from various marine safety authorities, a significant percentage of boating accidents involve PWCs, many of which result in serious injuries or fatalities. This growing safety risk has led to stricter regulations, higher insurance costs, and even restrictions on PWC use in certain water bodies.

For instance, according to the Recreational Boating Statistics 2023, there were 47 deaths involving PWC in the U.S.

MARKET OPPORTUNITES

Expansion of Tourism and Rental Services to Create Ample Opportunities for Market

The rising global travel and adventure tourism continue to boost demand for recreational water activities. Coastal destinations, island resorts, and waterfront cities are increasingly offering PWC rentals as part of their leisure and adventure packages, making the experience more accessible to tourists who may not own a craft. This rental model broadens the user base beyond private owners but also provides recurring revenue for operators and manufacturers through fleet sales. Additionally, the growing popularity of eco-tourism and water adventure parks is driving resorts and marine service providers to invest in fleets of modern, eco-friendly PWCs, including electric models that meet sustainability requirements. As international tourism rebounds strongly post-pandemic, the integration of personal watercrafts into resort activities, cruise ship packages, and recreational marinas is expected to significantly accelerate market growth.

Download Free sample to learn more about this report.

For instance:

Source: IBEF

According to IBEF, the travel market in India is projected to reach USD 125 billion by FY27 from an estimated USD 75 billion in FY20. By 2028, international tourist arrivals are expected to reach 30.5 billion and generate revenue of over USD 59 billion. However, domestic tourists are expected to drive the growth. This travel and tourism industry growth is indirectly boosting the PWC market.

Segmentation Analysis

By Product Type

Rising Interest in Water Sports Fueled Recreation Segment Growth

By product type, the market is segmented into rec-lite, recreation, stand-up, performance, and luxury/touring.

The recreation segment is projected to dominate the personal watercraft market by product type, accounting for 40.73% of the global market share in 2026. Increasing disposable incomes, coupled with a growing interest in water sports, coastal tourism, and adventure travel, are fueling the adoption of personal watercraft for recreational purposes. These watercrafts offer a thrilling yet accessible experience, making them highly popular among individuals, rental operators, and tourism companies. The rising trend of recreational boating and the expansion of organized water sports events further support the segment’s growth, positioning recreational personal watercrafts as a key contributor to the overall market expansion.

The luxury/touring segment is anticipated to witness the fastest growth in the coming years, driven by rising consumer preference for comfort, advanced features, and long-distance recreational rides. Unlike entry-level models, luxury/touring personal watercrafts are equipped with premium technologies such as GPS navigation, enhanced seating ergonomics, sound systems, larger fuel tanks, and superior stability, making them ideal for extended trips and water-based tourism.

In addition, segments such as Rec-Lite, Stand-Up, and Performance personal watercrafts are also experiencing notable growth, driven by their importance and widespread use across various water sports and recreational activities.

To know how our report can help streamline your business, Speak to Analyst

By Distribution Channel

Indirect Channel Segment Dominates Market as There is a Wide Dealer and Distributor Network

By distribution channel, the market is segmented into direct and indirect channel.

The indirect channel is expected to lead by distribution channel, contributing 83.68% globally in 2026 primarily due to the presence of a wide dealer and distributor network, which ensures extensive market reach and accessibility for customers. Dealers and distributors play a crucial role in connecting manufacturers with end users by offering localized sales points, easy availability of products, and personalized customer support. As a result, the widespread dealer and distributor presence has positioned the indirect channel as the leading mode of sales in the market.

The direct channel segment is also witnessing significant growth as manufacturers increasingly focus on strengthening their online presence and direct-to-consumer sales models. With the rise of e-commerce platforms and official brand websites, customers can now conveniently explore product portfolios, compare specifications, and make purchases directly from the manufacturer. Growing consumer preference for transparency, convenience, and exclusive brand experiences is therefore driving notable expansion in the direct channel segment of the PWC market.

By Propulsion

ICE Segment to Lead Market as It Provides Longer Riding Ranges and Higher Towing Capacity

By propulsion, the market is segmented into ICE and electric.

The Internal Combustion Engine (ICE) segment is anticipated to dominate the market as it offers longer riding ranges and higher towing capacity compared to emerging alternatives, making it highly suitable for extended touring and high-performance activities. Their ability to deliver consistent speed, superior acceleration, and the capability to tow equipment or additional riders gives them a clear advantage over electric models, which are still limited by battery capacity and charging infrastructure. This combination of performance, range, and versatility strongly positions the ICE segment as the leading category in the global PWC market.

The electric segment is also witnessing significant growth, driven by the rising emphasis on sustainability and the global shift toward eco-friendly mobility solutions. Growing environmental concerns and stricter emission regulations are encouraging manufacturers to invest in electric personal watercraft that produce zero emissions and operate with reduced noise levels, enhancing the overall user experience while minimizing ecological impact.

By End User

Rental Operator Segment to Dominate Market Owing to Increasing Demand for Recreational Activities

By end user, the market is segmented into individual user, rental operator, and military/law enforcements.

The rental operator segment is expected to lead by end use, holding 46.65% of the global market share in 2026, owing to the rising demand for water sports and recreational activities across coastal regions, lakes, and tourist destinations. Many consumers, especially tourists and occasional riders, prefer renting PWC rather than purchasing, as it provides a cost-effective way to experience the thrill of water-based activities without long-term ownership expenses. Rental operators typically offer fleets of various PWC models, catering to different customer preferences, from recreational rides to high-performance experiences.

The individual user segment is anticipated to grow at a significant rate as the demand for water sports is increasing. The individual user segment is anticipated to grow at a significant rate, driven by rising consumer interest in recreational boating, adventure tourism, and water-based leisure activities.

The military/law enforcements segment is also projected to grow at a significant rate, driven by the rising demand for water patrolling and maritime security operations.

PERSONAL WATERCRAFT MARKET REGIONAL OUTLOOK

By region, the market is divided into North America, Europe, Asia Pacific, and the Rest of the World.

North America

North America Personal Watercraft Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America Dominates Market Due to Greater Consumer Spending on Leisure and Recreational Activities

North America contributed 42.36% to the global market in 2025, with a valuation of USD 0.53 billion, and is projected to reach USD 0.57 billion in 2026, owing to higher consumer spending on leisure and recreational activities across the region. The presence of a well-established water sports culture, extensive coastlines, and numerous lakes and rivers has made personal watercraft highly popular among enthusiasts. The U.S. and Canada, in particular, account for a large share of global PWC sales, supported by strong demand for recreational boating, adventure tourism, and water-based sporting events. The U.S. market is projected to reach USD 0.36 billion by 2026.

Download Free sample to learn more about this report.

Europe

Europe accounted for USD 0.31 billion in 2025, representing 25.03% of the global market share, and is projected to reach USD 0.34 billion in 2026. The Europe personal watercraft market is also emerging and is anticipated as the fastest-growing market, driven by the rapid expansion of water-based tourism, recreational boating, and adventure sports across the region. Countries such as France, Italy, Spain, Croatia, and Greece are witnessing strong demand due to their extensive coastlines, thriving beach tourism, and popularity as global holiday destinations. The increasing number of marinas, boating clubs, and water sports facilities is further fueling adoption among both individual users and rental operators. The Croatia market is projected to reach USD 0.03 billion by 2026 and the Germany market is projected to reach USD 0.09 billion by 2026.

Rest of the World and Asia Pacific

The Asia Pacific market was valued at USD 0.28 billion in 2025, capturing 21.78% of global revenue, and is estimated to reach USD 0.3 billion in 2026. The Rest of the World region captured 10.56% of the global market in 2025, generating USD 0.13 billion in revenue, and is projected to reach USD 0.14 billion in 2026. The rest of the world and Asia Pacific personal watercraft market are also expected to witness significant growth, driven by rising interest in recreational boating and PWC rentals, supported by the expansion of waterfront tourism in these regions. The Japan market is projected to reach USD 0.08 billion by 2026, the China market is projected to reach USD 0.04 billion by 2026, and the India market is projected to reach USD 0.02 billion by 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Companies Focus on Enhancing Portfolio to Propel Market Expansion

The market is highly consolidated, with three leading players—BRP (Sea-Doo), Yamaha (WaveRunner), and Kawasaki (Jet Ski), collectively accounting for the majority of global sales. BRP’s Sea-Doo brand holds the largest market share, offering a wide portfolio that spans Rec-Lite, Luxury/Touring, and Performance models, supported by strong branding, frequent product innovation, and a robust dealer network. Yamaha’s WaveRunner lineup is renowned for reliability, advanced engineering, and racing pedigree, making it a strong competitor in both recreational and performance categories. Kawasaki, the original “Jet Ski” brand, retains a loyal customer base, particularly in the stand-up and high-performance niches, with its Ultra and SX-R series.

LIST OF KEY PERSONAL WATERCRAFT COMPANIES PROFILED

- BRP Inc. (Sea-Doo) (Canada)

- Yamaha Motor Co., Ltd (Japan)

- Kawasaki Heavy Industries, Ltd. (Japan)

- Taiga Motors (Canada)

- Belassi GmbH (Austria)

- Narke (Hungary)

- Polaris Inc (U.S.)

- Krash Industries (Australia)

- Gibbs Sports Amphibians (U.S.)

KEY INDUSTRY DEVELOPMENTS

- July 2025 – Taiga Motors Inc., a Canadian manufacturer of electric powersports vehicles, announced a strategic partnership with Aqua superPower, the world’s leading marine fast-charging network provider. The collaboration aims to accelerate the electrification of marine transportation by combining Taiga’s innovative electric watercraft with Aqua superPower’s expanding global charging infrastructure.

- April 2025 - Yamaha Motor Co., Ltd. announced that its subsidiary, Yamaha Motor Australia Pty Ltd., had signed a purchase agreement with subsidiaries of BRP Inc., Canada, to acquire 100% of the shares of Telwater Pty Ltd., an Australian aluminum boat manufacturer. The completion of the acquisition remains subject to the necessary regulatory approvals, including competition law clearances and related permits.

- July 2024 - Kawasaki, a global leader in PWC innovation, announced the launch of its 2025 Jet Ski line-up, headlined by the introduction of the Ultra 160LX-S Sea Angler. Specifically designed for fishing enthusiasts, the new model will make its U.K. debut and will be available exclusively through Boats.co.uk, Kawasaki’s official distributor in the region.

- June 2024 - Auxilia Networks announced the addition of Jet Ski Safaris, based in Queensland’s Gold Coast, to its client portfolio. Recognized as Australia’s premier provider of water-based soft adventure experiences, Jet Ski Safaris operates the nation’s largest jet ski fleet, further strengthening Auxilia Networks’ presence in the adventure tourism sector.

- November 2023, Taiga Motors Corporation, Canada’s leading electric power sports innovator, announced it as the exclusive PWC supplier for the UIM E1 World Championship, the world’s first all-electric powerboat racing series. This partnership positions Taiga at the forefront of a transformative era in competitive boating, where clean technology and sustainability take center stage.

REPORT COVERAGE

The global personal watercraft market research report provides detailed market analysis and focuses on key aspects such as leading companies, product types, distribution channels, propulsion, and end users. Besides this, the report offers insights into the latest market trends and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors that have contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.51% from 2026 to 2034 |

|

Unit |

Value (USD Billion) & Volume (Thousand Units) |

|

Segmentation |

By Product Type · Rec-Lite · Recreation · Stand-Up · Performance · Luxury/Touring By Distribution Channel · Direct · Indirect Channel By Propulsion · ICE · Electric By End User · Individual User · Rental Operator · Military/Law Enforcements By Region · North America (By Product Type, By Distribution Channel, By Propulsion, and By End User) o U.S. (By Product Type) o Canada (By Product Type) o Mexico (By Product Type) · Europe (By Product Type, By Distribution Channel, By Propulsion, and By End User) o Germany (By Product Type) o France (By Product Type) o U.K. (By Product Type) o Rest of Europe (By Product Type) · Asia Pacific (By Product Type, By Distribution Channel, By Propulsion, and By End User) o China (By Product Type) o Japan (By Product Type) o India (By Product Type) o South Korea (By Product Type) o Rest of Asia Pacific (By Product Type) Rest of the World (By Product Type, By Distribution Channel, By Propulsion, and By End User) |

Frequently Asked Questions

The global personal watercraft market size is projected to grow from USD 1.35 billion in 2026 to USD 2.59 billion by 2034, exhibiting a CAGR of 8.51% during the forecast period.

The market is expected to register a CAGR of 8.51% during the forecast period of 2026-2034.

The increasing global demand for water sports and recreational activities is driving the market growth.

North America leads the global market.

The U.S. leads the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us