PFAS Alternatives Market Size, Share & Industry Analysis, By Chemistry (Silicone-based, Hydrocarbon-based, Acrylic-based, Bio-based, Polyurethane-based, and Others), By End Use (Packaging, Paints & Coatings, Textiles & Apparel, Firefighting, Consumer Goods & Personal Care, Industrial Manufacturing, and Others), and Regional Forecast, 2026-2034

PFAS Alternatives Market Size and Future Outlook

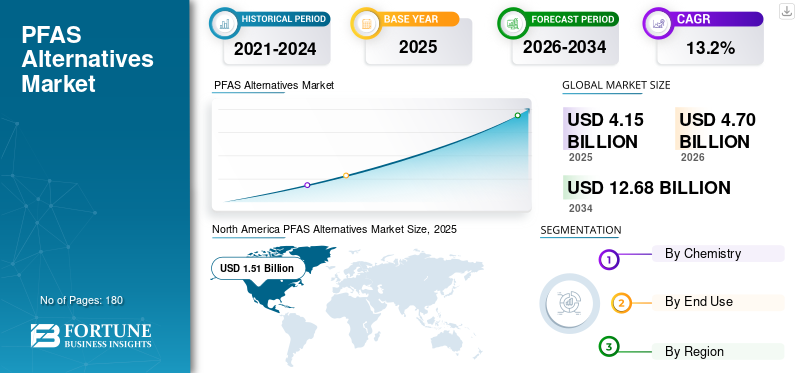

The PFAS alternatives market size was valued at USD 4.15 billion in 2025. The market is projected to grow from USD 4.70 billion in 2026 to USD 12.68 billion by 2034, exhibiting a CAGR of 13.2% during the forecast period. North America dominated the PFAS alternatives market with a market share of 36.38% in 2025.

Per- and Polyfluoroalkyl Substances (PFAS) alternatives are specialty materials, chemistries, and technology platforms designed to replace fluorinated substances used for water, oil, grease, heat, chemical, and stain resistance across multiple industries. These alternatives include fluorine-free surfactants, silicone-based chemistries, hydrocarbon waxes, bio-based coatings, ceramic and sol-gel coatings, plasma surface treatments, and fluorine-free firefighting foams. They are increasingly used in applications including textiles, coatings, firefighting foams, electronics, personal care, consumer goods and food packaging industries, where PFAS phase-out pressures are rising.

The market is being driven by tightening regulatory scrutiny, growing environmental and health concerns linked to persistent “forever chemicals,” and stronger demand from brands and downstream manufacturers for safer, compliant, and more sustainable material systems. Regulatory action in the EU and the U.S., including restrictions on PFAS in firefighting foams and broader PFAS management initiatives, is accelerating the transition toward alternatives.

Specialty chemical companies, coating innovators shape the global market, and fluorine-free technology providers are focused on safer substitution across packaging, textiles, coatings, firefighting foams, and industrial applications. Leading companies operating in the market include Dow, Evonik, Clariant, Ensinger, and Fraunhofer, which offer certified solutions. These players are strengthening their portfolios through PFAS-free coatings, fluorine-free repellents, non-fluorinated surfactants, and alternative barrier technologies to meet rising regulatory and customer demand.

Download Free sample to learn more about this report.

PFAS ALTERNATIVES MARKET TRENDS

Shift toward Fluorine-Free Chemistries is Prominent Market Trend

The market is witnessing a strong shift toward fluorine-free chemistries as manufacturers across packaging, textiles, coatings, firefighting, and consumer goods reduce dependence on persistent fluorinated substances. Companies are increasingly developing silicone-based, acrylic-based, hydrocarbon-based, polyurethane-based, and bio-based alternatives that can deliver water resistance, grease resistance, surface protection, and durability without long-term environmental persistence. This trend is particularly visible in food packaging and apparel, where brand owners are under pressure to meet sustainability commitments and avoid future compliance risks. As a result, product innovation is moving from simple chemical replacement toward application-specific performance engineering, enabling suppliers to create safer formulations tailored to each end-use requirement, thus driving product demand.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Tightening PFAS Regulations and Rising Environmental Awareness are Expected to Drive Market Growth

Tightening PFAS regulations across North America, Europe, and other major markets is becoming a primary driver for PFAS alternatives market growth. Stricter compliance requirements and rising preference for environmentally friendly materials are expected to accelerate large-scale substitution over time. Governments across major economies are increasingly restricting the use of PFAS in food-contact packaging, firefighting foams, textiles, cosmetics, coatings, and consumer products due to various health concerns over their persistence, bioaccumulation, and potential health impacts. This is pushing manufacturers and brand owners to replace fluorinated chemistries with safer alternatives such as silicone-based, acrylic-based, hydrocarbon-based, bio-based, and other fluorine-free solutions. In addition, growing consumer awareness around “forever chemicals” is encouraging companies to reformulate products, strengthen sustainability claims, and reduce long-term liability risks. Therefore, stricter compliance requirements and rising preference for environmentally responsible materials are expected to drive the market growth over the forecast period.

- The EU is acting heavily via a horizontal approach (banning the whole group) under REACH, while the U.S. is using a combination of environmental law (CERCLA) and chemical management (TSCA) to target high-priority PFAS.

MARKET RESTRAINTS

Higher Reformulation Costs and Validation Complexity Slowing Commercial Adoption

Higher reformulation costs and technical validation requirements remain key restraints for the market. PFAS chemistries have historically offered a unique combination of oil repellency, water resistance, chemical stability, heat resistance, and durability, making direct replacement difficult in several high-performance applications. Alternative materials often require extensive testing to confirm performance, safety, processing compatibility, durability, and regulatory acceptance before commercial use. This increases development timelines and raises costs for manufacturers, especially in coatings, industrial manufacturing, electronics, and firefighting applications. In addition, some alternatives may need equipment adjustments or multi-chemistry systems to achieve comparable results. Hence, adoption can be slower where performance failure carries operational, safety, or compliance risks.

MARKET OPPORTUNITIES

Growing Scope for Bio-Based and Green Chemistry Alternatives in Packaging and Textiles Creates Lucrative Opportunities

Bio-based and green chemistry alternatives are creating strong opportunities in the market, particularly across packaging and textiles. Food packaging producers are actively seeking renewable and safer barrier materials that can provide grease, oil, and moisture resistance without fluorinated additives. Similarly, apparel and technical textile manufacturers are adopting fluorine-free durable water repellent finishes to meet brand sustainability goals and consumer preference for safer products. Innovations in plant-based coatings, bio-waxes, polysaccharide-based barriers, silicone hybrids, and other low-toxicity chemistries are expanding the commercial scope of PFAS replacement. Therefore, suppliers that can balance performance, cost, composability, and regulatory compliance are expected to capture attractive growth opportunities in the coming years.

Segmentation Analysis

By Chemistry

Silicone-based Alternatives Dominate the Market Owing to Strong Performance in Repellency and Surface Protection Applications

Based on chemistry, the market is segmented into silicone-based, hydrocarbon-based, acrylic-based, bio-based, polyurethane-based, and others.

Silicone-based alternatives account for the largest share of the market, due to their strong water repellency, thermal stability, flexibility, and compatibility with coatings, textiles, personal care, packaging, and industrial surface treatment applications. These materials are increasingly preferred where formulators need non-fluorinated solutions with reliable durability and safer compliance positioning. Their use in barrier coatings, release agents, sealants, and protective finishes continues to expand as manufacturers move away from legacy PFAS chemistries.

Bio-based PFAS alternatives are emerging as one of the fastest-growing as brands, packaging converters, textile manufacturers, and coating formulators prioritize renewable and lower-toxicity materials. These alternatives are gaining traction in food-contact packaging, paper coatings, textiles, and consumer-facing products where sustainability claims and regulatory compliance strongly influence material selection. Although performance optimization remains important, bio-based chemistries are benefiting from rising investment in green chemistry platforms and circular material innovation, driving their demand at a CAGR of 14.9% during 2026–2034.

The others segment includes emerging and application-specific alternatives such as ceramic coatings, sol-gel systems, plasma treatments, wax blends, specialty additives, and hybrid non-fluorinated technologies. These solutions are often developed for niche applications where conventional replacement chemistries may not fully meet end-use performance needs. Demand is supported by innovation in electronics, industrial processing, high-barrier coatings, and specialized surface modification technologies. The segment is anticipated to grow at a CAGR of 11.6% during the forecast period as it remains important for customized substitution strategies.

By End Use

Packaging Leads Owing to Accelerated PFAS Phase-Out in Food-Contact and Consumer Packaging

Based on end use, the market is segmented into packaging, paints & coatings, textiles & apparel, firefighting, consumer goods & personal care, industrial manufacturing, and others.

To know how our report can help streamline your business, Speak to Analyst

Packaging accounted for the largest PFAS alternatives market share in 2025, supported by rapid substitution of fluorinated grease and water-resistant coatings in food packaging, molded fiber products, paper wraps, disposable containers, and consumer packaging formats. Brand owners, packaging converters, and foodservice companies are increasingly shifting toward silicone-based, acrylic-based, hydrocarbon-based, and bio-based barrier systems to meet regulatory and retailer requirements. As packaging remains one of the most visible and highly regulated PFAS exposure areas, demand for safer alternatives is expected to remain strong.

Textiles and apparel are emerging as one of the most dynamic end-use areas, driven by the replacement of PFAS-based durable water repellent finishes in outdoor wear, sportswear, uniforms, upholstery, footwear, and technical fabrics. Manufacturers are increasingly adopting fluorine-free repellents, silicone-based treatments, wax systems, and bio-based finishes to maintain water resistance while improving sustainability positioning. The segment is also benefiting from brand-level chemical restrictions and consumer preference for safer apparel materials, driving the segment’s growth at a CAGR of 14.3%.

Firefighting is a critical substitution area for PFAS alternatives, particularly due to the phase-out of aqueous film-forming foams containing fluorinated surfactants. Airports, defense facilities, industrial plants, municipal fire departments, oil & gas sites, and emergency-response agencies are increasingly transitioning toward fluorine-free foam systems. However, adoption requires performance validation, equipment compatibility checks, and training adjustments, which can moderate the replacement pace in some high-risk environments. Hence, the segment is projected to register a CAGR of 12.0% from 2026 to 2034.

PFAS Alternatives Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America and the Middle East & Africa.

Asia Pacific

North America PFAS Alternatives Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific reached USD 1.12 billion in 2025, growing at the fastest regional CAGR of 13.9% through 2034. The region’s growth is supported by expanding manufacturing activity, rising export-driven compliance requirements, and increasing adoption of PFAS-free materials across packaging, textiles, electronics, coatings, and industrial applications. China and India are emerging as major demand centers as global brands and regulators push supply chains toward safer chemical systems. In addition, large-scale textile production, packaging conversion, and industrial manufacturing capacity across the Asia Pacific are creating strong opportunities for alternative chemistries.

China PFAS Alternatives Market

China accounted for approximately USD 0.69 billion in 2026, representing around 14.7% of global sales. The country’s position is supported by its large packaging, textile, coatings, electronics, and consumer goods manufacturing base. As export-oriented manufacturers face stricter PFAS-related requirements from North America and Europe, demand for compliant fluorine-free alternatives is increasing across both consumer-facing and industrial applications.

To know how our report can help streamline your business, Speak to Analyst

India PFAS Alternatives Market

India market is predicted to reach USD 0.10 billion in 2026, contributing nearly 2.2% of global revenues. Market growth is being supported by expanding packaging consumption, textile production, personal care manufacturing, and industrial coatings demand. While adoption remains at an earlier stage compared to China, India is expected to benefit from rising regulatory awareness, multinational brand sourcing requirements, and increasing demand for safer material substitutes in export-linked industries.

North America

North America held the largest share with market value worth USD 1.51 billion in 2025, growing at a CAGR of 12.6% through 2034. The region represents largest demand base for the market, supported by stricter regulatory action, rising litigation pressure, and early substitution across packaging, textiles, firefighting foams, coatings, and consumer products. Demand is particularly strong in food-contact packaging and fluorine-free firefighting foam applications, where federal and state-level restrictions are accelerating reformulation. The presence of large chemical companies, consumer brands, and packaging converters further supports faster adoption of PFAS-free solutions across commercial applications.

U.S. PFAS Alternatives Market

The U.S. market will account for approximately USD 1.47 billion in 2026, representing around 31.3% of global sales. The country remains the single largest market globally, driven by state-level PFAS bans, retailer-led chemical restrictions, and growing adoption of PFAS-free alternatives in food packaging, apparel, firefighting, cosmetics, and industrial products.

Europe

Europe reached USD 1.25 billion in 2025, expanding at a CAGR of 13.6% over the forecast period. The region is one of the most regulation-driven markets for PFAS alternatives, with demand supported by broad PFAS restriction proposals, chemical safety policies, and strong sustainability targets across packaging, textiles, coatings, and consumer goods. European Union manufacturers are increasingly replacing fluorinated substances with silicone-based, bio-based, acrylic, and hydrocarbon-based alternatives to meet compliance requirements and brand-level chemical management standards.

Germany PFAS Alternatives Market

Germany will reach nearly USD 0.22 billion in 2026, accounting for around 4.7% of global demand. Growth is supported by the country’s strong industrial manufacturing base, coatings sector, automotive supply chain, packaging industry, and regulatory focus on safer chemical alternatives. German manufacturers are increasingly adopting PFAS-free materials in industrial coatings, engineered components, consumer packaging, and textile finishing applications to align with EU chemical transition goals.

U.K. PFAS Alternatives Market

The U.K. market stood at approximately USD 0.11 billion in 2026, representing around 2.3% of global revenues. Demand is being supported by rising awareness around persistent chemicals, retailer sustainability requirements, and gradual reformulation across packaging, cosmetics, textiles, and consumer goods.

Latin America

Latin America reached USD 0.16 billion in 2025 and expected to grow with a CAGR of 12.0% over the forecast period. The region represents a developing but gradually expanding market for PFAS alternatives, with demand concentrated in packaging, consumer goods, textiles, coatings, and selected industrial applications. Adoption is being shaped more by multinational brand compliance and export-market requirements than by highly advanced domestic PFAS regulations. However, increasing awareness of safer chemicals and sustainable packaging is expected to support steady regional growth.

Brazil PFAS Alternatives Market

Brazil is expected to reach USD 0.07 billion in 2026, representing around 1.5% of global sales. The country is the leading Latin American market, supported by its sizable packaging, personal care, consumer goods, textile, and industrial manufacturing base. Demand for PFAS alternatives is expected to rise as domestic producers align with global brand standards and sustainability-linked product requirements.

Middle East & Africa

The Middle East & Africa reached USD 0.11 billion in 2025, expanding at a CAGR of 11.7% through 2034. The region currently holds a smaller share of the market, with demand primarily linked to industrial manufacturing, oil & gas safety applications, firefighting foams, packaging, and construction-related coatings. Adoption is comparatively gradual due to lower regulatory pressure. Still, opportunities are emerging as airports, industrial facilities, and multinational companies begin shifting toward fluorine-free foam systems and safer material alternatives.

COMPETITIVE LANDSCAPE

Key Industry Players

Material Innovation and Strategic Partnerships Are Reshaping Competitive Positioning

The PFAS alternatives market is moderately fragmented, with competition shaped by specialty chemical expertise, application-specific formulation capabilities, and regulatory-compliant product development. Leading players globally include Dow, Evonik, Clariant, Ensinger, and Fraunhofer, supported by several emerging suppliers focusing on fluorine-free coatings, repellents, polymer processing aids, and firefighting foams. Companies are increasingly adopting strategies such as PFAS-free product launches, portfolio reformulation, green chemistry investments, partnerships with packaging and textile converters, and expansion of fluorine-free foam solutions. Innovation is mainly focused on matching PFAS-like performance in grease resistance, water repellency, durability, processing efficiency, and fire suppression while reducing environmental persistence. As regulatory pressure intensifies, investments in bio-based chemistries, silicone-based systems, acrylic alternatives, and non-fluorinated surfactants are reshaping competitive positioning and accelerating substitution across packaging, textiles, coatings, and industrial applications.

LIST OF KEY PFAS ALTERNATIVES COMPANIES PROFILED

- Archroma (Switzerland)

- Clariant (Switzerland)

- Dow (U.S.)

- Ensinger (Germany)

- Evonik (Germany)

- Fraunhofer (Germany)

- Kemira Oyj (Finland)

- Oerlikon (Switzerland)

- Solenis (U.S.)

- Victrex (U.K.)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Taplin Group secured a contract worth approximately USD 0.11 million from MBS International Airport for PFAS decontamination and transition support from AFFF systems to fluorine-free firefighting foam. The project includes the supply of 680 gallons of fluorine-free foam and testing of firefighting vehicles to meet FAA requirements.

- November 2025: Rely FX released the P2.5SFFF fluorine-free portable foam fire extinguisher, using NUFOAM, a PFAS-free foam agent solution for Class A and Class B fire suppression. The product is positioned to support portable fire-safety applications as users shift away from PFAS-containing foam systems.

- September 2025: INX International and Impermea Materials partnered to scale the distribution of OLEO-PAK 4100, a PFAS-free and plastic-free coating for recyclable and compostable food packaging. The collaboration is intended to expand access to sustainable barrier coatings across INX’s packaging network.

- June 2025: Clariant launched its AddWorks PPA product line, a new generation of PFAS-free polymer processing aids for polyolefin extrusion applications. The solution is designed to replace conventional fluoropolymer-based processing aids while supporting melt fracture control, extrusion efficiency, and film quality in food-contact and packaging applications.

- April 2025: Perimeter Solutions introduced SOLBERG SPARTAN 1% Fluorine-Free Class A/B Foam Concentrate at FDIC 2025 in the U.S. The product is designed for broad fire scenarios, including structure, wildland, vehicle, gasoline, and dumpster fires, strengthening the company’s fluorine-free foam portfolio.

REPORT COVERAGE

The PFAS Alternatives market analysis provides an in-depth study of market size & forecast across all market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 13.2% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Chemistry, End Use, and Region |

| By Chemistry |

|

| By End Use |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 4.15 billion in 2025 and is projected to reach USD 12.68 billion by 2034.

In 2025, Asia Pacific’s market value stood at USD 1.12 billion.

Recording a CAGR of 13.2%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The packaging end use segment is leading in the market.

Tightening global PFAS regulations and rising environmental awareness are driving the market growth.

Dow, Evonik, Clariant, Ensinger, and Fraunhofer are some of the prominent players in the market.

North America held the highest market share in 2025.

Shift toward fluorine-free chemistries is expected to favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us