Pharmaceutical Cold Chain Packaging Market Size, Share & Industry Analysis, By Material (Plastic, Paper & Paperboard, Metal, and Others), By Type (Active and Passive), By Product Type (Shippers & Containers, Boxes, Refrigerants & Coolants, and Others), By Application (Biopharmaceutical Companies, Clinical Research Organizations, Hospitals, Logistics & Distribution Companies, and Others), and Regional Forecast, 2026-2034

Pharmaceutical Cold Chain Packaging Market Size and Future Outlook

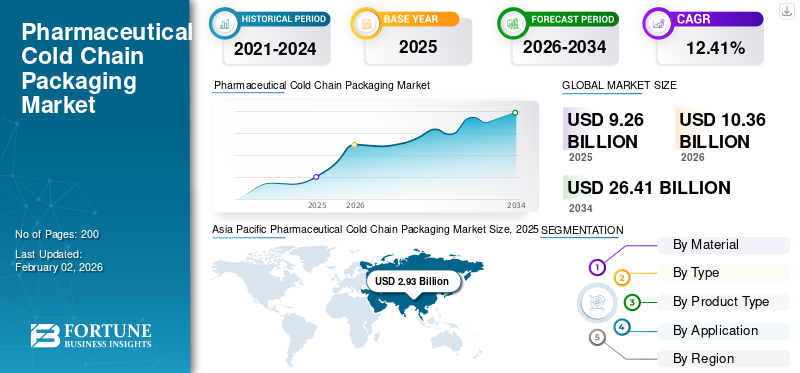

The global pharmaceutical cold chain packaging market size was valued at USD 9.26 billion in 2025 and is projected to grow from USD 10.36 billion in 2026 to USD 26.41 billion by 2034, exhibiting a CAGR of 12.41% during the forecast period. Asia Pacific dominated the pharmaceutical cold chain packaging market with a market share of 31.70% in 2025.

Pharmaceutical cold chain packaging pertains to specialized packaging solutions that are engineered to sustain controlled temperature conditions for temperature-sensitive pharmaceutical products such as vaccines, biologics, insulin, blood plasma, and specific diagnostic reagents during storage and transportation. Regulatory bodies such as the U.S. FDA, EMA, and WHO mandate strict compliance with Good Distribution Practices (GDP) for the transportation of pharmaceuticals. Cold chain packaging solutions that ensure ongoing temperature validation and traceability assist companies in upholding regulatory compliance and preventing expensive recalls or product rejections, thereby enhancing market expansion.

Furthermore, the market encompasses several key players, Sonoco ThermoSafe, Cold Chain Technologies, and Sealed Air, at the forefront. A broad portfolio with innovative product launches, and strong geographic presence expansion have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

Pharmaceutical Cold Chain Packaging Market KEY TAKEAWAYS

- 2025 Market Size: USD 9.26 Billion

- 2026 Market Size: USD 10.36 Billion

- 2034 Forecast Market Size: USD 26.41 Billion

- CAGR: 12.41% from 2026–2034

- Asia Pacific dominated the pharmaceutical cold chain packaging market with a 31.70% share in 2025.

- The plastic segment is projected to account for 43.24% of the market in 2026.

- The passive segment is expected to hold a 58.40% market share in 2026.

Asia Pacific

Asia Pacific accounted for USD 2.93 billion in 2025 and is projected to reach USD 3.31 billion in 2026.

North America

North America generated USD 2.29 billion in 2025 and is expected to reach USD 2.57 billion in 2026.

Europe

Europe reached USD 1.86 billion in 2025 and is projected to grow to USD 2.08 billion in 2026.

U.S.

The pharmaceutical cold chain packaging market is estimated to reach USD 2.02 billion by 2026.

Japan

The pharmaceutical cold chain packaging market is estimated to reach USD 0.62 billion by 2026

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Biopharmaceuticals and Temperature-Sensitive Drugs Drives Market Growth

The expansion of the global pharmaceutical cold chain packaging market is chiefly influenced by the rising demand for biopharmaceuticals, vaccines, and specialty medications that necessitate stringent temperature regulation during both storage and transportation. The growth of biologics, which includes monoclonal antibodies, cell and gene therapies, and insulin, has increased the necessity for dependable cold chain packaging solutions to ensure the efficacy and safety of these drugs. Moreover, the continuous vaccination initiatives and the increase in clinical trials for temperature-sensitive products in emerging markets further stimulate demand.

The heightened emphasis on patient safety and the rigorous regulatory standards set by agencies such as the FDA and EMA have also motivated pharmaceutical companies to invest in sophisticated, validated cold chain packaging systems, further driving the global pharmaceutical cold chain packaging market growth.

MARKET RESTRAINTS

High Costs and Complex Supply Chain Infrastructure May Hamper Market Growth

Despite the considerable growth potential, the market encounters limitations stemming from the substantial expenses associated with cold chain infrastructure and packaging materials. Ensuring temperature-controlled conditions over extended distances requires a significant capital outlay for insulated containers, Phase Change Materials (PCMs), refrigerated transportation, and real-time monitoring systems. Additionally, developing economies often lack sufficient cold chain logistics infrastructure, which can lead to difficulties in maintaining product integrity. The operational complexities, along with elevated energy consumption and the necessity for skilled personnel, further restrict the broad implementation of advanced cold chain packaging solutions.

MARKET OPPORTUNITIES

Technological Advancements and Sustainable Packaging Solutions Create Development Opportunities

The advent of new technologies in cold chain packaging, such as tracking systems enabled by IoT, temperature sensors, and data loggers, offers significant opportunities for market growth. These advancements improve visibility and traceability across the supply chain, ensuring compliance and minimizing product losses. Additionally, the growing focus on sustainability is driving the development of environmentally friendly packaging materials, including recyclable and reusable insulated shippers. Businesses are concentrating on the development of phase-change materials that have a low environmental footprint and high thermal efficiency, thereby creating opportunities for differentiation and expansion in the changing landscape of green packaging. Thus, implementation of technologies such as vacuum insulated panels, temperature controlled packaging solutions, and others also offers potential opportunities.

MARKET CHALLENGES

Regulatory Compliance and Risk of Product Degradation Pose Major Obstacles to Market Growth

One significant challenge facing the pharmaceutical cold chain packaging market is the need to comply with various international regulatory standards. The differing guidelines across regions concerning temperature monitoring, packaging validation, and transportation introduce complexities for global pharmaceutical manufacturers. Moreover, any disruption in the cold chain, whether caused by equipment malfunction, human error, or logistical delays, can result in irreversible product degradation and financial losses. The necessity for ongoing temperature validation and documentation imposes additional operational challenges for stakeholders throughout the value chain.

PHARMACEUTICAL COLD CHAIN PACKAGING MARKET TRENDS

Integration of Smart Packaging and Digital Cold Chain Monitoring Emerges as a Market Trend

A significant trend influencing the market is the swift incorporation of digital technologies into cold chain packaging systems. The implementation of smart packaging featuring embedded sensors, RFID tags, and cloud-based monitoring platforms facilitates real-time temperature monitoring and predictive analytics. This digital transformation not only improves supply chain transparency but also minimizes spoilage risks and facilitates regulatory compliance. Furthermore, the market is experiencing a transition toward lightweight, reusable, and modular packaging designs that maximize space and lower shipping expenses. Strategic partnerships between pharmaceutical firms and logistics providers are additionally fostering the uptake of intelligent, data-driven cold chain packaging systems.

Download Free sample to learn more about this report.

Segmentation Analysis

By Material

Notable Benefits Offered by Plastic Material Propel Segment Growth

In terms of material, the market is categorized into plastic, paper & paperboard, metal, and others.

In 2025, the plastic segment is set to capture the largest market share and will dominate in 2026 with a 43.24% share. Plastic materials are crucial for the pharmaceutical cold chain packaging market growth, due to their remarkable durability, insulation capabilities, and cost-effectiveness. Polypropylene (PP), Polyethylene (PE), Polyurethane (PU), and Expanded Polystyrene (EPS) are commonly utilized in insulated containers, boxes, and pallet shippers due to their lightweight characteristics and excellent thermal resistance. These materials assist in preserving stable internal temperatures throughout extended transportation, while also decreasing the total shipping weight, thereby lowering logistics expenses.

The paper & paperboard material segment is expected to grow at a CAGR of 12.23% over the forecast period.

By Type

Noteworthy Characteristics of Passive Cold Chain Solutions Boost the Segment’s Growth

In terms of type, the market is categorized into active and passive.

The passive segment dominated in 2025 and will lead the market in 2026 with a 58.40% market share. Passive cold chain solutions are experiencing significant growth in the pharmaceutical cold chain packaging sector, attributed to their ease of use, cost efficiency, and dependability in sustaining controlled temperatures without requiring external power sources. These systems employ insulated containers, Phase Change Materials (PCMs), dry ice, or gel packs to maintain temperature control over prolonged durations, rendering them suitable for short- to medium-distance shipments and regions with inadequate infrastructure. Their self-sufficient design guarantees consistent thermal performance even in difficult conditions, thereby minimizing reliance on active refrigeration systems.

The active segment is expected to grow at a CAGR of 12.98% during the forecast period.

By Product Type

Rising Usage of Shippers & Containers in Pharmaceutical Sector Propels Segment Growth

In terms of product type, the market is categorized into shippers & containers, boxes, refrigerants & coolants, and others.

The shippers and containers segment attained a leading market share and will sustain its position in 2026 with a 46.81% share. The rising utilization of shippers and containers within the pharmaceutical industry is significantly propelling the market’s expansion. Shippers and containers are essential in preserving product integrity while transporting temperature sensitive pharmaceuticals, including vaccines, biologics, blood products, and clinical trial samples. These solutions are meticulously engineered to sustain stable internal temperatures over extended transit periods, guaranteeing that medications stay within the necessary temperature range from their point of origin to their final destination.

The boxes segment is expected to grow at a CAGR of 12.22% over the forecast period.

By Application

Escalating Demand for Cold Chain Packages from the Clinical Research Organizations Propelled Segmental Growth

Based on application, the market is segmented into biopharmaceutical companies, clinical research organizations, hospitals, logistics & distribution companies, and others.

To know how our report can help streamline your business, Speak to Analyst

Clinical research organizations was the leading segment in 2025 and will continue leading in 2026 with a 43.44% share. The increasing demand for cold chain packaging solutions among Clinical Research Organizations (CROs) has emerged as a significant factor driving growth in the pharmaceutical cold chain packaging sector. As the global landscape of clinical research develops especially in areas such as biologics, vaccines, and personalized medicine, CROs are taking on more responsibility for the storage and transportation of temperature-sensitive clinical trial materials, which include investigational medications, biological specimens, and diagnostic agents. It is essential to preserve the integrity of these materials, as any shift in temperature can compromise the results of trials and the regulatory approval processes.

In addition, the biopharmaceutical company application is projected to grow at a CAGR of 12.42% during the study period.

Pharmaceutical Cold Chain Packaging Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Pharmaceutical Cold Chain Packaging Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

Asia Pacific contributed 31.70% to the global market in 2025, with a valuation of USD 2.93 billion, and is projected to reach USD 3.31 billion in 2026. The region dominated the global pharmaceutical cold chain packaging industry with the expansion of pharmaceutical manufacturing in China, India, Japan, and South Korea. Strong emphasis on the production of biologics, the distribution of vaccines, and the export-oriented pharmaceutical trade is increasing demand for cold chain packaging solutions. Furthermore, governments are progressively allocating resources toward enhancing healthcare infrastructure and developing temperature-controlled logistics networks.

In 2026, India and China are estimated to reach USD 0.89 and USD 1.08 billion respectively. The Japan market is estimated to reach USD 0.62 billion in 2026.

North America

In 2025, North America represented USD 2.29 billion, accounting for 24.75% of the worldwide market, and is projected to grow to USD 2.57 billion in 2026. North America and Europe are anticipated to witness a notable growth in the coming years. During the forecast period, North America is projected to record the second highest growth rate of 12.44%, and reach USD 2.29 billion in 2025. The region is experiencing the most rapid growth, propelled by its robust biopharmaceutical production capabilities and sophisticated cold chain infrastructure. The U.S. is at the forefront of the global implementation of temperature-sensitive therapies, such as biologics, vaccines, and cell and gene therapies, which require reliable and validated cold chain packaging systems. In 2026, the U.S. market is estimated to reach USD 2.02 billion.

Europe

Following North America, Europe market generated USD 1.86 billion in 2025, representing 20.09% of the global market landscape, and is expected to reach USD 2.08 billion in 2026. Europe constitutes a major market influenced by stringent environmental and pharmaceutical regulations. The European Medicines Agency (EMA) requires strict adherence to temperature-controlled logistics, compelling companies to implement sophisticated insulated shippers and reusable cold chain packaging.

Backed by these factors, in 2026, the U.K. is expected to generate a revenue of USD 0.4 billion, while Germany and France will set a market size of USD 0.46 billion in 2026 and 0.29 billion in 2025 respectively.

Latin America

Latin America and the Middle East & Africa will witness a moderate growth. The market in Latin America reached USD 1.35 billion in 2025, representing 14.55% of total market revenue, and is projected to reach USD 1.49 billion in 2026, fueled by enhanced access to healthcare, the expansion of vaccination initiatives, and the importation of temperature-sensitive medications. Brazil and Mexico are experiencing a surge in pharmaceutical trade, which is generating a need for cold chain packaging solutions.

Middle East & Africa

The Middle East & Africa market was valued at USD 0.82 billion in 2025, capturing 8.91% of global revenue, and is estimated to reach USD 0.91 billion in 2026. The Middle East and Africa (MEA) is currently in the initial phase of enhancing its cold chain capabilities; however, it possesses significant potential owing to the increasing demand for temperature sensitive products, vaccines, biologics, and imported pharmaceuticals.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies Maintain their Position with Product Offerings and Strong Distribution Networks

The global pharmaceutical cold chain packaging industry exhibits a semi-concentrated structure, with numerous small- to mid-size companies actively operating across the globe. These players are actively involved in product innovation, strategic partnerships, and geographic expansion.

Sonoco ThermoSafe, Cold Chain Technologies, and Sealed Air are some of the dominating players in the market. A comprehensive range of unit-dose packaging products, global presence through a strong distribution network, and collaborations with research and academic institutes are a few characteristics that support the dominance of these players.

Apart from this, other prominent players in the market include Insulated Products Corporation, CSafe Global LLC, and DGP Intelsius Ltd. These companies are undertaking various strategic initiatives, such as investments in R&D and partnerships with pharmaceutical companies to enhance their market presence.

LIST OF KEY PHARMACEUTICAL COLD CHAIN PACKAGING COMPANIES PROFILED

- Sonoco ThermoSafe (U.S.)

- Cold Chain Technologies (U.S.)

- Sealed Air (U.S.)

- Insulated Products Corporation (U.S.)

- CSafe Global LLC (U.S.)

- DGP Intelsius Ltd. (U.K.)

- Inmark Global Holdings, LLC (U.S.)

- Pelican BioThermal LLC (U.S.)

- Cryopak (U.S.)

- Envirotainer AB (Sweden)

- va-Q-tec AG (Germany)

- TemperPack Technologies, Inc. (U.S.)

- CoolPac (Australia)

- TempAid Cold Chain Packaging (Canada)

- Cold Chain Packing & Logistics Ltd. (Saudi Arabia)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Nordic Cold Chain Solutions introduced the Nordic Express Pack, a tailored solution for pharmaceutical cold chain packaging designed to ensure safe and effective transport of GLP-1 medications. This specialized solution is intended to address the growing demand for accurate thermal control when shipping advanced therapies within the healthcare supply chain. GLP-1 medications, widely used for diabetes treatment and weight management, necessitate stringent temperature regulation during transportation to preserve stability and adhere to strict pharmaceutical regulations.

- August 2025: Celcius Logistics unveiled Celcius+, a dedicated logistics branch aimed specifically at the pharmaceutical supply chain. The firm stated that Celcius+ will tackle the challenges of temperature regulation, regulatory compliance, and the need for real-time visibility for medications, vaccines, and other delicate products. According to the company, Celcius+ will utilize its technology platform to offer real-time tracking, ongoing temperature monitoring, and AI-driven route optimization.

- March 2025: Cold Chain Technologies, a worldwide supplier of innovative thermal packaging and digital monitoring solutions for the transport of temperature-sensitive life sciences products, announced the purchase of Global Cold Chain Solutions, a company that offers passive cold chain solutions mainly in Australia and India. GCCS specializes in designing and producing high-performance thermal assurance solutions for a wide range of life sciences applications.

- February 2025: UPS Healthcare revealed the establishment of three specialized cross-docking facilities within its worldwide logistics network, strategically positioned in Milan, Frankfurt, and Mexico City. These facilities aim to cater to the specific logistical requirements of the healthcare sector, especially for pharmaceutical shipments that are sensitive to time and temperature. This expansion reinforces UPS Healthcare's dedication to developing strong and efficient global supply chains.

- October 2024: Peli BioThermal, a company focused on temperature-sensitive packaging, introduced Crēdo Vault, an innovative bulk shipping solution designed specifically for the pharmaceutical and life sciences industries. This offering seeks to improve cold chain logistics by delivering dependable thermal performance and real-time monitoring for shipments. The Crēdo Vault aims to tackle the typical issues customers encounter, such as preserving product quality and lowering shipping expenses.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 12.41% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Material

By Type

By Product Type

By Application

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 10.36 billion in 2026 and is projected to reach USD 26.41 billion by 2034.

In 2025, Asia Pacific reached a market value of USD 2.93 billion.

The market is expected to exhibit a CAGR of 12.41% during the forecast period of 2026-2034.

The shippers and containers segment led the market by product type.

The key factor driving the market growth is the rising demand for biopharmaceuticals and temperature-sensitive drugs.

Sealed Air, Mondi, Pregis Corporation, Smurfit Kappa, DS Smith, and ProAmpac are some of the prominent players in the market.

Asia Pacific dominated the market in 2025 by holding the largest share.

Augmenting demand from the pharmaceutical sector is one of the factors expected to favor the product adoption.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us