Cold Chain Packaging Market Size, Share & Industry Analysis, By Service Type (Refrigerated Transportation and Refrigerated Warehousing), By Temperature Range (Chilled [8°C to 0°C], Frozen [0°C to -25°C], and Deep Frozen [Below -25°C]), By Product Type (EPS Containers, PUR Containers, Pallet Shippers, Vacuum Insulated Panels, and Others), By End-use Industry (Pharmaceuticals, Food, and Industrial), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

KEY MARKET INSIGHTS

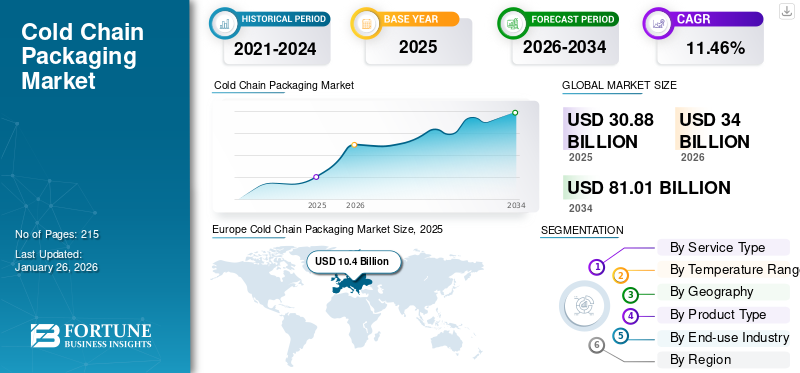

The global cold chain packaging market size was valued at USD 30.88 billion in 2025. It is projected to grow from USD 34.00 billion in 2026 and to USD 81.01 billion by 2034, exhibiting a CAGR of 11.46% during the forecast period. Europe dominated the cold chain packaging market with a market share of 33.68% in 2025.

Cold chain packaging refers to specialized solutions designed to maintain the temperature of sensitive products throughout the supply chain. This is essential for preserving the quality and efficacy of perishable goods, including vaccines, fresh produce, and biologics.

Sancell and Cold Chain Technologies are leading cold chain packaging manufacturers, holding the largest global cold chain packaging market share.

Download Free sample to learn more about this report.

Cold Chain Packaging Market Key Takeaways

- 2025 Market Size: USD 30.88 billion

- 2026 Market Size: USD 34.00 billion

- 2034 Forecast Market Size: USD 81.01 billion

- CAGR: 11.46% from 2026–2034

- Europe dominated the cold chain packaging market with a 33.68% share in 2025.

- Refrigerated transportation accounted for a 71.66% market share in 2026.

- Frozen food held a 43.83% market share in 2026.

Europe

Europe remained the leading regional market, reaching USD 10.4 billion in 2025 and projected to grow to USD 11.47 billion in 2026.

Asia Pacific

Asia Pacific accounted for 30.32% of global demand in 2025, with the market projected to reach USD 10.55 billion in 2026.

North America

North America reached USD 6.83 billion in 2025 and is projected to grow to USD 7.23 billion in 2026.

U.S.

The market is projected to reach USD 7.23 billion by 2026.

Japan

The market is projected to reach USD 2.71 billion by 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Increasing Demand for Pharmaceuticals and Biologics Industry Propels Market Growth

The global cold chain packaging market growth is significantly driven by the increasing demand for pharmaceuticals and biologics that require temperature-sensitive transportation. The rapid growth of the biopharmaceutical industry, along with the proliferation of biologics and specialty drugs, has increased the need for reliable cold-chain logistics. Biologics, vaccines, and certain pharmaceuticals are highly sensitive to temperature variations and can lose efficacy or become harmful if exposed to unsuitable conditions. This necessitates specialized packaging solutions that can maintain consistent temperatures throughout the logistics process.

Growth in the Global Food and Beverage Industry Enhances Market Growth

The growth of the global food and beverage industry, particularly in frozen foods, dairy, and fresh produce, drives the market. As consumer lifestyles change, there has been a notable increase in demand for ready-to-eat meals, frozen foods, and other perishable items that require temperature-controlled storage and transportation. Urbanization, rising disposable incomes, and an increasing preference for convenient food options have further fueled this demand, especially in developing regions where cold chain infrastructure is rapidly improving.

MARKET RESTRAINTS

High Costs Associated with Cold Chain Packaging Hampers Market Growth

One of the primary restraints in the market is the high cost associated with the development, production, and operation of temperature-controlled packaging solutions. It involves advanced materials and technologies, such as vacuum insulation panels, phase-change materials, and IoT-enabled sensors, which significantly increase production costs. Additionally, maintaining the infrastructure required for cold chain logistics, such as refrigerated trucks, warehouses, and monitoring systems, further adds operational expenses for businesses.

MARKET OPPORTUNITIES

Utilization of Sustainable Packaging Service Types Will Generate Growth Opportunities

Pharmaceutical companies are increasingly utilizing recyclable and biodegradable plastics for vials to reduce environmental impact. Biodegradable plastics decompose in three to six months faster than traditional plastic, which takes hundreds of years. Several biodegradable plastics such as Polylactic acid (PLA), recycled plastics such as R-PET recycled HDPE, and various others are used for the manufacturing of vials, generating potential growth opportunities in the forthcoming years.

MARKET CHALLENGES

Supply Chain Disruptions and Temperature Excursions Challenge Market Growth

Maintaining the integrity of cold chain logistics is a challenging task, particularly in the face of supply chain disruptions. Factors such as transportation delays, infrastructure failures, and unpredictable weather conditions can result in temperature excursions, compromising the quality and safety of temperature-sensitive products. These disruptions can lead to significant financial losses, especially in industries such as pharmaceuticals, where biologics and vaccines are highly valuable.

Download Free sample to learn more about this report.

MARKET TRENDS

Integration of Smart and IoT-Enabled Packaging Emerges as a Key Trend

Smart and IoT-enabled packaging presents significant opportunities in the market. The growing need for real-time monitoring and supply chain visibility has driven the adoption of connected solutions. Smart packaging technologies, such as temperature sensors, RFID tags, and data loggers, allow stakeholders to monitor environmental conditions throughout the supply chain. This ensures the integrity of temperature-sensitive goods and helps companies comply with stringent regulatory requirements.

IMPACT OF TRADE PROTECTIONISM

Trade protectionism, characterized by tariffs, import restrictions, and other barriers, can significantly affects the market. These measures may lead to increased cost-effectiveness for raw materials and finished products, disrupt supply chains, and create uncertainties in international trade. Companies may need to adapt by localizing production, diversifying suppliers, or investing in alternative materials to mitigate these challenges.

RESEARCH AND DEVELOPMENT

Ongoing research and development efforts focus on enhancing the efficiency, sustainability, and cost-effectiveness of such solutions. Innovations include the development of advanced insulation materials, smart packaging technologies, and eco-friendly alternatives. Collaborations between industry players and research institutions are pivotal in driving these advancements.

SEGMENTATION ANALYSIS

By Service Type

Refrigerated TransportationDominates due to Rise in the Demand for Pharmaceutical Products

Based on service type, the market is segmented into refrigerated transportation and refrigerated warehousing.

Refrigerated transportation will be the dominant material segment and will experience significant growth during the forecast period, accounting for a 71.66% market share in 2026. The rise in pharmaceutical products requiring controlled temperatures, such as vaccines, biologics, and specialty drugs has driven the demand for refrigerated transport. These products are highly sensitive to temperature fluctuations and can lose their effectiveness if exposed to inappropriate conditions. The need to ensure that these products remain effective from manufacturing to final delivery has made refrigerated transport indispensable in the pharmaceutical industry.

Refrigerated warehousing is the second-dominating service type segment. Consumers increasingly demand fresh and minimally processed foods, driving growth in the fresh and frozen food sector.

By Temperature Range

Increasing Usage of Frozen Range in Food Sector Contribute to the Segment’s Growth

Based on temperature range, the market is segmented into chilled [8°C to 0°C], frozen [0°C to -25°C], and deep frozen [Below -25°C]. Frozen [0°C to -25°C] is the dominating temperature range.

The frozen temperature range (0°C to −25°C) will dominate the market, as the frozen food industry will expand rapidly due to the growing preference for convenient, ready-to-eat meals and frozen produce, accounting for a 43.83% market share in 2026. Consumers, especially in urban areas, demand high-quality products that can be stored for extended periods without compromising freshness. Frozen packaging solutions are essential for maintaining product integrity during transportation and storage, supporting this growing demand.

Chilled [8°C to 0°C] is the second-dominating segment. The globalization of trade in perishable goods, such as seafood, meat, and frozen vegetables, has increased the need for reliable cold chain logistics.

By Product Type

Growing Demand from Food & Pharmaceutical Companies Contributes to the Segment’s Growth of Pallet Shippers

Based on product type, the market is segmented into EPS containers, PUR containers, pallet shippers, vacuum insulated panels, and others.

The Pallet shippers segment is projected to dominate the market with a share of 34.59% in 2026. Pallet shippers are designed for large-scale transportation, allowing companies to move bulk quantities of products efficiently. They maximize the use of available storage space in trucks, air cargo, or shipping containers, reducing overall logistics costs. This feature is particularly beneficial for pharmaceutical companies and food distributors dealing with high-volume shipments.

EPS Containers are the second-dominating segment. These insulated containers are ideal for transporting bulk quantities of temperature-sensitive products such as pharmaceuticals, biologics, and perishable food items, making them a preferred choice in industries with strict temperature requirements.

By End-use Industry

Augmenting Demand from the Food Sector Propels Segmental Growth

Based on end use, the market is segmented into pharmaceuticals, food, and industrial.

The rising global demand for perishable products including fresh produce, dairy, seafood, frozen foods, and meat drives the food industry’s dominance in the market. Consumers increasingly prioritize freshness, nutritional value, and food quality, making temperature control essential throughout the supply chain. Cold chain packaging will ensure these products remain fresh and free from spoilage during transportation and storage, with the food end-use industry accounting for a 56.62% market share in 2026.

Pharmaceuticals are the second-leading end-use segment. The pharmaceutical industry also significantly contributes to the market growth, driven by the demand for biologics, vaccines, and other temperature-sensitive drugs.

To know how our report can help streamline your business, Speak to Analyst

COLD PACKAGING MARKET REGIONAL OUTLOOK

The market has been studied geographically across five main regions: North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Europe

Europe Cold Chain Packaging Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Growing Demand from Personal Care and Cosmetic Sector Enhance Europe’s Market Growth

Europe contributed approximately USD 10.4 billion to the global market in 2025, accounting for 33.68% share, and is expected to reach USD 11.47 billion in 2026. The European market is witnessing rising demand for biologics, vaccines, and other temperature-sensitive pharmaceuticals, driving the need for reliable cold chain solutions. Additionally, the region’s proximity to emerging markets increases the demand for temperature-controlled transportation of perishable goods, with the Europe market valued at USD 10.4 billion in 2025. The UK market is projected to reach USD 1.9 Billion by 2026, while the Germany market is projected to reach USD 2.72 Billion by 2026.

- According to Cosmetics Europe, the personal care association, Europe is a global leader in the personal care market, with retail sales of cosmetics and personal care products is valued at USD 103 billion in 2023.

North America

Rising Demand for Biologics Drives the Growth of the Market in North America

The market in North America reached USD 6.83 billion in 2025, representing 22.11% of total market revenue, and is projected to reach USD 7.23 billion in 2026. The pharmaceutical industry in North America plays a significant role in driving the market, driven by the demand for biologics, vaccines, and other temperature-sensitive drugs. The COVID-19 pandemic emphasized the critical need for cold chain solutions, especially for vaccine distribution, further driving growth in the market. The U.S. market is projected to reach USD 7.23 Billion by 2026.

- According to the European Federation of Pharmaceutical Industries and Association, in 2021, North America accounted for 49.1% of global pharmaceutical sales, with 64.4% of new medicines launched in the U.S. between 2016-2021.

Asia Pacific

Rapidly Expanding E-commerce Industry Cushions the Market Growth in Asia Pacific

In 2025, the Asia Pacific market stood at USD 9.36 billion, representing 30.32% of global demand, and is projected to grow to USD 10.55 billion in 2026. The Asia Pacific region is witnessing rapid growth, driven by the increasing demand for perishable goods, expanding e-commerce, and improving cold chain infrastructure, particularly in emerging economies. The Japan market is projected to reach USD 2.71 Billion by 2026, the China market is projected to reach USD 3.46 Billion by 2026, and the India market is projected to reach USD 2.02 Billion by 2026.

- According to the Department of Pharmaceuticals, the Indian pharmaceutical industry ranks third globally in pharmaceutical production by volume. From FY18 to FY23, the Indian pharmaceutical industry recorded a growth rate of 6-8%, which was majorly driven by an 8% increase in exports.

Latin America

Surge in Demand for Perishable Food Products Encourages Market Growth

The Latin America market accounted for USD 3.27 billion in 2025, representing 10.60% of the global industry, and is expected to reach USD 3.65 billion in 2026. The market in Latin America is growing steadily, driven by increasing consumer demand for perishable food products, along with improvements in cold chain logistics infrastructure, particularly in Brazil, Mexico, and Argentina.

- Mexico is one of the top 10 markets globally for personal care and cosmetic products and ranks second for beauty products in Latin America, behind only Brazil. According to the U.S. Department of Commerce’s International Trade Administration (ITA), Mexico imported USD 1.4 billion worth of cosmetics and personal care products in 2022.

Middle East & Africa

Rising Adoption in Food & Pharmaceutical Sector Propels Market Growth in the Middle East & Africa Region

Middle East & Africa maintained a strong presence in the global market, reaching USD 1.02 billion in 2025, accounting for 3.29% share, and is expected to reach USD 1.1 billion in 2026. The Middle East & Africa (MEA) region presents significant opportunities for the market, especially in the food and beverage and pharmaceutical sectors. However, limited infrastructure in certain regions, particularly in Africa, slows adoption.

- According to the Gulf Petrochemicals and Chemicals Association, the chemical industry in the GCC (Gulf Cooperation Council) generated USD 107.8 billion in revenue in 2022, further contributing 5% to the region's GDP and 39% to its manufacturing GDP.

FUTURE OUTLOOK

The cold chain packaging market is poised for robust growth, driven by technological advancements, increasing demand for temperature-sensitive products, and a heightened focus on sustainability. Companies that embrace innovation and adapt to evolving regulatory landscapes are likely to gain a competitive edge in this dynamic market.

It plays a vital role in ensuring the integrity of temperature-sensitive products across various industries. Staying abreast of market trends, challenges, and opportunities is essential for stakeholders aiming to thrive in this evolving landscape.

Competitive Landscape

KEY INDUSTRY PLAYERS

Key Market Participants Are Launching New Products to Expand their Customer Base

The global cold chain packaging market is highly fragmented and competitive, with a few key players are dominating the market by offering innovative packaging solutions. These major market players constantly focus on expanding their customer base across regions by innovating their existing wide range of products. The report highlights the recent developments by the manufacturers.

Major players in the industry include Sancell, Sonoco ThermoSafe, Polar Tech Industries Inc., Cold Chain Technologies, Peli BioThermal, and Orora Group. Other companies are also working on delivering advanced packaging solutions to meet the evolving needs of the industry.

Some of the Key Companies Profiled in the Report:

- Sancell (Australia)

- Sonoco ThermoSafe (U.S.)

- Polar Tech Industries Inc. (U.S.)

- Cold Chain Technologies (U.S.)

- Peli BioThermal (U.S.)

- Orora Group (Australia)

- CREOPACK (Canada)

- Sofrigam (France)

- Intelsius (U.K.)

- Nordic Cold Chain Solutions (U.S.)

- Tempack (Spain)

- Cryopak (U.S.)

- Softbox Systems (U.K.)

- Sealed Air Corporation (U.S.)

- Orion Plastics Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- October 2023 – Cold Chain Technologies announced the acquisition of Exeltainer, SL, an international provider of isothermal packaging solutions for the pharmaceutical industry; with its manufacturing plants in Spain and Brazil.

- April 2023 – Mettcover Global opened a new warehouse in Pennsylvania, U.S., strategically located to store and distribute thermal covers and data loggers to clients across the U.S.

- February 2023 – Peli BioThermal released a new cargo shipper, Crēdo™ Cargo bulk shippers to simplify global logistics challenges.

- October 2022 – ECEPLAST formed a joint venture company, CargoCLIMA BV, with VacQPack in Holland as part of its new strategic plan. The company focused on the modified atmosphere packaging and liner bags to prevent food loss.

- September 2022 – Ecocool developed a new high-performance thermal hood ECO-XTREME, in the pharmaceutical sector. The innovative system consists of a highly insulating hood - partly made of recycled material - combined with a blanket made of gel-filled pillows.

INVESTMENT ANALYSIS AND OPPORTUNITIES

In October 2023, Sonoco ThermoSafe announced an expansion of its operations to better serve customers across the U.S. and around the globe. With a strong commitment to efficiency, quality, and customer satisfaction, Sonoco ThermoSafe is investing in cutting-edge machinery, automation, and improved production capabilities.

The new investments would empower the company to effectively meet the evolving needs of its clientele, especially as they diversify their packaging solutions with sustainability goals.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

The market research report provides a detailed market analysis. It covers key aspects, such as top key players, competitive landscape, service types, market segments, Porter’s five forces analysis, and market segments. Besides, the report highlights current market trends and key industry developments. In addition to the abovementioned factors, the report encompasses several factors that have contributed to the market growth in recent years.

Report Scope and Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 11.46% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Service Type

|

|

By Temperature Range

|

|

|

By Product Type

|

|

|

By End-use Industry

|

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was USD 30.88 billion in 2025.

The market is likely to grow at a CAGR of 11.46% over the forecast period.

Pallet shippers product type segment is expected to dominate the market in the forecast period.

The market size of Europe stood at USD 10.4 billion in 2025.

Some of the top players in the market are Sancell, Sonoco ThermoSafe, Polar Tech Industries Inc., Cold Chain Technologies, Peli BioThermal, and Orora Group.

The global market size is expected to reach USD 81.01 billion by 2034.

- 2021-2034

- 2025

- 2021-2024

- 215

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us