Cold Chain Packaging Refrigerants Market Size, Share & Industry Analysis, By Product Type (Gel Packs, Foam Bricks, and Others), By End-use Industry (Pharmaceuticals, Food, and Industrial), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

KEY MARKET INSIGHTS

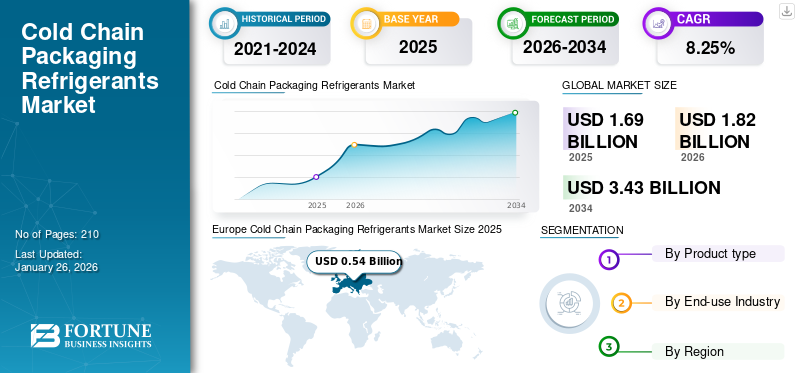

The global cold chain packaging refrigerants market size was valued at USD 1.69 billion in 2025. It is projected to be worth USD 1.82 billion in 2026 and reach USD 3.43 billion by 2034, exhibiting a CAGR of 8.25% during the forecast period. Europe dominated the cold chain packaging refrigerants market with a market share of 32.06% in 2025.

Cold chain packaging refrigerants are used inside passive cold chain packaging containers, such as Polyurethane (PUR) boxes to keep the temperature inside the box regulated. These refrigerants are significantly used in cold chain packaging to protect the temperature of sensitive products, such as vaccines, drugs, and others. These refrigerants allow users to effectively reduce their operational costs without compromising on the quality of the products kept inside the containers.

Product innovation has been a key factor in the growth of the market in recent years; the cold chain packaging refrigerants market’s growth is expected to remain steady in the future. Key players are focused on developing sustainable refrigerant products and customized solutions for customers as per their requirement. For instance, Cold Chain Technologies offers Koolit gel pack refrigerants based on standard designs and customized solutions. Besides, it also offers gel in various materials, such as puncture-resistant nylon laminate film, polyethylene pouch, and spun-woven material backed by polyethylene film.

Download Free sample to learn more about this report.

COLD CHAIN PACKAGING REFRIGERANTS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 1.69 billion

- 2026 Market Size: USD 1.82 billion

- 2034 Forecast Market Size: USD 3.43 billion

- CAGR: 8.25% from 2026–2034

- Europe dominated the cold chain packaging refrigerants market with a market share of 32.06% in 2025.

- Gel packs is estimated to hold the largest market with a share of 44.50% in 2026.

- The food segment will accounts for the largest global cold chain packaging refrigerants market contributing 54.93% globally in 2026.

North America

North America contributed approximately USD 0.37 billion to the global market in 2025, accounting for 22.22% share, and is expected to reach USD 0.39 billion in 2026.

Europe

In 2025, the Europe market stood at USD 0.54 billion, representing 32.06% of global demand, and is projected to grow to USD 0.58 billion in 2026.

Asia Pacific

The Asia Pacific region captured 31.17% of the global market in 2025, generating USD 0.53 billion in revenue, and is projected to reach USD 0.58 billion in 2026.

U.S.

The U.S. market is projected to reach USD 0.34 billion by 2026.

Japan

The Japan market is projected to reach USD 0.1 billion by 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Need for Cold Chain Packaging in Pharmaceutical Industry to Preserve Temperature-Sensitive Products Will Drive Market Growth

Cold chain packaging products are used in significant quantities in the pharmaceutical industry for packaging pharmaceutical ingredients and products that are highly temperature-sensitive. The drug or product may lose its properties or even degrade in quality when exposed to relatively high temperatures. Thus, these products require specialized temperature-cooled packaging and transportation systems to ensure that their chemical and functional value is preserved.

As per IQVIA’s Pharmaceutical Commerce Analysis, 2018, cold chain logistics (including products and transportation) accounts for around 18% of the total pharmaceutical spending. Also, the popularity of cold chain solutions is growing at twice the speed than that of non-cold chain solutions in the pharmaceutical industry. Owing to different advantages, the adoption rate of cold chain packaging is high in this industry globally, which suggests strong growth in demand for cold packaging refrigerants in the coming years.

Increasing Dependency of Food Industry on Cold Chain Packaging to Drive Market Growth

Similar to pharmaceutical products, some of the food products are temperature-sensitive. Food products experience degradation when exposed to high temperatures. Thus, processed and unprocessed food needs to be transported in temperature-controlled vehicles and packaging over long distances to ensure their quality in the end market.

As per the United Nations, the world population is expected to reach 9.7 billion in 2050. The strain on food resources, which is already high, needs to be addressed to support the needs of an increasing population. Cold chain packaging refrigerants play a pivotal role in securing the quality of the food that is being transported over long distances. The adoption of these products plays an extremely important role in fulfilling the need for sustainable food packaging solutions from food processing industries. Food wastage incurs huge losses for companies. Cold chain packaging solutions help retain food quality, which in turn, increases the food safety and profit margins of the manufacturers.

MARKET RESTRAINTS

High Cost and Rising Environmental Issues to Confine Market Growth

Cold chain packaging refrigerants are relatively costly compared to non-cold chain packaging products due to the fact that these solutions are specially tailored to regulate and maintain the temperature around them to keep the product encapsulated in the best quality. A lot of money is invested in designing these products, along with other systems, such as refrigerators, sensors, monitoring devices, and others that work simultaneously to achieve the desired temperature. This results in low adoption of cold packaging solutions across industries.

Moreover, rising environmental concerns due to the extensive use of packaging materials are restraining the growth of the market. As a result, the high cost of innovative cold packaging solutions restricts their adoption in the developing markets and industries.

MARKET OPPORTUNITIES

Development of Eco-friendly Cold Chain Packaging Solutions Will Open New Avenues of Market Growth

Owing to the strict environmental regulations and commitment toward sustainability goals, the need to develop eco-friendly packaging solutions is increasing. Companies are investing heavily in research & development activities to develop such innovative solutions. For instance, Nordic Cold Chain Solutions introduced the world’s first drain-friendly gel packs that are either completely reusable or disposable at the discretion of the recipient in the cold chain industry.

Innovation drives the development of such products, opening new avenues of growth for the cold chain packaging refrigerants market. Also, with change in the mode of transportation, the regulations on the use of permissible materials have changed. Thus, as customers change their transportation modes for the delivery of particular products, the cost of new cold packaging products needs to be optimized so that it does not affect the manufacturer’s operating profit. As a result, the development of universal solutions or standardized cost-effective solutions can accelerate the growth of the market in the coming years.

MARKET CHALLENGES

Advanced Refrigerant Costs and Regulations Hinder Small Businesses in Developing Areas

The elevated expenses linked to advanced refrigerant technologies create an obstacle, especially for small and medium-sized businesses in developing areas, where financial limitations restrict access to cutting-edge solutions. Moreover, the ecological effects of conventional refrigerants such as hydrofluorocarbons (HFCs) have resulted in strict regulations designed to limit their use, making compliance challenging for producers. Moreover, ensuring temperature consistency across the supply chain is challenging; any interruption may lead to product degradation and monetary losses, which discourages the use of advanced refrigerant technologies.

Cold Chain Packaging Refrigerants Market Trends

Reusable Cold Chain Delivery Bins are Increasing Due to Sustainability Goals and Supportive Regulations

Reusable cold chain parcels and pallet delivery bins are being increasingly used every year, thereby assisting pharmaceutical manufacturing companies in transporting high-value products to major markets across the world. According to Pelican’s 2020 Biopharma Cold Chain Logistics Sustainability Survey, around 38% of biopharma companies had used reusable rental containers, while 25% explored them in 2019. The survey also reveals that the availability of rental programs and the growth of network stations across the world to renovate the reusable shipping containers has also increased customers’ access to this affordable and flexible alternative.

Companies are focusing on the development of eco-friendly cold packaging products that will allow consumers, such as pharma companies, to reduce their carbon footprint and meet their sustainability goals to comply with the governing regulations. For instance, the UN, in its study for SDG Industry Matrix, Healthcare & Life Sciences, May 2017, insisted on generating less waste for pharma and healthcare organizations. The UN’s SDG 12 emphasizes sustainable consumption and production, which calls for organizations, including those in life sciences, to develop and implement improved processes to reduce, reuse, and recycle packaging.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Product Type

Gel Packs Provide Insulation, Reducing Dry Ice Usage in Cold Chain Packaging

Based on product type, the market is segmented into gel packs, foam bricks, and others. Gel packs is estimated to hold the largest market with a share of 44.50% in 2026. The gel packs segment dominated the global market with over two-fifths of the market’s share. These packs are effectively used in combination with cold chain packaging containers to keep the contents of the containers in the desired temperature range. Moreover, they can be reused multiple times if proper refrigeration procedures are followed. In long-haul shipping applications, gel packs, when used with Vacuum-Insulated Panels (VIPs), offer extended autonomy.

The foam bricks segment accounted for the second-largest share of the market. They are generally used for lining the container and can withstand extremely cold temperatures in the range of -15°C to -21°C. The use of these bricks significantly reduces the amount of dry ice used in a particular application. Other segments include products, such as phase change materials, mats, and more.

By End-use Industry

Food Segment Dominates Market Due to Increasing Domestic and International Trade

Based on end-use industry, the market is segmented into food, pharmaceuticals, and industrial.

The food segment will accounts for the largest global cold chain packaging refrigerants market contributing 54.93% globally in 2026, due to the transportation of large volumes of food across the globe. Frozen meat, vegetables, fruits, fruit pulp, juices, beverages, dairy products, seafood, confectionery, and other agricultural produce are transported using cold chain packaging solutions. Owing to the increasing domestic and international trade of food products, this segment is expected to lead the market over the forecast period.

The pharmaceutical segment accounted for more than one-fourth of the global market value in 2024. It is the fastest-growing segment in the market owing to the increasing trade of medicines, vaccines, and other medical products. Pharmaceutical companies are investing heavily in cold packaging solutions, and in 2024, it is estimated that biopharma companies spent around USD 15 billion on cold chain logistics alone. This spending is increasing gradually every year at a healthy rate.

To know how our report can help streamline your business, Speak to Analyst

COLD CHAIN PACKAGING REFRIGERANTS MARKET REGIONAL OUTLOOK

The market has been studied geographically across five main regions: North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America Leads Market With Well-Established Technology & Knowledge Base and Strong Focus on Sustainability and Innovation

North America contributed approximately USD 0.37 billion to the global market in 2025, accounting for 22.22% share, and is expected to reach USD 0.39 billion in 2026. North America is one of the largest producers and consumers of cold packaging in the world. It accounts for the second-largest share of the global market. The U.S. dominates the regional market due to its technological advancements and well-established supply chain. The country’s large area and uneven population distribution make the usage of cold packaging even more profound to transport food and pharmaceutical products to remote locations.

Companies in North America are well equipped with technical teams and expertise that drive the cold packaging industry in the region toward innovation. The innovative products have benefited end-use industries in the region, especially the pharmaceutical and healthcare industries, by helping them achieve their sustainability goals and make significant cost savings. Moreover, products, such as frozen ready-to-eat meals are quite popular in the region, which will drive the market. The USDA has set standards for the safe handling of food products, which includes requirements for cold chain logistics to prevent spoilage and contamination. The U.S. market is projected to reach USD 0.34 billion by 2026.

European Market Thrives Due to Temperature Variations, With Germany Leading in Food Exports and GDP Contributions

Europe Cold Chain Packaging Refrigerants Market Size 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, the Europe market stood at USD 0.54 billion, representing 32.06% of global demand, and is projected to grow to USD 0.58 billion in 2026. The European cold packaging refrigerants market is dominated by Germany, France, the U.K., Italy and Spain. The temperature profile changes drastically for each country in Europe, and thus, advanced temperature monitoring and packaging solutions are employed to transport temperature-sensitive products. These countries are expected to provide more growth opportunities compared to Western Europe due to developments and expansion of economies.

Almost one-third of the packaged food & beverage products produced in Germany are exported to other nations across the globe. Food & beverage is the fourth-largest sector in the country, contributing to its GDP growth. As per GTAI, in Germany, the largest industry segments by production value are meat & sausage products (24%), dairy products (15%), baked goods (10%), and confectionary (8%). The UK market is projected to reach USD 0.07 billion by 2026, and the Germany market is projected to reach USD 0.13 billion by 2026.

Asia Pacific Market Grows Rapidly, Driven by Cold Packaging Demand, Rising Income, and Population

The Asia Pacific region captured 31.17% of the global market in 2025, generating USD 0.53 billion in revenue, and is projected to reach USD 0.58 billion in 2026. Asia Pacific is the fastest-growing region in the global market, and is expected to dominate by the end of the forecast period. The adoption of cold packaging is increasing at a healthy rate in the region owing to the rapid development of cold storage projects, rising disposable income, and expanding population. China, Japan, and South Korea account for a large share of the market as these countries have well-established supply chains and companies that provide a wide range of cold packaging products. The region exports large amounts of pharma and agricultural products to North America, Europe, and the rest of the world. However, the trade war between the U.S. and China has discouraged imports and exports to a certain extent. The development of a local supply chain is the only effective way for the long term generation of business in the region. Emerging countries, such as India, Indonesia, Bangladesh, and others are lucrative markets. India dominates the world in terms of the production of vaccines. It is estimated that around 60% of the vaccines are produced in India. The COVID-19 vaccines were also produced on a large scale in India, and their transportation across the globe increased the need for high quantities of cold packaging solutions.

The Japan market is projected to reach USD 0.1 billion by 2026, the China market is projected to reach USD 0.2 billion by 2026, and the India market is projected to reach USD 0.14 billion by 2026.

Road Transportation Dominates Cold Packaging In Latin America

Latin America recorded a market size of USD 0.18 billion in 2025, capturing 10.83% of the global market share, and is projected to reach USD 0.2 billion in 2026. Road transportation is the dominant way of transport in the region for the cold packaging business. Building a strong supply chain has always been the aim of major players in the region as it is divided into many countries, which makes the supply chain complex. The cost of transportation increases rapidly from country to country. For instance, in Argentina, it costs 18% more to move a 20-foot ocean container from Rosario to Buenos Aires than from Hong Kong to Buenos Aires, as per analysis by industry experts.

Mexico has been a lucrative market. The U.S.–Mexico–Canada Agreement (USMCA) was signed to cover issues including, enforcement, labor, environment, and access to medicines, and significant progress has been made under the agreement. However, Latin America lacks infrastructure, which can confine the regional market’s growth.

Middle East & Africa's Cold Packaging Refrigerants Market is Driven by High-Income GCC Countries with Superior Medical Infrastructure

In 2025, Middle East & Africa generated USD 0.06 billion, contributing 3.72% to global market revenue, and is projected to grow to USD 0.07 billion in 2026. GCC countries are major consumers of cold chain packaging refrigerants due to their infrastructure and high-income businesses. Also, these countries have some of the best medical infrastructures in the world, which makes the use of cold packaging more critical in the pharmaceutical industry due to regional temperature profiles. The food industry dominates the demand for cold packaging in the region. Large quantities of cold packaging refrigerants are used to protect vegetables, fruits, and other agricultural produce.

In Africa, leading cold chain associations, such as the Global Cold Chain Alliance are working with local manufacturers to develop and strengthen cold chain logistics. In August 2020, the Global Cold Chain Alliance’s South African office successfully hosted a virtual cold store operations short course with students from South Africa, Ghana, Namibia, Kenya, and Nigeria participating in the same. Such initiatives are projected to create potential demand for cold chain packaging in developing countries of Africa during the forecast period. Africa is one of the leading exporters of agricultural produce to many countries around the world. Therefore, with the rapid adoption of the latest logistics technologies, the demand for cold chain packaging is increasing in the region. Owing to the well-developed pharmaceutical and food sectors, South Africa is a key market for cold chain packaging. However, the cold chain network is undeveloped in many African countries, which represents a key challenge in the cold chain packaging refrigerants market growth.

FUTURE OUTLOOK & INVESTMENTS

The 260,000 sq. ft. temperature-controlled facility at Mehsana will attract over USD 1,130 million investment and be used to store frozen processed food items. Maersk’s new Cold Store facility will be constructed close to the customer’s manufacturing facility and serve as the mother Cold Store facility. The 14,700-pallet position facility will be built at the Fanidhar Mega Food Park and will be one of India’s largest single-shed cold stores. The large facility will help the customer store all the cargo in a single facility instead of multiple smaller facilities before dispatch.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Market Participants to Witness Significant Growth Opportunities with New Product Launches

The global market for cold packaging refrigerants is highly fragmented and competitive. A few significant players are dominating the market by offering innovative packaging solutions in the packaging industry. These players are focusing on expanding their customer base across regions by innovating their existing range of products. The report also highlights the key market developments.

Major players in the industry include Cold Chain Technologies, Blowkings, Sonoco Thermosafe, THERMOCON, Sofrigam, Creative Packaging Company, and others. Numerous other companies operating in the market are focused on delivering advanced packaging solutions.

List of Key Cold Chain Packaging Refrigerants Companies Profiled:

- Cold Chain Technologies (U.S.)

- Blowkings (India)

- Sonoco Thermosafe (U.S.)

- THERMOCON (Germany)

- Sofrigam (France)

- Creative Packaging Company (U.S.)

- Nordic Cold Chain Solutions (U.S.)

- Tempack (Spain)

- Cryopak (U.S.)

- Coolways (Netherlands)

- Pelton Shepherd Industries (U.S.)

- Cryolux America (U.S.)

- The Pack Corporation (Japan)

- Sancell (Australia)

KEY INDUSTRY DEVELOPMENTS:

- October 2023 – Cold Chain Technologies announced the acquisition of Exeltainer, SL, an international provider of isothermal packaging solutions for the pharmaceutical industry with its manufacturing plants in Spain and Brazil.

- April 2023 – Mettcover Global opened a new warehouse in Pennsylvania, U.S. The storage facility is strategically located in Free Port, Pennsylvania. The facility will enable Mettcover to store and distribute thermal covers and data loggers to clients across the U.S.

- February 2023 – Peli BioThermal released a new cargo shipper, Crēdo™ Cargo bulk shippers, to simplify global logistics challenges.

- October 2022 – ECEPLAST, according to its new strategic development plan, started a joint venture company, CargoCLIMA BV, with VacQPack in Holland. The new company will be focusing on modified atmosphere packaging and use ECEPLAST’s liner bags to prevent food loss.

- September 2022 – Ecocool developed a completely new product category in the pharmaceutical segment with the new high-performance thermal hood ECO-XTREME. The system consists of a highly insulating hood - partly made of recycled material - combined with a blanket made of gel-filled pillows.

REPORT COVERAGE

The report provides a detailed market analysis and also focuses on key aspects, such as top players, competitive landscape, product types, market segments, Porter’s five forces analysis, and leading segments of the product. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the abovementioned factors, the report encompasses several factors that have contributed to the market’s growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.25% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type · Gel Packs · Foam Bricks · Others |

|

By End-use Industry · Pharmaceuticals · Food · Industrial |

|

|

By Region · North America (By Product Type, End-use Industry, and Country) o U.S. (By End-use Industry) o Canada (By End-use Industry) · Europe (By Product Type, End-use Industry, and Country) o Germany (By End-use Industry) o France (By End-use Industry) o U.K. (By End-use Industry) o Spain (By End-use Industry) o Italy (By End-use Industry) o Russia (By End-use Industry) o Poland (By End-use Industry) o Romania (By End-use Industry) o Rest of Europe (By End-use Industry) · Asia Pacific (By Product Type, End-use Industry, and Country) o China (By End-use Industry) o India (By End-use Industry) o Japan(By End-use Industry) o Australia (By End-use Industry) o Southeast Asia (By End-use Industry) o Rest of Asia Pacific (By End-use Industry) · Latin America (By Product Type, End-use Industry, and Country) o Brazil (By End-use Industry) o Mexico (By End-use Industry) o Argentina (By End-use Industry) o Rest of Latin America (By End-use Industry) · Middle East & Africa (By Product Type, End-use Industry, and Country) o Saudi Arabia (By End-use Industry) o UAE (By End-use Industry) o Oman (By End-use Industry) o South Africa (By End-use Industry) o Rest of the Middle East & Africa (By End-use Industry) |

Frequently Asked Questions

Fortune Business Insights says that the global cold chain packaging refrigerant market size was valued $1.69 billion in 2025 and is expected to grow to $3.43 billion by 2034, with a CAGR of 8.25%.

The market will register a CAGR of 8.25% and exhibit steady growth in the forecast period (2026-2034).

The gel packs segment is expected to lead the market during the forecast period.

The rising demand for biopharmaceutical products is the key factor driving the market.

Cold Chain Technologies, Sonoco Thermosafe, and Nordic Cold Solutions are the leading players in the market.

Europe dominated the global market in terms of share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 210

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us