Pharmaceutical Gelatin Market Size, Share & Industry Analysis, By Source (Bovine, Porcine, Marine, and Others), By Function (Film-forming & Coating Agent, Gelling & Thickening Agent, Stabilizing Agent, and Others), By Application (Hard Capsules, Soft Capsules, Tablets, and Others), By Type (Type A and Type B), By End User (Pharmaceutical Companies, Capsule Manufacturers, CMOs & CDMOs, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

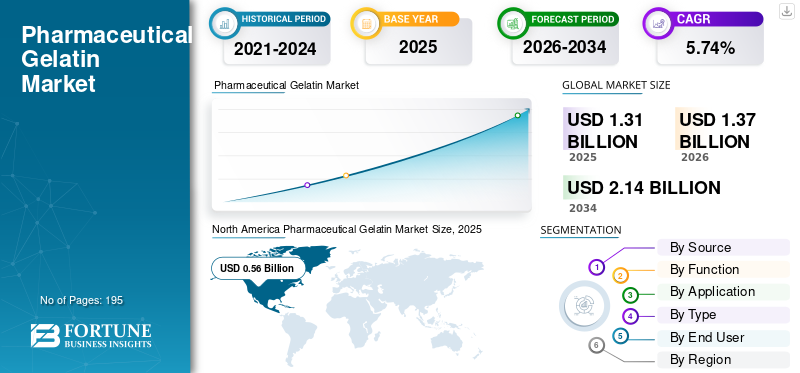

The global pharmaceutical gelatin market size was valued at USD 1.31 billion in 2025. The market is projected to grow from USD 1.37 billion in 2026 to USD 2.14 billion by 2034, exhibiting a CAGR of 5.74% during the forecast period. North America dominated the global market with a market share of 42.75% in 2025.

Pharmaceutical gelatin refers to gelatin that meets stringent purity, microbiological, and endotoxin specifications for use in drug products. It is a specialty segment of the broader gelatin industry that supplies high-purity gelatin for pharmaceutical applications such as hard and soft capsules, tablet coatings, wound dressings, and certain parenteral uses. This market is witnessing a strong growth driven by rising global pharmaceutical production and demand for oral solid dosage forms.

Various key industry players, such as GELITA AG, Darling Ingredients, PB Leiner, and others play an important role in shaping this market. These companies are focusing on innovative product offerings to maintain their market presence.

Download Free sample to learn more about this report.

PHARMACEUTICAL GENATIN MARKET TRENDS

Growing Demand for Specialty, Low-endotoxin, and Traceable Gelatins is a Significant Trend Observed in Market

Specialty, low-endotoxin, and fully traceable gelatins are gaining demand as pharma and biomedical developers tighten controls on bioburden/endotoxins, especially for implants, hemostats, wound care materials, drug-delivery matrices, and sensitive formulations where inflammatory risk and batch variability matter. This trend is also tied to quality-by-design in excipients as suppliers are differentiating with endotoxin-controlled grades and application-specific portfolios rather than one-size-fits-all gelatin. These factors are supporting the overall global market growth.

- For instance, in March 2024, Rousselot (Darling Ingredients) announced online access to its research- and technical-grade gelatins through BIO INX in multiple regions.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Global Pharmaceutical Production and Demand for Oral Solid Dosage Forms is Propelling Market Growth

Rising global pharmaceutical production and demand for oral solid dosage forms is prominently driving the global pharmaceutical gelatin market growth as these formats remain the pillar for high-volume prescription drugs, OTC products, and supplements. As pharmaceutical output expands, manufacturers scale solid-dose manufacturing and encapsulation, increasing consumption of pharma-grade gelatin used in hard gelatin capsules and in certain coating/binding applications. Moreover, oral formats are favored as they are cost-efficient, scalable, and patient-friendly, which keeps capsules/tablets central as treatment volumes rise across chronic diseases and aging populations. All these factors cumulatively drive the overall market growth.

- For instance, in December 2024, Lonza announced capacity expansions at its sites in Rewari (India) and Suzhou (China), including additional Hard Gelatin Capsule (HGC) lines to meet growing regional demand.

MARKET RESTRAINTS

Dependence on Animal-Sourced Raw Materials to Limit Market Growth

Pharmaceutical gelatin depends heavily on animal by-products (mainly porcine/bovine skins and bones), so supply is associated to livestock availability, slaughter volumes, and meat-processing continuity making the market structurally exposed to upstream shocks. This dependence creates a raw-material volatility risk when animal supply is hampered due to factors such as disease outbreaks, culling, movement controls etc., gelatin producers can face reduced input availability, longer lead times, and higher procurement costs. This results in limiting the market growth to certain extent.

- For instance, in December 2025, Malaysia imposed an immediate ban on most pork and pork-product imports from Spain following an African swine fever (ASF) outbreak

MARKET OPPORTUNITIES

Ongoing R&D into Alternative Capsule Materials to Offer Market Growth Opportunities

R&D into alternative capsule materials such as HPMC, pullulan, and other plant-based polymers is accelerating, creating a lucrative opportunity for the broader capsule supply chain to serve fast-growing demand for vegan/vegetarian, clean-label, allergen-free, and religion-compliant dosage forms. It also enables new product positioning in sensitive formulations (acid-resistant, delayed-release, odor masking), where alternative materials can reduce the need for extra coatings and processing steps driving adoption in nutraceuticals and select pharma use cases. All these factors would drive the market growth in the coming years.

- For instance, in February 2025, ACG announced fully vegan printed capsules made from plant-based polymers (HPMC), positioned as an alternative to traditional gelatin capsules

MARKET CHALLENGES

Stringent Regulatory Requirements for Pharmaceutical-Grade Gelatin Pose a Critical Challenge to Market Growth

Pharmaceutical-grade gelatin faces stringent regulatory scrutiny as it is an animal-derived excipient used directly in dosage forms (especially capsules), so regulators expect tight control of source traceability, viral/TSE risk, impurities, microbiology, and batch consistency. Manufacturers must comply not only with pharmacopoeial standards but also with robust GMP documentation, which increases time, cost, and complexity for product qualification. All the factors cumulatively affect the market growth.

Segmentation Analysis

By Source

Rising Demand for Bovine Sourced Gelatin to Propel Porcine Segmental Growth

Based on the source, the market is divided into bovine, porcine, marine, and others.

The porcine segment is likely to capture the largest global pharmaceutical gelatin market share. This can be attributed to higher acceptance across the globe, robust performance, and strong demand for hard capsule and softgel production. Additionally, advantages offered by porcine gelatin such as broader compatibility, diverse raw material options, and consistent gel strength also boosted the segment growth.

- For instance, companies such as GELITA AG, Darling Ingredients, and others offer porcine sourced gelatin.

The marine segment is anticipated to rise with a CAGR of 8.49% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Function

High Demand for Film-forming & Coating Agents Owing to Usage in Every Production Batch to Boost Segmental Growth

On the basis of function, the market is divided into film-forming & coating agent, gelling & thickening agent, stabilizing agent, and others.

The film-forming & coating agent segment dominated the global market in 2025. Film-forming applications are repeat, high-throughput purchases as capsules/coatings are consumed continuously with every production batch. In addition, manufacturers also prefer gelatin films for swallowability, taste/odor masking, and dose-form protection, which supports broad adoption across the globe. Furthermore, the segment is set to hold 64.5% share in 2026.

- For instance, in January 2025, ACG announced the commencement of operations at its new capsule manufacturing facility in Rayong, Thailand, which is dedicated to producing empty hard gelatin capsules.

The stabilizing agent segment is anticipated to rise with a CAGR of 8.30% over the forecast period.

By Application

Large Base of Hard Gelatin Capsules to Boost Segmental Growth

On the basis of application, the market is divided into hard capsules, soft capsules, tablets, and others.

The hard capsules segment captured the highest share of the global market in 2025. The segment held the largest share as they are one of the most widely used oral solid dosage forms for delivering powders, pellets, and even some non-aqueous/semi-solid fills. This results in very large, repeat-volume consumption of capsule-grade gelatin. Furthermore, the segment is set to hold 48.5% share in 2026.

- For instance, companies such as Darling Ingredients, Lapi Gelatine S.p.A., and others are some of the leading companies offering gelating for hard capsules.

The soft capsules segment is anticipated to rise with a CAGR of 6.94% over the forecast period.

By Type

Faster Production and Wide Usage of Type A Support Segmental Dominance

Based on the type, the market is divided into type A and type B.

The type A segment is expected to account for the largest global market share. Factors supporting the segment dominance include broad availability of type A, faster production, higher preference for capsule applications, and others. Furthermore, the segment is set to hold 60.9% share in 2026.

The type B gelatin segment is anticipated to rise with a CAGR of 6.21% over the forecast period.

By End User

Higher Demand from Pharmaceutical Companies Supported their Leading Position

Based on end user, the market is segmented pharmaceutical companies, capsule manufacturers, CMOs & CDMOs, and others.

The pharmaceutical companies segment captured the dominating position in the global market. These are the primary formulators and producers of finished dosage forms such as capsules, tablets, and soft gels that require high-purity gelatin as a core excipient or shell material. These companies maintain large, continuous production volumes, driving stable, high-volume procurement of gelatin relative to outsourced partners and intermediaries. Furthermore, the segment is set to hold 40.3% share in 2026.

In addition, CMOs & CDMOs are projected to grow at a CAGR of 6.52% during the study period.

Pharmaceutical Gelatin Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Pharmaceutical Gelatin Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America’s market size was USD 0.54 billion in 2024 and captured the dominating position. The region also maintained its dominance in 2025, with USD 0.56 billion. This dominance is supported by high per-capita pharmaceutical consumption and established capsule manufacturing. Moreover, the strong demand for specialty grades and vaccine-grade gelatin in the U.S. supported the country’s market growth.

U.S. Pharmaceutical Gelatin Market

The U.S. market dominated the North American market and is valued approximated at around USD 0.54 billion in 2026, accounting for roughly 39.0% of global market.

Europe

Europe pharmaceutical gelatin market size is projected to witness a CAGR of 5.29% in the coming years. The region is anticipated to become the second highest among all regions. The region would reach a market size of USD 0.34 billion by 2026. The factors such as significant demand for traceability, high-quality grades, and alternative sources due to food-safety regulations and consumer preferences have majorly driven the European market growth.

U.K Pharmaceutical Gelatin Market

The U.K. pharmaceutical gelatin market in 2026 is estimated at around USD 0.06 billion, representing roughly 4.4% of global revenues.

Germany Pharmaceutical Gelatin Market

Germany pharmaceutical gelatin market size is projected to reach approximately USD 0.07 billion in 2026, equivalent to around 5.5% of global sales.

Asia Pacific

Asia Pacific pharmaceutical gelatin market size is projected to be valued at USD 0.29 billion in 2026 and secure the position of the third-largest region in the global industry. This is driven by large pharmaceutical production base along with expanding pharmaceutical and nutraceutical manufacturing.

Japan Pharmaceutical Gelatin Market

The Japan pharmaceutical gelatin market in 2026 is estimated at around USD 0.06 billion, accounting for roughly 4.6% of global revenues.

China Pharmaceutical Gelatin Market

China’s pharmaceutical gelatin market is projected to reach revenues of around USD 0.09 billion in 2026, representing roughly 6.5% of global sales. China is both a major producer and consumer of gelatin raw materials.

India Pharmaceutical Gelatin Market

The India pharmaceutical gelatin market in 2026 is estimated at around USD 0.04 billion, accounting for roughly 3.1% of global revenues.

Latin America and Middle East & Africa

The Latin America and the Middle East and Africa regions would witness a slower growth rate in this near future. The Latin America pharmaceutical gelatin market size is set to reach a valuation of USD 0.08 billion in 2026. These regions show steady adoption, however, the growing demand for capsule production is anticipated to drive the market growth.

GCC Pharmaceutical Gelatin Market

The GCC pharmaceutical gelatin market is projected to reach around USD 0.03 billion in 2026, representing roughly 2.2% of global revenues. This is driven by growing pharmaceutical production in GCC.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Strategic Initiatives by Leading Entities to Strengthen Market Share

The global market for pharmaceutical gelatin shows a fragmented structure due to the presence of several well-established as well as emerging players in the market. Prominent players including GELITA AG, Darling Ingredients, and PB Leiner are anticipated to account for the dominating shares in the global market. This is due to their widespread product portfolios, strong geographic presence, and focus on innovative product launches.

Other key players in the pharmaceutical gelatin market include Olympus Corporation, Barco, EIZO, and others. New product development, collaborations & partnerships, and product enhancements are some of the strategies undertaken by these players to gain market share.

LIST OF KEY PHARMACEUTICAL GELATIN COMPANIES PROFILED

- GELITA AG (Germany)

- Darling Ingredients (U.S.)

- PB Leiner (Belgium)

- Nitta Gelatin, Inc. (Japan)

- Lapi Gelatine S.p.A. (Italy)

- Weishardt (France)

- Sterling Biotech Limited (India)

- EWALD-Gelatine GmbH (Germany)

- Trobas Gelatine B.V. (The Netherlands)

- ITALGEL S.p.A. (Italy)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Darling Ingredients Inc. and Tessenderlo Group signed a definitive agreement to form Nextida, combining the collagen and gelatin segments of their companies.

- November 2025: India Gelatine & Chemicals Ltd announced an expansion project to upgrade the existing plant to increase gelatine capacity from 2,000 MT to up to 2,700 MT.

- September 2025: Rousselot unveiled gelatin prototypes positioned as high-performance biomaterials for medical device development expanding high-purity gelatin use-cases closely tied to pharma-grade specs.

- July 2025: Nitta Gelatin India announced an expansion plan to strengthen its bio-products position.

- June 2025: GELITA showcased its Endotoxin Controlled Excipients (ECE), including MEDELLAPRO (gelatin) and VACCIPRO (collagen peptides) for demanding pharma/biomedical applications.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.74% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Source, Function, Application, Type, End User, and Region |

|

By Source |

· Bovine · Porcine · Marine · Others |

|

By Function |

· Film-forming & Coating Agent · Gelling & Thickening Agent · Stabilizing Agent · Others |

|

By Application |

· Hard Capsules · Soft Capsules · Tablets · Others |

|

By Type |

· Type A · Type B |

|

By End User |

· Pharmaceutical Companies · Capsule Manufacturers · CMOs & CDMOs · Others |

|

By Region |

· North America (By Source, Function, Application, Type, End User, and Country) o U.S. o Canada · Europe (By Source, Function, Application, Type, End User, and Country/Sub-region) o Germany o U.K. o France o Spain o Italy o Scandinavia o Rest of Europe · Asia Pacific (By Source, Function, Application, Type, End User, and Country/Sub-region) o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific · Latin America (By Source, Function, Application, Type, End User, and Country/Sub-region) o Brazil o Mexico o Rest of Latin America · Middle East & Africa (By Source, Function, Application, Type, End User, and Country/Sub-region) o GCC o South Africa o Rest of Middle East & Africa |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1.31 billion in 2025 and is projected to reach USD 2.14 billion by 2034.

In 2025, the market value stood at USD 0.56 billion.

The market is expected to exhibit a CAGR of 5.74% during the forecast period of 2026-2034.

By source, the porcine segment is expected to lead the market.

Rising global pharmaceutical production and demand for oral solid dosage forms is primarily driving market expansion.

GELITA AG, Darling Ingredients, and PB Leiner are some of the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 195

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us